How to Evaluate the $700B AI Infrastructure Investment Cycle

just now

Evaluating the trajectory of a Dutch Bros stock investment requires looking past conventional valuation models and focusing on sheer physical momentum. The beverage chain recently delivered a dramatic bottom-line earnings spike in 2025, driven by an aggressive nationwide land grab that consistently exceeds market expectations. This rapid pace of store openings has positioned the company as the fastest-growing drive-thru chain in the United States, capturing market share from slower legacy competitors.

The market context is intensifying rapidly ahead of the highly anticipated 6 May 2026 first-quarter earnings report. As of late April 2026, shares are trading near $57.44, assigning the expanding enterprise a substantial $9.2 billion market capitalisation. This upcoming financial print will test whether the company can maintain its extraordinary momentum.

This analysis deconstructs the structural mechanics driving that premium price tag. By examining the unique drive-thru real estate strategy, the nationwide food menu rollout, and the underlying growth fundamentals, investors can better determine if the current valuation accurately reflects the long-term potential of the asset.

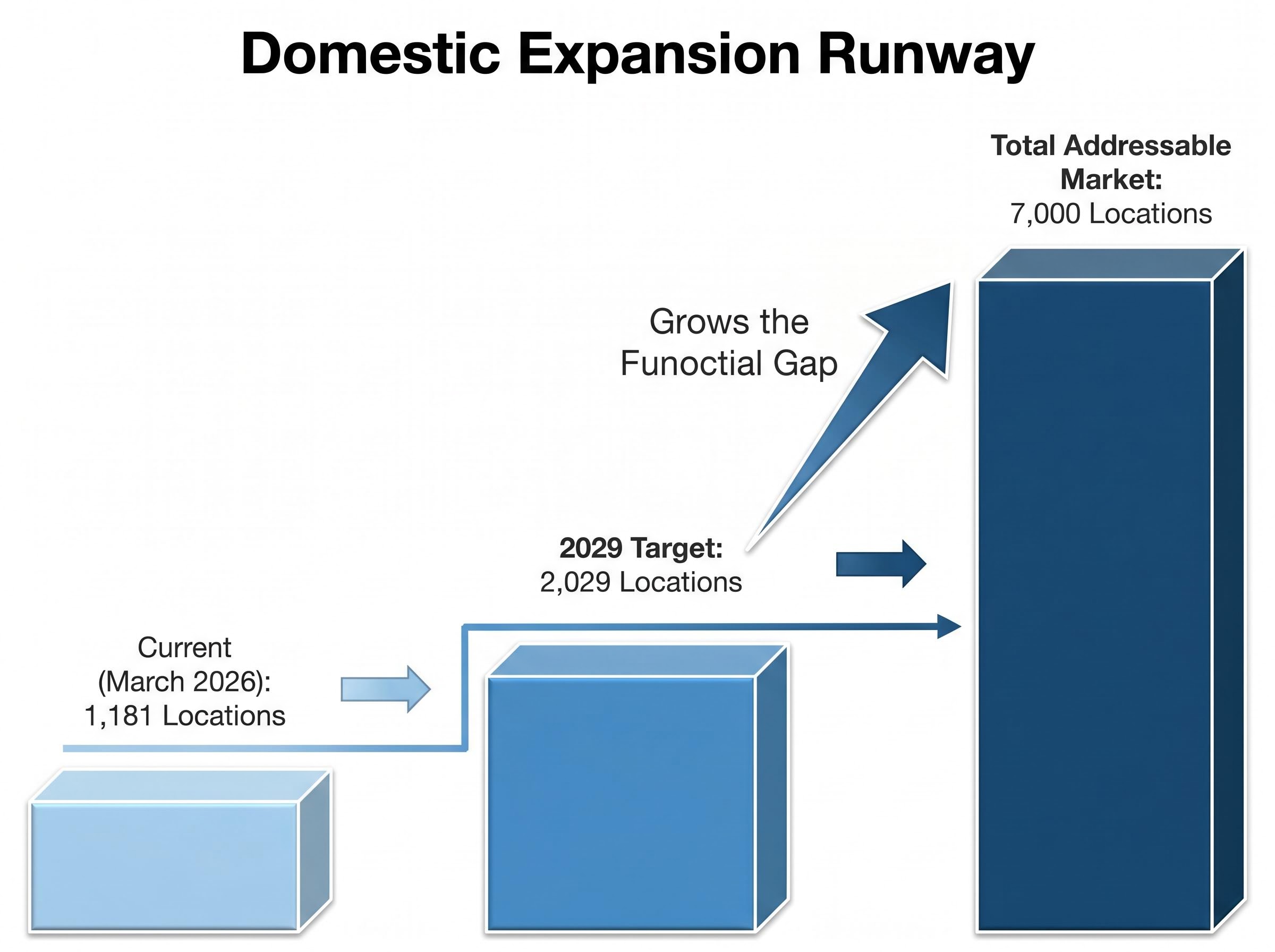

The physical momentum behind the enterprise is relentless, operating with a speed that few retail chains can match. Management closed out 2025 with 1,136 locations across the country and immediately accelerated the pace of construction into the new year. By 24 March 2026, the operational footprint had already expanded to 1,181 distinct shops.

This immediate expansion implies at least 45 new openings in the first quarter alone, demonstrating remarkable operational efficiency in site acquisition, permitting, and rapid construction. Crucially, this aggressive scaling is directly translating into formidable financial performance. According to company data, top-line sales expanded by an impressive 27.9% in 2025, proving that the new store growth is capturing genuine, untapped consumer demand rather than cannibalising foot traffic from existing locations.

The company maintains a firm, clearly articulated target of 181 total system shop openings for the full 2026 calendar year.

Filing the official Dutch Bros’ 2025 Form 10-K with regulators formalised these aggressive expansion targets into legally binding corporate projections, demonstrating management’s high conviction in their execution pipeline.

Investors need to verify that the company can maintain this hyper-growth trajectory without stalling under its own weight. Tracking physical store count confirms management is executing perfectly on its primary growth lever.

