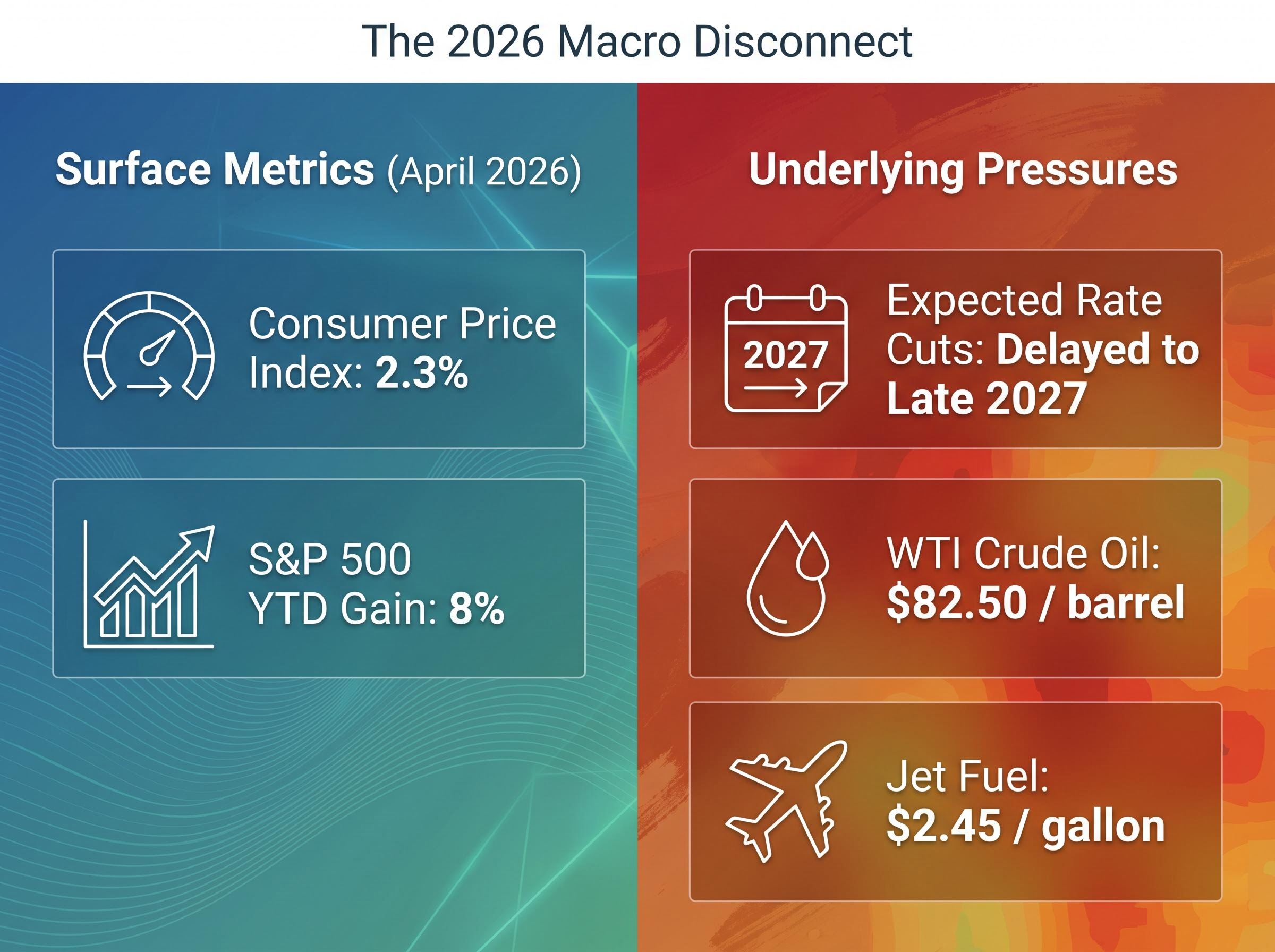

The United States Consumer Price Index sits at a cooling 2.3% in April 2026, yet according to market analysts, equity markets are pricing in a reality where interest rate cuts will not materialise until late 2027. This disconnect between headline disinflation and extended restrictive monetary policy stems from a complex intersection of international conflicts and targeted financial restriction campaigns. These macro headwinds are creating localised pricing pressures that fundamentally complicate central bank calculations.

