Retail Investor Trends: Analysing the 2026 Flight to Global ETFs

2 mins ago

The modern beverage market has produced two extraordinary success stories currently battling near the $9 billion valuation mark. Their blueprints for reaching this milestone could not be more different. For investors comparing a Celsius versus Dutch Bros stock allocation, the choice demands evaluating two entirely distinct operational frameworks.

As of late April 2026, both Celsius Holdings and Dutch Bros are navigating critical growth phases that will define their next decade. Celsius is actively working to prove its international viability following its 2025 Alani Nu buyout. At the same time, Dutch Bros continues an aggressive physical expansion across the United States ahead of its May 2026 earnings call.

Investors must weigh the rapid consumer packaged goods scalability of Celsius against the high predictability retail engine of Dutch Bros. Understanding these structural differences is the only way to accurately assess which equity offers the superior risk to reward profile.

To accurately compare these valuations, analysts must first isolate the core operational models that define these two enterprises. A consumer packaged goods brand scales differently than a physical drive-through franchise. Comparing a high margin canned drink business directly to a capital intensive retail chain requires looking at different fundamental metrics.

For investors new to the beverage sector, consumer packaged goods companies act primarily as brand creators and wholesalers. They formulate the product and contract external distributors to secure retail visibility. Conversely, physical retail operators own the real estate and manage the entire transaction lifecycle.

| Company | Business Model | Current Market Cap (April 2026) | Gross Margin |

|---|---|---|---|

| Celsius Holdings | Consumer Packaged Goods (CPG) | $8.37 billion | According to estimates, ~49.2% |

| Dutch Bros | Drive-Through Coffee Retail | $9.2 billion | According to estimates, >25.0% |

Celsius leverages third-party distribution networks to capture shelf space without purchasing real estate. This asset-light approach requires significantly lower capital expenditures to enter new geographical markets. The company manufactures the product and relies on distribution partners to place it in front of consumers.

This structure eliminates the need for expensive retail leases and massive retail labour forces. According to estimates, this operational efficiency generates gross profitability reaching 49.2%. The primary risk in this model remains the intense competition for limited grocery shelf space.

Dutch Bros requires heavy upfront capital to build and staff new physical locations. This real estate intensive strategy offers a distinct long-term payoff through customer capture. The company owns the entire transaction from order to delivery, maintaining complete pricing control.

According to estimates, this physical structure yields gross margins slightly exceeding 25%. The lower margin reflects the higher overhead required to maintain a physical presence and employ retail staff. Recognising these structural differences helps investors understand why the two equities carry vastly different valuation multiples.

The SEC Form 10-K disclosures for the company outline how maintaining retail staff and physical property leases directly impacts the bottom line, providing a transparent view of these ongoing overhead requirements.