| Timeframe | Total Locations | Growth Milestone |

|---|---|---|

| End of 2022 | Baseline rapid expansion phase | |

| End of 2025 | 1,136 | Closed year with high momentum |

| 24 March 2026 | 1,181 | 45 initial Q1 openings completed |

| 2026 Year-End Target | 1,317 | Assuming 181 total targeted openings |

The sheer speed of this physical expansion is only possible because of the underlying unit economics of the business model. Unlike traditional sit-down coffee competitors, the drive-thru-only format relies on a significantly smaller real estate footprint that requires less upfront capital. This fundamental structural difference creates a durable economic moat by drastically reducing both initial build-out costs and ongoing operational overhead.

This nimble footprint provides a distinct advantage over heritage brands that are currently executing complex strategic turnaround initiatives to revitalize their aging, dining-room-heavy portfolios.

These inherent design efficiencies lead to faster construction times and vastly improved operational leverage, which served as the primary catalyst for the 2025 earnings boom. By systematically stripping away dining rooms and indoor seating areas, the company maximises customer throughput and minimises the friction typically associated with the traditional cafe experience.

The financial result of this highly streamlined model is exceptionally consistent performance across varying regional market conditions. Management has now reported an impressive streak of consecutive quarters of comparable location revenue growth, proving the undeniable durability of the concept. The model relies on three distinct structural advantages to maintain this momentum:

While physical footprint expansion provides reliable baseline growth, the next major revenue catalyst lies inside the existing shops. The company is fundamentally raising the revenue ceiling for every location by moving aggressively into nationwide food offerings. The strategic intent behind this operational shift is clear, focusing entirely on increasing the average transaction value and driving new customer acquisition during traditionally slower afternoon hours.

The implementation timeline has progressed rapidly from its initial testing phase to a broad regional deployment. After successfully scaling from just four pilot shops in Phoenix in early 2025, the food programme is currently operating in 300 shops across 11 different states. Management has formally planned a full nationwide rollout by the end of 2026, signalling immense confidence in the supply chain logistics.

Adding a permanent food menu represents the most significant operational and logistical shift in the company’s corporate history.

