How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

10 hrs ago

The iShares Expanded Tech-Software Sector ETF (IGV) has fallen more than 20% year-to-date as of late April 2026, and a single word keeps surfacing in analyst commentary to explain why: “SaaSpocalypse.” The concern is not a routine tech selloff. It is a structural thesis, gaining traction among institutional investors and retail analysts alike, that agentic AI tools may be on the verge of making large swaths of enterprise software subscriptions redundant. That thesis is actively moving price action in major names including Palantir and Salesforce right now. What follows explains what agentic AI actually does, why it threatens the SaaS business model at a mechanical level, where the evidence for disruption is real versus speculative, and how investors can think about exposure to enterprise software stocks in a market that is visibly repricing the sector.

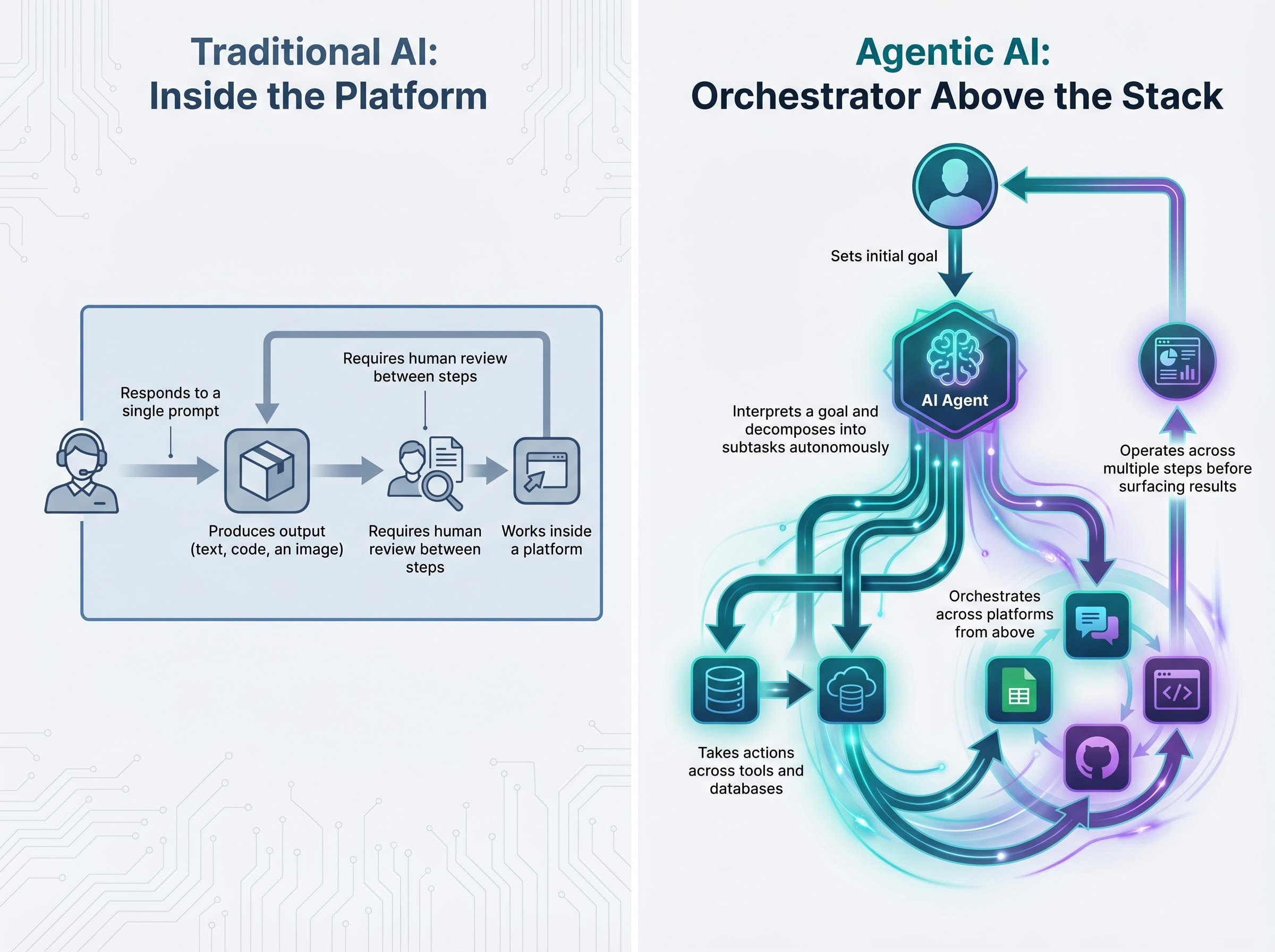

Most people already interact with AI as a response tool. A chatbot answers a question. A generative model drafts an email when prompted. The human remains in the loop at every step, issuing instructions, reviewing output, deciding what happens next.

Agentic AI operates differently. An AI “agent” can receive a high-level objective, plan the steps required, execute them across multiple systems, evaluate its own output, and iterate, all without a human issuing commands at each stage. Consider a practical enterprise example: an agent ingests a sales pipeline, drafts personalised follow-up emails, updates CRM records, flags at-risk deals, and routes exceptions to a human reviewer. The human sets the goal once. The agent handles the workflow end to end.

The distinction matters across several dimensions:

