Retail Investor Trends: Analysing the 2026 Flight to Global ETFs

2 mins ago

Celsius Holdings (CELH) has delivered massive historical revenue expansion, while Dutch Bros (BROS) steadily advances towards a stated domestic capacity of 7,000 retail locations. Evaluating the investment case for Celsius versus Dutch Bros stock requires analysing two entirely different business models operating within the same consumer sector.

In late April 2026, Celsius is consolidating its packaged goods dominance following its acquisition of Alani Nu, capitalising on expanding distribution networks. Meanwhile, Dutch Bros is actively battling commodity cost pressures while continuing to open hundreds of physical drive-thru sites across the United States.

Consensus estimates project an earnings per share jump for Celsius by 2028. This growth profile presents a stark contrast to the premium valuation markets have assigned to the aggressive, predictable retail expansion of Dutch Bros.

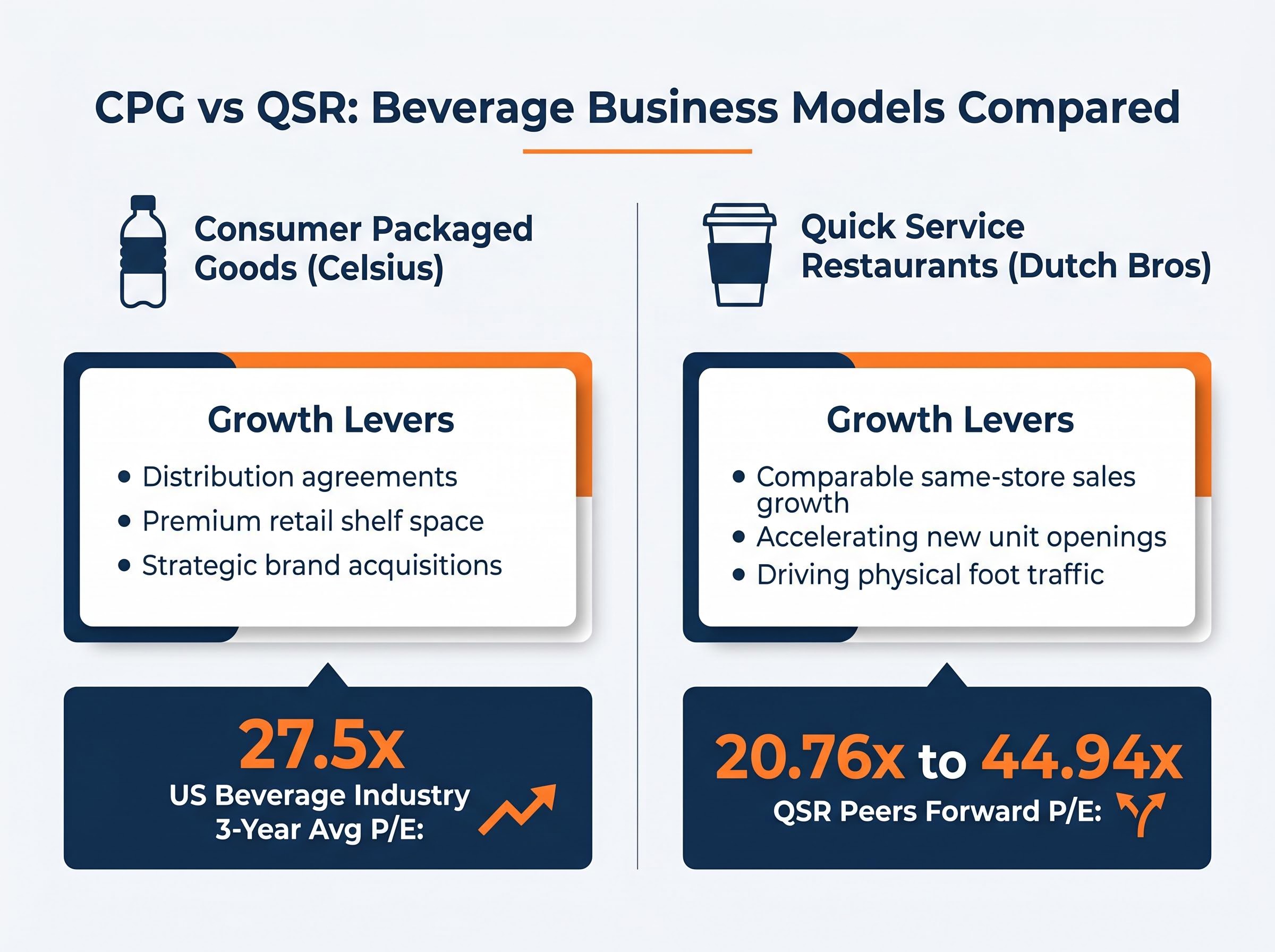

Before comparing specific stock metrics, investors must establish a framework for evaluating a consumer packaged goods brand against a physical retail chain. Celsius operates a traditional packaged goods model, relying on strategic distribution partnerships and retailer shelf space to generate scale without heavy real estate investments. Dutch Bros operates as a quick-service restaurant, functioning as a real estate and logistics machine that requires heavy capital expenditure to construct dedicated drive-thru facilities.

