As the major technology conglomerates release their first-quarter earnings in late April 2026, the scale of AI infrastructure investment required to maintain sector leadership is coming into sharp focus. The underlying narrative of advanced computing has moved rapidly from software algorithms to the physical hardware and energy resources required to sustain them. This structural transition presents specific commercial opportunities, with the most lucrative plays currently found in the alternative power sector rather than software development.

According to market data, Amazon, Alphabet, Meta, and Microsoft currently constitute approximately 18.3% of the S&P 500 index valuation. Their ongoing capital expenditure commitments indicate a distinct shift in how institutional money values technology infrastructure. These four corporations are driving a massive reallocation of capital across the equity markets, prioritising tangible assets and energy security over pure software expansion.

Wall Street analysts expect an unprecedented influx of capital into the physical foundations of these networks over the coming months. Global IT spending related to data centres is projected to reach $582 billion in 2026.

Wall Street projections indicate that technology infrastructure spending will reach between $530 billion and $700 billion throughout 2026.

Reconciling Massive Tech Valuations with Unclear Profit Margins

The initial euphoria surrounding advanced computing has transitioned into a strict evaluation of return on invested capital. Investment professionals are applying intense scrutiny to the quarterly disclosures rolling in, looking for clear paths to long-term monetisation. This scrutiny highlights a growing tension between aggressive spending cycles and the protection of immediate profit margins.

Currently, data centres are commanding valuations at approximately 40x revenue multiples, which are metrics typically reserved for high-growth software platforms. These elevated multiples are largely justified by their direct access to power and integrated physical assets rather than immediate software yields. The market is effectively pricing in decades of guaranteed demand for the physical spaces where computation happens.

This aggressive capital deployment has simultaneously ignited a historic semiconductor supercycle, as hyperscalers pour billions into the physical hardware required to populate these highly valued facilities.

Major cloud providers face specific financial pressures as they build out this physical capacity:

Extended timelines for translating physical data centre construction into recurring software revenue. Unprecedented capital requirements to secure baseline electrical generation for planned facilities. * Increasing costs associated with advanced cooling systems and next-generation processing hardware.