Anthropic’s Claude managed agents represent the most-cited current example of this architecture in production. Anthropic claims 10x faster time-to-production versus custom-built agent solutions, and Asana is among the named early enterprise adopters. The velocity of adoption is visible in the numbers: Anthropic’s managed agent product grew annualised recurring revenue from $9 billion to $30 billion in four months.

The architectural shift that matters most for investors is positional. An AI agent does not need to be inside Salesforce or Zendesk to perform the task those platforms were purchased to perform. It sits above the software stack, orchestrating workflows across whatever tools are available, or replacing them entirely.

The line is direct: if an agent can execute the workflow, the platform that housed the workflow becomes optional. That is the mechanism behind the SaaSpocalypse thesis, and it is what makes the current selloff different from a standard valuation correction.

The Software-as-a-Service model generates revenue through per-seat subscriptions. Enterprises pay recurring fees proportional to the number of human users accessing a platform. A company with 5,000 salespeople using a CRM pays for 5,000 seats. The model works beautifully when every workflow requires a human to log in and act.

AI agents do not require seats. They do not log in. They do not need the graphical interface layer that per-seat pricing was built around. When a single agent can handle the work previously distributed across a customer service team, the procurement logic shifts. IT budget consolidation begins at the margin as teams ask whether five specialised platforms are necessary when one agentic layer handles all five workflows.

The per-seat pricing collapse and infrastructure beneficiaries of the agentic transition sit on opposite ends of the same structural shift: IDC projects that 70% of vendors will move to consumption or outcome-based pricing by 2028, meaning the valuation discount being applied to today’s SaaS names may reflect a model change that is already mechanically underway.

