How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

6 hrs ago

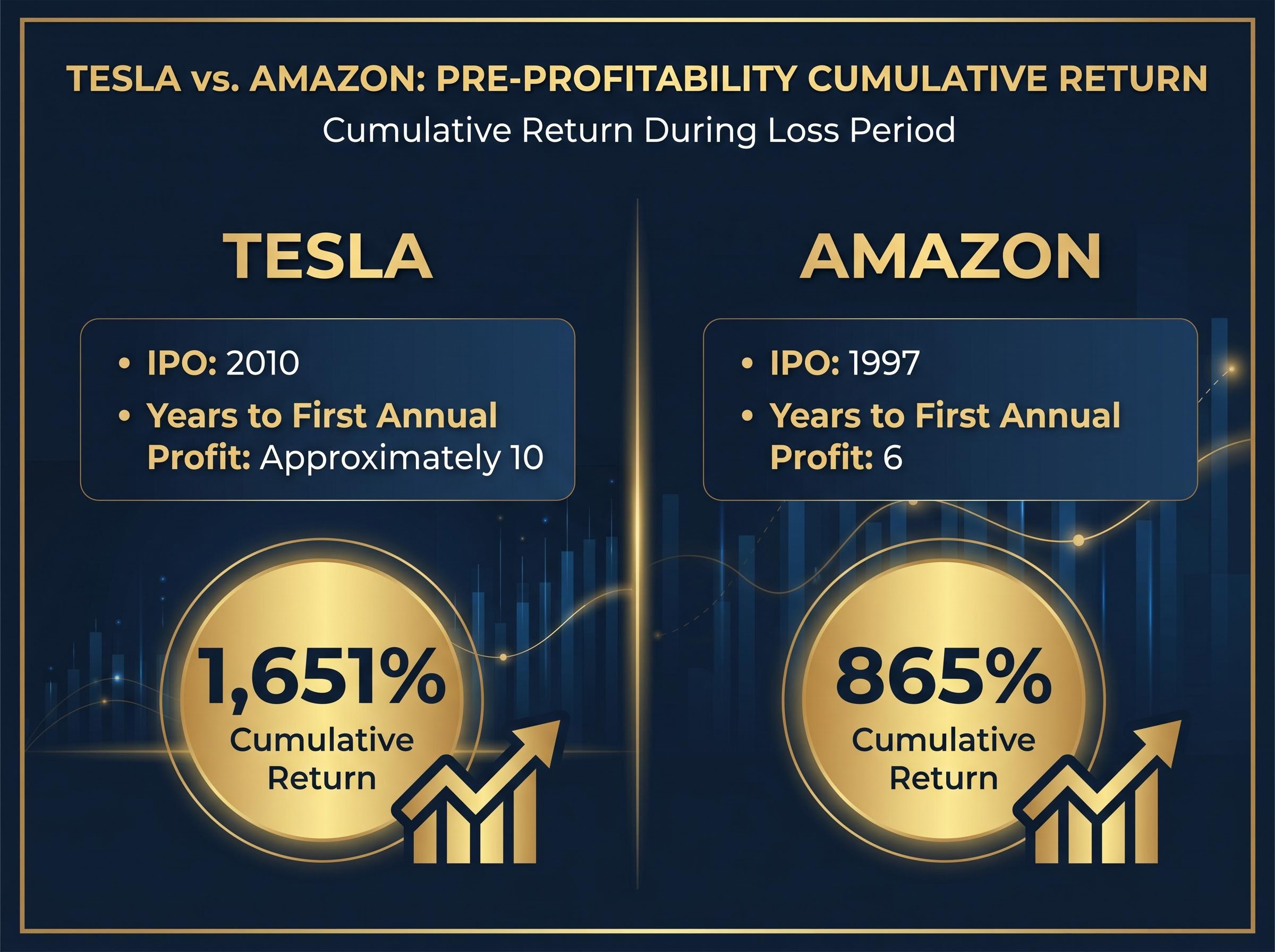

Forty years ago, a company losing money for a decade would have been a cautionary tale. Tesla did exactly that, posting annual losses for roughly ten years after its 2010 IPO, and rewarded patient shareholders with a 1,651% return before it ever reported a full year of profit.

That record matters right now because the US Securities and Exchange Commission (SEC) is circulating a proposal to make quarterly earnings filings optional. SEC Chair Paul Atkins has framed the shift as a remedy for corporate short-termism, the idea that 90-day reporting cycles pressure executives to sacrifice long-run value for near-term results. The premise sounds intuitive. Whether it holds up against the actual market record is a different question.

What follows is an examination of what the empirical data, spanning Tesla, Amazon, the Russell 2000, and cross-country academic research, reveals about how equity markets treat companies that think long. The evidence offers a clearer framework for evaluating long-term growth stocks and a more accurate mental model of how market pricing actually works.

