An objective analysis of Lululemon reveals a staggering destruction of $17 billion in shareholder equity over the past half-decade. Grounded in the reality of April 2026, the highly recognisable athletic brand faces an active proxy fight launched by founder Chip Wilson, alongside stagnant regional sales that have forced a critical reassessment of the company’s trajectory. With former Nike executive Heidi O’Neill preparing to assume leadership in September 2026, this evaluation separates the underlying business metrics from public boardroom drama. A fundamental breakdown of the brand’s current valuation provides clarity on whether the core enterprise can recover its premium market positioning.

Analyzing the 66 percent plunge in stakeholder equity

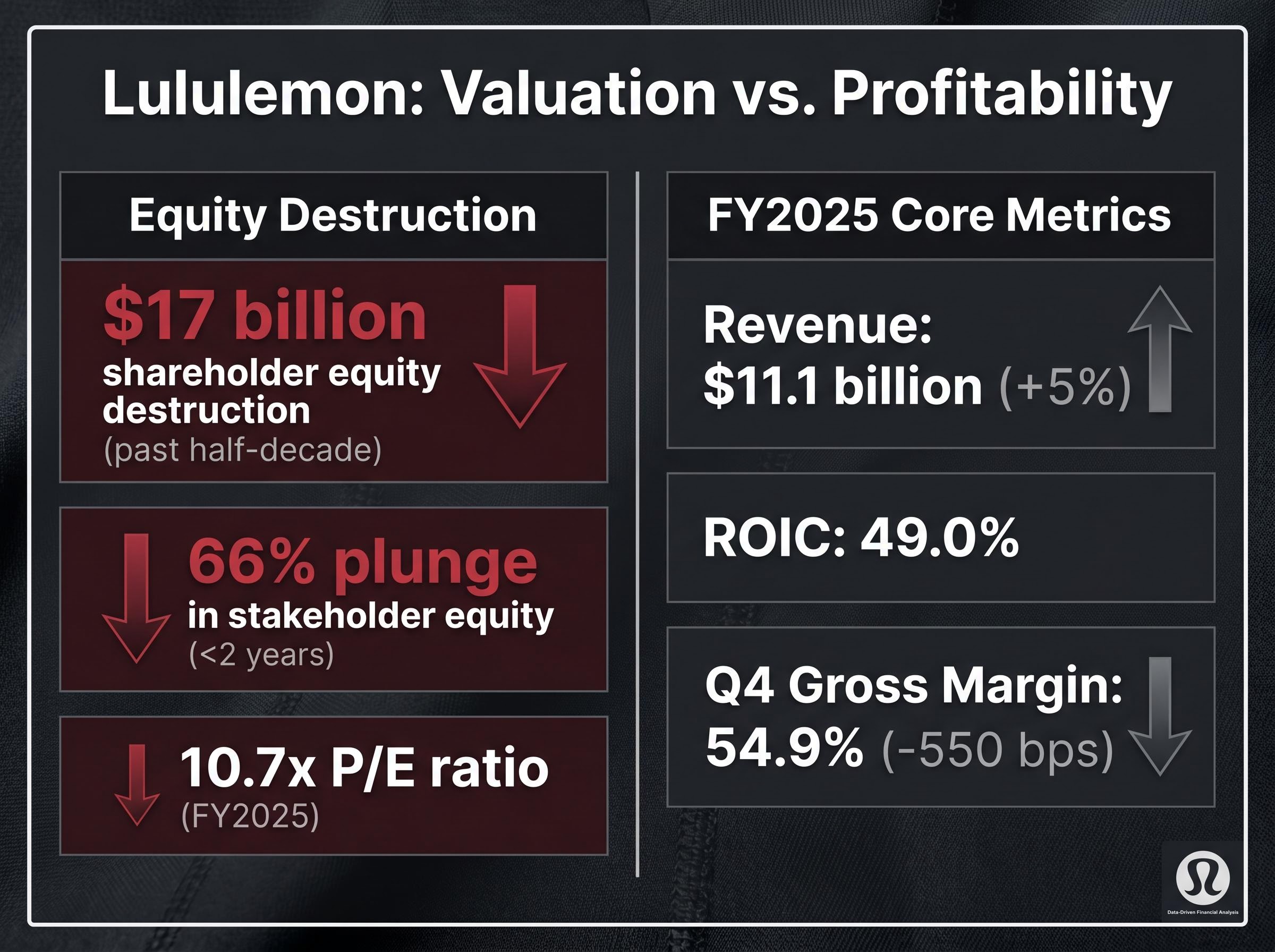

According to reports, the deterioration of stakeholder equity by 66 percent in less than two years anchors the current crisis in undeniable mathematical reality. According to reports, while the broader market has rallied, the athletic apparel manufacturer has trailed the industry midpoint by 19.5 percent over 12 months and 63.6 percent over 36 months. This underperformance is particularly striking when contrasted with the company’s still-elite underlying profitability metrics.

The current trading multiple reflects deep market scepticism regarding future growth rather than immediate insolvency. Based on FY2025 earnings, the stock currently trades at a price-to-earnings ratio of approximately 10.7x. Investors are essentially pricing the equity as a mature, low-growth retailer, heavily discounting the historical premium attached to the brand.

The fundamental trigger for this multiple compression appeared clearly in the most recent earnings data. During Q4 FY2025, the gross margin contracted by 550 basis points to 54.9 percent, signalling a loss of pricing power in a highly competitive sector.

The official Lululemon FY2025 financial results confirm this margin compression alongside a revenue figure of $11.1 billion, illustrating how top-line growth is masking underlying profitability pressures.

| Metric | FY2025 Result | YoY Change | Market Implication |

|---|---|---|---|

| Revenue | $11.1 billion | Up 5 percent | Slowing top-line momentum |

| Diluted EPS | $13.26 | Met internal targets | Earnings holding despite headwinds |

| Q4 Gross Margin | 54.9 percent | Down 550 basis points | Pricing power under pressure |

| ROIC | 49.0 percent | Maintained elite level | Core capital efficiency remains intact |

Investors must evaluate whether the current stock price represents a value trap or a deeply discounted entry point. The baseline quantitative evidence suggests the business remains highly profitable, but the market requires proof that the margin contraction is temporary rather than structural.

