SEC Moves to End Mandatory Quarterly Reporting After 50 Years

17 hrs ago

Cleveland-Cliffs beat Wall Street estimates on both revenue and earnings in Q1 2026, yet the stock dropped 5% the morning after the release. The disconnect between headline performance and share price movement raises the question of what investors are actually pricing in for the steelmaker.

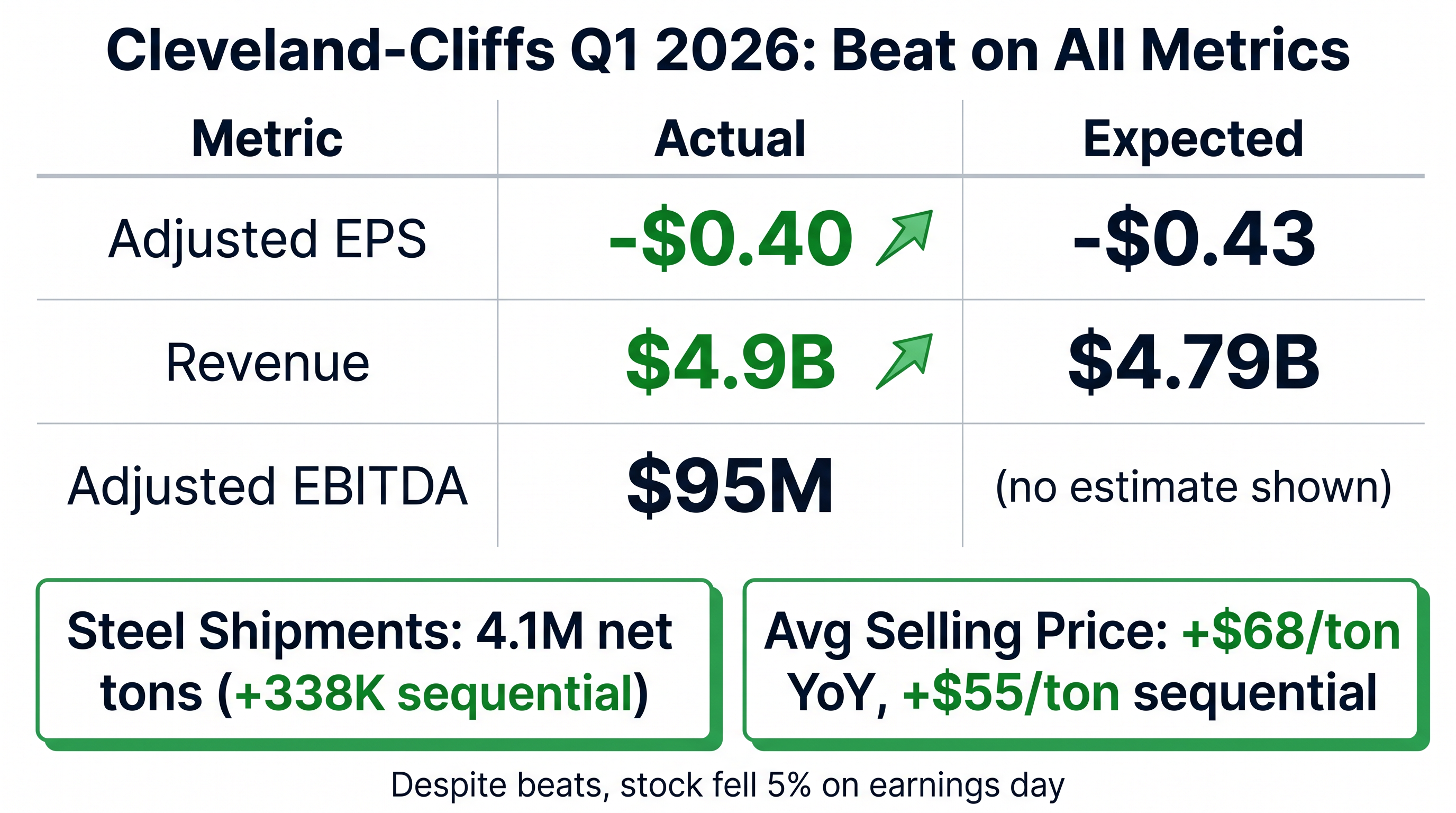

The Q1 earnings release on 20 April delivered adjusted EPS of -$0.40 versus -$0.43 expected, and revenue of $4.9 billion versus $4.79 billion expected. Both represented outperformance against a backdrop of steel prices near two-year highs. Yet the market reaction suggests deeper concerns about cost sustainability and strategic execution persist.

