The United States implementation of a strict economic embargo against Iranian ports this month has triggered an immediate and severe reaction across global energy markets. This aggressive foreign policy manoeuvre, designed to restrict funding channels amid escalating Middle Eastern conflicts, is rapidly translating into domestic economic pain for American households at both the fuel pump and the retail checkout. The economic impact of geopolitical conflict has evolved from an abstract overseas risk into a direct, measurable drain on consumer wallets and corporate balance sheets.

This analysis traces the exact path of the current geopolitical disruption. The examination moves from international raw material markets through to corporate earnings, consumer behavioural shifts, and ultimately central bank monetary policy decisions. Understanding this precise transmission mechanism provides investors with a clearer framework for assessing the macroeconomic volatility that will define the remainder of 2026.

The Energy Catalyst and Global Market Repricing

The April 2026 United States blockade of Iranian ports has structurally altered the near-term supply outlook for global crude. By restricting tanker movements and enforcing strict new sanctions on Tehran, policymakers aimed to curtail regional hostilities. However, the resulting disruptions in the Strait of Hormuz have amplified the geopolitical premium on global oil benchmarks.

This tension hits the ledger first in the international commodity markets before cascading down to the domestic economy. As of 29 April, the pricing pressure has become acute, with WTI crude oil currently trading at $102.41 per barrel, while Brent crude stands elevated at $112.83 per barrel.

For the American consumer, this international repricing is highly visible.

| Energy Benchmark | Late March 2026 Base | Mid-to-Late April 2026 |

|---|---|---|

| WTI Crude Oil | Pre-embargo levels | $102.41 per barrel |

| Brent Crude Oil | Pre-embargo levels | $112.83 per barrel |

| US Regular Gasoline | $3.990 per gallon | $4.123 per gallon |

This direct connection between international crude pricing and domestic fuel costs forces immediate adjustments to household budgets. United States regular gasoline prices spiked to $4.123 per gallon by 13 April, up from $3.990 just weeks prior. Understanding the severity of this primary energy shock is necessary for investors trying to gauge the baseline inflation risk facing the domestic economy this quarter.

The official EIA short-term energy outlook data projects regular gasoline retail prices peaking at nearly $4.30 per gallon during the second quarter of 2026, confirming the persistent nature of this fuel shock for domestic consumers.

When big ASX news breaks, our subscribers know first

Understanding the Anatomy of a Supply Side Shock

A supply side shock occurs when an external event suddenly restricts the availability of critical raw materials, forcing prices upward regardless of consumer demand. Unlike demand-driven inflation, which central banks can cool by raising interest rates to slow borrowing, supply constraints are largely immune to monetary policy.

Energy is the ultimate economic input, and its demand is highly inelastic for the average consumer. Most households cannot simply choose to stop commuting or heating their homes when prices spike, forcing them to absorb the higher costs. This absorption systematically drains consumer wallets and creates a compounding effect across the broader economy.

The transmission mechanism of energy-driven inflation follows a precise path from international waters to domestic storefronts:

- Extraction and Transit Squeeze: Geopolitical tensions restrict access to major shipping lanes, applying immediate premiums to raw crude prices.

- Refinery and Distribution Markups: Higher raw input costs are passed directly to wholesale distributors and logistics companies.

- Freight and Supply Chain Compounding: Every physical good requires transportation, meaning elevated diesel and aviation fuel costs are baked into the wholesale price of manufactured items.

- Final Retail Pricing Adjustment: Retailers must increase shelf prices to protect their profit margins, forcing consumers to pay more for basic necessities.

Central banks historically struggle to manage this specific type of inflation because raising interest rates does not clear blocked shipping lanes or produce more oil. The global economic threat is severe enough that the International Monetary Fund and World Bank recently pledged $150 billion to support economies highly vulnerable to these exact energy volatility disruptions. This framework explains why a localised conflict half a world away inevitably forces American households to change their daily budgets.

For readers wanting to understand how these compounded inflationary forces threaten broader economic growth, our dedicated guide to oil-driven recession mechanics examines the four distinct channels through which sustained crude inflation directly curtails national output.