Navigating the inflation impact on stocks requires investors to look beyond surface-level data to understand how corporate margins are actually absorbing these crosscurrents. The broader market appears stable, but beneath the index level, extreme sector divergence is unfolding.

The current market environment demands a precise analytical framework. Investors must distinguish between companies caught in persistent macroeconomic headwinds and those riding massive secular technology investments.

Geopolitical Tensions and the Energy Market Ripple Effect

The broader stock market presents an optimistic facade, with the S&P 500 posting an 8% year-to-date gain by late April 2026. However, this headline performance obscures the immediate physical reality of global energy markets. The United States administration has escalated its financial restriction campaign against Iran, sending direct structural ripples through global energy pricing.

This geopolitical friction establishes a hard floor under commodity prices. It creates a baseline of persistent costs that directly challenges the broader disinflationary narrative presented by consumer metrics. Market participants must weigh a stabilised broader index against highly volatile commodity inputs that threaten specific corporate profit margins.

Market Analysis “The divergence between a cooling 2.3% consumer price index and stubbornly high industrial inputs reveals a segmented economy, where headline numbers mask the real operational costs eroding profit margins in transport and manufacturing.”

The Commodity Cost Floor

Localised conflicts in the Middle East have effectively placed a permanent premium on global energy transit and supply chain insurance. WTI crude oil is currently trading at $82.50 per barrel, transferring immediate pressure through the industrial complex. Refined products reflect an even sharper operational reality, with Jet fuel priced at $2.45 per gallon.

The EIA Short-Term Energy Outlook projects these wholesale jet fuel prices and crude oil averages will maintain persistent pressure on transportation networks throughout the year, forcing airlines to reconsider their traditional hedging strategies.

These elevated fuel inputs do not stay contained within the energy sector. They transition rapidly through logistics networks, forcing transport providers and consumer goods distributors to either absorb the cost or attempt to pass it forward to consumers.

Investors observing this dynamic must recognise that headline inflation numbers consistently conceal underlying commodity volatility. This specific cost floor can abruptly alter corporate profitability forecasts for the remainder of the year.

When big ASX news breaks, our subscribers know first

The Mechanics of ‘Higher for Longer’ Monetary Policy

The mechanical relationship between these geopolitical shocks and delayed interest rate cuts explains why central bank policy remains highly restrictive. Persistent energy costs force the Federal Reserve into a cautious holding pattern, despite the headline inflation metric cooling to 2.3%. Current benchmark interest rates are held unchanged.

Data from the CME FedWatch Tool indicates that the next reduction in borrowing costs is delayed. This prolonged timeline fundamentally alters the valuation math for equities. When borrowing costs remain elevated for an extended period, equity valuations face mechanical downward pressure through three primary channels:

Recent options pricing from the CME Group FedWatch Tool confirms that traders have aggressively priced out early rate relief, reflecting a growing consensus that baseline financing costs will not normalise until well into 2027.

Discount rate expansion, which heavily reduces the present value of future corporate earnings for growth-oriented companies. Borrowing cost increases, which directly compress operating margins for debt-reliant industrial operators. * Consumer spending constraints, as higher consumer financing rates limit household discretionary budgets over time.

Future economic projections remain exceptionally cautious as monetary policymakers assess how deeply these elevated costs will penetrate the broader economy. The market is also applying heavy scrutiny to potential leadership adjustments at the central bank. Speculation surrounding potential nominee Kevin Warsh suggests a continuation of stringent monetary discipline rather than early relief.

This mechanical reality dictates that prolonged elevated rates physically alter the valuation environment. Companies that require cheap capital for aggressive expansion face an increasingly difficult operational hurdle over the next eighteen months.

Sector Divergence: Margin Squeeze vs. Value Resilience

The uneven distribution of this macroeconomic pain becomes starkly visible in first-quarter corporate earnings data. Severe operational pressures are heavily concentrated in the aviation and hospitality sectors. JetBlue reported its first-quarter margins were squeezed by 5%, a direct result of elevated fuel costs bypassing their hedging strategies.