Food attachment rates directly increase individual ticket sizes, efficiently turning standard beverage orders into higher-margin bundled transactions. Wall Street analysts are currently waiting for concrete Average Unit Volume data in the upcoming 6 May 2026 earnings report to accurately adjust their forward-looking revenue models. Understanding the financial impact of this rollout helps investors accurately gauge the potential for outsized same-store sales growth in the back half of the year.

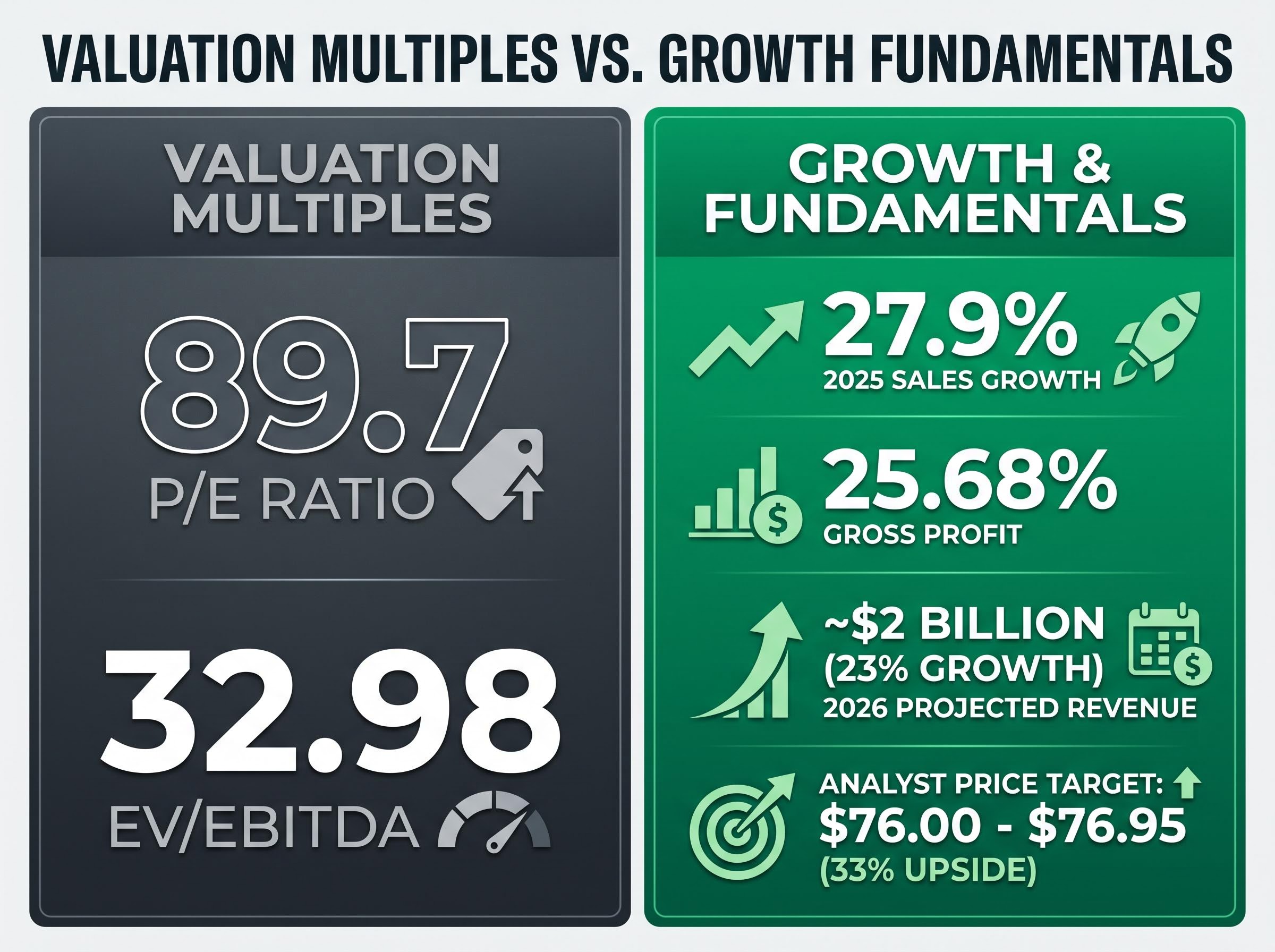

Investors must confront a cold financial reality when evaluating this particular equity opportunity. The stock is currently priced for absolute operational perfection, trading at a steep trailing P/E ratio of approximately 89.7 and an EV/EBITDA multiple of 32.98. These are undeniably premium valuation multiples that require flawless corporate execution and uninterrupted growth to maintain.

