Global energy arteries are facing severe physical threats, yet nearly half of retail market participants are expressing unbridled financial optimism. This specific investor sentiment divide defines the late April 2026 environment, where US equities brush against dot-com bubble valuations simultaneously with Brent crude climbing past $112 per barrel due to Middle East hostilities. The cognitive dissonance on Wall Street requires careful examination.

Beneath the surface of the current market rally lies a complex architecture of structural vulnerabilities and psychological blind spots. Risk algorithms are currently ignoring physical world disruptions in favour of technological growth narratives. This analysis maps the fundamental disconnect between asset prices and macroeconomic realities, revealing the tripwires that threaten to reprice global equities.

How Markets Attempt to Price the Unquantifiable Threat of War

Financial markets possess highly efficient mechanisms for pricing measurable economic risks, such as interest rate trajectories or corporate debt levels. Geopolitical risks, particularly regional conflicts, present an entirely different computational challenge. Financial algorithms and traders historically default to ignoring threats to maritime routes until a physical disruption forces a sudden, violent repricing.

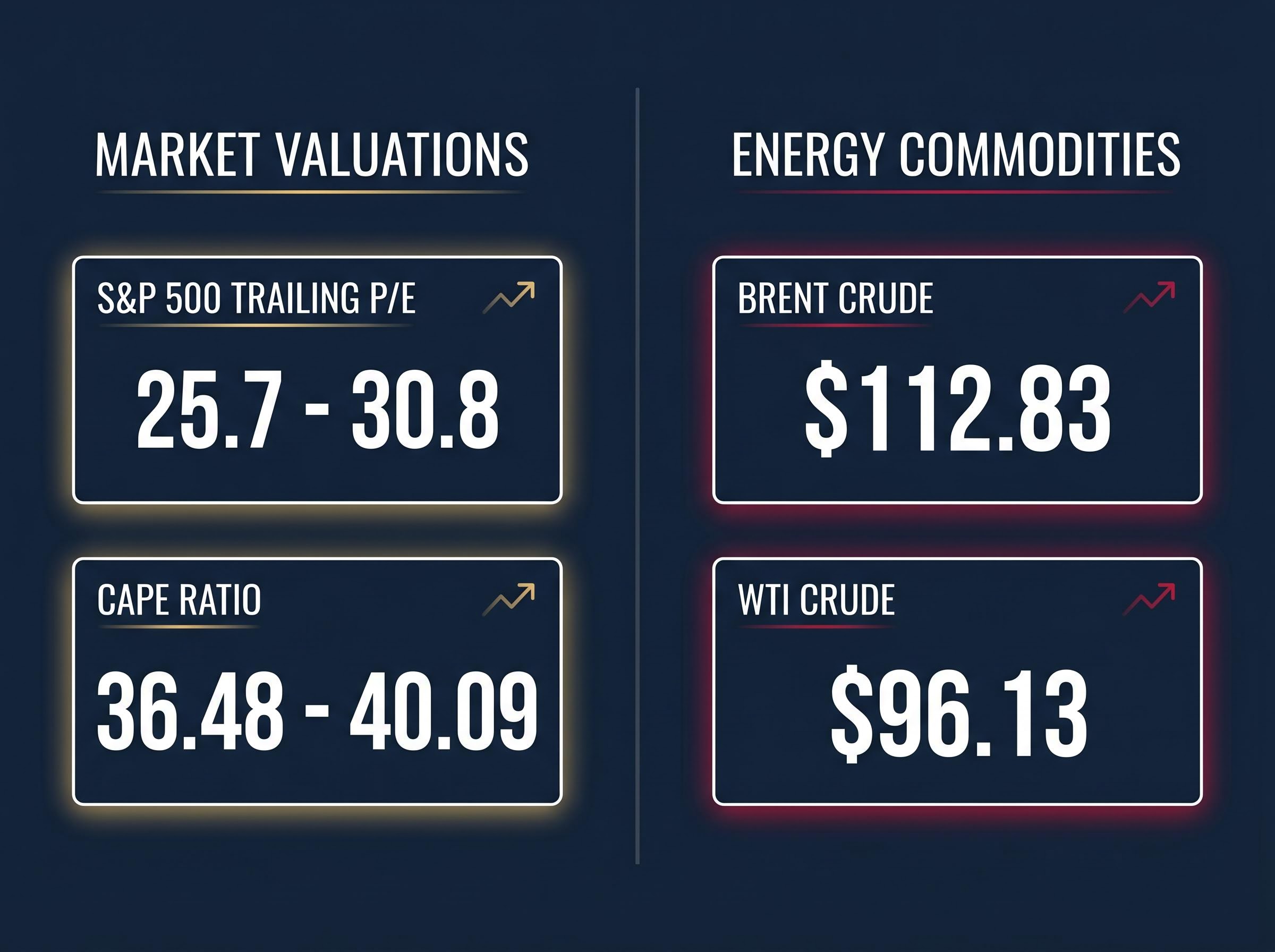

Currently, AI-driven earnings optimism functions as a psychological shield, actively blinding the market to macroeconomic realities. This technological enthusiasm has pushed the S&P 500 trailing P/E ratio to a precarious band between 25.7 and 30.8. The valuation disconnect becomes sharper when observing the CAPE ratio, which is hovering between 36.48 and 40.09, placing current market multiples near historic extremes.

This Yale CAPE ratio data demonstrates that equity valuations are now stretching into percentiles rarely seen outside of major historical speculative bubbles.

Historical pricing models struggle to quantify the precise financial impact of international instability before the supply chain breaks. Traders routinely fail to price several qualitative factors into asset values:

The probability of diplomatic negotiations failing over extended timeframes The compounding effect of shipping insurance premiums on corporate margins The secondary inflation shocks resulting from rerouted energy shipments The exact breaking point of consumer tolerance for elevated petrol prices