Similarly, international hostilities in the Middle East are demonstrably impacting specific discretionary travel segments. Booking Holdings reported a decline in first-quarter accommodation occupancy expansion, despite maintaining a broader global occupancy rate of 68%.

Contrast this vulnerability with the pricing power demonstrated by value-oriented retailers. TJX Companies has successfully maintained 10% margins through strategic pricing adjustments and tight inventory control. Costco has similarly defended its profitability, maintaining 7.5% margins amidst a highly complex supply chain environment.

| Company | Sector Focus | Q1 2026 Margin & Growth Impact |

|---|---|---|

| JetBlue | Aviation | 5% margin squeeze from fuel costs |

| TJX Companies | Value Retail | Maintained 10% margins |

| Costco | Wholesale Retail | Maintained 7.5% margins |

Paradoxically, consumer transaction data reveals that underlying spending remains highly resilient in specific categories. Visa reported first-quarter payment volumes up 12%, while American Express payment volumes climbed 15%.

Much of this apparent consumer resilience is being supported by households rapidly drawing down their finite savings buffers, establishing an aggregate spending pattern that mathematical models suggest is fundamentally unsustainable.

This sector divergence provides the primary analytical lens for current stock selection. Companies with the pricing power necessary to survive an extended period of high interest rates are clearly separating from those exposed to unhedged operational costs.

The AI Infrastructure Paradox Defying Macro Gravity

While traditional sectors battle margin compression, secular technology investments are operating in a completely different paradigm. Massive capital expenditure in artificial intelligence infrastructure is proceeding without regard for elevated borrowing costs or geopolitical tensions. Four major technology companies have outlined approximately $650 billion in planned 2026 capital expenditure.

This unprecedented AI infrastructure investment is heavily concentrated on physical hardware and data centre construction, initiating a massive semiconductor supercycle that operates almost entirely outside standard economic cycles.

This infrastructure expansion dictates the trajectory of the broader market. According to market data, Amazon, Alphabet, Meta, and Microsoft currently represent a combined 18.3% weighting in the S&P 500. Their specific spending guidance effectively insulates a significant portion of the index from traditional macroeconomic gravity.

Amazon anticipates approximately $200 billion in capital expenditure for the year, while Alphabet has guided for $175 billion to $185 billion.

| Technology Company | 2026 Capex Guidance | Q1 2026 Expected Sales Growth |

|---|---|---|

| Alphabet | $175-$185 billion | 50.1% (Google Cloud) |

| Amazon | ~$200 billion | 25.0% (AWS) |

| Microsoft | Significant baseline increase | 40.0% (Azure) |

| Meta | $115-$135 billion | 31.0% (Total Expected Sales) |

This dual-track market is also creating profound secondary benefits for alternative power providers. The immense energy demands of artificial intelligence data centres are driving immediate revenue recalibrations across the industrial utility space.

Bloom Energy experienced a post-market stock appreciation after raising its 2026 revenue projection. Investors are witnessing a clear flow of capital into sectors securely detached from the macroeconomic headwinds pressuring the rest of the economy.

Strategic Positioning for the 2027 Rate Horizon

The core tension in current equity markets exists between localised geopolitical inflation risks and the sheer force of resilient technology spending. The Federal Reserve timeline pushes meaningful monetary relief out to late 2027, confirming that the current restrictive environment requires long-term portfolio adaptation.

This reality requires a deliberate shift in equity strategy today. The analytical framework for the next eighteen months necessitates selecting equities with either distinct pricing power or direct exposure to secular infrastructure growth. Companies lacking these defensive characteristics will likely struggle to maintain valuations as elevated borrowing costs continue to compress corporate earnings.

Investors must recognise that navigating this environment requires precise sector selection rather than broad market exposure. The divergence between margin-squeezed transport operators and cash-rich technology infrastructure builders will only widen as the rate horizon extends further into the decade.

For investors wanting to explore the potential triggers for a sudden equity repricing, our detailed coverage of market correction risk examines how algorithmic trading models currently fail to price in the persistent supply shocks and global maritime logistics threats shaping the 2026 outlook.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.