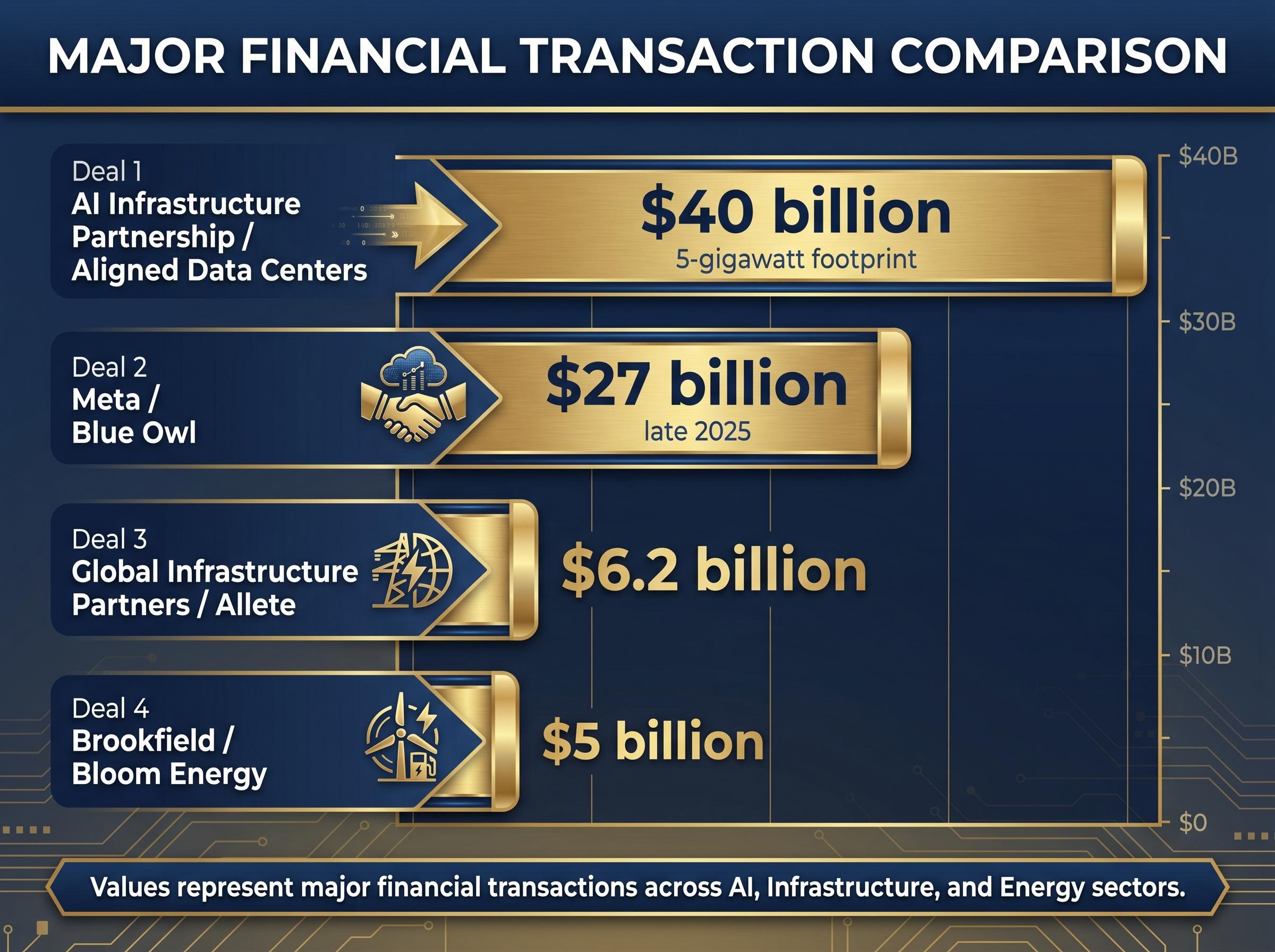

Companies are already moving to lock down future capacity regardless of the immediate margin impact. In late 2025, Meta secured a $27 billion deal with Blue Owl specifically to guarantee future data centre capacity. This kind of outstanding financial commitment underscores how access to physical infrastructure now outweighs short-term margin protection.

When big ASX news breaks, our subscribers know first

Understanding the American Power Grid Deficit

Advanced computing facilities require a continuous and massive baseline of electrical demand that traditional utility grids are struggling to supply. When a server farm runs complex processing models, the power required for calculation and subsequent cooling far exceeds the draw of conventional enterprise databases. The thermal management of next-generation hardware requires industrial-scale water and power resources that outstrip local utility capabilities.

The physical limitations of the existing United States energy transmission infrastructure mean that power availability remains the single largest barrier to global facility expansion. Over 23 gigawatts of IT capacity is currently under construction worldwide, straining municipal grids that were not designed for concentrated industrial loads. This rapid expansion creates a severe domestic power deficit that traditional energy providers cannot quickly solve.

