The United States is currently projecting an economic outlook that contradicts itself at the checkout counter. On the surface, consumer spending patterns in April 2026 suggest a resilient market, yet household confidence metrics are flashing severe warning signals. This divergence presents a critical challenge for financial professionals attempting to price risk accurately in a volatile geopolitical environment. Investors relying solely on aggregate data risk missing the structural fractures forming beneath the headline numbers. The true state of American consumer liquidity is far more precarious than the top-line figures imply.

Energy Shocks and the Evaporation of Household Liquidity

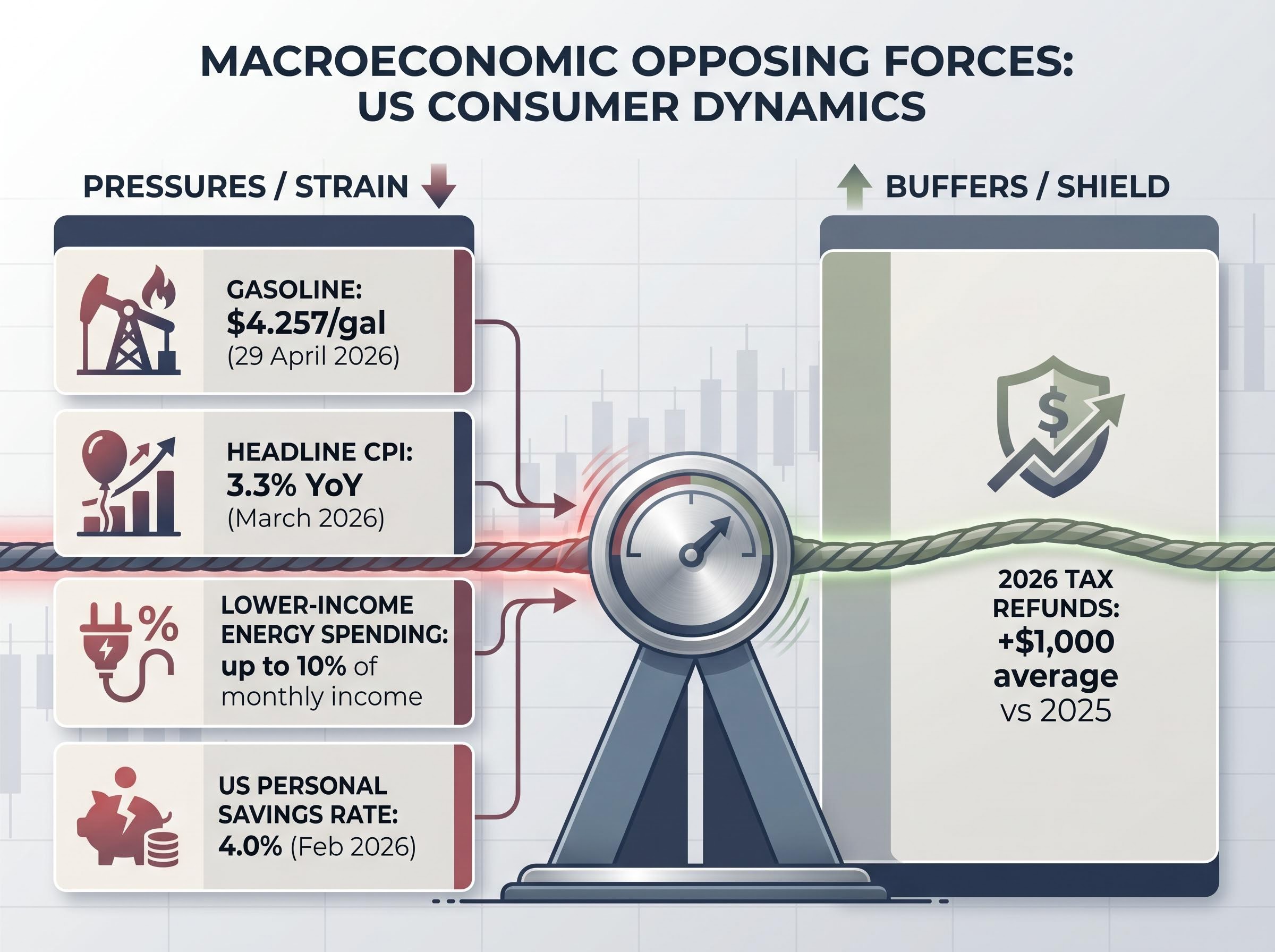

Escalating military conflicts in the Middle East are actively eroding working-class purchasing power at an alarming rate. The uncertainty surrounding the Strait of Hormuz has pushed the US average retail gasoline price to $4.257 per gallon as of 29 April 2026. This geopolitical energy shock forces lower-income households to burn through their remaining, already depleted financial reserves simply to cover mandatory transit and heating costs.

