Nasdaq Jumps 1.3% as AI Chips Lead Back-to-Back SOX Surge

1 hr ago

Regeneron reported a substantial non-GAAP EPS beat for the first quarter of 2026, surpassing Wall Street expectations. Alongside this earnings beat, the company immediately announced a massive $3.0 billion share repurchase programme.

This dual announcement in April 2026 highlights a complex operational reality for the biotechnology company. While analysts celebrated the top-line performance, underlying manufacturing challenges in Ireland forced a downward revision in full-year margin guidance.

Corporate leadership is actively balancing these physical operational disruptions and product life cycle transitions with aggressive capital allocation. This Regeneron earnings analysis examines how management uses specific financial tools to protect shareholder value. The ongoing strategy demonstrates how biotechnology firms can fund long-term innovation even during periods of temporary margin compression.

The top-line figures for the first quarter present a clear financial beat against analyst consensus. Total corporate income reached $3.6 billion, marking a 19% year-on-year increase compared to early 2025. This revenue performance pushed non-GAAP diluted earnings per share to $9.47.

Wall Street analysts had projected an earnings per share of $8.90 prior to the release. The final result represents a decisive beat that supported an initial upward valuation in early trading hours. Beneath these headline numbers, the company absorbed immediate financial deductions.

Evaluating these significant quarterly reports often involves analyzing options pricing during earnings season to see how market makers anticipate volatility and price in potential surprises before the numbers are released.

An acquired in-process research and development charge of $102 million pre-tax was applied during the quarter. This specific charge reduced the GAAP diluted earnings per share by $0.82, pulling down the unadjusted bottom line. Investors must separate the adjusted earnings triumph from these foundational financial realities to accurately assess the company’s valuation.

| Metric | Q1 2025 Actuals | Q1 2026 Estimates | Q1 2026 Actual Results |

|---|---|---|---|

| Total Corporate Income | ~$3.02 billion | N/A | $3.6 billion |

| Non-GAAP Diluted EPS | N/A | $8.97 | $9.47 |

| GAAP EPS Impact from IPR&D | N/A | N/A | Down $0.82 |

The quarterly financial reports carry the weight of a concrete supply chain event at the company’s Limerick manufacturing facility in Ireland. Unanticipated repairs forced a temporary interruption of bulk manufacturing production during the first few months of the year. This bottleneck created immediate overhead expenses and resulted in discarded inventory on the production floor.

Management successfully navigated the disruption to avoid interrupting end-user product availability. The physical shutdown, however, exacted a direct toll on profitability metrics for the quarter. GAAP gross margins dropped, leading to a downward revision in full-year margin guidance.

This compression highlights the critical difference between a temporary operational hurdle and a structural business decline. The loss of margin was driven entirely by facility repairs rather than a failure in product pricing power.

The margin suppression from the Limerick facility will persist into the second quarter. Initial production safely resumed in April 2026, but standard production volumes are not expected to be fully restored until the end of Q2.

This timeline forced executives to adjust their forward-looking forecasts. The company lowered full-year 2026 GAAP gross margin guidance to 77%-78%, down from the initial projection of 79%-80%. The revision signals to investors that overhead expenses will continue to drag on profitability until standard operations normalise in the second half of the year.

For investors looking to weigh these operational headwinds against the company’s long-term commercial strengths, our detailed coverage of Regeneron’s Q1 margin pressures examines the specific impact of the EYLEA franchise transition and the robust growth from the Sanofi partnership.

Corporate finance teams frequently use share repurchases as a strategic shock absorber against temporary operational turbulence. A share repurchase programme is a corporate action where a company buys back its own stock from the open market. This mechanism mathematically reduces the total number of outstanding shares available to the public.

The deployment of internal capital aligns with NBER research on corporate payout strategies, which highlights how management teams routinely leverage market repurchases during transitional periods to stabilize per-share metrics while resolving internal supply chain hurdles.

