How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

10 hrs ago

Michael Burry, the investor who built his reputation by shorting the U.S. housing market before the 2008 financial crisis, announced on 16 April 2026 that he would initiate a position in Salesforce (CRM) the following trading day. The move, disclosed via his Substack, cited a specific valuation thesis centred on what Burry characterised as overstated technical pressures and a margin of safety in a stock that had shed roughly 33% year-to-date. At the same time, he steered away from high-multiple growth names like Palantir (PLTR), which was trading at approximately 109x forward earnings. This analysis unpacks what Burry actually said, how the Salesforce-versus-Palantir valuation gap looks in numbers, what the so-called SaaSpocalypse thesis means for the enterprise software sector, and whether Salesforce’s structural defences justify the contrarian bet.

Burry does not frequently telegraph live positions. When he does, the signal carries weight precisely because of its rarity. His 16 April Substack post named Salesforce as his next trade, with plans to buy on 17 April 2026, and laid out a thesis grounded in valuation discipline rather than sector optimism.

According to secondary source reporting from CNBC and The Motley Fool, Burry attributed CRM’s selloff to technical and macro pressures, specifically private credit stress and software debt concerns, rather than fundamental deterioration in the business. He characterised the stock as resilient to the broader “software apocalypse” that he believes threatens select competitors with weaker competitive positioning.

Burry’s core thesis framing (via secondary sources): Private credit and software debt pressures on CRM are overstated, providing a “margin of safety.” Salesforce is resilient to the software apocalypse, unlike certain competitors vulnerable to advanced large language models.