This dynamic represents an active destruction of future consumer capacity, rather than a temporary pricing blip. Lower-income households are currently spending up to 10% of their monthly income on energy requirements alone. As fuel costs compound, these households are systematically stripped of their ability to participate in discretionary retail markets, accelerating the bifurcation of the American economy.

Economic Impact Commentary “Sustained higher energy costs will inevitably feed through to the broader economy, raising real concerns about potential stagflation,” noted Paul Donovan, Chief Global Economist at UBS.

Core Inflation vs Transitory Shocks

The volatility in energy markets has directly accelerated domestic inflation metrics, completely disrupting previous stabilisation narratives. Headline CPI inflation rose to 3.3% year-over-year in March 2026, driven heavily by these external supply-side disruptions. In stark contrast, the core inflation rate, which strips out volatile food and energy costs, held steadier at 0.3% month-over-month.

The official consumer price index data confirms that energy components are heavily skewing the broader basket of goods, forcing analysts to separate volatile commodity spikes from baseline domestic pricing pressures.

Central banks face a structural disadvantage when attempting to manage geopolitical energy shocks. Traditional interest rate tools cannot drill for oil, clear shipping lanes, or resolve military conflicts. Consequently, monetary policymakers struggle to contain this supply-side inflation without heavily penalising the broader domestic economy through artificially constrained credit.