The proposal is straightforward in structure: quarterly Form 10-Q filings would become optional, with companies permitted to shift to semiannual reporting while retaining the annual 10-K and material-event 8-K requirements. Atkins described the proposal as “very close” to issuance for public comment on 21 April 2026; it was submitted to the White House Office of Management and Budget (OMB) for review on 22 April 2026.

“Make IPOs great again” Chair Atkins has positioned the proposal as part of a broader deregulatory agenda aimed at reducing the compliance burden on public companies and encouraging long-range business focus over short-term earnings management.

The intellectual premise underneath the proposal is specific: mandatory quarterly reporting induces executives to cut research and development spending and capital expenditure to hit 90-day numbers, at the expense of compounding long-run returns. That concern has genuine academic support in executive survey literature. Berkshire Hathaway has long advocated against quarterly earnings guidance on precisely these grounds.

The broader $2.7 billion figure cited in the debate refers to SEC-related disclosure compliance costs generally, not exclusively to quarterly 10-Q filing expenses, a distinction worth noting. And while the managerial short-termism concern is well documented in surveys, the market-level evidence that investors themselves are systematically short-termist is far thinner. That gap between the premise and the proof is where the analysis begins.

The practical deterrent may prove stronger than the regulatory permission: institutional responses to the SEC quarterly reporting reform include signals from Citadel and Fidelity that companies adopting semiannual schedules could face position reduction or valuation reassessment, creating a cost-of-capital headwind that the SEC’s compliance-cost savings may not offset.

