SocGen Quadruples Commodities to 20% in June Portfolio Shift

10 hrs ago

Wall Street is currently witnessing an unprecedented capital deployment cycle, where major technology firms are expected to spend upwards of $600 billion this year alone on artificial intelligence infrastructure. As of late April 2026, the market focus has shifted away from the software companies building language models toward the physical hardware ecosystem powering them.

This rotation makes component suppliers the primary beneficiaries of the current spending spree. It also creates a critical moment for investors evaluating AI stocks and broader technology portfolios. The gap between the scale of this physical infrastructure rollout and previous technology cycles is historically significant.

This analysis provides a clear framework for understanding how massive hyperscaler investments flow through the semiconductor supply chain. It details how capital expenditure translates into hardware revenue and how to evaluate the emerging risks threatening this historic market rally.

Understanding the sheer volume of guaranteed capital flowing into the sector gives investors a reliable baseline for evaluating the revenue pipelines of hardware suppliers over the next 18 to 24 months. The current infrastructure supercycle operates on a simple principle. Software ambitions dictate hardware purchasing.

To train and run increasingly complex models, technology companies require massive arrays of specialised processors, memory, and networking equipment. This demand directly fills the order books of semiconductor fabrication plants and component designers.

This structural change in Big Tech priorities is evident in projected operating cash flow allocations. According to company data, forecasts show infrastructure expenditures expanding from 50% of operating cash flow in 2024 to approximately 90% by 2027. This represents a permanent reallocation of corporate resources rather than a temporary trend.

Companies are committing capital well before the software applications are fully commercialised.

The sheer scale of these financial commitments through the end of the calendar year and into 2027 is staggering. According to aggregate consensus estimates, total hyperscaler capital expenditures will range from $600 billion to $750 billion in 2026.

A detailed Futurum Group infrastructure analysis validates these massive projections, confirming that data centre and custom silicon allocations are driving an unprecedented reallocation of corporate operating cash flow.

Alphabet is guiding for $175 billion to $185 billion in spending. Amazon is projecting infrastructure investments reaching approximately $200 billion. Meta is committing between $115 billion and $135 billion to secure its model training capabilities.

| Technology Giant | 2026 Estimated Capex | Infrastructure Focus Area |

|---|---|---|

| Amazon | ~$200 billion | Data centre expansion and networking |

| Alphabet (Google) | $175 billion to $185 billion | Custom silicon and compute capacity |

| Meta | $115 billion to $135 billion | AI model training infrastructure |

This massive capital outlay creates a highly visible revenue pipeline for the hardware sector. Financial analysts are tracking these corporate budgets as leading indicators for semiconductor earnings. The capital deployed by these technology giants effectively guarantees production volume for the world’s leading chip fabricators.

The direct correlation between these announced infrastructure budgets and the explosive valuation growth of downstream chip manufacturers is unmistakable. Component manufacturers are translating hyperscaler spending directly into tangible profitability and shareholder value.

This dynamic separates the specific, outsized gains seen within the semiconductor sector since the beginning of the year from the broader market recovery.

Investors are heavily rewarding the firms physically building the architecture of the future.

