When Morgan Stanley’s optimistic scenario becomes the base case for the third consecutive quarter, something structural is happening. According to reports, on April 29, 2026, the firm raised its price target to $767, up from $582, designating Seagate Technology as its top IT hardware pick. The prior bull case is now the floor.

Evaluating Seagate stock requires understanding that the hard disk drive market is emerging from a decade-long decline into what analysts categorise as a structural supercycle. Artificial intelligence data volumes are expanding demand for bulk storage at a pace the industry had not modelled. This analysis examines the forces behind that shift, Seagate’s technological lead, and how these dynamics are materialising in financial results.

The AI data explosion is creating a structural storage demand problem that HDDs are uniquely positioned to solve

Artificial intelligence token volumes and inference logging generate persistent, large-scale cold and warm storage requirements. These needs are distinct from the performance-tier storage required for active computing. Cloud providers must house this exploding volume of data economically, routing demand specifically toward hard disk drives.

Hard disk drives maintain a 60% to 70% share of hyperscaler bulk storage, functioning as a durable structural position rather than a legacy holdover. This dominance is anchored by cost-per-terabyte economics that flash alternatives cannot currently match at scale.

Cloud Storage Market Reality According to industry estimates, hard disk drives capture roughly 80% of total cloud storage procurement demand, cementing their role as the backbone of modern data architecture.

Seagate management projects mid-20s percent annual exabyte demand growth. This projection aligns with the massive infrastructure capital expenditure already committed by major hyperscalers through 2026.

This accelerating AI infrastructure demand extends beyond storage hardware to the physical data centres themselves, with leading facility operators reporting record forward order books to accommodate new hyperscale deployments.

| Hyperscaler | Projected 2026 Capex | Storage Allocation Estimate |

|---|---|---|

| Amazon Web Services | $150 billion (2026-2030) | Approximately 25% |

| Microsoft Azure | Approximately $55 billion | Significant AI storage buildout |

| Google Cloud | Approximately $50 billion | 60-70% HDD bulk storage |

When big ASX news breaks, our subscribers know first

Why HDDs still dominate cloud storage: the cost-per-terabyte moat explained

Hyperscale data centres segment storage into distinct performance tiers based on access frequency and latency thresholds. Hard disk drives occupy the bulk, cold, and warm tiers where access speed matters far less than raw cost per terabyte. This cost advantage creates a structural barrier that solid-state drives cannot yet cross at hyperscaler scale.

While the fastest active tiers are increasingly transitioning toward AI in-memory compute solutions that process data directly on the chip, these low-latency formats remain cost-prohibitive for long-term archiving.

While solid-state drives have made cost gains, the pricing gap at the high-capacity bulk storage tier remains wide. This persistent gap ensures hard drive economics dominate procurement decisions for critical workloads.

AI training datasets requiring massive archival capacity Continuous inference logs generated by deployed AI models * Long-term archival data for regulatory compliance

According to market estimates, during the first quarter of 2026, the average cost-per-terabyte rose approximately 5% quarter-over-quarter, easily surpassing the 1% anticipated increase. This pricing strength illustrates genuine market power rather than commodity pressure.

How HAMR keeps widening the cost-per-terabyte gap

Heat-assisted magnetic recording technology extends this competitive moat by increasing areal density. The technology uses a laser to heat the disk surface during writing, allowing tighter bit packing. This enables higher capacity per drive without requiring entirely new manufacturing footprints.

Density gains connect directly to storage economics because more terabytes per unit reduces the per-terabyte cost at roughly the same manufacturing expense. A 40TB drive offers a 33% capacity gain versus prior-generation drives, driving down unit costs for cloud providers. Seagate began volume shipping 44TB Mozaic 4+ drives to hyperscalers in March 2026, marking the industry’s highest-capacity milestone.

Seagate’s HAMR lead over Western Digital is the competitive moat that matters most right now

The competitive comparison between Seagate and Western Digital is not a static ranking, but a widening timeline gap. Seagate has shipped 40TB drives in volume since 2025, securing a critical first-mover advantage. Western Digital’s volume production using the new magnetic recording standard does not begin until 2027.

Hyperscaler procurement qualification cycles are long and complex. Seagate’s early ramp locks in supply relationships that cannot be easily redirected once the supercycle reaches full force. Western Digital’s primary competitive response for 2026 is limited to its 40TB UltraSMR drives, which rely on older recording principles.

