Big Tech Earnings Face $600B AI Reality Check Today

just now

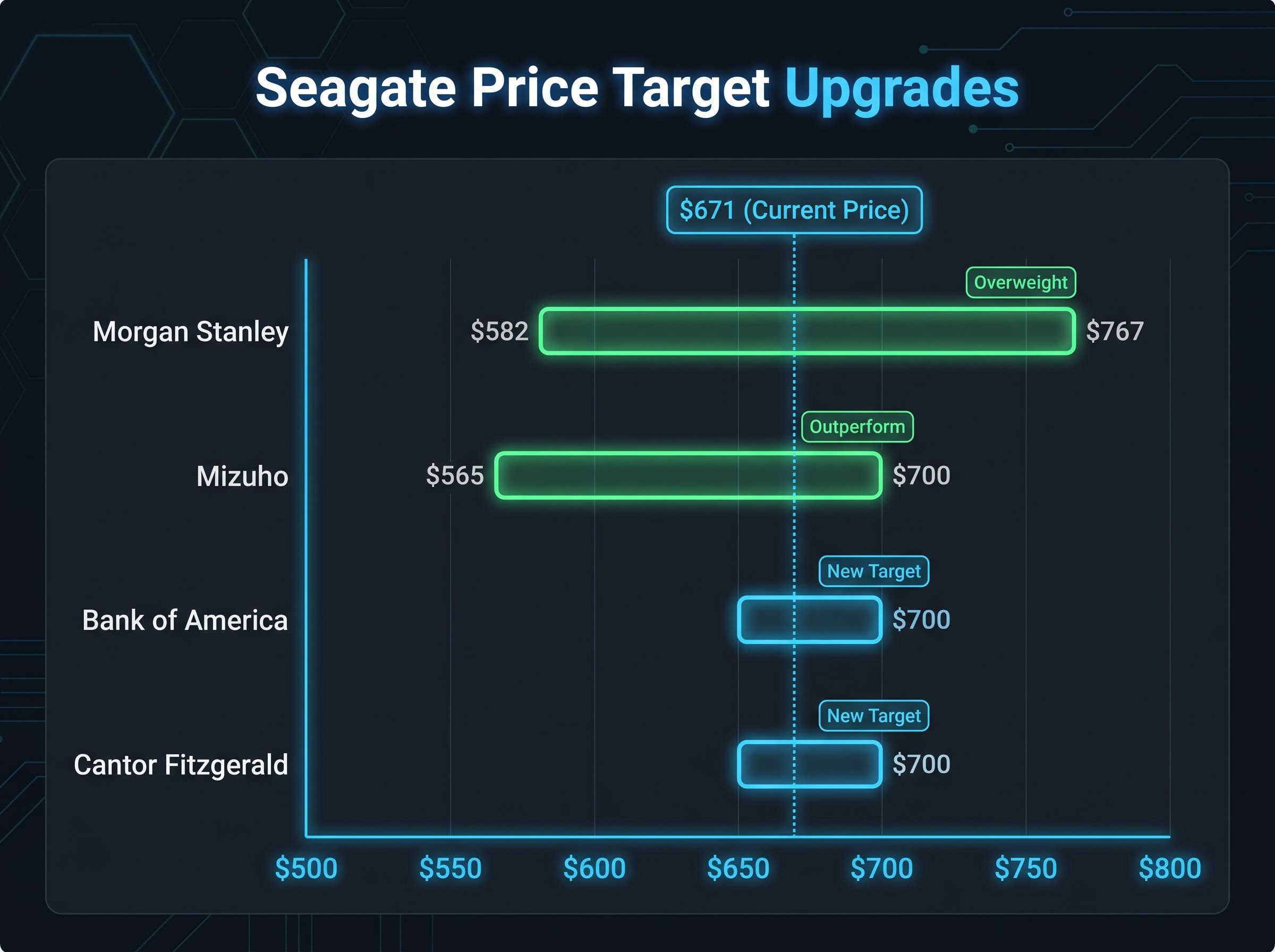

Following the April 28, 2026, earnings release, the stock price for Seagate surged 16% to $671, prompting major investment banks to fundamentally recalibrate their forward target valuations. Establishing a new stock price target for the storage manufacturer requires accounting for a decisive breakout that pushed past both consensus estimates and historical pricing power limits.

Institutions are frantically adjusting their models as artificial intelligence infrastructure spending redefines sector expectations. This analysis unpacks the mathematics behind the new analyst projections, the underlying quarterly financial performance, and the physical manufacturing constraints extending into 2027 that are fuelling this rally. Retail and institutional investors alike must evaluate these shifting baseline metrics to determine if current trading levels still offer upside.

Trading volume spiked on April 29, 2026, as institutional investors absorbed a wave of aggressive target revisions. Previously optimistic scenarios have now become standard baseline expectations across trading floors over the last three quarters.

Morgan Stanley led the revaluation, lifting its projection from $582 to $767 while maintaining an Overweight rating. According to unverified reports, the firm also introduced a highly aggressive bull case scenario of $1,131, based on a 22x multiplier and $51.39 in projected per-share earnings.