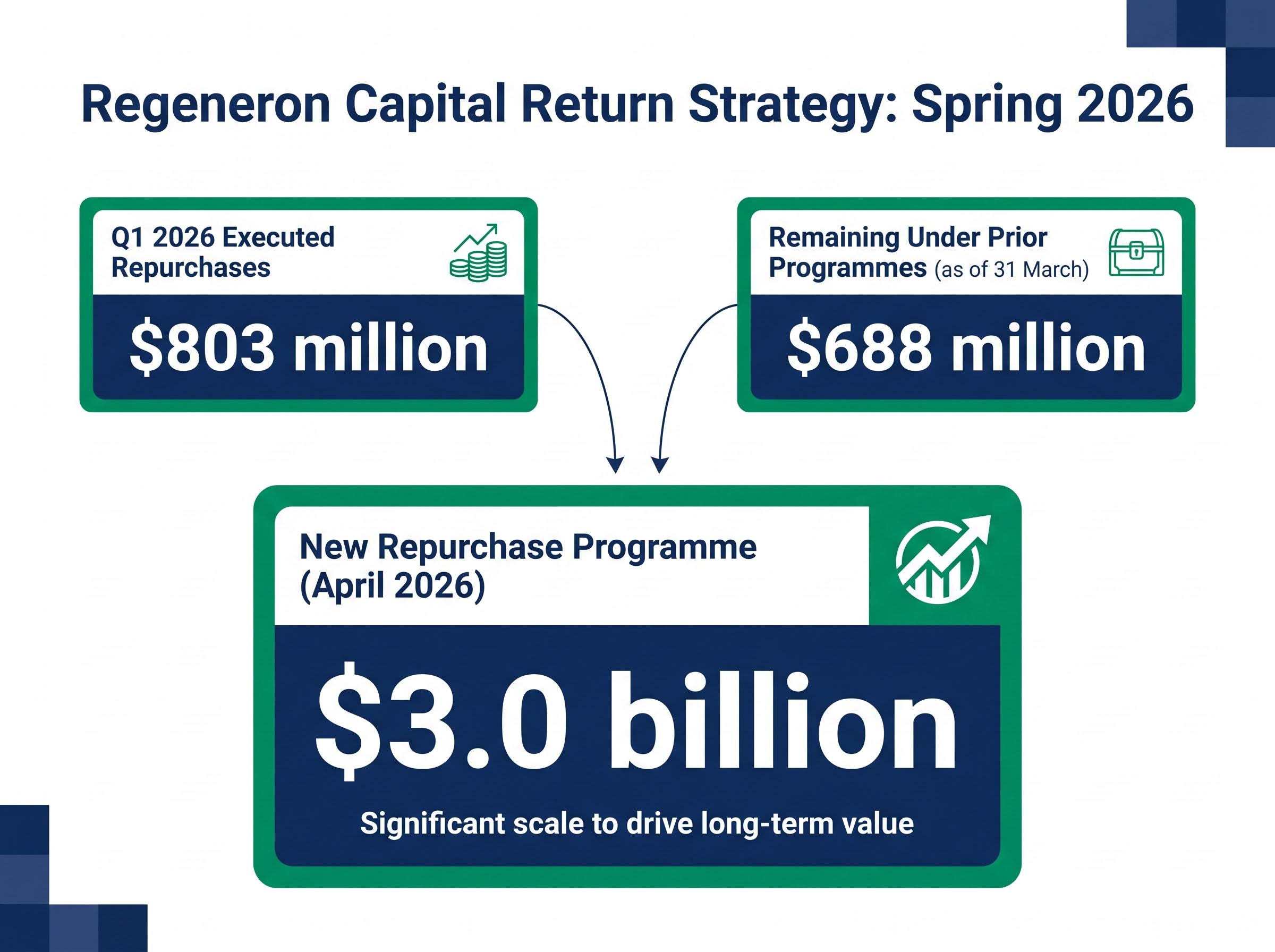

Management deployed this strategy actively during the Limerick margin pressures. The company repurchased $803 million worth of common stock during the first quarter of 2026. As of 31 March, there was $688 million remaining under prior repurchase programmes.

