Global Energy Crisis: the New Rules of Macro Investing

2 mins ago

The April 2025 acquisition of Alani Nu for $1.8 billion immediately expanded the top-line profile of the company, yet Celsius Holdings stock continues to trade in a defined range of $34.00 to $35.00 as of late April 2026. This pricing pattern reflects a market capitalisation hovering between $8.5 billion and $9.0 billion. The stabilisation of the share price signals that investors are currently weighing massive revenue expansion against the mechanical costs of corporate integration.

With upcoming Q1 earnings expected in early May 2026, the business faces a clear test of its financial modelling and operational efficiency. The core analytical thesis centres on whether the brand can maintain its hyper-growth trajectory to justify these premium valuation multiples in a highly competitive sector.

The dual-brand strategy deployed by Celsius successfully captured an estimated 20% share of the United States energy drink market, fortifying its competitive positioning against legacy rivals. Integrating the Alani Nu portfolio generated a massive quarterly revenue surge, pushing Q4 2025 figures to $721.6 million. This result represented a 117% year-over-year increase, paired with an adjusted Q4 2025 earnings per share (EPS) of $0.26 that exceeded market expectations.

However, this aggressive top-line expansion introduced temporary pressure on profitability margins. The Q4 2025 gross margin contracted to 47.4%, illustrating the near-term financial squeeze characteristic of large-scale corporate integration. Management projections indicate a margin rebound into the low 50% range following the completion of first-half 2026 integration efforts.

The official full-year 2025 financial results issued by the company detail how these specific margin contractions stem from the initial operational costs of absorbing the massive Alani Nu supply chain network.

Investors require precise visibility into exactly where the company stands regarding profitability right now. Understanding this timeline for margin recovery is an important step for evaluating short-term equity risk ahead of the May earnings release. The upcoming H1 2026 milestones stand as clear proving grounds for realising synergistic cost savings across the newly combined entity.

Leadership Integration Update “Our integration efforts have shown strong momentum and distribution gains across all target demographics, setting a foundation for operational efficiency moving into the second half of the year,” executives noted during the Consumer Analyst Group of New York (CAGNY) presentation on 19 February 2026.

| Financial Metric | Q4 2025 Reported Result | 2026 Forward Expectation |

|---|---|---|

| Quarterly Revenue | $721.6 million | Pending Q1 release in May |

| Gross Margin | 47.4% | Rebound to low 50% range post-H1 |

| US Market Share | Estimated 20% | Consolidation of dual-brand operations |

Traditional value-investing metrics often fail to capture the forward-looking mechanics of consumer packaged goods operating in hyper-growth phases. A price-to-earnings (P/E) multiple communicates market expectations for future earnings rather than serving as a strict reflection of current baseline profitability. For high-growth assets, investors pay a premium upfront based on the mathematical probability of sustained exponential returns.

When evaluating beverage stock growth models, this upfront premium often contrasts sharply against capital-intensive retail operators that carry lower gross margins but more predictable physical expansion targets.

This dynamic explains the massive upward trajectory the stock experienced over the half-decade concluding in March 2024. By the end of 2025, the P/E ratio for the company hovered between 503x and 571x. While these figures appear disconnected from standard market averages, they encode specific Wall Street expectations regarding future sector dominance and international scalability.

Evaluating such high-multiple equities requires finance-focused readers to look past immediate sticker shock. The valuation models rely entirely on the company executing its multi-year expansion without faltering against established legacy competitors.

The premium valuation sits within a broader overarching energy drink market projected to achieve a compound annual growth rate (CAGR) of 8% through 2033. This macro-level expansion provides the necessary total addressable market for aggressive earnings projections. A premium multiple remains mathematically defensible only if the company continues capturing an outsized share of this 8% industry growth.

Consensus analyst forecasts predict aggressive expansion over the next two years, requiring precise operational execution to materialise. Wall Street projections anticipate a top-line sales expansion from 2026 through 2028. Over this identical forecasting window, diluted earnings per share metrics are projected to jump.