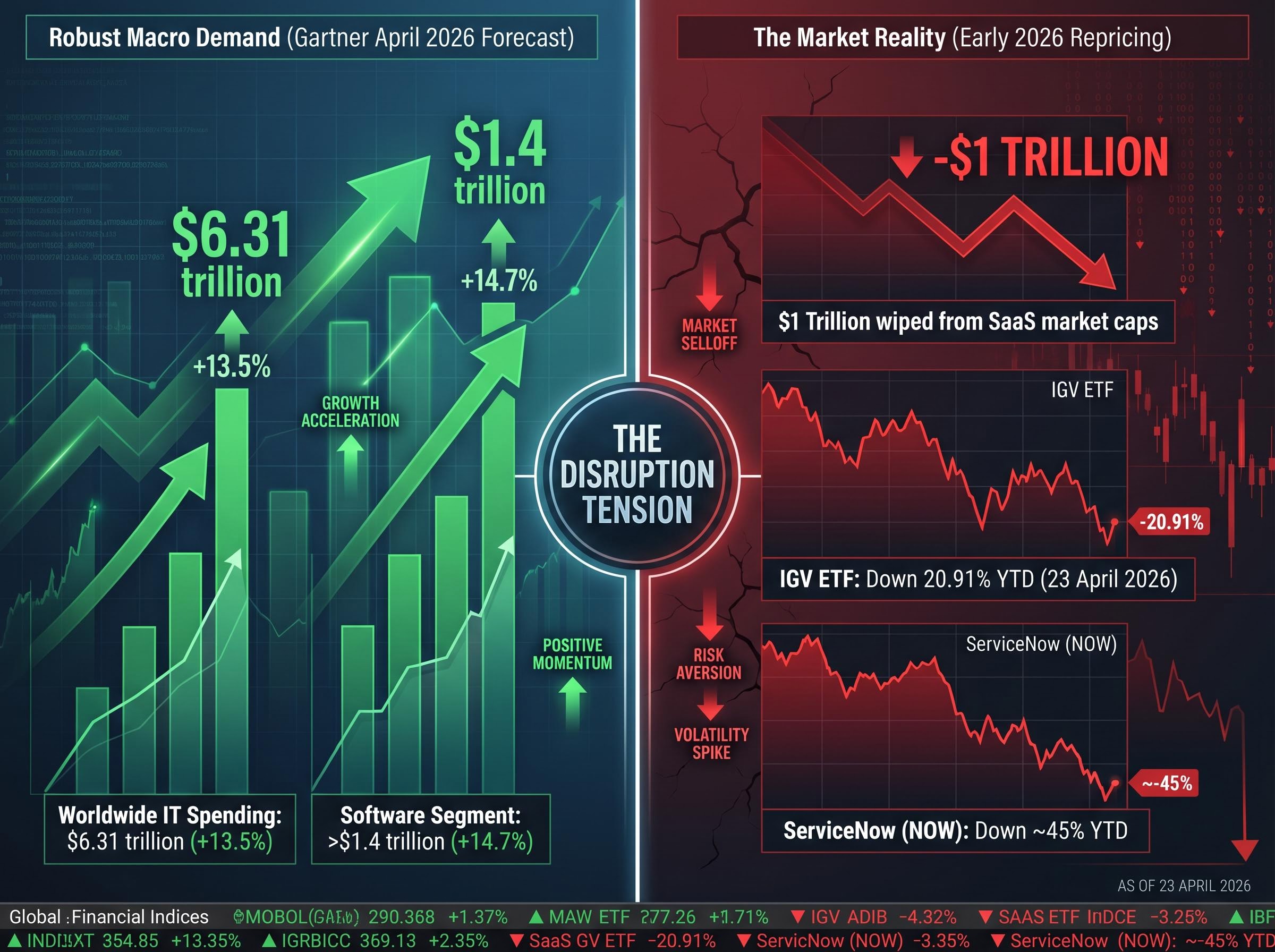

The macro picture, however, remains constructive. Gartner’s April 2026 forecast projects worldwide IT spending growing 13.5% to $6.31 trillion in 2026, with the software segment up 14.7% to over $1.4 trillion. Demand for enterprise software is not collapsing. What is collapsing is investor confidence in the pricing model that captures that demand.

An estimated $1 trillion has been wiped from SaaS market capitalisations in early 2026, attributed to investor concern over AI agent adoption.

The IGV ETF is down 20.91% year-to-date as of 23 April 2026. The BVP Nasdaq Emerging Cloud Index sits at 1,275.82. Both confirm sector-wide repricing, not isolated weakness in a handful of names.

| Software Category | Traditional Revenue Model | Where Agentic AI Inserts | Risk Level |

|---|---|---|---|

| CRM | Per-seat subscription | Agent handles pipeline management, follow-ups, and deal tracking | High |

| Customer Service | Per-agent or per-ticket pricing | Agent resolves queries end-to-end without human escalation | High |

| Developer Productivity | Per-seat or usage-based | Managed agent frameworks reduce reliance on specialised build environments | Moderate-High |

| Workflow Automation | Per-workflow or per-user | Agent orchestrates multi-system processes without dedicated platform | Moderate-High |

The disruption is not uniform. Three categories face the most immediate pressure:

The two most watched enterprise software names in the current repricing are not just “AI stocks.” They represent two distinct strategic bets on where value will accrue in an agentic world.

| Metric | Palantir (PLTR) | Salesforce (CRM) |

|---|---|---|

| Market Cap (April 2026) | $342.22 billion | $145.74 billion |

| Latest Annual Revenue | $4.475 billion (FY2025) | $41.5 billion (FY2026) |

| Revenue Growth Rate | 70% YoY (Q4 2025) | Double-digit organic |

| Forward Multiple | ~106x forward earnings | Significantly lower |

| Agentic AI Strategy | AIP: ontology-first, complexity-driven | Agentforce: platform repositioning |

The valuation gap is striking. Palantir commands a market cap of $342.22 billion on $4.475 billion in annual revenue. Salesforce sits at $145.74 billion on $41.5 billion. That disparity encodes a fundamental disagreement about where the premium should sit.

Palantir’s AIP (Artificial Intelligence Platform) is built on an ontology-based data architecture, a method of linking disparate data sources into a unified, continuously updated operational picture. In practical terms, it means a defence agency or large enterprise can connect logistics systems, financial data, and operational feeds into a single decision-making layer.

Q4 2025 revenue reached $1.4 billion, up 70% year-over-year. U.S. commercial revenue surged 137% year-over-year to $507 million. Full-year 2026 guidance calls for $7.182-$7.198 billion, representing 61% growth.

The numbers are strong. The debate is about what they cost to buy. At approximately 106x forward earnings, with the stock already down roughly 20% year-to-date and 31-38% from its 52-week high of $207.52, the valuation remains a focal point. Michael Burry’s April 2026 commentary argued that AIP’s complexity is a liability when simpler agentic tools offer faster time-to-production. Wedbush countered that AIP’s enterprise entrenchment is durable and that Burry’s critique underestimates the platform’s stickiness.

Salesforce has taken the opposite approach: rather than defending a legacy model, it is repositioning as the platform through which enterprises deploy AI agents across CRM workflows. Agentforce is that bet.

Agentforce deals grew 50-57% quarter-over-quarter in Q4 fiscal 2026, early evidence of commercial traction. Fiscal 2027 guidance targets a return to double-digit organic revenue growth, with acceleration expected in the second half. That guidance is the test. If Agentforce translates to revenue acceleration, Salesforce’s pivot validates the thesis that incumbents can absorb the agentic transition. If growth stalls, the per-seat erosion thesis gains ground.

Michael Burry’s April 2026 public critique of Palantir did not land in a vacuum. His focus on the approximately 106x forward earnings multiple triggered a 7.3% single-day decline in the stock, erasing roughly $23 billion in market capitalisation. The sensitivity of the move reveals how fragile the valuation consensus has become.

Burry’s positioning, however, was not simply bearish on enterprise software. He simultaneously initiated a long position in Salesforce, citing record free cash flow and shareholder returns as his rationale. Salesforce returned $14 billion to shareholders in fiscal 2026, representing 99% of free cash flow. Burry stated plans to add to the position at a further discount, framing CRM as a fundamentals-driven value call rather than a pure AI enthusiasm trade.

His broader portfolio confirms this is a systematic value rotation, not a one-off contrarian bet. Confirmed long positions include:

Wedbush disagreed publicly and directly.

On 14 April 2026, Wedbush pushed back forcefully, asserting that Burry’s bearish take on Palantir would ultimately be shown to be incorrect, and pointing to the company’s accelerating growth trajectory and deeply embedded AIP deployments across enterprise customers as the basis for sustained conviction.

The disagreement is not academic. It maps directly onto the core question for SaaS stocks: does complexity and data depth protect premium multiples, or does the market eventually reprice them when simpler competitors achieve comparable results faster?

Investors wanting to stress-test the valuation gap between these two names in more detail will find our deep-dive into Burry’s Salesforce valuation thesis versus Palantir, which works through the margin of safety calculation at 13.5x forward earnings, the proprietary data moat argument for Salesforce’s resilience, and the specific Q1 FY2027 earnings triggers that will validate or challenge the contrarian position.