Market analysts tracking the Morgan Stanley price target upgrade point to the hardware manufacturer’s newfound pricing leverage as the primary justification for this premium valuation multiplier.

| Bank | Previous Target | New Target | Rating |

|---|---|---|---|

| Morgan Stanley | $582 | $767 | Overweight |

| Mizuho | $565 | $700 | Outperform |

| Bank of America | N/A | $700 | N/A |

| Cantor Fitzgerald | N/A | $700 | N/A |

Matching upward revisions immediately followed from other major institutions seeking to capture the changing market dynamics. Mizuho increased its valuation from $565 to $700, upgrading its rating to Outperform while citing sustained market demand across cloud providers. Bank of America and Cantor Fitzgerald both established new target valuations at $700, validating the immediate market euphoria observed during morning trading sessions.

Investors evaluating the current $671 share price must understand the precise rationale driving these elevated institutional models.

Analyst Commentary “Artificial intelligence use cases are fundamentally accelerating digital information retention, shifting the baseline metrics for long-term storage requirements across major cloud providers,” according to analysis from Morgan Stanley.

To understand the surging stock valuation, investors must pivot from the trading floor to the physical realities of modern server facilities. Generative artificial intelligence systems require massive, continuous increases in data retention to successfully train their underlying models.

According to unverified reports, while expensive flash storage handles immediate processing tasks, traditional hard disk drives fulfill approximately 80% of total cloud data storage capacity requirements. These legacy magnetic drives provide the only economically viable method for storing the vast archives of information that modern algorithms require.

The fundamental cost advantage of these magnetic formats makes them uniquely suited for cold and warm storage applications within hyperscale data centers, establishing a durable moat against alternative technologies.

A small group of suppliers is tightly controlling inventory, ensuring that purchasing requests consistently exceed available hardware limits. According to unverified reports, the average cost per terabyte increased by 5% sequentially in the first quarter, vastly outperforming the initial 1% estimate.

This cloud investment cycle has doubled Remaining Performance Obligations to $1.1 trillion among top Cloud Service Providers. The infrastructure requirements driven by artificial intelligence include:

Massive archival capacity for raw training data retention Cost-effective nearline storage for secondary processing tasks * High-density physical hardware to maximise facility floor space

This physical demand grounds the soaring share price in demonstrable business mechanics rather than pure speculation.

The forward-looking analyst optimism rests on the indisputable reality of the immediate past quarter. According to unverified reports, the company reported earnings per share of $4.10, comfortably surpassing the $3.47 consensus expectation.

The official Seagate Fiscal Q3 2026 financial results validate these robust figures, detailing the non-GAAP diluted earnings metrics that drove the subsequent stock market rally.

Top-line metrics similarly caught the broader market off guard and triggered the massive trading volume. According to unverified reports, revenue reached $3.1 billion for the quarter, compared to the $2.95 billion projected by analysts. This translated to a year-over-year revenue growth rate of 44%, alongside a sequential growth rate of 10%.

| Metric | Q3 Consensus Expected | Q3 Actual | Q4 Forward Guidance |

|---|---|---|---|

| Earnings Per Share (EPS) | $3.47 | Unverified: $4.10 | $5.00 |

| Revenue | $2.95 billion | $3.1 billion | $3.45 billion |

Management seamlessly transitioned this momentum into highly optimistic forward guidance for the upcoming June quarter. According to unverified reports, the company expects $3.45 billion in sales and $5.00 in per-share profits for the upcoming period. These foundational numbers justify the institutional upgrades and provide exact margins for the financial beat.