| Metric | 2023 Baseline | 2030 Projection | 2035 Projection |

|---|---|---|---|

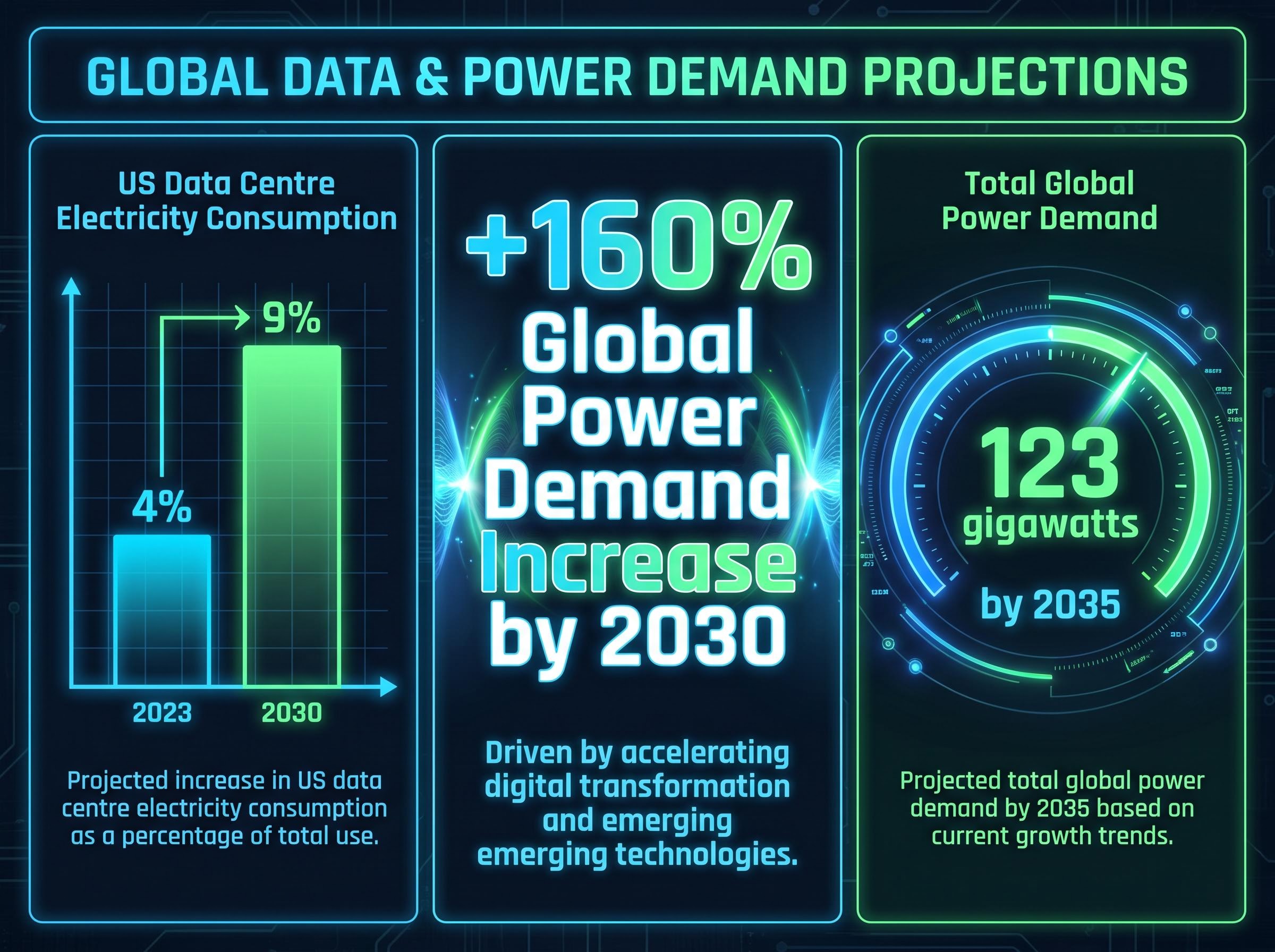

| US Electricity Consumption (Data Centres) | 4% | 9% | Pending |

| Global Power Demand Increase | Baseline | +160% | Pending |

| Total Global Power Demand | Current Capacity | Doubled Capacity | 123 gigawatts |

United States facilities are estimated to consume up to 9% of total domestic electricity by 2030, representing a significant jump from 4% in 2023. On a global scale, capacity is expected to double by 2030, with related power demand projected to rise by over 160%. Projections suggest a potential 123 gigawatts of power demand globally by 2035, fundamentally altering the energy sector.

Official IEA data centre electricity projections reinforce these domestic constraints, modeling a scenario where United States power usage increases by 130 percent over the same period to support accelerating artificial intelligence workloads.

Alternative Energy Emerges as the Primary Beneficiary

With municipal utility grids unable to accommodate this load, alternative and onsite energy generation has emerged as the definitive bottleneck breaker for technology companies. Alternative power providers are actively translating this grid scarcity into immediate revenue acceleration. Strategic partnerships with database giants validate the onsite power generation model as a commercial necessity rather than just an environmental preference.

Traditional backup equipment manufacturers are capitalising on this trend by pivoting aggressively into hyperscale data centre infrastructure, securing lucrative contracts to provide continuous operational power.

The first-quarter 2026 financial outperformance of major sector players provides hard evidence of this shift. Companies providing independent power solutions are seeing massive commercial returns as technology firms bypass traditional utilities. Bloom Energy provides a clear case study of this dynamic in action.