Current aggregated Wall Street consensus forecasts indicate an average price target approaching $66.88, which suggests institutional analysts still see substantial upside potential if the company executes its integration effectively.

This magnitude of earnings growth relies directly on the full-year realisation of the Alani Nu acquisition. The mathematical logic assumes that top-line revenue will scale while integration costs simultaneously fall away. Deconstructing these multi-year forecasts provides a concrete framework for evaluating whether the current stock price accurately prices in future execution or leaves room for upside.

Achieving the projected EPS jump demands specific operational levers:

Realising synergistic cost reductions from supply chain consolidation, particularly in overlapping raw material procurement. Executing sustained volume growth across the combined dual-brand portfolio by leveraging unified shelf-space negotiations. Stabilising marketing spend as a percentage of total revenue following the initial acquisition awareness campaigns. Delivering gross margin recovery into the low 50% range by late 2026.

These projections carry inherent risk factors within the intensely crowded beverage sector. The market features heavy competition from deeply capitalised legacy brands attempting to reclaim lost shelf space through aggressive promotional pricing.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various competitive risk factors.

While domestic sales currently drive the bulk of revenue, international expansion serves as the fundamental mechanism for sustaining long-term momentum. The saturated North American market necessitates a shift in focus toward the massive runway available in international territories. This geographic diversification strategy is heavily relied upon to justify the ambitious 2028 earnings forecasts.

Other major consumer packaged goods and retail beverage operators similarly hinge their long-term growth on international brand expansion efforts, particularly targeting high-volume consumer bases in Asian and European markets to offset domestic saturation.