For investors evaluating CLF, the gap between operational momentum and market scepticism demands closer examination. This analysis breaks down what the Q1 numbers actually reveal about Cleveland-Cliffs’ trajectory, where the risks and opportunities sit across the coming quarters, and what conditions would need to materialise for the stock to re-rate higher.

The beat was real. Adjusted EPS of -$0.40 came in $0.03 better than consensus, revenue of $4.9 billion exceeded estimates by $110 million, and adjusted EBITDA improved to $95 million from deeply negative territory a year earlier. Steel shipments rose to 4.1 million net tons, up 338,000 tons sequentially, and average selling prices climbed $68 per ton year-over-year and $55 per ton sequentially.

Then the curtain pulled back. An $80 million one-time energy cost impact from extreme February cold crushed what would have been a more meaningful EBITDA improvement. Natural gas prices spiked to three-year highs during the quarter, hitting blast furnace operations and heat treatment processes directly.

The February 2026 natural gas price spike that compressed Cleveland-Cliffs’ Q1 EBITDA by $80 million traced directly to the Iran conflict that triggered the greatest global energy security challenge in history, with cascading supply disruptions pushing spot prices to three-year highs across North American markets.

The operational momentum beneath the noise was solid. Higher shipment volumes and sequential pricing gains showed the core business executing against a constructive market backdrop. But the stock’s 5% drop the next morning signalled the market is focused on cost volatility risk, not headline beats.

Key Q1 metrics:

Energy Cost Impact The $80 million energy cost headwind from the natural gas price spike materially compressed EBITDA despite volume and pricing strength.

Hot-rolled coil priced at $1,101 per ton as of 21 April 2026, up 5% over the past month and near the highest levels since early 2024. The pricing environment is the most constructive it has been in two years. For a company shipping 16.5 to 17.0 million net tons annually, every $10 per ton move in steel pricing has an outsized impact on EBITDA.

Management guided a $60 per ton sequential price rise for Q2, building on the momentum already visible in Q1 average selling prices. Trade protections and global supply disruptions are raising imported steel costs, benefiting domestic producers like Cleveland-Cliffs. The tailwind is structural, not transient.

The White House proclamation on modified Section 232 tariffs for steel imports established new tariff rates up to 50% applied to the full customs value of steel products, which raises imported steel costs and directly benefits domestic producers operating in the U.S. market.

Revenue diversification across three major segments provides demand stability:

| Segment | Revenue | % of Total |

|---|---|---|

| Distributors/Converters | $1.5 billion | 31% |

| Infrastructure/Manufacturing | $1.4 billion | 29% |

| Automotive | $1.4 billion | 29% |

No single segment shows breakout strength, but overall order books are full with extended lead times. Resilient U.S. supply chains and shifts from aluminium to steel in automotive and appliances underpin demand.

The question is not whether steel prices are high. The question is whether Cleveland-Cliffs can convert this into free cash flow after cost pressures are accounted for. The pricing environment creates leverage; execution determines whether that leverage compounds or compresses.

Integrated steelmakers like Cleveland-Cliffs operate high-fixed-cost businesses where profitability is determined by the spread between selling prices and production costs, not just revenue levels. A company can beat revenue estimates and still disappoint the market if the cost side erodes margins faster than the top line grows.

Natural gas plays a critical role in steelmaking. Blast furnace operations require sustained heat, and heat treatment processes lock in metallurgical properties. When natural gas prices spike, as they did to three-year highs in February 2026, the impact flows directly to the bottom line. There is no hedging delay, no inventory buffer. The cost hits immediately.

Utilisation rates matter because they spread fixed costs across more tons. Higher shipment volumes improve per-unit economics. Cleveland-Cliffs has optimised operations by idling less efficient plate mills, enhancing efficiency without losing capability. But utilisation only helps if the variable cost base stays disciplined.

Three factors drive steelmaker profitability:

For investors unfamiliar with steel sector dynamics, understanding the cost-spread model explains why the market can punish a stock that beat estimates. Revenue growth means little if the cost side is eroding margins faster. The Q1 earnings reaction was a textbook example of this principle in action.

