Vance Pulls Out of Iran Talks, Sending Brent Below $80

1 hr ago

The expansion of artificial intelligence is widely perceived as a digital software transition, yet it relies entirely on trillions of dollars currently flowing into heavy physical facilities. As April 2026 draws to a close, financial markets are eagerly anticipating Wednesday after-market financial disclosures from Alphabet, Amazon, Meta, and Microsoft. According to market data, these four hyperscalers account for 18.3 percent of the S&P 500 weighting, and their collective digital hardware demand dictates broader market momentum.

Evaluating AI infrastructure stocks requires looking beyond traditional chipmakers to understand the physical constraints of data processing. This analysis maps the capital flowing into alternative power providers, cooling systems, and traditional utilities that sustain hyper-scale computing. The transition from digital applications to physical utility requires a comprehensive analytical structure to identify the most viable commercial beneficiaries. Tracking this capital rotation provides a clearer view of the technology sector’s actual physical footprint.

Major technology firms are allocating unprecedented capital to build out physical processing facilities in 2026. Alphabet set its capital expenditure guidance between $175 billion and $185 billion, nearly doubling previous annual spending to fund specific hardware expansion. Amazon is projecting a similar trajectory, with expected spending reaching $200 billion to support its hyperscaler capacity demands.

Microsoft reported Q1 2026 capital expenditures of $34.9 billion, implying an annual pace of approximately $140 billion. Half of this allocated capital flows directly into data centre servers, thermal management systems, and related physical facilities. This direct expenditure correlates with the immense commercial momentum seen across hardware manufacturers in early 2026.

Nvidia continues to capture a significant portion of this spending, posting an 85 percent year-to-date gain as it supplies the foundational processing units. Server manufacturer Super Micro Computer is up 120 percent for the year, while liquid cooling specialist Vertiv has gained 65 percent. Investors monitoring these technology allocations can identify the most immediate downstream beneficiaries by tracking where corporate capital intersects with physical limits.

This concentrated AI capital expenditure serves as a major driver for semiconductor stock valuations, rewarding hardware manufacturers who can meet immediate delivery schedules.

| Company | Estimated 2026 CapEx | Q1 2026 Hardware Momentum | Primary Infrastructure Focus |

|---|---|---|---|

| Alphabet | $175B to $185B | N/A (Hyperscaler) | Data centre expansion and custom processing |

| Amazon | $200B | N/A (Hyperscaler) | AWS physical server capacity |

| Microsoft | $140B (Annualised) | N/A (Hyperscaler) | Server hardware and thermal management |

| Nvidia | N/A (Beneficiary) | +85% YTD | Advanced processing semiconductors |

| Super Micro Computer | N/A (Beneficiary) | +120% YTD | High-density server architecture |

| Vertiv | N/A (Beneficiary) | +65% YTD | Liquid cooling systems |

The physical expansion of processing capacity is ultimately bounded by raw electricity generation. Modern data centres require exponentially more power than traditional cloud storage facilities because of advanced power density requirements. Processing complex learning models generates concentrated thermal output that standard air conditioning cannot mitigate.

High-density computing systems mandate liquid cooling and massive electrical capacity to function safely. A recent RAND study highlighted projected United States power capacity shortfalls across 22 specific sites dedicated to these advanced data centres. Both the Brookings Institution and the Milken Institute are currently evaluating the global energy demands of these systems, noting that power grid limitations present a hard ceiling for technology growth.

Energy generation represents the single greatest physical constraint on scaling processing capacity through 2030. Selecting successful software applications yields minimal returns if the underlying physical grid cannot supply their computing demands. The distinction between standard and high-density infrastructure dictates where power is consumed most rapidly.

The EPRI data center grid strain report projects that this rapid adoption of artificial intelligence will force electricity consumption to unprecedented levels, requiring utility providers to drastically upgrade transmission infrastructure.

Traditional cloud infrastructure relies on ambient air cooling and standard power draw designed for simple data retrieval. Modern high-density computing infrastructure requires continuous maximum power draw for complex calculations. * Advanced facilities necessitate specialised liquid cooling systems that consume substantial additional energy to maintain safe operating temperatures.