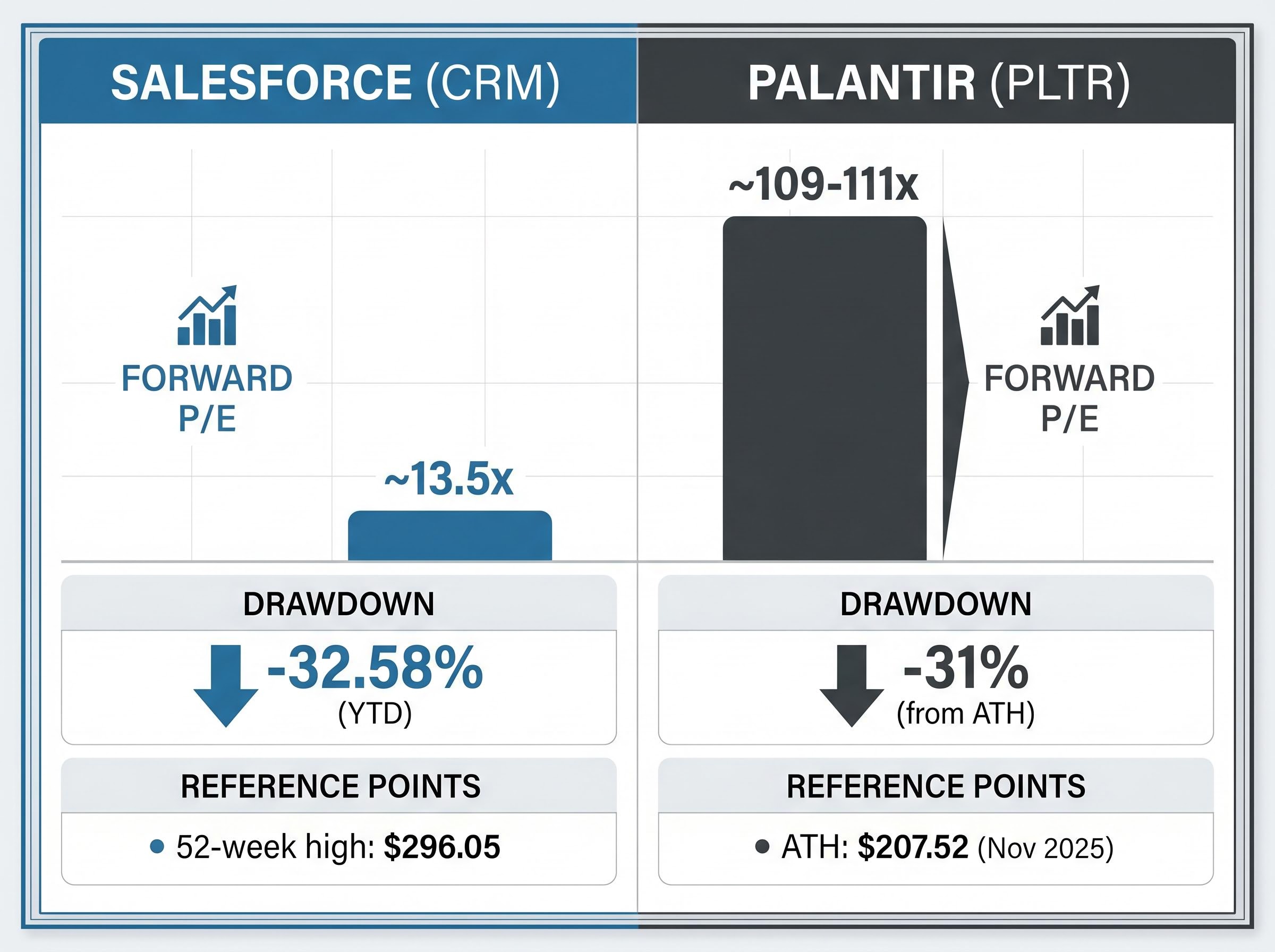

CRM closed at approximately $182.14 on 17 April, the day Burry entered. By 24 April, the stock had slipped to $178.16, leaving the position modestly underwater. The year-to-date decline stood at approximately 32.58% as of that date. Burry did not disclose his position size.

The distinction Burry drew between price and value is the analytical core of the trade. The market priced CRM as though the business were deteriorating; Burry’s thesis is that the compression reflects fear, not fundamentals.

The numbers tell the story before any analyst commentary does.

Salesforce traded at a forward price-to-earnings (P/E) ratio of approximately 13.5x as of late April 2026. Palantir traded at approximately 109-111x. That is not a modest gap. It is an eightfold difference in what the market is willing to pay per dollar of expected earnings over the next twelve months.

Forward P/E compares a company’s current share price to its expected earnings per share over the next 12 months. A higher ratio signals that the market is pricing in stronger future growth, but it also means more downside risk if that growth disappoints.

CRM’s 13.5x reading is unusually compressed for a company generating $11.20 billion in quarterly revenue. The 33% year-to-date decline created the valuation contraction. For Palantir, the 109-111x multiple reflects aggressive growth expectations tied to its government and defence data contracts and AI positioning, but it also makes the stock significantly more exposed to multiple compression if those expectations moderate.

| Metric | Salesforce (CRM) | Palantir (PLTR) | What it signals |

|---|---|---|---|

| Forward P/E | ~13.5x | ~109-111x | CRM priced for minimal growth; PLTR priced for sustained high growth |

| YTD price change | -32.58% | -31% from ATH | Both under pressure, but CRM’s multiple has compressed far more |

| Market cap | ~$152 billion | ~$143.09/share | CRM is a larger enterprise by revenue; PLTR commands a growth premium |

| ATH drawdown | 52-week high: $296.05 | ATH: $207.52 (Nov 2025) | Both significantly off highs; CRM’s drawdown is steeper from its range |

The valuation gap is the single most important number in evaluating Burry’s thesis. At 13.5x forward earnings, Salesforce is being priced closer to a legacy value stock than a $45 billion-revenue enterprise software platform.

ServiceNow’s experience provides a live case study in enterprise software multiple compression: the company reported 22% subscription revenue growth and raised full-year guidance, yet saw its share price fall 17.58% in a single session when forward growth trajectory moderated, illustrating how growth stocks are priced on direction of travel rather than current performance levels.