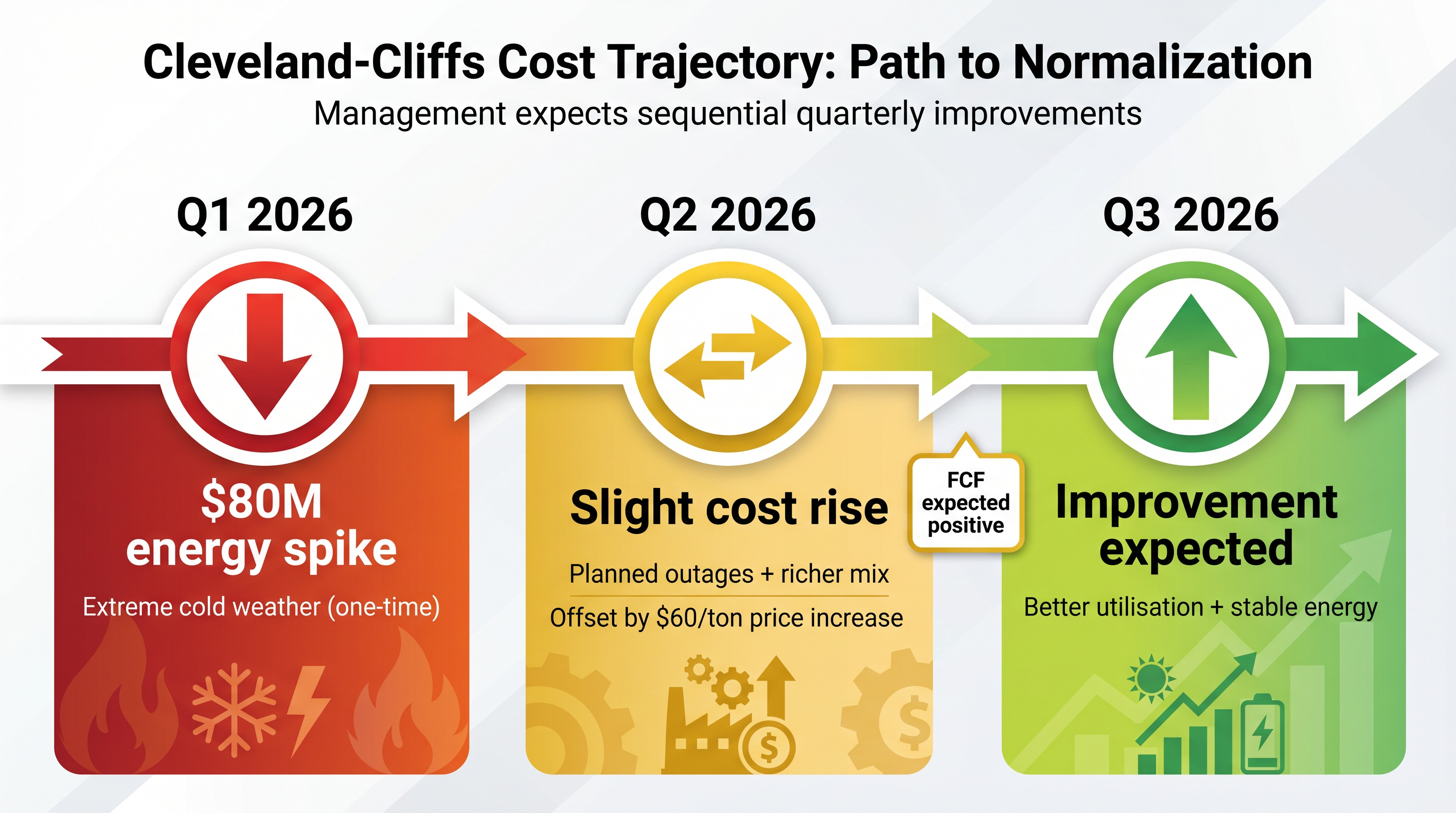

Management laid out a quarterly cost trajectory that suggests improving conditions ahead, but the path is not smooth. Q2 costs are expected to rise slightly from planned outages and a richer product mix, offset by the $60 per ton price increase already underway. Q3 is expected to show improvement from better utilisation and stable energy conditions.

The $80 million Q1 energy spike is non-recurring under normal weather conditions. That much is clear. What is less clear is the trajectory of costs in the quarters ahead, as management expects slight increases in Q2 before improvement materialises in Q3.

Commodity price volatility in Q1 2026, including the 9.6% oil crash that followed Iran’s reopening of the Strait of Hormuz, illustrates how quickly energy input costs can reverse when geopolitical risk premiums evaporate, a dynamic that could support Cleveland-Cliffs’ cost normalisation thesis if natural gas follows a similar trajectory.

Working capital built $130 million in Q1 from rising accounts receivable, prices, and shipments. Q2 is expected to see a slight release via inventory reductions, supporting free cash flow generation. Management expects Q2 free cash flow to turn positive.

Quarterly cost trajectory:

Cost Guidance Management expects sequential quarterly improvements in earnings and cash flow, with Q2 free cash flow expected to turn positive.