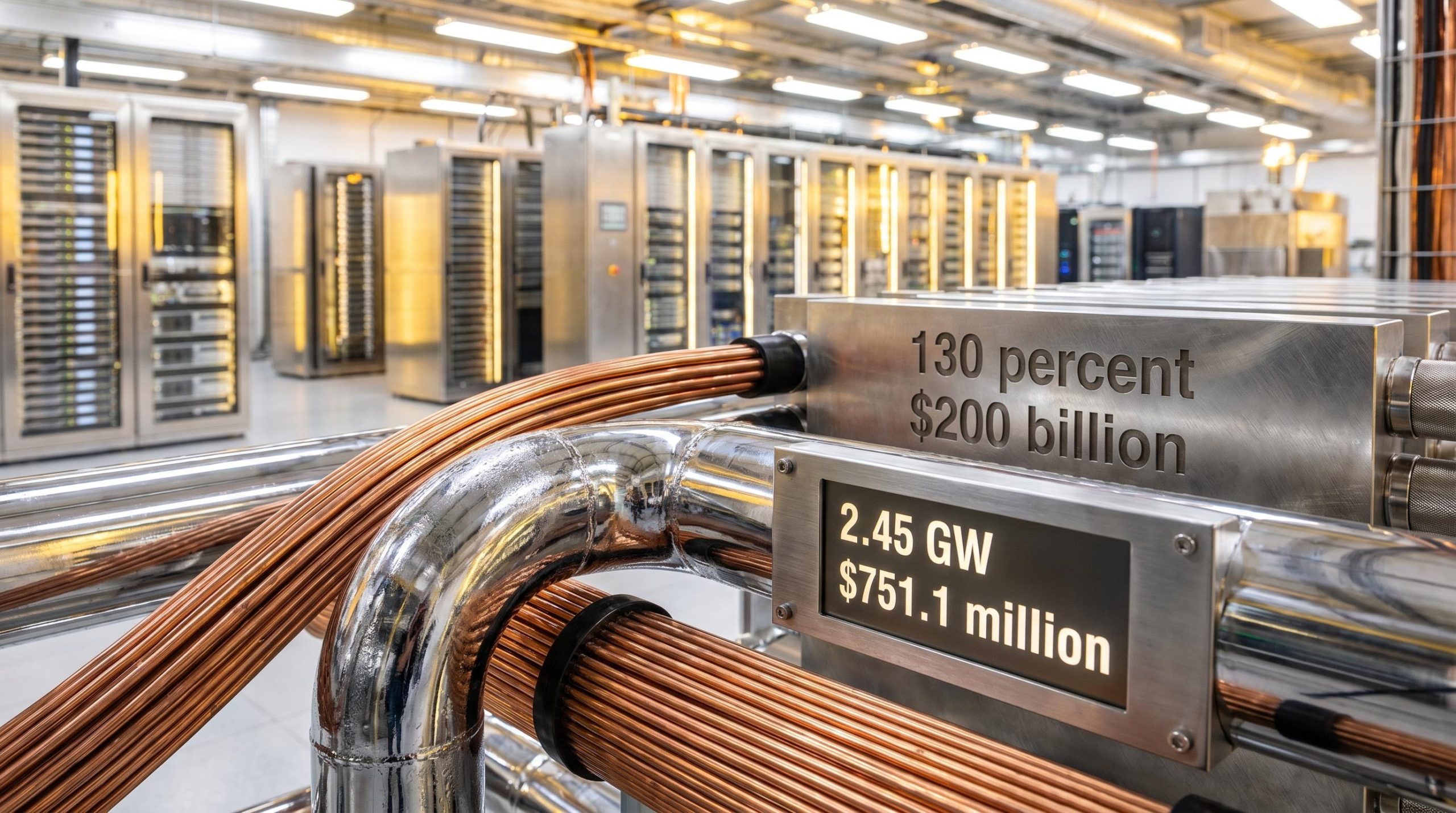

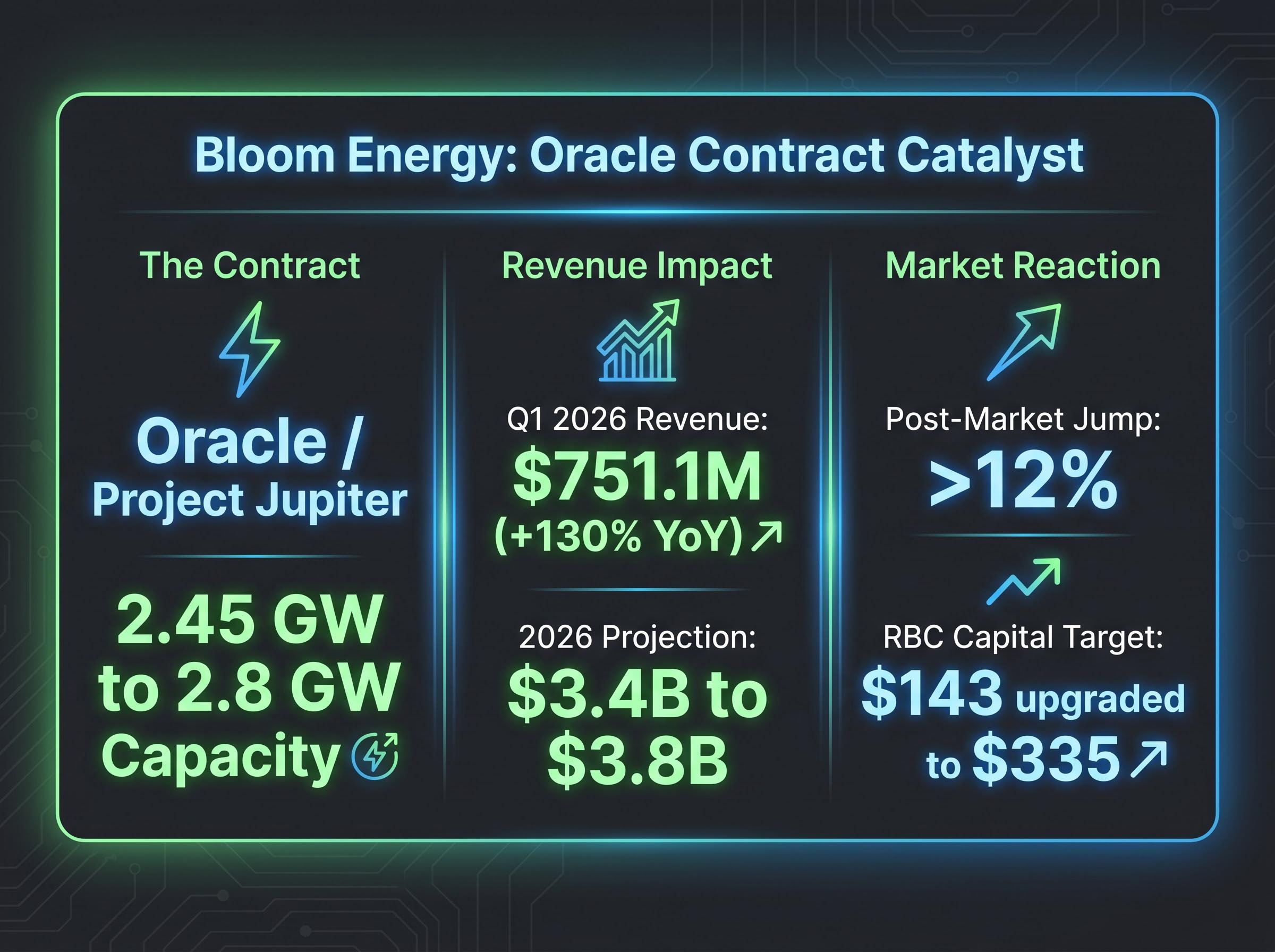

The theoretical constraints of grid capacity are translating into concrete commercial agreements for alternative power providers. Bloom Energy recently secured a major hyperscaler contract with Oracle, known as Project Jupiter, to deploy up to 2.45 GW of fuel cell capacity. Some industry reports suggest the total capacity could reach up to 2.8 GW, validating the capital rotation into alternative energy to solve immediate grid limitations.

The commercial impact of these utility agreements is visible in recent financial disclosures. According to company data, Bloom Energy reported Q1 2026 revenue of $751.1 million, representing an increase of 130 percent year-on-year. According to company data, the company elevated its 2026 revenue projections to span between $3.4 billion and $3.8 billion, underscoring the lucrative nature of hyperscaler utility contracts.