Market strategists are increasingly highlighting the vulnerability of these elevated valuations to physical world disruptions.

Piper Sandler Market Warning “The critical necessity of keeping the Strait of Hormuz open ensures broad market stability, and global equities remain highly vulnerable to severe energy shocks,” said Craig Johnson, Chief Market Technician at Piper Sandler.

This dynamic means the market is not bulletproof, but rather relying on a flawed pricing mechanism for international instability.

When big ASX news breaks, our subscribers know first

The Widening Chasm Between Retail Bullishness and Consumer Reality

The macroeconomic abstraction of market multiples translates into a fractured reality at ground level. Aggregate optimism currently masks a severe division within the American consumer base, where retail market bullishness runs counter to deteriorating purchasing power.

Survey data from the American Association of Individual Investors for the week ending 23 April 2026 highlights this extraordinary retail confidence. Bullishness reached 46.0%, remaining significantly elevated above historical norms despite a slight cooling from mid-April highs.

| Sentiment Category | 23 April 2026 Reading | Historical Long-Term Average |

|---|---|---|

| Bullish | 46.0% | 37.5% to 38.0% |

| Neutral | 19.5% | |

| Bearish | 34.4% |

While this retail investor confidence supports equity inflows, the underlying consumer economy presents a starkly different picture. Elevated transportation and fuel costs are actively consuming the budgets of lower-income demographics. Research indicates the lowest earning quintile currently spends four times as much on gasoline relative to their income compared to higher earners.

Official ACEEE energy burden metrics show this disproportionate fuel cost acts as a highly regressive tax, systematically draining discretionary capital from working-class communities.

Because fuel costs aggressively drive up the prices of food and travel, 65% of consumers report that prices are outpacing their income growth. Wealthy households continue to execute high transaction volumes, sustaining the aggregate spending data that algorithms interpret as economic strength. This creates a precarious macroeconomic situation where baseline costs are rising rapidly.