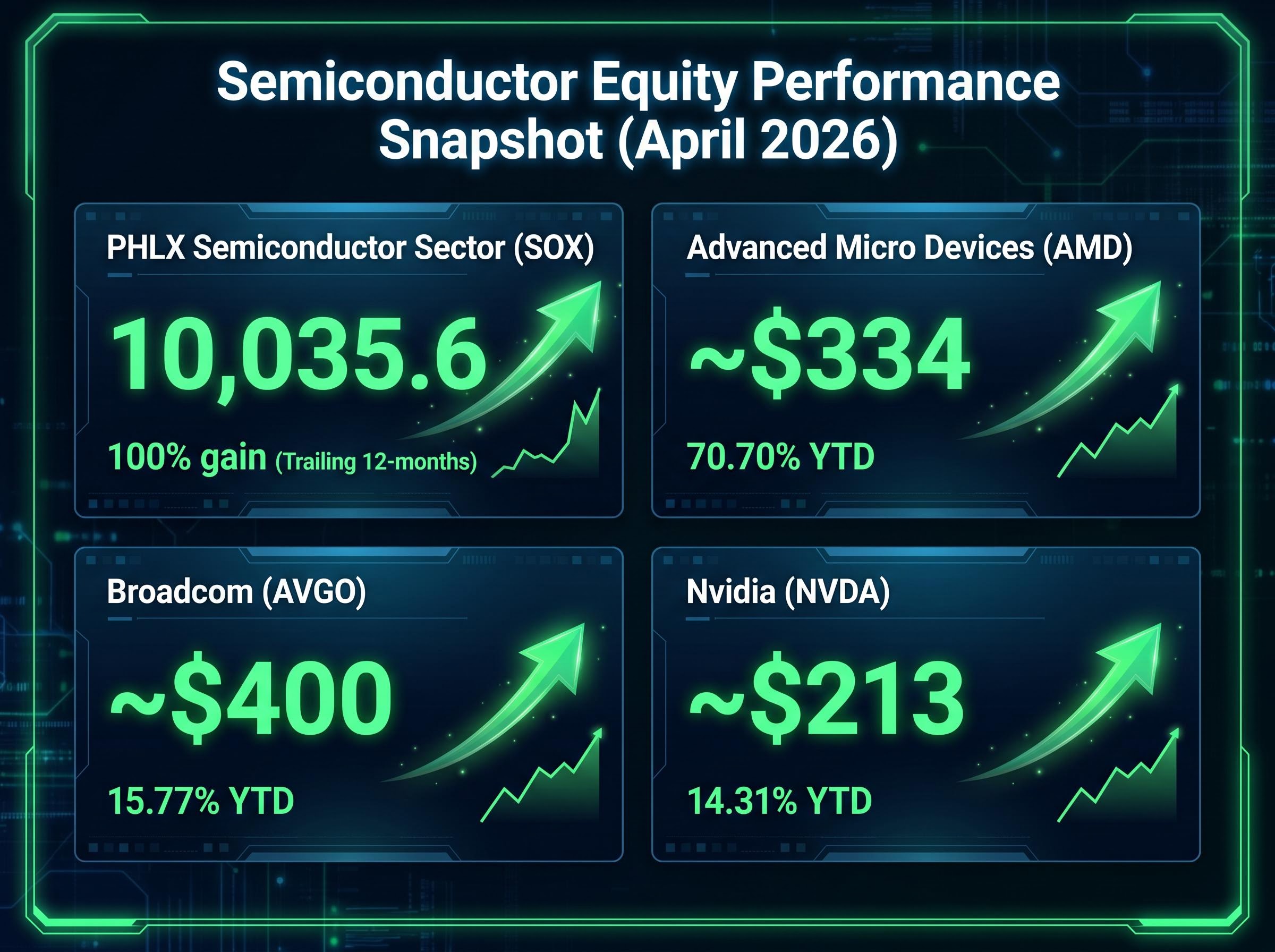

The PHLX Semiconductor Sector (SOX) is currently trading near 10,035.6, representing massive year-to-date gains. According to market data, this index has achieved a 100% gain over the trailing twelve months, reflecting the sustained momentum of the infrastructure buildout.

By connecting abstract spending announcements to concrete equity performance, readers can identify which segments of the supply chain capture the most commercial value. The following metrics highlight the specific year-to-date performance of major semiconductor equities as of April 2026:

Advanced Micro Devices (AMD): Surged 70.70% year-to-date to approximately $334. Broadcom (AVGO): Advanced 15.77% year-to-date to roughly $400. * Nvidia (NVDA): Up 14.31% year-to-date, trading near $213.

These individual corporate beneficiaries reveal how each firm captures a different segment of the infrastructure buildout. Nvidia and Advanced Micro Devices continue to dominate the raw compute processing demand required for model training. Their graphics processing units remain the foundational components of the modern data centre.

Meanwhile, networking specialists like Broadcom capture the vital connectivity requirements needed to link massive data arrays together. As data centres grow larger, the complexity of moving data between processors increases, creating a secondary revenue stream for networking suppliers.

A similar supply shock is impacting the data storage market, where major enterprise hardware vendors have completely sold out their high capacity production through the end of the year.

While hardware suppliers enjoy unprecedented revenue visibility, a single software stumble at the top of the chain can send immediate shockwaves down to these manufacturers. Friction points are emerging where software monetisation has failed to keep pace with hardware deployment expectations.

This vulnerability represents the primary near-term risk for investors holding supply chain equities.