Analyst Upgrade Catalyst Following the Oracle capacity agreement, RBC Capital analysts upgraded Bloom Energy shares, establishing an extreme outlier price target of $335, up from $143, reflecting the sudden market premium placed on immediate energy generation.

Market appetite for infrastructure solutions responded aggressively to the data. According to market data, post-market share prices jumped more than 12 percent following the announcement. Average price targets for the stock now sit between $124 and $156 across the broader analyst consensus.

Investors exploring the alternative utility landscape will find our full explainer on hyperscaler grid bypass strategies, which details how tech companies are securing behind-the-meter generation models to achieve total energy independence.

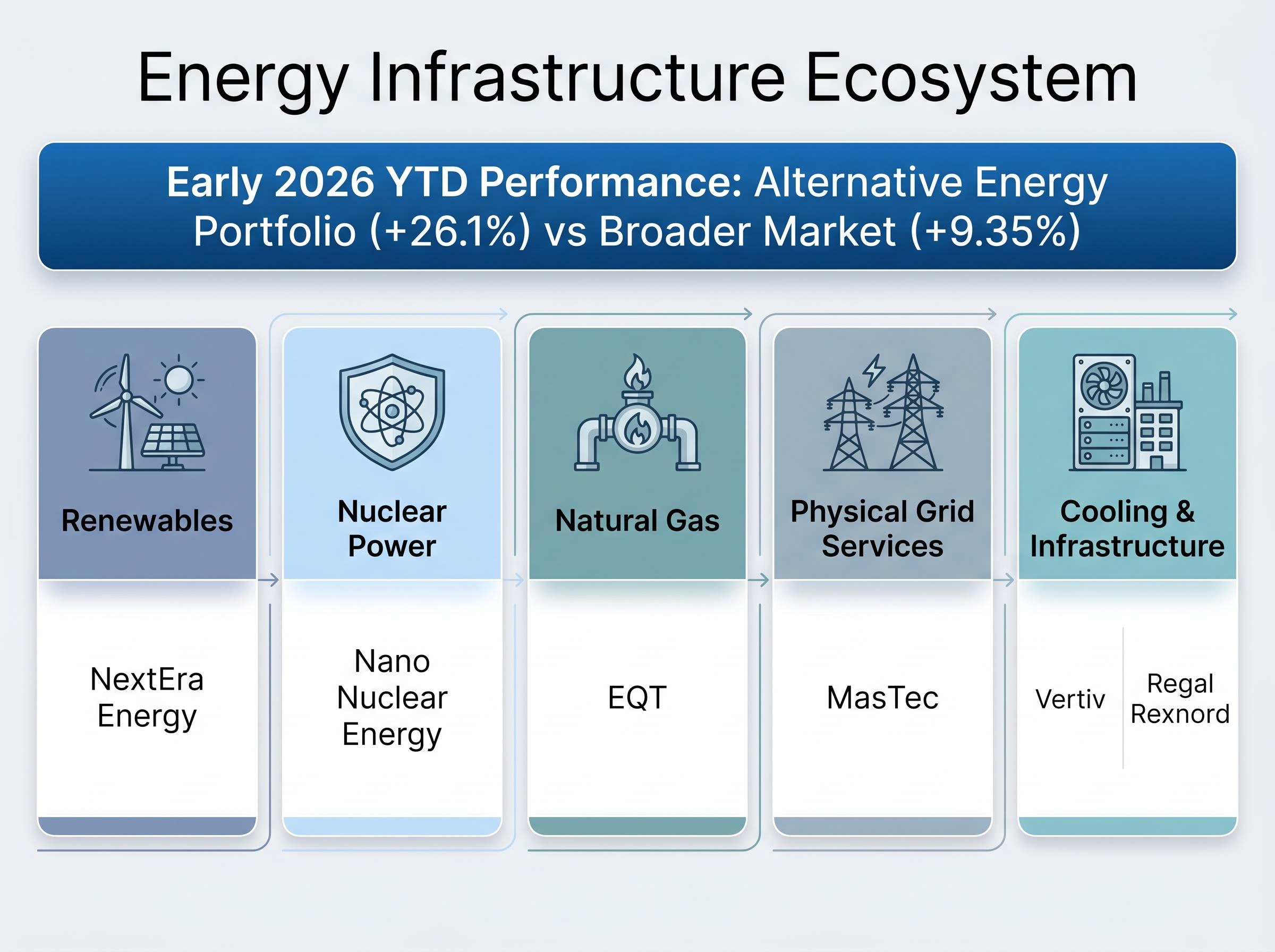

A successful portfolio approach to grid constraints requires looking beyond a single fuel source. Different types of traditional and alternative energy providers are stepping in to fill the expanding power gap. Capitalising on this energy deficit involves categorising the specific sub-sectors benefiting from the physical buildout.

Financial data indicates a broad sector rotation is well underway. According to market reports, a specific alternative energy model portfolio advanced 26.1 percent year-to-date in early 2026, significantly outpacing the broader market index gain of 9.35 percent. Investors are mapping distinct ecosystem participants across multiple energy disciplines to find sustainable momentum stocks.

Companies building the physical transmission lines and thermal management systems are structurally equal in importance to the power generators. Moving electricity from new alternative sources to specific data hubs requires extensive civil engineering and specialised hardware. Commercial cooling and physical infrastructure firms, such as Vertiv and Regal Rexnord, capture substantial upside from this necessary grid enhancement.

Optimism regarding this capital expenditure supercycle must be weighed against hard systemic constraints. The macroeconomic environment presents immediate challenges for infrastructure financing. According to economic reports, current United States baseline interest rates remain stable between 3.50 percent and 3.75 percent, with analysts expecting no monetary easing until late 2027.

The latest Federal Reserve FOMC statement reinforces this restrictive monetary timeline, signaling to markets that borrowing costs for multi-year civil engineering projects will remain elevated for the foreseeable future.

Sustained inflationary pressures and elevated borrowing costs directly affect the viability of massive, multi-year construction projects. Furthermore, specific corporate performance misses threaten the internal capital generation required to fund these ambitions. Reports in early 2026 indicated that OpenAI missed internal user and revenue performance objectives, raising concerns about the sustainability of hyperscaler spending.