The cost guidance shows the path forward. Investors are right to question whether Q2 and Q3 will hold to the improved trajectory management now projects. Q2 is a prove-it quarter for cost execution.

No deal has been announced despite the original H1 2026 target. Management cited evolving market and geopolitical conditions, including Middle East currency disruptions affecting South Korea, as factors delaying finalisation. Discussions remain ongoing, but the tone from management suggests reduced urgency rather than collapsed negotiations.

U.S. market strength has made Cleveland-Cliffs less dependent on external capital or partnerships. Steel pricing near two-year highs and improving volume trends reduce the strategic necessity of a partnership in the near term. Management indicated no rush to finalise.

What a partnership could offer remains speculative: potential technology sharing, capacity optimisation, or financial investment. No terms have been disclosed. No asset sales, including Toledo or FPT, are tied to the partnership discussions.

What remains unknown about the partnership:

The POSCO partnership is potential upside, not a base case assumption. Investors should view it as optionality that could accelerate deleveraging or capacity optimisation if announced. But it is not a catalyst to underwrite in the near term.

For investors wanting to understand the broader strategic options Cleveland-Cliffs could pursue beyond the POSCO partnership, our dedicated guide to what strategic reviews mean for shareholders covers asset sales, capacity optimisation, and partnership structures with case studies from recent industrial sector reviews.

Current analyst consensus is a Hold rating with an average price target around $11.50. At $9.44 post-earnings, the stock trades at a 20%+ discount to average targets. But this gap reflects uncertainty rather than conviction. Recent price targets from JP Morgan at $10.00 (set 14 April 2026) and Wells Fargo at $9.00 (set 19 March 2026) reflect cautious positioning.

The 52-week range of $5.63 to $16.70 illustrates the volatility Cleveland-Cliffs has experienced over the past year. The current price sits closer to the low end of that range than the high, despite steel pricing conditions that are materially better than they were at the range’s peak.

| Firm | Analyst | Price Target | Date |

|---|---|---|---|

| JP Morgan | Bill Peterson | $10.00 | 14 April 2026 |

| Wells Fargo | Timna Tanners | $9.00 | 19 March 2026 |

| Consensus Average | – | $11.50 | – |

What would change sentiment? Two consecutive quarters of positive free cash flow would demonstrate that pricing tailwinds are converting into cash generation. Cost guidance that holds without revision would restore forecasting credibility. A POSCO deal announcement would provide strategic optionality and potentially accelerate deleveraging.

The valuation gap between current price and analyst targets exists because the market is discounting execution risk. For investors considering CLF, the setup offers asymmetric upside if cost control improves. But the Hold consensus reflects that this improvement is not yet proven. The stock’s re-rating depends on delivery, not potential.

Cleveland-Cliffs delivered a better-than-expected Q1 on revenue and earnings, but the market’s 5% selloff signals that investors are focused on cost volatility and execution risk rather than headline beats. Steel pricing near two-year highs creates real EBITDA leverage potential, but the company needs to demonstrate cost control in Q2 and Q3 to convert pricing tailwinds into shareholder value.

The $80 million one-time energy hit was real, and it masked what would have been a stronger EBITDA print. Management expects sequential quarterly improvements ahead, with Q2 free cash flow expected to turn positive. The POSCO partnership is optionality, not a base case assumption. Analyst targets imply 20%+ upside, but consensus remains Hold pending execution proof.

Investors should watch Q2 results closely for evidence of cost normalisation and free cash flow generation. The stock’s re-rating depends less on steel prices, which are already supportive, and more on whether management can deliver on cost guidance. The setup is there. The execution has yet to follow.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Despite beating adjusted EPS and revenue estimates, the market focused on cost volatility risks, particularly an $80 million one-time energy cost hit from February's natural gas spike, which compressed EBITDA and raised concerns about future cost execution.

Cleveland-Cliffs has been in discussions with South Korean steelmaker POSCO for a potential partnership that could involve technology sharing, capacity optimisation, or financial investment, but the original H1 2026 target has been missed and no terms have been disclosed, making it optionality rather than a near-term catalyst.

Cleveland-Cliffs ships 16.5 to 17.0 million net tons annually, so every $10 per ton move in steel pricing has an outsized impact on EBITDA, with hot-rolled coil near $1,101 per ton in April 2026 creating significant leverage if the company can control its cost base.

The consensus analyst price target sits around $11.50, implying more than 20% upside from the post-earnings price of $9.44, though the consensus rating remains a Hold as analysts wait for proof of cost control and positive free cash flow generation.

Investors should monitor whether Q2 free cash flow turns positive as management guided, whether the $60 per ton sequential price increase flows through to EBITDA, and whether cost guidance holds without further upward revision.