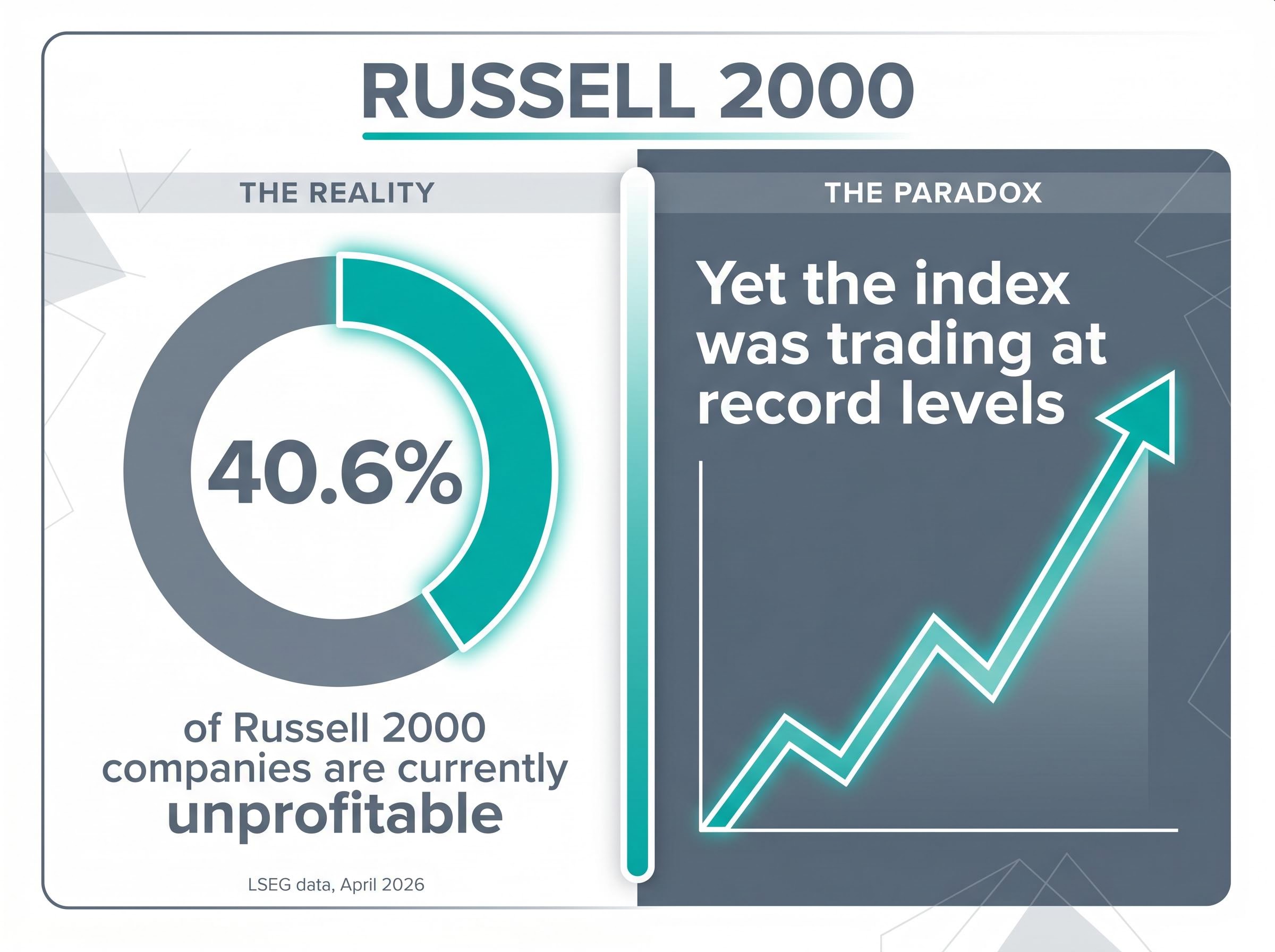

Tesla and Amazon are often treated as exceptional cases. The Russell 2000 suggests they are not.

Roughly 40.6% of the Russell 2000’s constituents are currently unprofitable, according to LSEG data as of approximately April 2026. The index was trading at record levels at time of publication.

40.6% of Russell 2000 companies are currently unprofitable, yet the index was trading at record levels, a combination that is structurally incompatible with the claim that markets systematically punish non-earners.

An index cannot reach record levels while nearly half its members are losing money if market pricing is dominated by short-term earnings fixation. The data does not mean every unprofitable company is being rewarded. It means the market is selectively pricing future potential in a large subset of current loss-makers, distinguishing between companies reinvesting for growth and companies failing to generate revenue.

The Russell 2000 is particularly relevant here because it represents the small-cap, domestically focused universe with limited institutional coverage, precisely the companies most likely to adopt semiannual reporting if the SEC proposal is finalised. For investors in small-cap growth names, the data challenges a common heuristic that unprofitable small-caps are inherently speculative. Selectivity, not blanket caution, is the more accurate posture.

1,651%: Tesla’s cumulative return from IPO through the end of 2019, its final full year of reported annual losses. Investors held through a decade of red ink, and the market priced something the income statement was not showing.

The numbers are worth sitting with before moving to interpretation.

| Company | IPO Year | Years to First Annual Profit | Cumulative Return During Loss Period | Data Source |

|---|---|---|---|---|

| Tesla | 2010 | Approximately 10 | 1,651% | LSEG |

| Amazon | 1997 | 6 | 865% | LSEG |

These returns were generated not despite investor awareness of losses, but alongside it. Quarterly filings disclosed every loss in real time. Investors read the 10-Qs, absorbed the numbers, and kept buying. If markets were genuinely driven by short-term earnings fixation, that pattern of patience across a decade of Tesla losses would be structurally impossible.

The interpretive implication is direct: equity markets function as forward-discounting mechanisms, pricing expected future cash flows rather than trailing reported earnings. What the income statement showed and what the share price reflected were measuring different things. The income statement recorded the cost of reinvestment. The share price reflected the market’s estimate of what that reinvestment would eventually produce.

The split valuation signals in the current S&P 500, where the Shiller P/E has reached 40.09 (its second-highest reading in 155 years) while the forward P/E has compressed to near five-year norms, reflect precisely this gap between trailing and forward-looking measures: the two metrics disagree because they are measuring different things, much as Tesla’s income statement and share price measured different things throughout its loss period.

The Tesla and Amazon evidence is not a fluke. It reflects a specific pricing mechanism that applies broadly to pre-profitability growth companies.

Equity valuation for these companies depends on discounted future cash flows (the present value of money a company is expected to generate in future years) and total addressable market estimates (the total revenue opportunity available in a company’s target industry). Trailing twelve-month earnings per share, the metric most associated with quarterly reporting cycles, is largely irrelevant to how these companies are priced.

Markets look for a specific set of characteristics when pricing a pre-profitability company:

The general pattern over approximately the past two decades has been that growth stocks, whose valuations depend on distant future earnings, have outperformed value stocks in aggregate. If markets were purely focused on near-term results, the opposite would hold. (Specific 2025-2026 Russell 1000 Growth versus Value index figures were not verified in available research; FTSE Russell and S&P Dow Jones Indices provide current data for readers seeking the latest comparison.)

Harvard Law professor Lucian Bebchuk’s 2021 corporate governance forum writing reinforces this reading, noting that markets process long-term signals from management behaviour, capital allocation, and competitive positioning rather than relying solely on the most recent quarterly result.

The distinction that matters most is between losses from deliberate reinvestment and losses from operational failure. A company spending heavily on research and customer acquisition while growing revenue at 40% annually sends a fundamentally different signal than a company burning cash with flat or declining revenue.