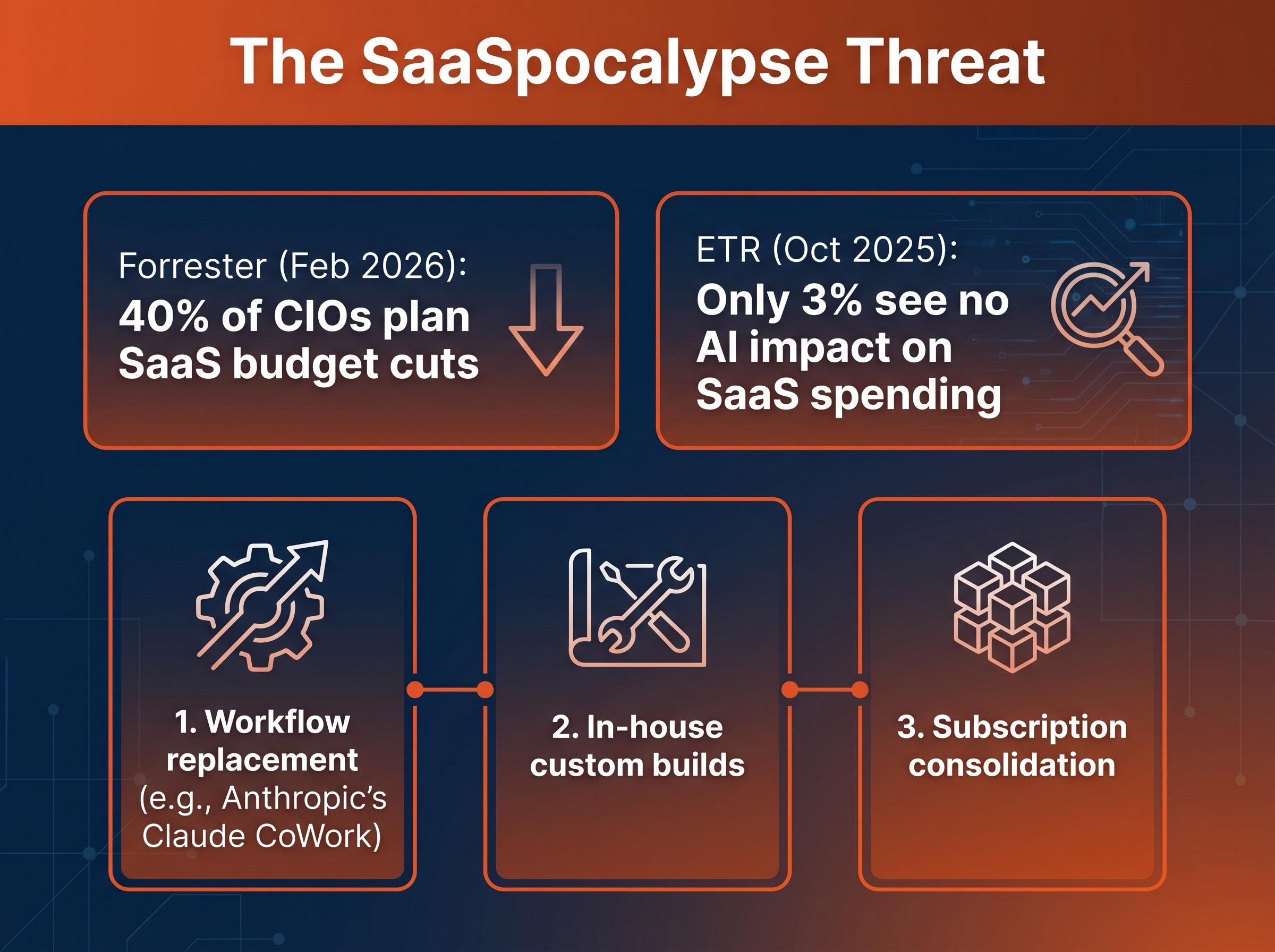

The term is not hyperbole invented by social media. Forrester published a report in February 2026 titled “SaaS as We Know It Is Dead: How to Survive the SaaS-pocalypse,” and the data supporting the thesis is specific.

Forrester’s February 2026 research on SaaS disruption identifies AI agent innovation as the primary mechanism eroding traditional SaaS workflow ownership, with CIOs surveyed reporting active budget reallocation away from point solutions toward AI-augmented platforms.

Forrester, February 2026: “40% of CIOs surveyed plan SaaS budget cuts.”

A separate survey from ETR in October 2025 found that only 3% of respondents saw no AI impact on SaaS spending. The near-universal acknowledgement of disruption pressure is what separates this from a fringe concern.

The threat operates through three specific channels:

The disruption has not fully played out. New AI model releases from OpenAI and Anthropic could trigger further sector-wide multiple compression. For software investors, the question is not whether agentic AI will reshape the sector; the survey data confirms that expectation is already embedded in CIO planning. The question is which platforms survive the reallocation.

The bear case treats all enterprise SaaS platforms as equally exposed. Burry’s thesis, and the analysis supporting it, draws a sharper line.

Salesforce holds years of integrated customer data across sales, marketing, commerce, and service functions. That proprietary data layer is not something a generic large language model can replicate without the underlying infrastructure. A CIO can deploy an agentic AI tool to automate a workflow, but that tool still needs the customer data, relationship history, and cross-functional integration that Salesforce’s platform provides.

Salesforce’s specific structural defences include:

The counterargument deserves honest treatment. Risks persist around in-house CRM builds enabled by large language models and potential per-user pricing pressure as agentic tools reduce the number of human users interacting with the platform. This is not a clean thesis without execution risk.

Crucially, no major software company including Salesforce, Adobe, ServiceNow, or SAP has filed revenue warnings citing AI competition, and the absence of AI disruption evidence in software earnings represents what some analysts characterise as a materially bullish signal hiding inside a bearish-looking price chart.