The headline retail spending numbers supporting the current market rally are built on an unsustainable foundation. They rely on wealthy consumer spending and the widespread depletion of middle-class savings, rather than broad economic health. The chasm between rising equity portfolios and shrinking household budgets cannot widen indefinitely.

Institutional Hedging Reveals the Smart Money Strategy

A stark divergence is forming between retail investors chasing AI equity rallies and institutional investors making tactical risk adjustments. Professional money managers are quietly preparing for potential downside, executing defensive manoeuvres beneath the calm surface of headline equity indices.

Major financial institutions are simultaneously calculating a near term recession probability of nearly 50 percent, prompting these defensive shifts across asset classes as macro indicators deteriorate.

Equity volatility metrics suggest a complacent market, with the VIX closing at a moderated 18.30 on 28 April 2026. However, the energy markets tell a different story that institutions are actively pricing in. WTI crude reached $96.13 per barrel and Brent hit $112.83, driving significant institutional adjustments across non-equity asset classes.

The energy shocks have already triggered rate-led sell-offs in fixed income markets. Geopolitical escalation has concurrently triggered a distinct risk-off response in emerging market debt. Institutions are executing a specific defensive strategy, maintaining long-term constructive outlooks while heavily prioritising immediate liquidity to navigate the conflict.

Professional asset managers are actively adjusting exposure across specific segments:

- Reducing duration risk in fixed income portfolios as energy inflation threatens to keep interest rates elevated

- Trimming exposure to emerging market sovereign debt that is highly sensitive to oil price shocks

- Increasing cash allocations to build liquidity buffers for potential rapid repricing events

- Adding strategic hedges in commodity markets to offset potential equity drawdowns

These hidden mechanics of institutional defensive positioning offer a blueprint for capital preservation. They leave the overarching retail bullishness looking increasingly isolated and exposed.

The Tripwires That Could Force a Sudden Market Repricing

The current equilibrium relies on the assumption that the Middle East conflict will remain contained. Certain breaking points exist where the market can no longer ignore physical supply disruptions, creating the perfect conditions for a rapid economic correction.

Paul Donovan, Chief Economist at UBS Wealth Management, has noted that markets are displaying a distinct optimism bias around proposals to reopen the Gulf. This psychological buffering will inevitably fail if the disconnect between baseline consumer costs and sustained buying behaviour reaches its mathematical limit.

An Extended Disruption in the Strait of Hormuz

If current threats materialise into physical blockades, the immediate supply chain and energy price consequences would force an algorithmic recalculation of corporate earnings. A sustained closure would shatter the current market optimism bias, as shipping insurance costs and delayed deliveries directly impact corporate margins.

Investors exploring how specific price thresholds might force institutional selling will find our detailed coverage of Goldman Sachs equity triggers, which examines the precise Brent crude levels projected to initiate algorithmic offloading.

The Exhaustion of Consumer Reserves

The secondary tripwire is the breaking point where lower-income and middle-income consumers can no longer finance their living standards through debt and savings depletion. When this financing capacity breaks, the inevitable demand destruction will hit corporate earnings across the retail, travel, and consumer discretionary sectors.

The Fragile Foundation of the April Rally

The US stock market is currently floating on a dangerous mixture of technological optimism and wilful blindness to geopolitical risk. While institutional investors are quietly building liquidity lifeboats across fixed income and emerging markets, retail traders remain dangerously exposed to energy sector shocks. The divergence between algorithmic equity buying and the deteriorating purchasing power of the average consumer represents a structural vulnerability.

Elevated commodity prices embed a delayed inflation risk that will eventually transmit through transportation and producer pipelines, fundamentally challenging the consensus view that price stability has been achieved.

Historically, markets that ignore physical world disruptions eventually face violent realignments. Financial valuations cannot remain permanently detached from the cost of energy and the realities of global shipping.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.