The market requires proof that the massive capital expenditures will yield sustainable consumer applications.

The fragility of the current rally became apparent when OpenAI missed critical internal targets set for late 2025. The company failed to reach its goal of 1 billion weekly active users and fell short of its monthly revenue projections.

These misses prompted internal concerns regarding the sustainable funding of future data centres. Hardware suppliers felt the impact immediately, as investors reassessed the long-term viability of the current infrastructure expansion.

The market reaction was rapid and indiscriminate. US semiconductor equities experienced an immediate 2% to 5% pullback following these reports.

This reaction demonstrates the high sensitivity of component stocks to news from software developers. Major suppliers saw their share prices dip as institutions briefly recalibrated their forward revenue models.

Analyst Perspective on Software Friction “The recent OpenAI monetisation miss serves as a primary example of the friction between hardware availability and software revenue realisation. Sustained capital expenditure requires sustained application revenue, and any delay in the latter will immediately reprice the former.”

Hardware valuations remain tethered to the commercial success of the software platforms they support. Investors must protect their portfolios by monitoring these software monetisation rates as closely as semiconductor order books.

For readers wanting to understand the specific unit economics challenging these software models, our detailed coverage of escalating inference costs examines how high query expenses threaten to make generative applications fundamentally unprofitable and derail future spending plans.

Beyond short-term market reactions, financial analysts are actively debating the potential for an infrastructure bubble versus a sustained growth cycle. Consensus analyst perspectives confirm there are no signs of a systemic hardware bubble yet.

Current investments are generating tangible positive returns despite the heavy capital requirements. Technology firms are translating their infrastructure purchases into measurable efficiency gains and new product lines.