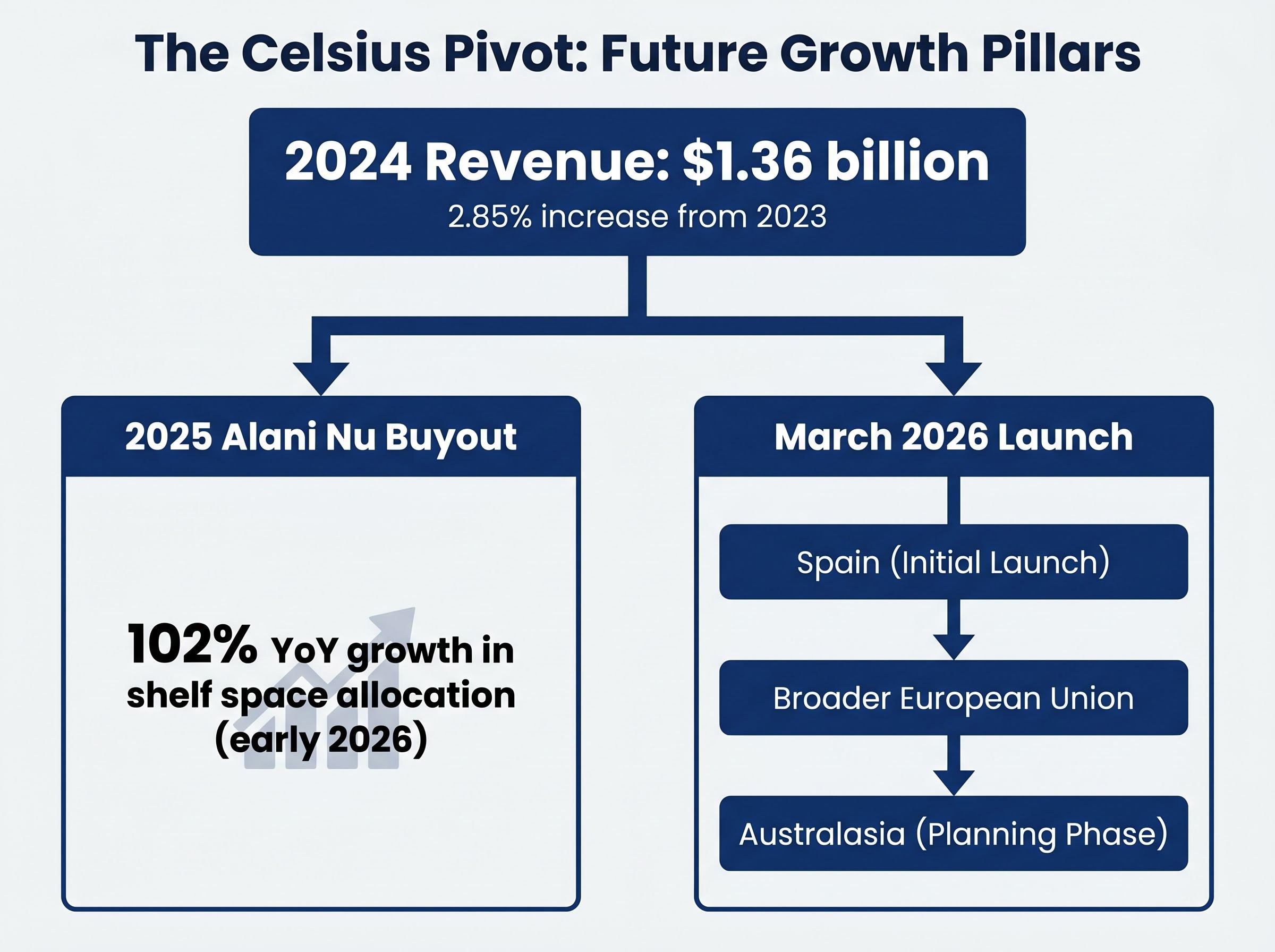

Celsius built its reputation as a domestic growth leader, but its forward valuation now depends heavily on its transition into a global acquirer. The company reported 2024 revenue of $1.36 billion, representing a 2.85% increase from 2023. This maturing domestic growth rate explains why management executed the 2025 Alani Nu buyout.

The acquisition strategically shifted the corporate portfolio toward sugar-free and health-oriented beverage options. These product lines align perfectly with modern dietary preferences across younger demographic cohorts.

The integration of Alani Nu is already demonstrating quantifiable momentum. The acquired brand secured a 102% year-over-year growth in shelf space allocation for early 2026. This expanded domestic footprint serves as a financial bridge while Celsius executes its overseas strategy. The company officially initiated its international expansion phase in March 2026.

A dedicated Celsius stock analysis reveals that the multi-brand strategy initiated by the Alani Nu acquisition has already helped capture over 20 percent of the US market share, validating management’s aggressive pivot.

Target geographic markets for this expansion include:

Spain (serving as the initial European launch market) Broader European Union territories following initial data collection * Australasia (currently in measured early-stage planning)

Financial analysts project that this combined acquisition and distribution strategy will yield significant upside if executed correctly. Top-line generation is anticipated to climb between 2026 and 2028. Furthermore, diluted earnings per share forecasts project a jump over the same window.

Investors must determine if Celsius can replicate its historic domestic success overseas. Securing international distributors requires navigating entrenched local competitors, and the cautious rollout in Spain reflects management acknowledging these geographical hurdles. These two pillars of acquisition and international distribution are now entirely responsible for justifying future share price growth.

Dutch Bros translates operational execution into a premium market valuation through relentless venue multiplication. The company achieved remarkable consistency through site-level execution, commanding the attention of institutional capital.

Operational Consistency “The company achieved its 19th consecutive year of positive same-store sales growth through 2025, demonstrating remarkable resilience across multiple economic cycles.”

This momentum continues to compound in the current fiscal year. Same-store sales grew 7.7% in the fourth quarter of 2025. Preliminary reports indicate 4% growth for the first quarter of 2026, signaling sustained consumer demand.

The brand builds durable competitive barriers rooted in local recognition and evolving economies of scale. By using its drive-through lanes to establish convenience in suburban markets, the company insulates itself from traditional retail foot traffic declines. The physical retail footprint reached 1,136 distinct sites by late 2025.