Markets distinguish between these profiles aggressively. Quarterly filings are actually the mechanism by which investors make this distinction in real time. The irony is pointed: it is the quarterly data that enables patient investors to track whether a growth company’s loss is the right kind of loss. Removing that data does not reduce short-termism; it reduces the information investors use to be patient intelligently.

The evidence against market-level short-termism is strong. The evidence against managerial short-termism is weaker, and the SEC proposal’s critics raise concerns that deserve consideration rather than dismissal.

Academic survey data consistently shows that executives sometimes cut R&D or defer capital expenditure to meet quarterly guidance. That behavioural pattern is real even if market pricing does not systematically reward it. The proposal, however, targets reporting frequency rather than guidance practices, which is a structural mismatch between the diagnosed problem and the proposed remedy.

Arif and De George’s 2018 study, analysing over 20,000 firm-years across 31 countries, found that semiannual reporters experience elevated stock price volatility around the quarterly announcement dates of US peer companies. Reduced reporting frequency creates its own information risks.

Srini Krishnamurthy of NC State University has argued that switching to semiannual reporting is unlikely to produce a meaningful shift in how managers plan long-term, and could enable dishonest management to conceal financial deterioration for longer periods. BlackRock and T. Rowe Price have opposed the proposal, as reported by Politico on 2 April 2026, signalling that institutional investors with sophisticated long-term mandates are not convinced that less information serves their clients better.

The UK experience after the EU Transparency Directive’s interim reporting mandate was lifted offers a useful precedent: fewer than 10% of firms stopped quarterly reporting, and those that did were predominantly smaller companies with thin analyst coverage.

The conditions under which reduced reporting frequency creates genuine investor risk are specific and identifiable:

Many corporate credit agreements contractually require quarterly financial reporting. A company that adopts semiannual reporting could trigger covenant violations in its existing debt arrangements, creating a structural barrier that has received less attention than the investor transparency debate.

This matters directly for growth investors because many pre-profitability companies carry significant debt loads. The practical universe of companies that could actually adopt semiannual reporting may be considerably narrower than the proposal implies.

The analytical arc points toward a specific conclusion: markets are not systematically short-termist in their pricing of growth companies. The Tesla, Amazon, and Russell 2000 evidence all point in the same direction. The SEC proposal, however, does not solve the managerial short-termism problem it claims to target, and may introduce new information risks for the very companies it is designed to help.

Investors in long-term growth stocks should monitor the following developments:

The evidence suggests that holding quality long-term growth stocks through loss periods is consistent with how markets have historically behaved. The more relevant risk is not reporting frequency; it is information quality. Whether the SEC proposal improves or degrades that quality is the question the public comment period should answer.

Long-horizon equity return expectations at current valuations add an important calibration to the patience argument: JPMorgan projects annualised S&P 500 returns of 5% or less over the next decade at a forward P/E of 20.8, which means investors who hold growth stocks through loss periods in a richly valued broad market are accepting more duration risk than the Tesla and Amazon historical analogies alone would suggest.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding the SEC proposal’s timeline and potential effects are subject to change based on regulatory developments and market conditions.

The empirical record, from Tesla’s decade of losses to the Russell 2000’s current composition, challenges the premise that equity markets systematically punish long-term thinking. The short-termism problem, to the extent it is real, lives more in the boardroom than in the stock price.

The SEC proposal raises legitimate questions about information asymmetry and small-cap transparency that deserve careful evaluation during the public comment period. Whether reducing reporting frequency helps or harms the companies it targets remains genuinely uncertain.

What is not uncertain is the mechanism. Markets price long-term growth potential by evaluating future cash flows, addressable markets, and reinvestment trajectories. Understanding that pricing mechanism is more useful to an investor than waiting for regulators to solve a problem the market may have already been navigating for decades.

Long-term growth stocks are shares in companies that reinvest heavily for future expansion, often at the expense of near-term profitability. Markets price them using discounted future cash flows and total addressable market estimates rather than trailing earnings per share.

Yes. Tesla generated a 1,651% cumulative return from its 2010 IPO through 2019, its final full year of annual losses, demonstrating that equity markets price expected future cash flows rather than current reported earnings.

Approximately 40.6% of Russell 2000 constituents are currently unprofitable, yet the index was trading at record levels as of April 2026, which indicates that markets selectively reward companies reinvesting for growth rather than systematically punishing loss-makers.

The SEC is proposing to make quarterly Form 10-Q filings optional, allowing companies to shift to semiannual reporting. Critics argue this could reduce the real-time information investors rely on to distinguish healthy reinvestment losses from operational failures, particularly for smaller growth companies.

Investors should evaluate revenue growth trajectory, gross margin direction, total addressable market size, and management's reinvestment track record, since these forward-looking signals are what equity markets use to price companies before they reach profitability.