The fundamental differences in these structures dictate different valuation benchmarks. The three-year average price-to-earnings ratio for the broader United States beverage industry sits at 27.5x. In contrast, quick-service restaurant peers typically trade at multiples between 20.76x and 44.94x forward earnings, reflecting the predictable cash flows of physical retail footprints.

The NYU Stern valuation datasets offer a comprehensive historical baseline for these sector multiples, confirming that traditional dining and quick-service operations consistently command higher premiums than their packaged beverage counterparts due to tangible asset backing.

The primary growth levers for each business model separate their specific investment cases:

Consumer Packaged Goods (Celsius): Growth relies on distribution agreements, securing premium retail shelf space, and executing strategic brand acquisitions. Quick Service Restaurants (Dutch Bros): Expansion depends on comparable same-store sales growth, accelerating new unit openings, and driving consistent physical foot traffic.

The strategic buyout of Alani Nu fundamentally altered the revenue trajectory for Celsius Holdings. By bringing a highly complementary functional beverage brand into its portfolio, Celsius expanded its demographic reach and created immediate revenue synergies. This expanded product suite leverages the company’s powerful distribution alignment with PepsiCo, acting as a direct catalyst for domestic dominance.

Rapid functional nutrition volume growth has recently rewarded other packaged health brands with significant market premiums, suggesting strong investor appetite for successful consolidators in the wellness space.