The consensus view remains broadly constructive. MarketBeat data as of April 2026 shows approximately 37 Strong Buy ratings, roughly 12 Hold ratings, and 1 Strong Sell. The mean price target sits at approximately $276-$283, implying roughly 55% upside from the 24 April close of $178.16.

Wall Street had not materially shifted its stance following Burry’s announcement, which means his move is contrarian even relative to a broadly bullish analyst community. Salesforce’s gross margin of 75.28% and dividend yield of 0.95% provide additional fundamental context for the valuation thesis.

Burry’s credibility rests on a specific kind of track record: being early, being right on the big calls, and being willing to absorb short-term pain while waiting for the thesis to resolve.

That methodology explains why a valuation gap of this magnitude, 13.5x versus 109x, would register as material to Burry. His approach is fundamentals-first, and the Salesforce thesis fits squarely within that framework.

For investors tracking how the broader universe of high-conviction managers is positioning around valuation dislocations, our full explainer on Bill Ackman’s H2 2026 market thesis covers Pershing Square’s argument that S&P 500 index-level valuations overstate broad market expensiveness, the specific H2 catalysts Ackman is pricing in, and how his concentrated bets on Uber, Amazon, and Meta compare structurally to Burry’s compressed-multiple approach.

The specific trade is interesting. The pattern it represents is more instructive.

When a sector trades down on a narrative threat, the stocks with the lowest fundamental multiples and the highest structural durability tend to offer the most asymmetric risk-reward profiles. Burry’s repositioning toward compressed-multiple fundamentals and away from high-multiple growth is a capital allocation case study in that principle.

The research does not confirm that Burry explicitly named Palantir negatively in his Substack post. What is documented is his movement toward a stock trading at 13.5x forward earnings and away from the category of growth-premium names. Palantir’s government and defence data moat may prove more durable than the implied scepticism suggests, but the 109x multiple remains a separate and distinct risk factor.

Salesforce reported Q4 FY2026 revenue of $11.20 billion (up 12% year-over-year) on 25 February 2026, with FY2027 revenue guidance of $45.8-$46.2 billion (approximately 10-11% growth). As of 24 April, CRM had declined approximately 2.2% since Burry’s 17 April entry.

Salesforce’s Q4 FY2026 earnings disclosures confirmed the $11.20 billion quarterly revenue figure and the FY2027 guidance range of $45.8-$46.2 billion, giving investors a primary-source reference point for the financial projections underpinning Burry’s valuation thesis.

Three unresolved risks will determine whether this call ages well:

The thesis is live, not settled.

Burry’s Salesforce bet is fundamentally a valuation argument, not a prediction that the SaaSpocalypse threat is illusory. He is betting that CRM’s proprietary data moat, enterprise integration depth, and 13.5x forward P/E provide enough margin of safety to outperform the sector even if disruption continues. The position was underwater as of 24 April, the sector remains volatile, and the next Salesforce earnings report (Q1 FY2027) will be the first real data point that either validates or challenges the thesis.

Investors tracking this space should watch three variables: CRM’s Q1 FY2027 results, Agentforce adoption metrics disclosed in that report, and any new agentic AI product announcements from OpenAI or Anthropic. Those three inputs will determine whether Burry’s contrarian discipline has identified value the market is mispricing, or whether the selloff reflects a structural shift the numbers have not yet caught up to.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Burry announced on 16 April 2026 via his Substack that he would initiate a Salesforce position the following day, arguing that the stock's roughly 33% year-to-date decline reflected overstated technical and macro pressures rather than fundamental business deterioration, creating a margin of safety at approximately 13.5x forward earnings.

The SaaSpocalypse refers to the disruption of traditional SaaS business models by agentic AI tools, as described in a Forrester report from February 2026, with 40% of CIOs surveyed planning SaaS budget cuts; Burry's thesis holds that Salesforce is more resilient than peers due to its proprietary data moat and Agentforce AI integration.

As of late April 2026, Salesforce traded at approximately 13.5x forward earnings while Palantir traded at approximately 109-111x forward earnings, an eightfold difference that reflects Palantir's aggressive AI-driven growth premium versus Salesforce's deeply compressed multiple following its sharp selloff.

Burry entered Salesforce on 17 April 2026 when CRM closed at approximately $182.14, and by 24 April the stock had declined to $178.16, leaving the position approximately 2.2% underwater with no position size disclosed.

Investors should monitor three key variables: Salesforce's Q1 FY2027 earnings results against forward guidance, Agentforce adoption metrics disclosed in that report, and any new agentic AI product announcements from OpenAI or Anthropic that could trigger additional sector-wide multiple compression.