However, Wall Street analysts continue to view the drive-thru model as a structurally safer growth asset despite the exceptionally high entry price. This sentiment is similar to how the market treats sector peers like Celsius Holdings, where rapid expansion justifies elevated multiples. The premium valuation is consistently weighed against remarkably strong underlying fundamentals and incredibly bullish consensus growth targets. According to company data, gross profit levels currently sit at a healthy 25.68%, providing the essential margin buffer needed to internally fund ongoing expansion efforts.

“Analysts maintain a bullish consensus price target of $76.00 to $76.95 for the stock, implying an approximate 33% upside potential from current April 2026 levels based on the strong revenue trajectory and reliable footprint expansion.”

Presenting these structural growth catalysts alongside the stark valuation allows investors to make a fully informed risk assessment. Market professionals typically rely on three primary justification drivers when defending the elevated P/E ratio:

Revenue trajectory: Current projections anticipate robust 23% growth, rapidly pushing the company to approximately $2 billion in total revenue for the 2026 fiscal year. Food rollout: The nationwide menu expansion provides an immediate, capital-efficient mechanism to dramatically boost same-store sales without requiring any new real estate acquisitions. * Loyalty programme success: Exceptional digital engagement continues to drive high-frequency customer visits, creating a predictable stream of recurring revenue across all geographic markets.

For investors wanting to contrast this physical asset expansion against alternative high-growth beverage models, our detailed coverage of the Celsius valuation gap examines how capital-intensive retail strategies compare to acquisition-driven packaged goods growth.

To genuinely understand the long-term compounding potential of this asset, investors must expand their perspective to evaluate the ultimate domestic addressable market. Management maintains a highly specific, firm target of reaching 2,029 operational stores by 2029.

Hitting this milestone means essentially doubling the current operational footprint in just three short years.

Even that aggressive three-year goal only captures a small fraction of the recently updated Total Addressable Market figures. Internal corporate projections now indicate a staggering long-term runway for over 7,000 potential restaurant locations nationwide before reaching domestic saturation.

The detailed Investor Day corporate strategy disclosures mapped out how this expanded footprint will penetrate suburban and semi-rural markets that legacy coffee competitors historically ignored.

By revealing the massive gap between the 1,181 current locations and the 7,000 location ultimate potential, the ongoing revenue trajectory gains critical perspective. The enterprise is still remarkably early in its corporate lifecycle, with decades of domestic geographic expansion still readily available to drive shareholder value.

The core tension for investors remains carefully balancing the aggressive, highly successful store growth against the undeniable premium valuation multiples currently attached to the equity. The structural advantages of the flexible, high-velocity real estate model position the company uniquely within the fiercely competitive broader beverage and quick-service restaurant sector.

The upcoming 6 May 2026 earnings call will serve as a critical short-term catalyst, providing exact same-shop sales growth metrics and the initial financial impacts of the food menu rollout. With a firm, clearly articulated management target of 2,029 locations by 2029 and an implied 33% upside from Wall Street analysts, the execution runway remains vast and highly compelling.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own thorough research and consult with licensed financial professionals before making any investment decisions. Past performance does not guarantee future results, and forward-looking financial projections remain subject to evolving market conditions.

Dutch Bros' rapid expansion is driven by its efficient drive-thru-only model, which requires smaller real estate footprints and less capital, allowing for faster construction and operational leverage.

Investors should monitor the upcoming Q1 2026 earnings report for Average Unit Volume data on the food menu rollout and track progress toward the 2,029 store target by 2029.

Dutch Bros stock trades at a premium valuation due to its hyper-growth trajectory, strong revenue growth projections, the ongoing nationwide food menu expansion, and its successful customer loyalty program.

The nationwide food menu is designed to increase average transaction values by attaching food items to beverage orders and attracting new customers during traditionally slower afternoon hours, boosting overall unit volumes.