In a deliberate signal of corporate confidence to the U.S. markets, the board authorised a new $3.0 billion share repurchase programme in April 2026. This aggressive capital return strategy artificially supports earnings per share during difficult quarters, buffering the impact of lowered gross margins.

The step-by-step mechanics of this financial strategy work as follows:

By authorising the new $3.0 billion programme, leadership has guaranteed substantial capital support for the stock price through the remainder of the Limerick facility recovery.

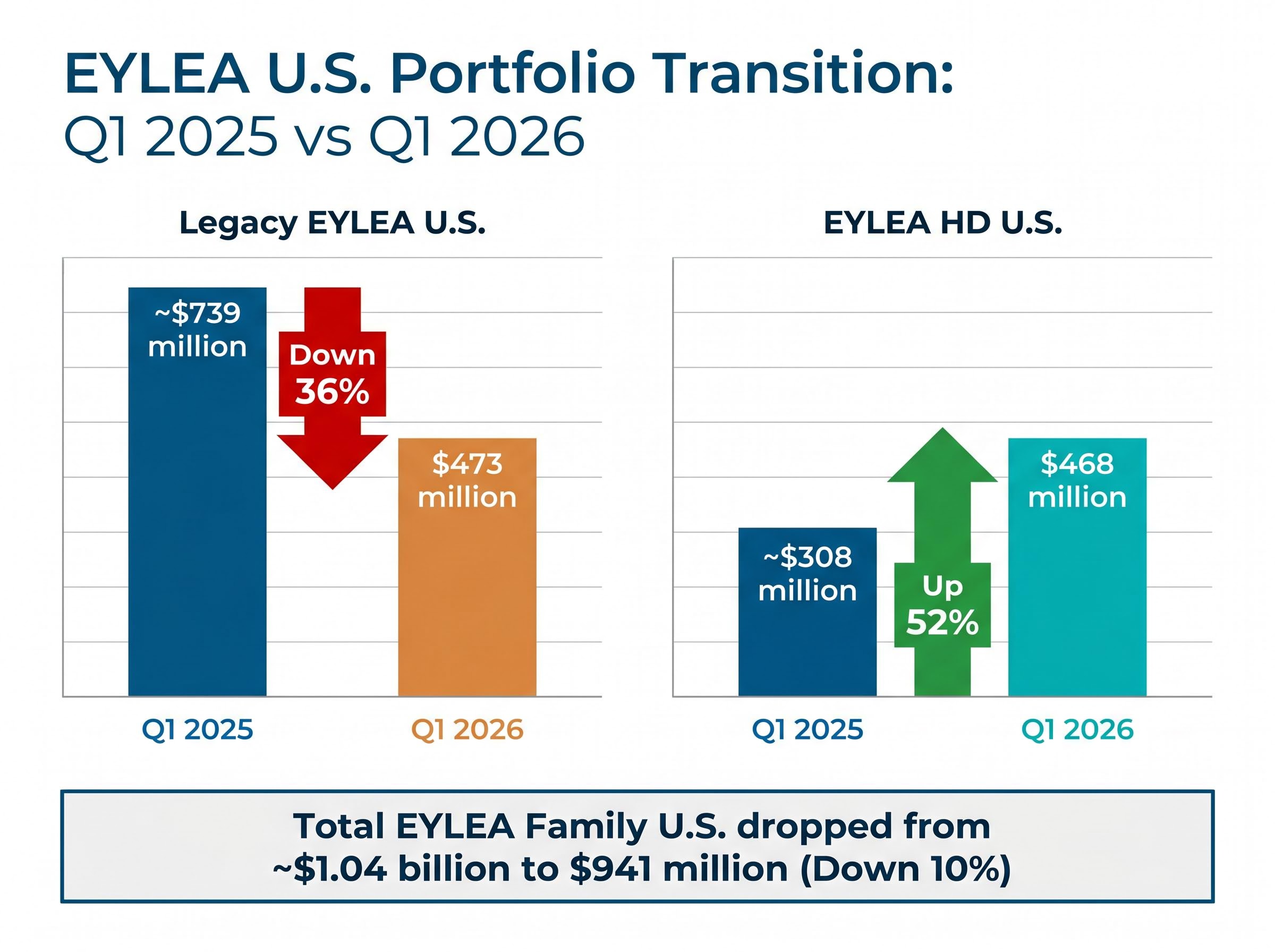

A critical competitive rotation is occurring within the company’s anti-VEGF portfolio across the U.S. market. Total U.S. EYLEA family sales dropped 10% year-on-year to $941 million, indicating broader competitive pressures in the ophthalmology sector. This aggregate figure conceals a rapid internal transition between specific product formulations.

Legacy EYLEA revenue fell to $473 million as prescribing physicians rotated patients to newer treatments. The newer EYLEA HD formulation successfully offset much of this decline, surging 52% to reach $468 million in net U.S. sales. Global net sales for the HD formulation performed even stronger, reaching $800.9 million total.

Outside the EYLEA franchise, a massive financial safety net exists through the Sanofi partnership. According to external reports, worldwide Dupixent purchases jumped 33% to $4.9 billion. This widespread global adoption generated direct partnership revenue for the quarter, providing necessary cash flow during the product transition.

The underlying strength of this safety net is evident in Sanofi’s Q1 financial disclosures, which document robust global prescription trends across multiple approved indications for the partnered immunology asset.

| Metric | Q1 2025 Revenue | Q1 2026 Revenue | Growth Percentage |

|---|---|---|---|

| Legacy EYLEA U.S. | ~$739 million | $473 million | Down 36% |

| EYLEA HD U.S. | ~$308 million | $468 million | Up 52% |

| Total EYLEA Family U.S. | ~$1.04 billion | $941 million | Down 10% |