Seagate achieved volume shipments of 44TB Mozaic 4+ drives on March 3, 2026. This forward milestone gives Seagate a premium-tier exclusivity window of 12 to 18 months, translating directly to pricing power.

Seagate holds approximately 42% of global exabyte shipments, while the combined triopoly share of Seagate and Western Digital accounts for 80% to 90% of the market.

| Metric | Seagate Technology | Western Digital |

|---|---|---|

| Current Highest Capacity | 44TB Mozaic 4+ | 32TB UltraSMR |

| Volume Status | Shipping since March 2026 | Targeting 2027 |

| Next Capacity Milestone | 50TB by 2027 | 40TB UltraSMR (2H 2026) |

| 2029-2030 Roadmap | 100TB by 2030 | 100TB by 2029 |

Seagate’s fiscal Q3 2026 results show the supercycle is already in the numbers

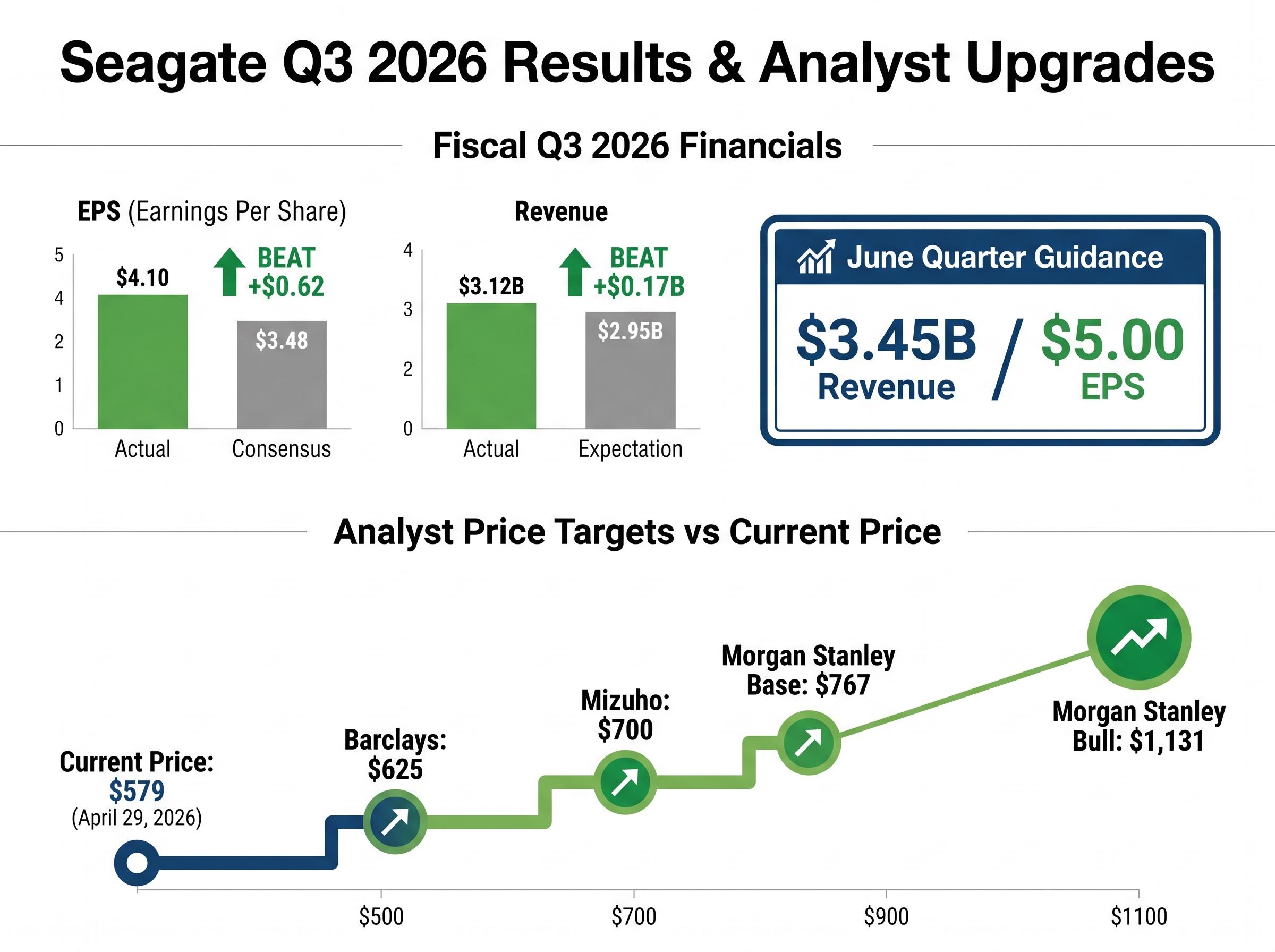

The structural thesis has crossed from forward-looking argument into current earnings reality. According to some reports, Seagate delivered fiscal third-quarter 2026 earnings per share of $4.10, comfortably beating the $3.48 consensus. According to published figures, revenue reached $3.12 billion, surpassing the $2.95 billion expectation and anchoring the financial reality of the data centre buildout.

The official figures published in Seagate Technology’s Form 8-K regulatory filing confirm these top-line beats while formally establishing the strong guidance for the coming quarter. Investors can track these exact margin improvements by examining the primary disclosures submitted to the Securities and Exchange Commission.

Higher-than-expected cost-per-terabyte gains flow through to gross margin expansion, directly driving earnings outperformance. According to analyst models, the June quarter guidance signals accelerating momentum, projecting $3.45 billion in revenue and $5.00 in earnings per share.

Market Outperformance According to some reports, Seagate shares traded near $579 on April 29, 2026, reflecting a gain of over 618% across the prior 12-month period.

Analysts are aggressively revising models to catch up with operational data. Morgan Stanley’s 2027 earnings estimate of $42.59 per share sits 32% above its prior base case and 132% above broader consensus.

Barclays: Raised target to $625 citing the structural upgrade cycle. Mizuho: Established a $700 target based on capacity constraint pricing. * Morgan Stanley: According to analyst reports, designated a $767 base target, with a bull case of $1,131 based on $51.39 in calendar 2027 earnings.

The risks that could interrupt the supercycle thesis

Investors must distinguish between risks that could end the cycle and those that merely create volatility. Customer concentration in major cloud providers means demand signals are strong but binary. A procurement pause from one hyperscaler would have an outsized impact on financial results.