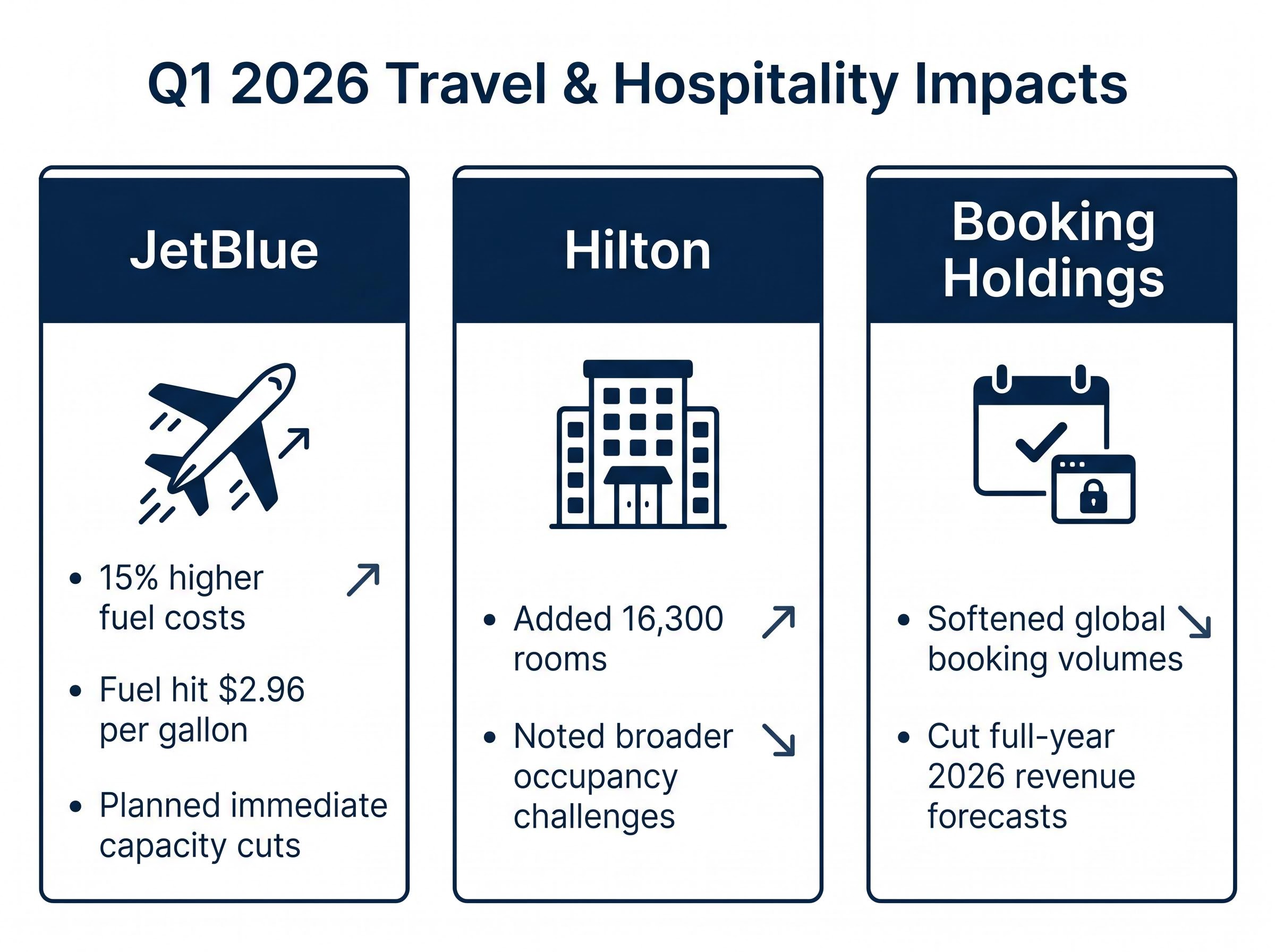

Grounded Flights and Squeezed Margins in Travel

The abstract threat of supply side inflation has already materialised into concrete corporate pain during the first-quarter 2026 earnings season. The travel and hospitality industry has emerged as the clearest casualty of the geopolitical energy shock.

Corporate leadership teams are facing the dual headwinds of surging operational costs and a softening consumer willingness to travel internationally. As margins compress, airlines and hotel operators are actively warning investors about the remainder of the year.