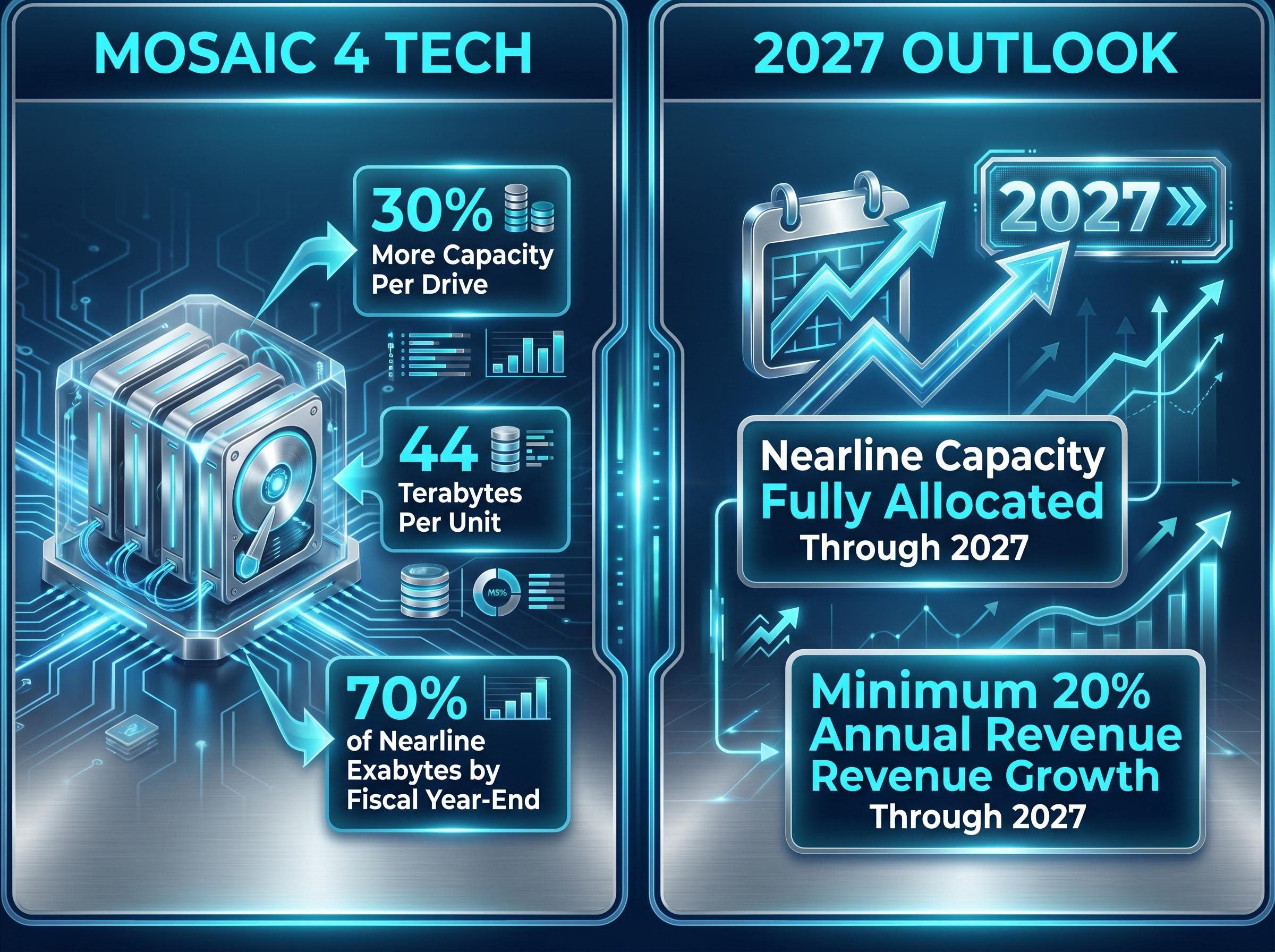

While explosive demand initiates the growth cycle, severely constrained supply is what hands the manufacturer near-total pricing leverage. Management commentary during the earnings call confirmed that nearline capacity is currently fully allocated through the entirety of 2027.

This production is secured via binding build-to-order contracts, extending revenue visibility far beyond the current quarter. Such extended visibility effectively mitigates the perceived risks of a sudden cyclical downturn that typically affects hardware manufacturers. These statements regarding forward production are speculative and subject to change based on actual market developments.

Management provided specific guidance points regarding this long-term growth trajectory:

A critical technological shift toward Heat-Assisted Magnetic Recording (HAMR) technology is further improving margin efficiency. The company’s Mosaic 4 innovation is currently delivering 30% more capacity per drive, pushing individual physical units to 44 terabytes.

Management projects that 70% of nearline Exabytes will operate on this specific advanced technology by the fiscal year-end. This technological transition allows the company to meet the escalating capacity demands while simultaneously improving production margins.

For readers wanting to evaluate the long-term sustainability of this hardware momentum, our deep-dive into the AI-driven HDD upcycle examines the total cost of ownership advantages over solid-state alternatives and highlights potential geopolitical export risks.

Wall Street is clearly treating storage hardware as a primary artificial intelligence derivative play. The synthesis of massive valuation upgrades with concrete supply constraints extending into 2027 creates a highly specific investment profile for anyone managing technology sector exposure.

This sector momentum immediately spilled over to competitors, with Western Digital stock jumping 11% in extended trading following the Seagate report. According to unverified reports, the institutional recalibration is perhaps best captured by the updated Morgan Stanley calendar year 2027 EPS projection of $42.59, a figure tracking 132% higher than general consensus estimates.

Past performance does not guarantee future results, and financial projections are subject to market conditions and supply chain risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Recent Seagate stock price target upgrades are primarily driven by surging demand from AI cloud infrastructure spending, strong Q3 2026 financial results, and constrained supply extending through 2027.

Seagate's Q3 2026 results significantly beat expectations, with earnings per share of $4.10 against a $3.47 consensus and revenue of $3.1 billion against a $2.95 billion projection, prompting a 16% stock surge.

Generative AI systems require massive, continuous increases in cost-effective data retention for training, with traditional hard disk drives fulfilling approximately 80% of total cloud data storage capacity requirements.

Seagate's nearline capacity is fully allocated through the entirety of 2027 via binding build-to-order contracts, indicating strong revenue visibility and limited supply for the next two years.