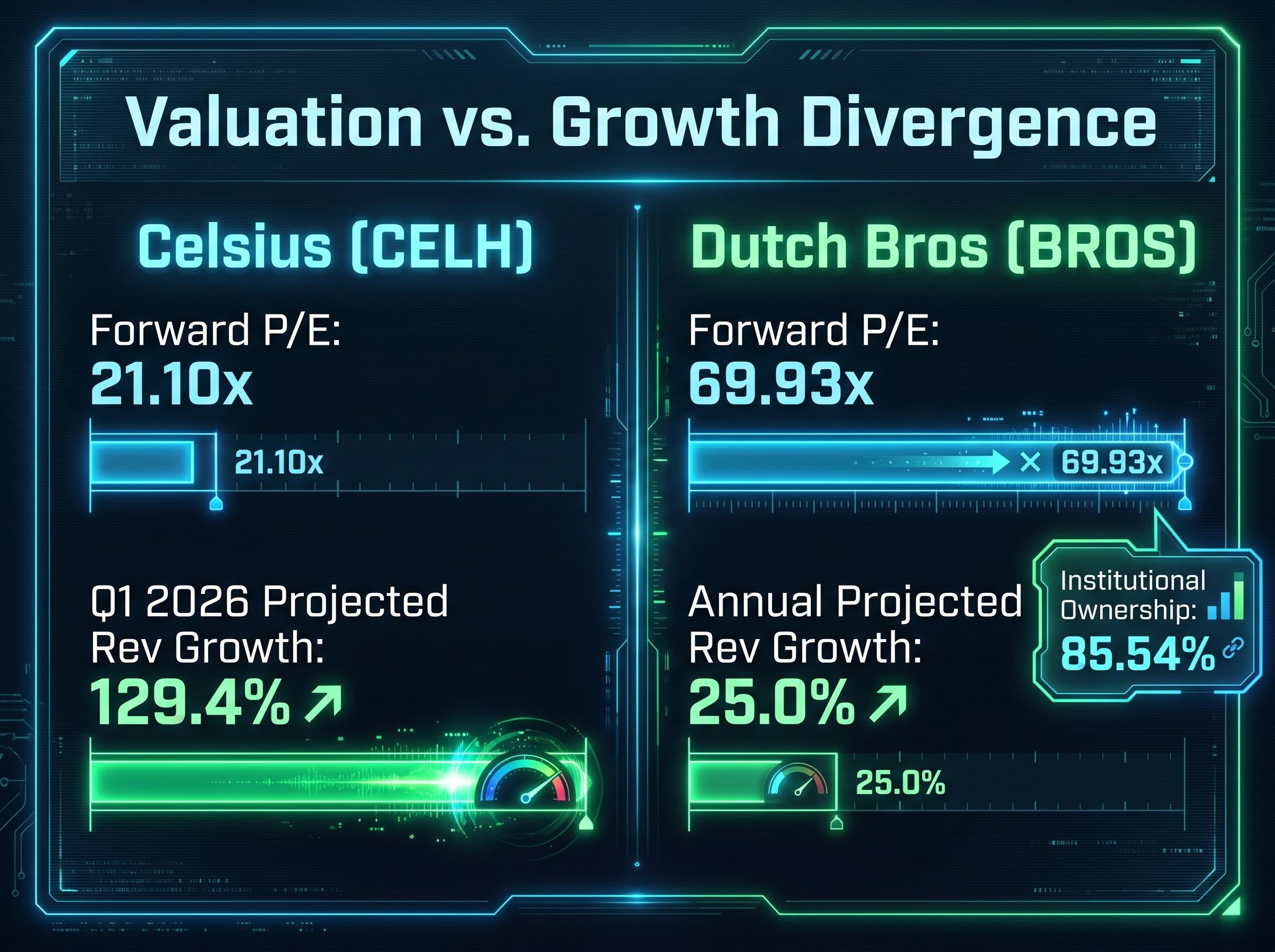

The impact of this consolidated portfolio is visible in near-term projections. Analysts forecast an aggressive ongoing expansion, estimating Q1 2026 revenue growth of 129.4 percent year-on-year.

Consensus Revenue Forecast “First-quarter 2026 estimates project 129.4 percent year-on-year revenue growth for Celsius, demonstrating the immediate top-line impact of the Alani Nu integration and expanded distribution networks.”

Looking further ahead, consensus estimates forecast top-line expansion between 2026 and 2028. These revenue increases are expected to flow through to the bottom line, with diluted earnings per share anticipated to jump by 2028. Currently, 95 percent of company revenue is generated in North America, highlighting the domestic concentration of this rapid growth.

While the domestic market provides the current foundation, international markets offer the required runway to achieve the 2028 revenue projections. Celsius is actively advancing an ongoing push into European nations, New Zealand, and Australia. These emerging distribution initiatives provide the structural volume capacity needed to sustain high double-digit growth expectations over the coming years.

While Celsius relies on distribution contracts, Dutch Bros derives its valuation from physical footprint momentum and the predictability of site-level economics. The company executes an aggressive nationwide storefront expansion strategy, committing heavy capital expenditure to construct dedicated drive-thru facilities. This infrastructure-heavy model offers highly predictable revenue scaling, provided that comparable retail site revenues maintain their historical consistency.

Management guidance points to steady top-line generation, with 2026 full-year revenue expected to sit between $2.0 billion and $2.03 billion. Future sales catalysts extend beyond simply opening new doors, as the potential introduction of edible items across the network could increase average transaction values.

However, World Coffee Portal industry analysis suggests that expanding food programs often introduces new profitability challenges for beverage-first chains, as the added complexities of food waste and increased labour requirements can offset top-line gains.