The differing impacts across sub-sectors reveal how the macro environment is crushing corporate margins:

Airline Operations: Carriers are absorbing direct hits to their primary operating expense. JetBlue reported financial losses tied directly to 15% higher fuel costs, which reached $2.96 per gallon, forcing the airline to plan immediate capacity cuts. Hospitality Networks: Accommodation providers are seeing structural softening. While Hilton added 16,300 rooms during the quarter, management noted broader occupancy challenges. * Online Travel Agencies: Platform aggregators are experiencing booking hesitations. Booking Holdings explicitly cited Middle East disruptions when discussing softened global booking volumes.

The official Booking Holdings first quarter financial results confirm that ongoing overseas conflicts are exerting a measurable downward pressure on room nights and gross booking metrics across the platform.

Readers holding consumer discretionary or travel equities must recognise the direct line between Middle Eastern disruptions and these downgraded corporate projections.

Downgraded Forward Guidance

The defensive posture taken by corporate leadership teams is most visible in their forward-looking financial statements. Booking Holdings made the rare move of cutting its full-year 2026 revenue forecasts entirely based on the uncertainty surrounding the overseas conflict.

Companies are actively recalibrating their capital allocation strategies to preserve cash. This defensive signalling suggests that executives do not view the current energy friction as a transient issue, but rather a persistent headwind that requires fundamental operational adjustments.

The American Consumer Pivots to Value Retail

As energy costs consume a larger percentage of the family budget, everyday Americans are actively changing their spending habits to survive the inflationary squeeze. This reallocation of household discretionary income is creating distinct winners and losers within the domestic retail sector.

A deeper analysis of underlying retail sales data reveals that aggregate consumer spending figures are increasingly masking the financial strain on lower-income households who are rapidly depleting their personal savings.

Traditional retail environments are facing increasing pressure as shoppers calculate the rising cost of basic commutes against non-essential purchases. Conversely, discount chains are experiencing a surge in foot traffic. According to recent commentary, Costco has noted distinct changes in shopper spending behaviours, with members actively migrating toward value-oriented items.

This shift functions as a defensive consumer strategy in a high-inflation environment, not merely a temporary blip in consumer confidence. TJX Companies is strategically positioned to capture this trade-down traffic. However, even discount operators are acknowledging the severity of the macro environment; TJX has still forecasted muted annual sales, citing the overall pressure on discretionary budgets.

For the financial community, this insight reveals critical sector rotation opportunities. Investors who recognise that consumer pain in traditional retail translates directly to increased market share for discount operators can position their portfolios defensively.

Central Bank Paralysis at the Federal Reserve

These compounding global flashpoints have essentially trapped central bankers into policy inaction. The Federal Reserve convenes for its highly anticipated Federal Open Market Committee meetings from 28 to 29 April facing a deeply complex macroeconomic picture.

Policymakers maintain a rationale that views short-term energy price spikes as temporary phenomena. The central bank prefers to maintain its focus on core Personal Consumption Expenditures, which typically strips out volatile food and energy metrics. However, the sheer velocity of the April crude shock makes this separation increasingly difficult to justify to a public experiencing immediate inflation at the petrol station.

The Federal Reserve must also navigate conflicting economic signals. Geopolitical risk is actively slowing consumer spending, yet domestic digital infrastructure continues to boom. Big technology firms are projected to spend $650 billion on artificial intelligence capital expenditures in 2026, driving massive revenue for energy infrastructure providers like Bloom Energy.