When big ASX news breaks, our subscribers know first

The Statistical Illusion of the Resilient Shopper

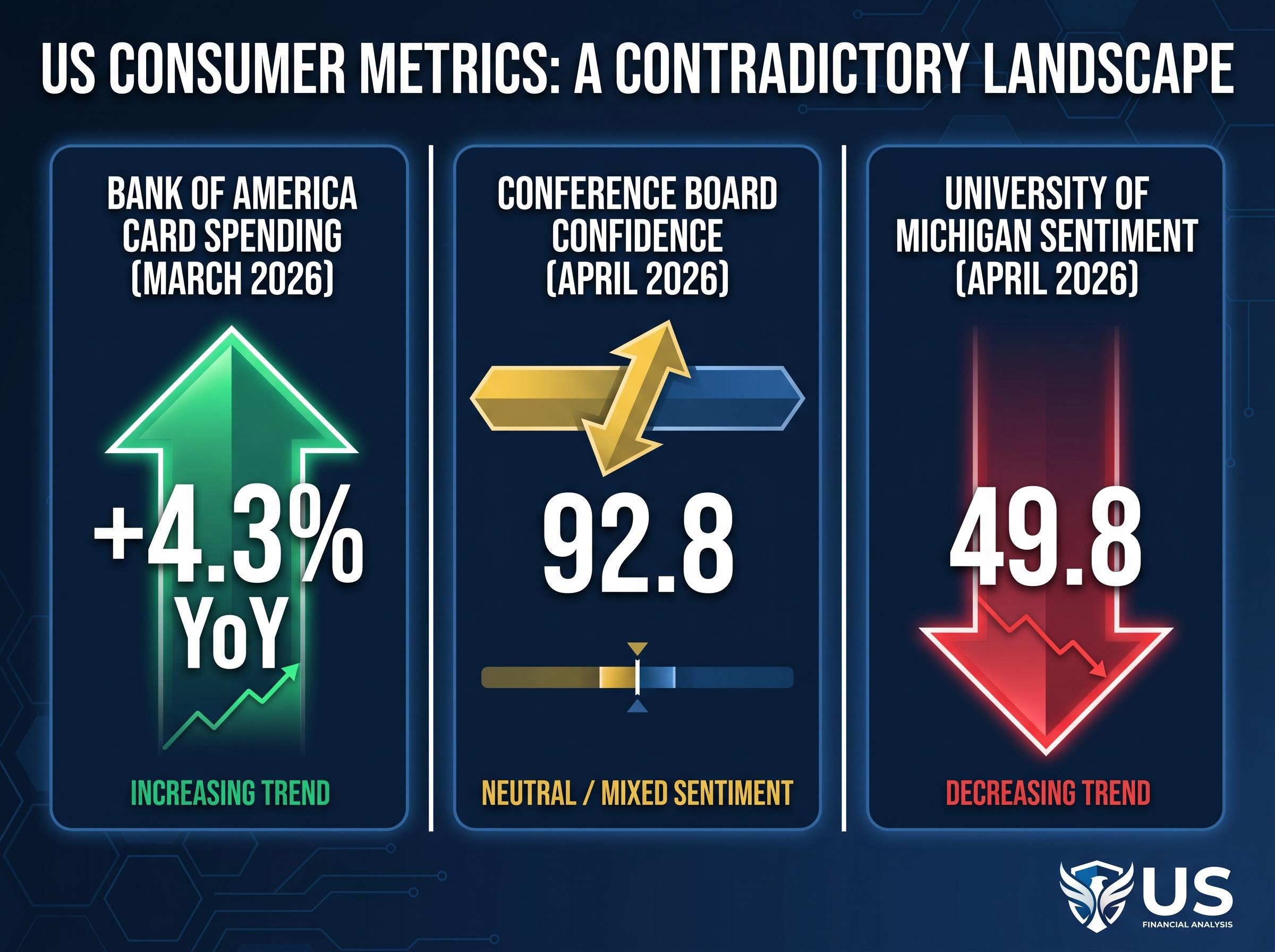

American retail data is currently generating false positive signals about the underlying health of the consumer base. Bank of America credit and debit card metrics show a 4.3% year-over-year increase in household spending for March 2026. This acceleration marks the largest gain since early 2023, painting a seemingly undeniable picture of strong consumption. Evaluated in isolation, this data suggests a domestic economy shrugging off both inflation and elevated interest rates.

However, survey data reveals a deep, structural disconnect between what consumers are spending and how they feel about their financial future. The University of Michigan Consumer Sentiment Index dropped sharply to a final reading of 49.8 in April 2026, capturing widespread financial distress at the household level. Conversely, The Conference Board Consumer Confidence Index rose slightly to 92.8 during the same period, demonstrating the mixed signalling that plagues current survey methodologies.

This stark contradiction is the first leading indicator of broader market vulnerability. Top-line retail sales figures fail entirely to capture the underlying financial exhaustion of average Americans, who are spending more simply to acquire the same volume of goods. Recognising this illusion is the necessary first step in assessing true macroeconomic health.

For readers wanting to examine the specific data sets driving this false narrative, our dedicated guide to the retail sales illusion explores how strong aggregate spending figures mask the rapid depletion of household savings across lower income brackets.

| Indicator Type | April 2026 Metric | Economic Signal |

|---|---|---|

| Bank of America Card Spending | +4.3% (YoY) | Strong top-line consumption |

| University of Michigan Sentiment | 49.8 | Severe household distress |

| Conference Board Confidence | 92.8 | Mixed to stable confidence |

Unpacking the K-Shaped Macroeconomic Shield

To interpret these conflicting reports accurately, observers must understand the mechanics of a bifurcated consumer market. Different income tiers are currently experiencing entirely different economic realities, creating a K-shaped dynamic across the domestic economy. This divergence creates a macroeconomic shield, where the financial strength of top earners artificially inflates aggregate national statistics.

Wealthy households possess the accumulated capital to absorb rising costs without fundamentally altering their consumption habits. These upper-tier consumers are supported by sustained wage growth, corporate dividends, and elevated asset valuations. Their continued discretionary spending effectively masks the rapidly deteriorating purchasing power of lower-income demographics within national data sets.

The middle and lower classes are cutting back, but the raw dollar volume of luxury and premium spending obscures this retreat. Several specific fiscal buffers currently protect high-income households while leaving others severely exposed.

Elevated tax returns: The 2026 tax refund season delivered an average of $1,000 more per household compared to 2025, providing a temporary liquidity injection that briefly masked systemic financial strain. Depleted aggregate savings: The US personal savings rate rested at just 4.0% as of February 2026, marking a precariously thin safety net for the broader working population facing escalating daily costs. * Concentrated wealth effects: Sustained equity valuations provide upper-tier households with deep financial resilience, allowing them to maintain spending patterns that lower-income demographics can no longer access.