The timeline for the company’s real estate rollout involves several specific milestones:

This methodical expansion translates physical store openings into projected revenue predictability. It allows investors to accurately value the tangible real estate assets and localised consumer habits backing the company.

A direct analysis of consensus estimates reveals a distinct divergence between the growth profiles and current market valuations of these two equities. Celsius currently trades at a forward price-to-earnings ratio of 21.10x, a surprisingly attractive multiple given its projected earnings expansion. In contrast, Dutch Bros trades at a substantial premium, carrying a forward price-to-earnings ratio of 69.93x.

The pricing gap becomes particularly notable when contrasting the near-term revenue trajectories. Celsius is projected to deliver triple-digit quarterly revenue growth estimates in early 2026, while Dutch Bros management has guided for approximately 25 percent annual growth. However, the premium attached to Dutch Bros equity is supported by heavy institutional ownership, which currently stands at 85.54 percent.

| Company | Forward P/E | 2026 Revenue Growth Est. | Consensus Price Target |

|---|---|---|---|

| Celsius (CELH) | 21.10x | 129.4% (Q1 YoY) | $65.40 (High: $85.00) |

| Dutch Bros (BROS) | 69.93x | 25.0% (Annual) | $75.96 (High: $95.00) |

This financial reality presents a unique commercial dynamic for investors. The faster-growing consumer packaged goods company currently trades at a significantly cheaper forward valuation multiple than the slower-growing retail operator.

For investors wanting to model alternative coffee sector valuations, our detailed coverage of Starbucks earnings projections examines how margin expansion timelines and operational productivity targets affect the long-term pricing of legacy retail operators.

Optimistic growth projections for both companies are counterbalanced by specific margin pressures and sector vulnerabilities. Celsius faces heavy competition in the functional beverage space, where emerging brands continuously threaten to capture market share and retail shelf space. Maintaining the rapid sales velocity required to justify its forward projections demands flawless execution in an increasingly saturated category.

New entrants are aggressively building scalable brand platforms targeting trending wellness categories, creating continuous shelf space battles for established incumbents.

Dutch Bros faces a different set of immediate operational hurdles, primarily driven by commodity input costs. The company expects same-shop sales growth to normalise between 3 percent and 5 percent for 2026. This moderation could severely test the resilience of the premium valuation multiple currently assigned to the stock.

Investors must evaluate both isolated operational risks and broader macroeconomic headwinds:

Isolated Risks (Dutch Bros): Near-term commodity cost pressures are severe, with an expected 200 basis points of cost-of-goods-sold impact in Q1 2026 due to rising coffee costs, settling at an 80 basis points pressure for the full year. Shared Risks (Industry-Wide): Both business models remain vulnerable to broader consumer discretionary spending slowdowns, as premium functional beverages and out-of-home coffee purchases are often early casualties in constrained household budgets.

Evaluating the forward pathways for these equities requires matching their specific growth mechanisms to appropriate investment timelines. Celsius offers a compelling, acquisition-bolstered growth narrative supported by international expansion, trading at a cheaper forward multiple relative to its near-term revenue generation. Conversely, Dutch Bros provides highly predictable physical asset expansion and steady retail cash flows, though investors must pay a steep premium for this visibility.

Market dynamics suggest that Celsius appeals to growth portfolios prioritising near-term earnings acceleration and international scale potential. Dutch Bros aligns more closely with strategies seeking methodical, real estate-backed compound growth over a multi-year horizon.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Celsius operates as a consumer packaged goods company, focusing on distribution and strategic brand acquisitions, while Dutch Bros is a quick-service restaurant chain, centered on physical drive-thru expansion and real estate investments.

The Alani Nu acquisition fundamentally altered Celsius's revenue trajectory by expanding its product portfolio and demographic reach, directly catalyzing domestic dominance through its PepsiCo distribution alignment.

Dutch Bros aims to operate 2,000 retail shops by the end of 2029 and estimates its ultimate long-term domestic market capacity at 7,000 total establishments.

Dutch Bros commands a premium valuation due to the highly predictable cash flows and tangible asset backing of its physical retail footprint, which investors often value highly despite slower growth rates compared to Celsius's CPG model.