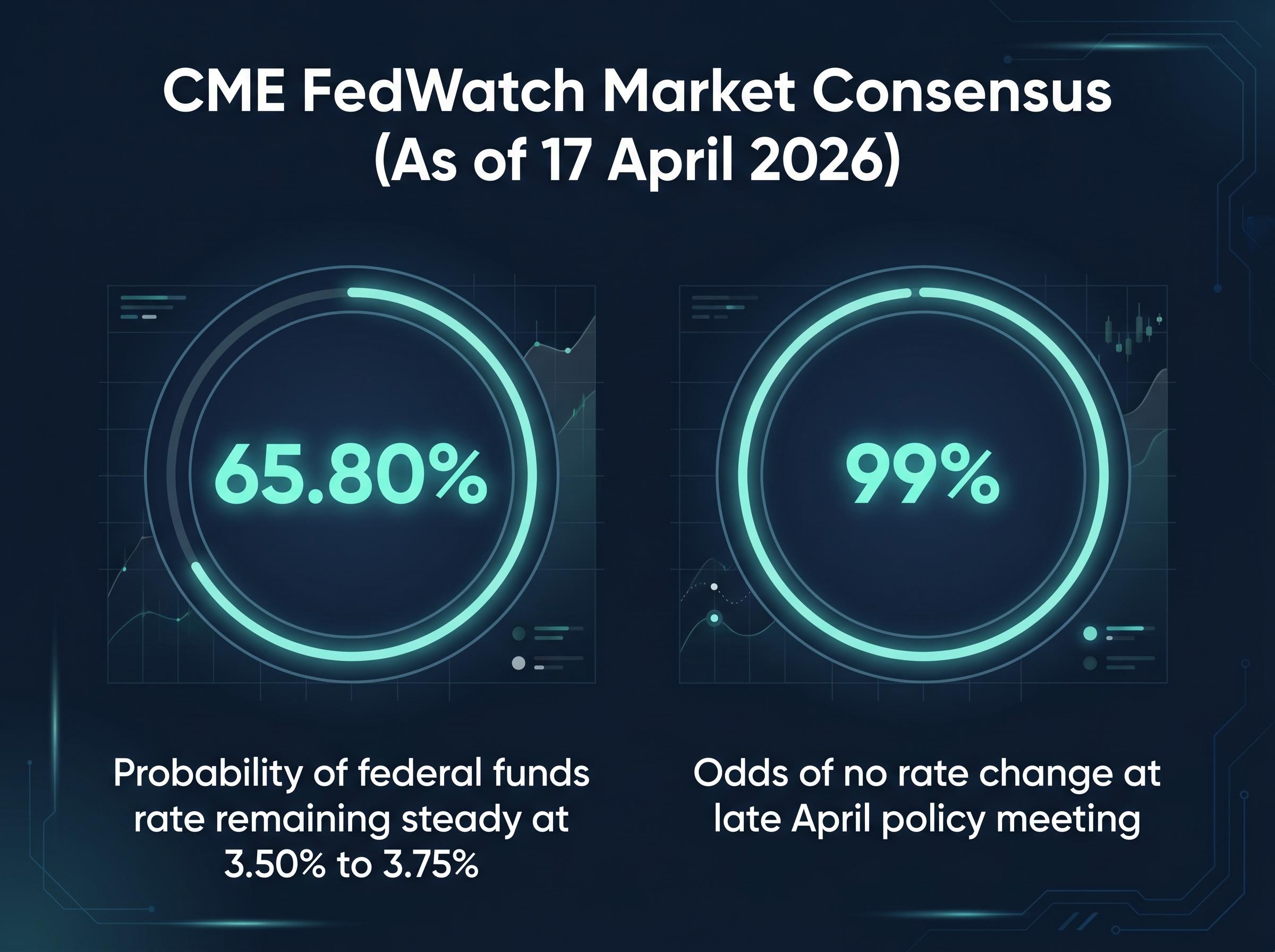

CME FedWatch Market Consensus As of 17 April 2026, CME FedWatch data indicated a 65.80% probability of the federal funds rate remaining steady at 3.50% to 3.75%. Markets are pricing in overwhelming 99% odds of no rate change at the late April policy meeting.

This data provides investors with the ultimate context for why interest rates will remain elevated for longer. Central bankers cannot risk cutting rates while supply chains are fractured, directly tying domestic corporate borrowing costs to overseas geopolitical standoffs.

Investors exploring how these prolonged rate holds might impact broader equity valuations will find our full explainer on S&P 500 energy vulnerabilities, which examines the historical warning signals triggered when record equity highs collide with surging commodity costs.

The Long Shadow of Global Instability on Domestic Markets

The cascading events of April 2026 confirm that geopolitical tensions are no longer isolated regional disputes. They are the primary drivers of domestic inflation, corporate earnings revisions, and consumer behavioural shifts.

As a direct consequence of this market friction, institutional recession probability estimates have surged toward the fifty percent threshold, indicating that major banks now view a severe economic contraction as a baseline scenario.

The transmission mechanism is clear: naval blockades disrupt crude transit, forcing energy prices higher, which compresses travel industry margins and drains household discretionary income. As long as the Iranian embargo and Middle Eastern disruptions persist, the Federal Reserve remains constrained, unable to provide the rate relief that equities markets previously anticipated.

Investors must recognise that the current macroeconomic environment requires a fundamental recalibration of risk. Building geopolitical risk premiums into portfolio expectations is now a necessity for the remainder of 2026, particularly for strategies exposed to consumer discretionary spending or rate-sensitive sectors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.