Rapid hardware growth also remains vulnerable to global supply chain instability. The ongoing United States government economic blockade against Iran sustains elevated energy costs, further complicating the operational expenses of running advanced computing facilities. Identifying these warning signs protects investors from sudden contractions in technology spending.

According to economic reports, macro financing costs remain elevated due to stable, high interest rates extending through 2027. Corporate revenue misses from major software developers could restrict available capital for future physical expansion. * Geopolitical supply chain disruptions continue to inflate baseline energy and material costs.

The transition from hyperscaler software ambitions to physical hardware constraints dictates the current capital rotation. Evaluating commercial opportunities in the physical buildout space requires monitoring both the technology majors and the utility providers. Wednesday after-market earnings reports from Alphabet, Amazon, Meta, and Microsoft will serve as the ultimate barometer for continued expenditure.

This pivot has already triggered a significant legacy software repricing, pushing capital out of traditional per-user licensing models and into highly efficient synthetic infrastructure platforms.

Market analysts project a $1 trillion broad infrastructure spending opportunity on the horizon as these physical networks scale. Investors can align their portfolios with this long-term energy transition by tracking the companies providing the specific thermal management and electrical generation required. Sustained hardware momentum relies entirely on resolving the immediate electrical capacity deficit.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

AI infrastructure stocks represent companies providing the physical hardware, energy, and cooling systems essential for developing and operating artificial intelligence, shifting focus from software to underlying physical assets.

Companies benefiting include chipmakers like Nvidia, server manufacturers such as Super Micro Computer, cooling specialists like Vertiv, and alternative energy providers like Bloom Energy, alongside traditional utilities and grid service firms.

The primary constraint on AI infrastructure growth through 2030 is the availability of raw electricity generation and the capacity of existing power grids to support high-density computing requirements.

Bloom Energy is capitalizing by securing large hyperscaler contracts, such as Project Jupiter with Oracle, to deploy significant fuel cell capacity for data centers, validating its role in solving immediate grid limitations.

Main headwinds include elevated interest rates projected through 2027, potential corporate revenue misses from major software developers, and ongoing geopolitical supply chain disruptions that inflate energy and material costs.