When big ASX news breaks, our subscribers know first

The Mechanics of Premium Athletic Valuation

Mass-market apparel economics rely on high volume and thin margins, whereas premium athletic wear valuation operates on a fundamentally different framework. High return on invested capital and expanded gross margins are entirely dependent on maintaining pricing power and brand exclusivity. When consumers perceive a brand as elite, they willingly absorb premium price points without requiring promotional discounting.

This dynamic explains why brand dilution destroys trading multiples far faster than simple revenue misses. The company achieved historically elite metrics based on this exclusivity, reporting 56 percent full-year gross margins and a 49 percent return on invested capital for FY2025. To justify returning to a premium valuation, the enterprise must defend its 21.2 percent share of the highly competitive US athleisure market against emerging premium competitors.

“The organisation’s struggles stem directly from executives failing to defend the athletic brand’s high-end status against mass-market dilution.”

Understanding this theoretical framework clarifies why seemingly minor brand decisions carry massive financial consequences. If the consumer perception of exclusivity fades, the pricing power evaporates, and the elite gross margins will inevitably revert to industry averages.

For readers wanting to understand the macroeconomic backdrop impacting discretionary apparel spending, our deep-dive into US recession risk and consumer strength details how depleted savings rates are forcing shoppers to pull back from premium brands.

Regional Stagnation and the Cost of Brand Dilution

The abstract financial losses stem directly from concrete operational choices and troubling revenue trends across the Americas. According to reports, for eight consecutive quarters, the company has reported stagnant or dropping identical-location revenue across North and South America. This regional stagnation represents the core operational failure driving current investor anxiety.

Internal product development cycle issues have severely hindered the company’s ability to respond to rapidly changing consumer tastes. Total Americas net revenue decreased 4 percent in Q4 FY2025, or 5 percent on a constant dollar basis. Peering deeper into the regional data reveals that US revenue dipped 1 percent, while Canadian revenue provided a slight offset with a 3 percent increase.

Part of this regional volume decline stems from widespread financial strain for lower-income households, which has increasingly forced aspirational shoppers out of the premium athleisure market entirely.