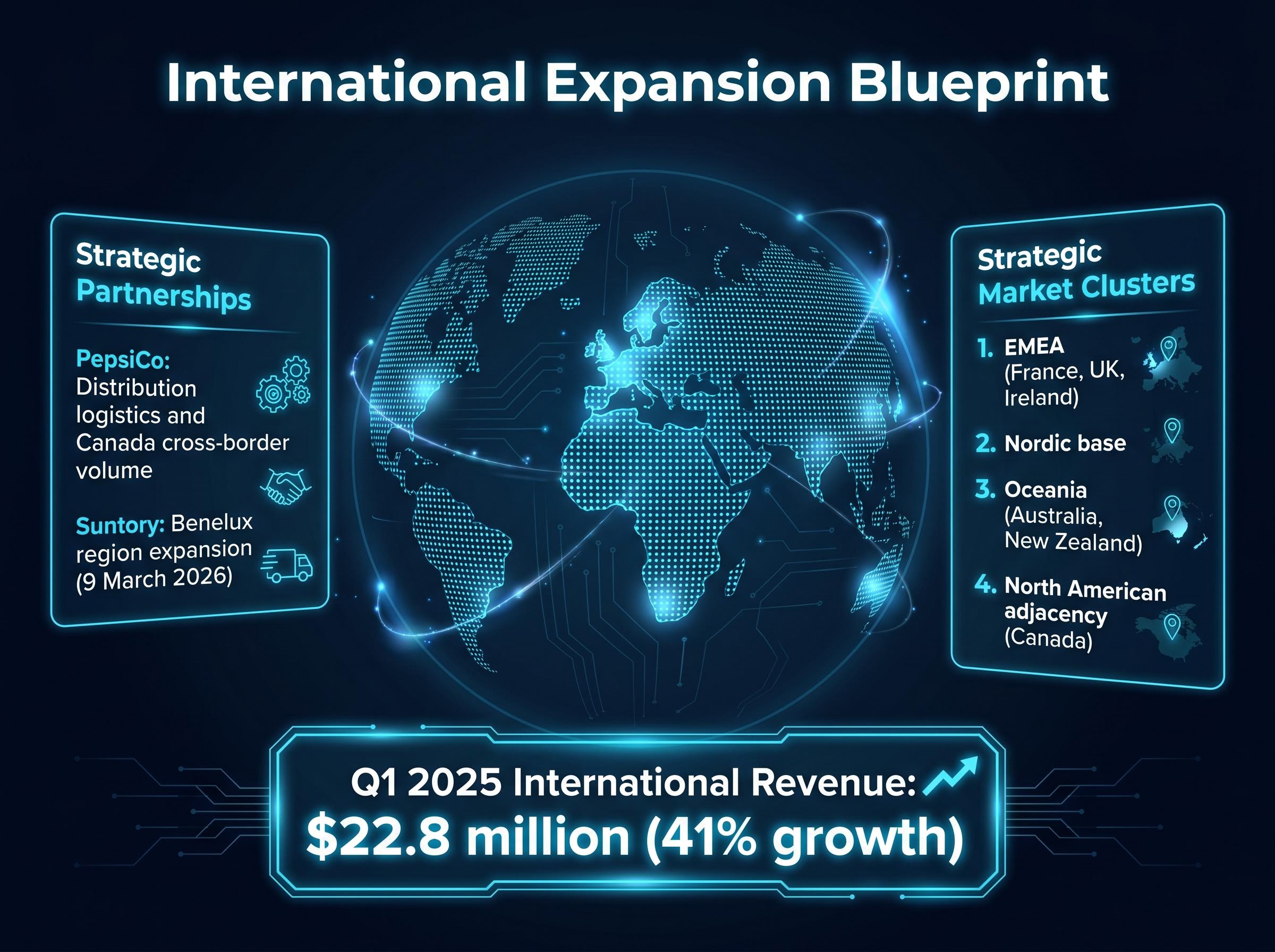

Rather than building proprietary infrastructure abroad, the company utilises established beverage giants to handle distribution logistics. This strategy actively leverages the formidable distribution network provided by PepsiCo, alongside new regional partnerships. These strategic alliances allow rapid market penetration with significantly lower upfront capital expenditure compared to organic international builds.

Recent explicit milestones demonstrate this blueprint actively executing in early 2026. On 9 March 2026, the company announced a major expansion into the Benelux region through a partnership with Suntory. This specific territory functions as a strategic gateway for broader European market penetration. The move builds upon historical baseline data from Q1 2025, which showed international revenue growing 41% to $22.8 million.

The current international brand footprint ranks several key market clusters by their strategic importance:

A balanced commercial assessment of the business reveals a core tension between undeniable operational momentum and a highly demanding market valuation. The company holds strong domestic positioning with a 20% market share, yet it must continuously navigate the ongoing margin pressures of acquisition integration. The current stock price anchor of $34.00 to $35.00 reflects a market waiting for definitive proof of profitability recovery.

The anticipated Q1 2026 earnings release in early May 2026 serves as the next immediate catalyst for the equity. Moving through the next four quarters, investors must monitor the exact timeline for gross margin normalisation and the pace of international revenue scaling.

For investors exploring the specific revenue targets required to maintain these premium multiples, our detailed coverage of Celsius stock forward earnings breaks down the multi-brand market share data and global expansion catalysts expected to drive the company through the end of the year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The April 2025 acquisition of Alani Nu for $1.8 billion immediately expanded Celsius Holdings' top-line profile, contributing to a 117% year-over-year revenue increase in Q4 2025.

Gross margins contracted to 47.4% in Q4 2025 due to the initial operational costs and complexities of absorbing the massive Alani Nu supply chain network during integration.

Celsius Holdings' Q1 2026 earnings are expected in early May 2026, serving as a key immediate catalyst for the equity as investors monitor profitability and operational efficiency.

Celsius Holdings is pursuing international expansion through strategic partnerships with established beverage giants like PepsiCo and Suntory, leveraging their distribution networks for rapid market penetration with lower capital expenditure.