Executive guidance targets 2,029 properties by 2029, operating against an estimated domestic ceiling. To maintain this aggressive trajectory, Dutch Bros plans to open 181 new locations throughout 2026. The predictability of this expansion pipeline is the primary driver of the stock’s premium multiple.

Understanding the timeline of these targets allows retail investors to model out long-term return expectations with a high degree of confidence. The company is actively testing culinary menu additions across operating sites to drive higher average ticket prices. If these food attach rates improve, the unit economics of each new drive-through location will scale beyond historical averages.

The strategic food integration planned for systemwide deployment by the end of 2026 will require careful execution, as these operational changes must not disrupt the speed of their existing beverage service.

A clear view of downside risk is essential before allocating capital to either enterprise. Investors must contrast the intense industry rivalry Celsius faces in the energy drink aisle against the local monopoly dynamic Dutch Bros builds in its drive-through lanes. The threat of lost grocery shelf space carries immediate revenue implications for consumer packaged goods operators.

This suburban dominance provides a critical buffer against larger legacy chains; for example, recent Starbucks turnaround initiatives have heavily focused on operational efficiency and digital engagement just to protect their existing customer base.

Celsius shares experienced a surge over the five years preceding their historic peak. This indicates extreme historical volatility that remains priced into the stock. Shareholders must stomach significant price swings as international expansion metrics are reported quarter by quarter.

Conversely, Dutch Bros presents a different vulnerability tied to its exceptional pricing multiples. The enterprise carries a total market capitalisation of $9.2 billion as of April 2026, slightly edging out Celsius at $8.37 billion. This hefty valuation relies entirely on future profitability expectations and flawless execution of the physical store rollout.

Primary macroeconomic threats to both consumer discretionary stocks include:

Prolonged inflation compressing disposable income for premium beverages Rising commercial real estate and construction costs affecting retail builds * Supply chain disruptions impacting input costs for aluminium packaging and coffee beans

By comparing these distinct vulnerabilities, readers can align their portfolio choices with their personal risk tolerance.

Financial analysts project distinct immediate upside potential for both equities. The massive upside tied to the Celsius international rollout contrasts sharply against the highly visible store expansion pipeline of Dutch Bros. These forward-looking metrics crystallise the exact timeline for potential investment payoffs.

Celsius consensus maintains a Strong Buy rating with a $60.75 price target. This projection represents massive upside from its $32.62 late April 2026 price. This target reflects Wall Street pricing in a successful European launch and sustained shelf space dominance.

Recent consensus analyst price targets for the equity reflect strong institutional confidence that this overseas distribution strategy will successfully accelerate top-line revenue over the coming quarters.

Meanwhile, Dutch Bros consensus maintains a Buy rating based on its predictable execution. Analysts project a 42.63% upside from its $55.38 late April 2026 level.

| Stock Symbol | Current Price (April 2026) | Analyst Price Target Upside |

|---|---|---|

| CELH | $32.62 | Target $60.75 (Significant Upside) |

| BROS | $55.38 | 42.63% Projected Upside |

These projections provide a clear benchmark for portfolio allocation over the next 12 to 24 months. The upcoming May 2026 earnings reports serve as near-term catalysts that will immediately test these valuations. Investors get a direct, quantifiable comparison of what the market expects from both operators.

The decision between these two beverage operators ultimately depends on investor timeline and volatility tolerance. Analysts recommend Celsius for growth-oriented portfolios willing to accept share price fluctuations in exchange for aggressive international expansion upside. Outsized returns are possible if the company captures European market share and integrates acquisitions successfully.

Conversely, analysts recommend Dutch Bros for investors prioritising consistent, predictable compound growth. The physical real estate expansion provides a transparent roadmap that insulates the company from the volatile shelf-space battles of the grocery aisle. The upcoming earnings season will immediately test both of these operational theses.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Celsius operates an asset-light consumer packaged goods (CPG) model relying on third-party distribution, while Dutch Bros utilizes a capital-intensive physical drive-through retail model with owned locations.

Celsius is executing an international expansion phase, starting with Spain as its initial European launch market, with plans for broader European Union territories and Australasia.

Investors should weigh Celsius's intense competition for grocery shelf space and international expansion execution risks against Dutch Bros' high valuation multiples and exposure to rising real estate and construction costs.

Dutch Bros is highlighted for its predictable unit expansion through new physical locations, with a clear roadmap targeting 2,029 properties by 2029, offering consistent compound growth.

As of late April 2026, Celsius has a Strong Buy rating with a $60.75 price target, representing significant upside, while Dutch Bros has a Buy rating with a projected 42.63% upside from its current level.