Bloom Energy reported first-quarter 2026 income expansion, easily surpassing analyst predictions.

Following this performance, the company elevated its full-year 2026 revenue expectations. Furthermore, the corporate stock valuation appreciated during post-market transactions. This market response demonstrates that investors are actively rewarding entities capable of generating independent electricity.

Private Capital Orchestrates the Great Grid Bypass

Institutional capital is rapidly shifting toward power-secured development, recognising that the most lucrative infrastructure plays are happening entirely off the public grid. Private equity firms, developers, and traditional utilities are forming massive consortiums dedicated to securing base generation. These groups are quietly buying up the baseline utility layer to guarantee operational capacity for future computing needs.

The scale of these private market transactions dwarfs many public market technology acquisitions. Global Infrastructure Partners executed a $6.2 billion acquisition of the utility company Allete, securing direct ownership of base power generation. This move underscores the strategic necessity of owning the actual electron production facilities.

The largest private capital infrastructure acquisitions and partnerships include:

- The $40 billion acquisition of Aligned Data Centers and its 5-gigawatt power footprint by the AI Infrastructure Partnership.

- A $6.2 billion acquisition of the utility company Allete by Global Infrastructure Partners.

- A $5 billion partnership between Brookfield and Bloom Energy targeting onsite power solutions.

- The advancement of a 7-gigawatt hub by New Era Energy and Digital Inc, following land acquisition completion in early 2026.

These capital flows illustrate how smart institutional money approaches the sector. The AI Infrastructure Partnership, formed by BlackRock Global Infrastructure Partners, MGX, Microsoft, and Nvidia, exemplifies this trend by directly pairing capital providers with hardware manufacturers to secure energy assets.

The official GAIIP investment framework outlines how this specific consortium intends to unlock up to $100 billion in total capital potential, demonstrating the sheer scale of private funding required to overcome current baseline utility limitations.

The Shift Toward Closed-Loop Ecosystems

The commercial appeal of onsite generation lies in the creation of closed-loop ecosystems. By developing their own power sources alongside data centres, hyperscalers bypass the regulatory hurdles and physical limitations of municipal grids.

This strategy accelerates deployment timelines significantly. Bypassing municipal utility delays allows technology companies to bring new processing capacity online years faster than waiting for traditional grid upgrades.

Commercial Considerations for Infrastructure Portfolios

To navigate this environment, active investors require a framework for evaluating companies operating within the facility supply chain. The core evaluation metric has shifted away from software multiples toward hardware and power realities. Assessing an asset now requires distinguishing between theoretical computing capabilities and physical access to reliable, scalable electricity.

Macroeconomic factors complicate these mega-projects. Capital requirements must be weighed against benchmark interest rates. Additionally, sustained increases in fuel costs and global energy prices, driven by ongoing international conflicts, continue to pressure supply chain margins.

When evaluating commercial infrastructure assets, consider three specific criteria:

Possession of secured, long-term power purchase agreements or onsite generation capabilities. Exposure to the physical hardware supply chain required for advanced cooling and electrical transmission. * Ability to fund multi-billion dollar capital expenditure cycles within the current interest rate environment.

Companies that score highly on these criteria are generally better positioned to absorb the massive upfront costs of facility development. Only entities with exceptional balance sheets or robust consortium backing can participate effectively in this capital-intensive cycle.

Readers interested in the broader macroeconomic vulnerabilities can explore our deep-dive into tech capital expenditure risks, which outlines how supply chain bottlenecks and margin compression could eventually threaten these elevated hardware valuations.

The New Fundamentals of Digital Expansion

The technology sector has undergone an irreversible shift from software-centric evaluations to power-centric valuations. The entities that generate, transmit, and secure electricity are emerging as the true winners of the current computing wave. As physical infrastructure becomes the primary bottleneck, control over energy determines control over market share.

This transition forces institutional investors to rapidly recalibrate their portfolio models, placing less emphasis on immediate software monetisation and more weight on the tangible ownership of computing capacity.

Wall Street projections of a $530 billion to $700 billion capital expenditure pipeline ensure this trend will persist. The remainder of the 2026 financial year is expected to see an increased convergence between the technology and utility sectors as these massive capital flows execute.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.