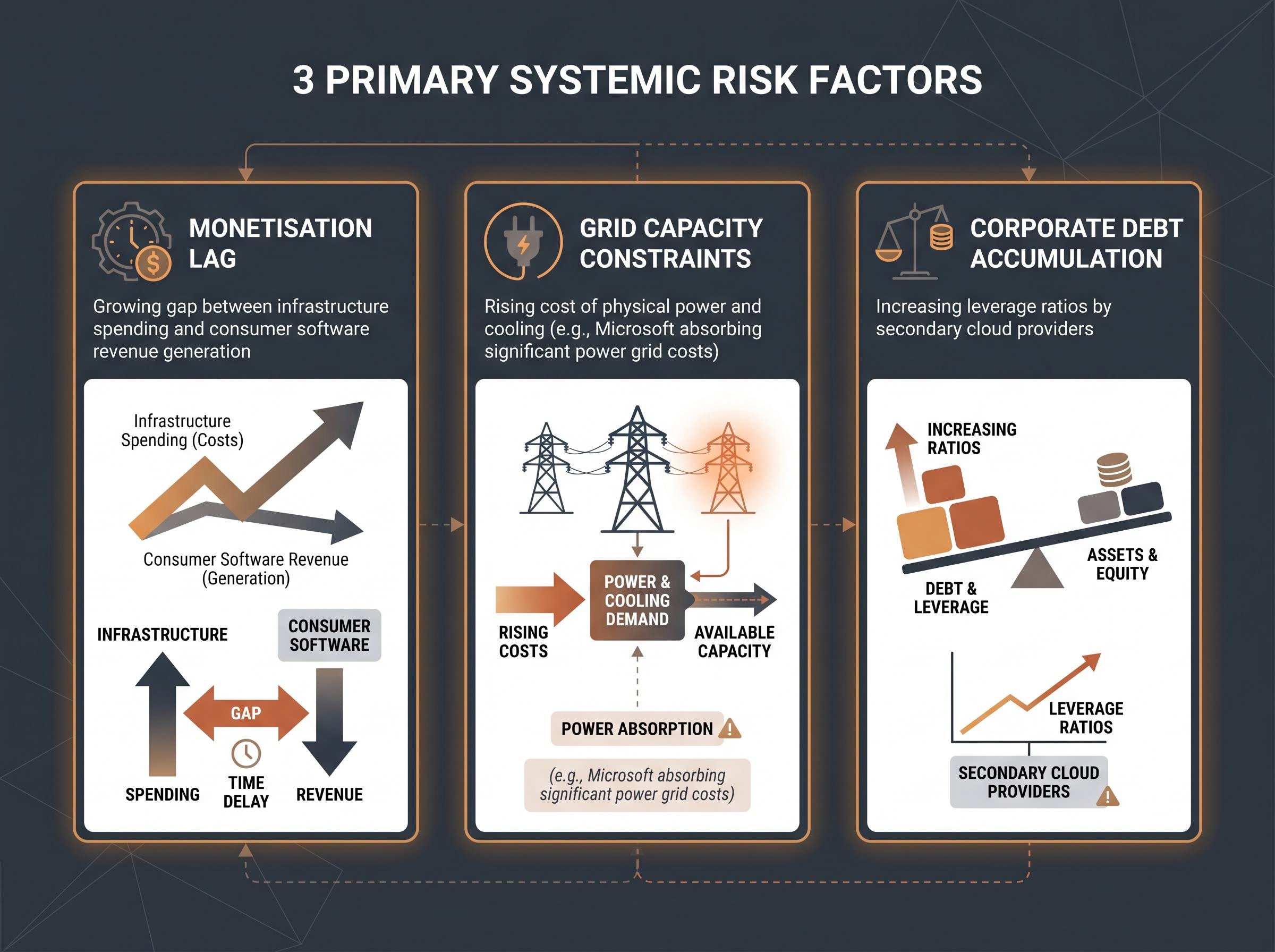

However, the distinction between isolated disruptions and systemic sector risk is narrowing as physical capacity constraints emerge. Microsoft is currently absorbing significant power grid costs, which increases its total capital expenditure per gigawatt of data centre capacity.

The secondary risks associated with the corporate debt accumulation required to fund these massive data facilities are also coming into focus. Data centre construction is increasingly constrained by local power availability rather than semiconductor supply.

The updated EIA electricity demand forecasts project historic four-year consumption growth driven directly by these facilities, indicating that regional utilities will struggle to provision enough power to match the hardware procurement pace.

Readers require a sophisticated framework for distinguishing between normal market corrections and genuine systemic threats. Evaluating the long-term health of the sector requires looking beyond daily share price fluctuations. Investors must monitor three primary risk factors:

These factors will dictate whether the current deployment cycle maintains its momentum into 2027. A failure in any of these three areas could force hyperscalers to aggressively reduce their hardware procurement budgets.

The core dynamic defining the remainder of 2026 is the tension between guaranteed hyperscaler spending and the growing necessity for software monetisation. Hardware suppliers possess historically strong order pipelines, but their valuations will face pressure if downstream software firms cannot demonstrate sustainable revenue models.

The market is shifting from an acquisition phase to a proof-of-concept phase.

Early cloud monetization metrics from major hyperscalers demonstrate robust initial service revenue, though the complete transition from heavy infrastructure investment to profit realization will dictate future hardware valuations.

Investors should monitor upcoming quarterly earnings reports from the major hyperscalers, specifically scrutinising forward capital expenditure guidance. Any downward revision in the projected $600 billion aggregate spend will signal that the software monetisation lag is affecting hardware procurement.

Analysts will be watching for signs that grid costs are suppressing further infrastructure expansion.

The outlook for the semiconductor sector remains positive, provided grid constraints do not cap physical deployment capabilities. Investors should maintain balanced exposure across both compute processing and networking infrastructure equities while hedging against potential software-driven volatility.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The current AI infrastructure supercycle is driven by major technology firms, known as hyperscalers, committing massive capital, projected at $600 billion to $750 billion in 2026, to acquire specialized processors, memory, and networking equipment for increasingly complex AI models. This represents a permanent reallocation of corporate resources rather than a temporary trend.

Hardware suppliers are directly benefiting as hyperscaler investments translate into highly visible revenue pipelines and increased order books for semiconductor fabricators and component designers. This dynamic has led to significant year-to-date gains for major semiconductor equities like AMD, Broadcom, and Nvidia.

Investors in AI stocks should monitor three primary risk factors: monetization lag, where software revenue trails hardware deployment; grid capacity constraints, impacting new data center power availability; and corporate debt accumulation by secondary cloud providers. These factors could force hyperscalers to reduce hardware procurement budgets.

Major technology giants are committing substantial funds, with Amazon projecting around $200 billion, Alphabet, Google, guiding for $175 billion to $185 billion, and Meta allocating $115 billion to $135 billion for AI model training capabilities. These investments primarily focus on data center expansion, custom silicon, and compute capacity.