Assessing the Disney Partnership Strategy

The controversial collaboration with The Walt Disney Company exemplifies the tension between driving immediate engagement and sacrificing long-term premium positioning. The decision to launch a dedicated retail presence in Downtown Disney in December 2025 generated significant industry debate. By associating a premium athletic label with a mass-market entertainment conglomerate, management prioritised immediate foot traffic over brand exclusivity.

“While the entertainment collaboration offers immediate consumer visibility, it raises serious questions regarding whether an upscale athleisure brand should associate so closely with mass-market family tourism properties,” noted an analyst.

By analysing these specific corporate decisions, market participants gain insight into management’s strategic mindset. The ultimate question remains whether the current leadership framework is capable of reversing the brand’s domestic decline without further compromising its upscale appeal.

Inside the 2026 Proxy Fight and Leadership Overhaul

The analytical lens must shift from the storefront to the boardroom, framing the current proxy battle as a direct reaction to the strategic failures previously outlined. Launched by founder Chip Wilson ahead of the 2026 annual shareholder gathering, the campaign focuses on alleged structural governance complaints and perceived conflicts of interest. According to reports, Wilson specifically highlights that four existing board members possess overlapping professional backgrounds with Advent International L.P.

The structural governance mechanics are central to the dispute, specifically the staggered board election framework. According to reports, only one-tenth of S&P 500 corporations maintain this staggered structure, which activists argue insulates directors from immediate shareholder accountability. Standstill negotiations between the parties collapsed recently.

The activist campaign has proposed three independent director nominees to execute a turnaround strategy:

- According to reports, Marc Maurer, a candidate credited with increasing corporate income fourfold during his tenure at On Holding AG.

- Laura Gentile, an executive offering extensive experience in sports media and brand positioning.

- According to reports, Eric Hirshberg, a former Activision executive who previously oversaw a 500 percent equity surge.

Corporate governance directly impacts capital allocation and strategic direction. The introduction of new Chief Executive Officer Heidi O’Neill, with an upcoming start date in September 2026, represents a critical turning point. Understanding this power struggle provides investors with a precise timeline for potential catalysts that could rapidly alter the stock’s trajectory.

Extensive financial news coverage regarding Heidi O’Neill’s executive appointment highlights the intense pressure she will face from founder Chip Wilson and his slate of independent director nominees.

Evaluating the 2026 Action Plan and Global Defense Strategy

To counter the activist narrative, the interim leadership team has deployed a defensive strategy anchored by the 2026 Action Plan. The core of this initiative is Agile Merchandising, an operational goal aimed at cutting product development cycles from 18 months down to 12 months. Management targets a boost in Spring 2026 sell-through by 25 percent year-over-year, aiming to prove they can accelerate innovation.

Similar to the strategic turnaround initiatives recently deployed by major food and beverage retailers, this acceleration of innovation requires flawless execution to successfully re-engage alienated core customers.

Investors must weigh these forward-looking targets against anticipated short-term pain, including a projected double-digit profit dip in Q1 2026. Total revenue guidance for FY2026 is set between $11.35 billion and $11.50 billion, representing modest growth of 2 to 4 percent. The strategy heavily relies on international expansion to mask domestic struggles, evidenced by Q4 FY2025 international revenue growth of 17 percent.

Past performance does not guarantee future results, and financial projections surrounding the 2026 Action Plan are subject to execution risks and changing market conditions. The distinct pillars of the turnaround effort include:

Inventory efficiencies designed to immediately improve working capital metrics. Supply chain acceleration targets to reduce the time from product conception to retail floors. * Aggressive international real estate expansion heavily reliant on consumer adoption in the China market.

This forward-looking synthesis requires investors to balance the immediate turnaround efforts against structural market headwinds. The fundamental question is whether accelerated international growth can successfully insulate the balance sheet while domestic brand erosion is addressed.

The True Cost of Corporate Misalignment

The core tension at the heart of this enterprise remains the gap between its historically elite legacy metrics and its current operational realities in the Americas. A business generating nearly a 50 percent return on invested capital rarely trades at a 10.7x multiple unless the market anticipates a structural collapse in pricing power. The resolution of the 2026 proxy fight and the success of the incoming Chief Executive will ultimately dictate whether the $17 billion valuation gap is a permanent wealth destruction event or a recoverable misstep.

Potential investors must monitor inventory turnover rates and domestic margin stabilisation in the coming quarters to validate any turnaround thesis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.