These unsustainable savings drawdowns mean that current aggregate spending levels cannot be maintained indefinitely, especially as credit card balances continue to climb.

This foundational concept helps analysts look past aggregate national averages to see the structural fractures in consumer liquidity.

Wall Street Opts Out of the Geopolitical Reality

Despite widespread professional warnings regarding supply chain vulnerabilities, equity markets are treating geopolitical volatility as mere background noise. American market participants are exhibiting a stubborn optimism that directly contradicts the deteriorating fundamentals of the working class. Traders are actively discounting the profound risks associated with the Strait of Hormuz and broader global instability, choosing instead to chase late-cycle momentum.

By systemically mispricing geopolitical risks in current valuations, equity markets are assuming a swift resolution to the conflict and ignoring the delayed inflationary pressures already moving through global supply chains.

According to the AAII Sentiment Survey for late April 2026, 46.0% of individual investors remain bullish. This marks an irrational jump in optimism from the pre-conflict bullish sentiment. Retail investor enthusiasm continues to climb even as structural risks build silently beneath the surface of elevated asset valuations.

Market psychology is currently overriding fundamental macroeconomic risks, creating a dangerous cognitive dissonance. Equity markets are failing to price in several specific geopolitical vulnerabilities.

- Prolonged transit disruptions: The market assumes that Middle Eastern energy flows will normalise quickly, despite ongoing and escalating military exchanges.

- Supply chain contagion: Valuations ignore the secondary inflationary effects of rerouted shipping lanes on general consumer goods pricing.

- Monetary policy paralysis: Markets refuse to acknowledge the inability of the Federal Reserve to cut interest rates while energy-driven headline inflation remains elevated.

Analysts are explicitly warning against assuming this resilience will last. Piper Sandler analyst Craig Johnson forecasts a volatile “jump, slump, and pump” cycle resulting in modest 5-6% overall market returns for the year. He advises investors to look far beyond the heavily concentrated “Magnificent 7” stocks to survive these impending structural shifts.

Projections for a Sudden Macroeconomic Correction

The conflicting variables of late-cycle momentum loss, persistent inflation, and artificial consumer spending are rapidly converging. A systemic correction becomes highly probable when the lower-tier consumer finally exhausts all available credit facilities and savings options. Current labour metrics offer only a thin veneer of stability over a deeply strained foundation.

Several major recession probability models are already adjusting to this deteriorating outlook, suggesting that sustained oil price shocks could entirely derail baseline growth expectations for the year.

April data confirms 6.9 million job openings for February 2026 and a slight drop in the unemployment rate to 4.3% for March 2026. While these figures appear adequate on the surface, they obscure the severe downside risks accumulating in the broader economy. Growth models are already beginning to register the heavy drag of elevated energy prices and widespread consumer exhaustion.

The IMF and the FOMC maintain a baseline GDP growth projection of 2.4% for 2026, but high-frequency data tells a more cautious story. The Atlanta Fed GDPNow estimate projects significantly slower Q1 real GDP growth at just 1.6%. If the lower-tier American consumer fractures completely under the weight of $4.257 gasoline, downside risk models suggest annual growth could quickly fall to 2.0-2.2%.

| Institution | 2026 GDP Forecast | Key Variables | Downside Risk |

|---|---|---|---|

| IMF | 2.4% | Wealth effects, wage growth | 2.0-2.2% if energy shocks persist |

| FOMC | 2.4% | Solid baseline growth | Uncertainty from global conflicts |

| Atlanta Fed | 1.6% (Q1 Estimate) | Immediate consumer metrics | Transitory slowdown risks |

Monitoring these forward-looking metrics is critical for risk management. They define the precise threshold where delayed rate cuts and exhausted credit finally overwhelm the broader American consumption engine.

A Reckoning for the Consumption Engine

The United States is currently operating two distinct economies that effectively mask a unified systemic risk. The elevated spending data recorded throughout early 2026 is a direct reflection of extreme wealth concentration, not broad or sustainable economic health. As energy shocks accelerate the financial exhaustion of the working class, the macroeconomic shield provided by high-income earners will inevitably fracture.

Investors must position themselves defensively ahead of this impending consumer exhaustion. The glaring gap between checkout counter data and plunging sentiment surveys is not a statistical anomaly, but a clear forward indicator of economic contraction. Portfolios heavily weighted toward discretionary retail or broad market indices face outsized exposure to this hidden liquidity crisis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.