The executive team must constantly balance funding massive ongoing research initiatives against the immediate demand for capital returns. The combination of strong partnership revenue from Dupixent and aggressive share buybacks provides the financial runway required to weather the Limerick margin squeeze.

While established companies can rely on robust commercial partnerships to generate cash, early-stage peers often execute large-scale capital raises to fund their precision drug pipelines through critical efficacy readouts without relying on immediate commercial revenue.

This buffer is necessary for sustaining the distinct therapeutic assets currently undergoing clinical evaluation. Investors will closely monitor the Ireland facility, with full operations expected to be restored by the end of Q2 2026. If manufacturing normalises on schedule, the gross margin pressure will lift, allowing more capital to flow directly into the clinical pipeline.

Executive Strategy Summary Management data indicates that the combination of partnership revenue and active capital returns will allow the company to advance its 50-asset clinical pipeline without interruption, successfully absorbing the temporary overhead costs from the Limerick facility.

This framework provides a clear perspective on the company’s operational trajectory through the remainder of the year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

A share repurchase program is a corporate action where a company buys back its own stock from the open market, reducing the total number of outstanding shares and often supporting earnings per share during transitional periods.

Regeneron lowered its full-year 2026 GAAP gross margin guidance due to unanticipated repairs and temporary production interruptions at its Limerick, Ireland manufacturing facility, which increased overhead expenses.

Regeneron is balancing operational challenges by using a $3.0 billion share repurchase program to buffer per-share metrics and leveraging robust partnership revenue from Dupixent to fund its 50-asset clinical pipeline without interruption.

While total U.S. EYLEA family sales dropped 10% year-on-year in Q1 2026, the newer EYLEA HD formulation saw a significant 52% surge in U.S. sales, largely offsetting the decline from the legacy EYLEA product.