Solid-state drive competition remains a relevant long-term threat. The cost-per-terabyte gap is durable in bulk cold storage today, but continued flash cost declines represent the most structurally significant challenge to the thesis.

Structural risks: what could actually break the thesis

Hyperscaler AI capital expenditure cyclicality serves as the primary demand-side risk. Execution delays in manufacturing scaling could narrow the technological moat, accelerating solid-state drive substitution.

Operational and geopolitical risks: volatility factors, not thesis-breakers

China’s Revised Foreign Trade Law, effective March 1, 2026, introduces new supply chain complexities. The United States Section 1260H export control list, updated January 2026, presents indirect compliance risks. Analysts cite high leverage relative to peers as a specific financial vulnerability. Antitrust scrutiny of the tight oligopoly structure could intensify alongside rising pricing power. * Western Digital’s 40TB UltraSMR release in late 2026 represents a near-term margin pressure risk.

For investors evaluating how broader macroeconomic headwinds could impact the tech sector, our deep-dive into current equity pricing fragility explores the historical warning signals flashing across the S&P 500 and the potential implications of a recessionary pullback.

The supercycle thesis has moved from projection to proof, but the window for the easy trade has narrowed

A compelling long-term thesis often collides with the reality of a stock that has run 618% in a single year. The easy entry point is gone, shifting the investment question to whether the analyst estimate revision cycle still has room to run.

The evidence suggests the revision cycle is not yet complete. The rapid 44TB volume ramp, strong June quarter guidance, and Morgan Stanley’s base case sitting 132% above consensus indicate that institutional models are still catching up. Seagate expects approximately 18% of fiscal 2026 exabytes to come from its high-density drives, a figure analysts view as conservative.

This ongoing revision explains why institutional price targets range from $475 up to $767 on a stock trading near $579. The spread of conviction highlights the importance of monitoring specific signals, particularly high-capacity shipment volumes and Western Digital’s qualification progress.

Institutional Conviction Morgan Stanley noted in its April 2026 upgrade that its “optimistic scenario has become the base case for the third straight quarter,” perfectly capturing the momentum of the revision cycle.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.