The macro tailwind and the disruption thesis can both be true at the same time. Gartner’s forecast for 13.5% IT spending growth in 2026 means overall software demand remains robust. Individual platform categories, however, can lose share to agentic layers even as the total addressable market expands.

According to Gartner’s 2026 projections, the software segment is forecast to expand by 14.7%, reaching more than $1.4 trillion, a scale of growth that sits uneasily alongside any thesis positioning the sector as facing near-term demand collapse.

The repricing extends well beyond Palantir and Salesforce. ServiceNow (NOW) has declined approximately 45% year-to-date, with a market cap of $92.99 billion as of 24 April 2026. The IGV ETF is down 20.91% year-to-date. The BVP Nasdaq Emerging Cloud Index reads 1,275.82. This is a sector-level repricing, which means investors need a sector-level framework.

The absence of revenue warnings from major software vendors is itself a data point: no SEC-mandated disclosures citing AI competition have emerged from Salesforce, Adobe, ServiceNow, Oracle, or SAP as of April 2026, a materially bullish signal that sits in direct tension with the scale of the sector repricing.

Two questions apply to any SaaS holding:

Long-term fundamental trajectories have not been erased. Analyst consensus projects Salesforce revenue reaching $60.64 billion by fiscal 2030. The question is not whether enterprise software generates revenue in five years. It is whether the pricing model, and therefore the margin structure, survives the transition intact.

The SaaSpocalypse thesis is real enough to be moving institutional capital and sector ETFs, but the timeline and magnitude of disruption remain genuinely contested. Macro IT spending data still points firmly upward, even as individual SaaS names reprice by 20-45% year-to-date. The tension between those two realities defines the current investment landscape for enterprise software.

Palantir and Salesforce represent two different strategic bets on how enterprise software value survives the agentic transition. Neither outcome is certain. The premium for complexity and the premium for distribution are both being tested simultaneously.

The data points that will validate or invalidate the thesis over the next two to three quarters are specific and trackable: Salesforce’s fiscal 2027 organic growth acceleration in the second half, Palantir’s AIP commercial adoption curve, and whether Anthropic’s managed agent ARR growth sustains or plateaus.

Investors looking for real-time proxies for how the market is pricing the disruption thesis can monitor the IGV ETF and the BVP Nasdaq Emerging Cloud Index as ongoing benchmarks, not as historical artefacts, but as live signals of where institutional consensus is settling.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced are subject to market conditions and various risk factors.

—

The SaaSpocalypse thesis holds that agentic AI tools can execute enterprise workflows without requiring per-seat software subscriptions, threatening the core pricing model that SaaS companies depend on for recurring revenue. It is currently driving sector-wide repricing, with the iShares Expanded Tech-Software Sector ETF down over 20% year-to-date as of April 2026.

Agentic AI receives a high-level objective and autonomously plans, executes, and evaluates tasks across multiple systems without requiring human input at each step, whereas traditional AI tools respond to a single prompt and produce output for human review. This means an AI agent can perform workflows previously requiring dedicated software platforms, removing the need for per-seat subscriptions.

Software categories facing the highest disruption risk include CRM platforms, customer service tools, and developer productivity environments, where AI agents can replicate core workflows end to end. Major names including Salesforce and ServiceNow, which is down approximately 45% year-to-date, are among the most closely watched.

Investors should assess two factors: whether a platform's core workflow can be replicated by a general-purpose agentic layer without accuracy or compliance loss, and whether the company is actively repositioning as an agentic platform rather than defending its legacy model. Companies building agentic capabilities, such as Salesforce with its Agentforce product, carry a different risk profile than those assuming the current subscription model persists.

Key signals to monitor include Salesforce's fiscal 2027 organic revenue growth acceleration in the second half of the year, Palantir's AIP commercial adoption curve, and whether Anthropic's managed agent ARR growth sustains or plateaus. The IGV ETF and the BVP Nasdaq Emerging Cloud Index also serve as live benchmarks for how institutional capital is pricing the disruption thesis.