Oil Crashes 9.6% as Iran Reopens Strait of Hormuz

Key Takeaways

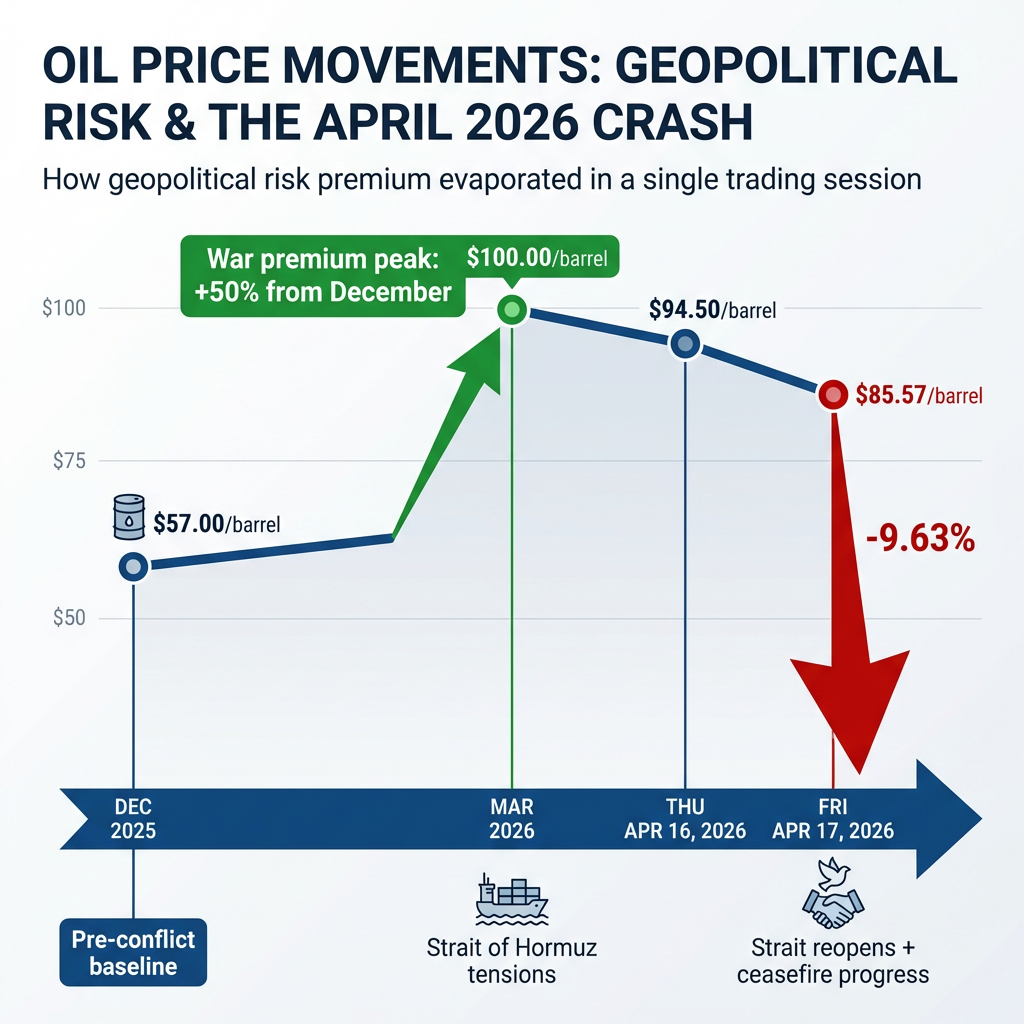

- Crude oil prices crashed 9.63% on April 17, 2026, closing at $85.57 per barrel after Iran confirmed the Strait of Hormuz had reopened and ceasefire negotiations advanced.

- The World Bank forecasts aggregate commodity prices will decline 7% in 2026 to six-year lows, while J.P. Morgan projects Brent crude will average $60 per barrel for the year.

- Commodity markets are fragmenting structurally, with lithium carbonate surging 110% year-over-year and gold approaching $4,850, even as traditional energy commodities face sustained bearish pressure.

- Lower commodity prices signal reduced U.S. inflation expectations, but bond markets remain cautious with the 10-year Treasury yield at 4.244%, suggesting the Fed is unlikely to cut rates imminently.

- A global oil surplus projected at 1.2 million barrels per day provides fundamental support for sustained lower energy prices beyond the temporary geopolitical risk premium reversal.

Crude oil prices crashed 9.63% on Friday, April 17, 2026, closing at $85.57 per barrel in one of the sharpest single-day declines this year. The collapse followed Iran’s declaration that the Strait of Hormuz had reopened and confirmation of progress in Persian Gulf ceasefire negotiations, eliminating the geopolitical risk premium that had inflated energy markets for weeks.

Brent crude dropped from approximately $100 per barrel on Thursday to roughly $90 on Friday. Despite the dramatic crash, oil remains more than 50% above its December 2025 levels. The broader commodity selloff extended beyond energy, with the S&P GSCI commodity spot index falling 4.45% to 679.10, signalling widespread weakness across raw materials markets.

Oil Prices Crash Nearly 10% as Strait of Hormuz Reopens

The April 17 collapse represents a sharp reversal of the war premium that had dominated pricing throughout March 2026. When geopolitical conflicts threaten critical supply routes or production regions, commodity traders incorporate risk premiums into prices to account for potential disruptions. Iran’s confirmation that the Strait of Hormuz (a chokepoint handling roughly one-fifth of global oil shipments) was open for transit removed the primary catalyst supporting elevated prices.

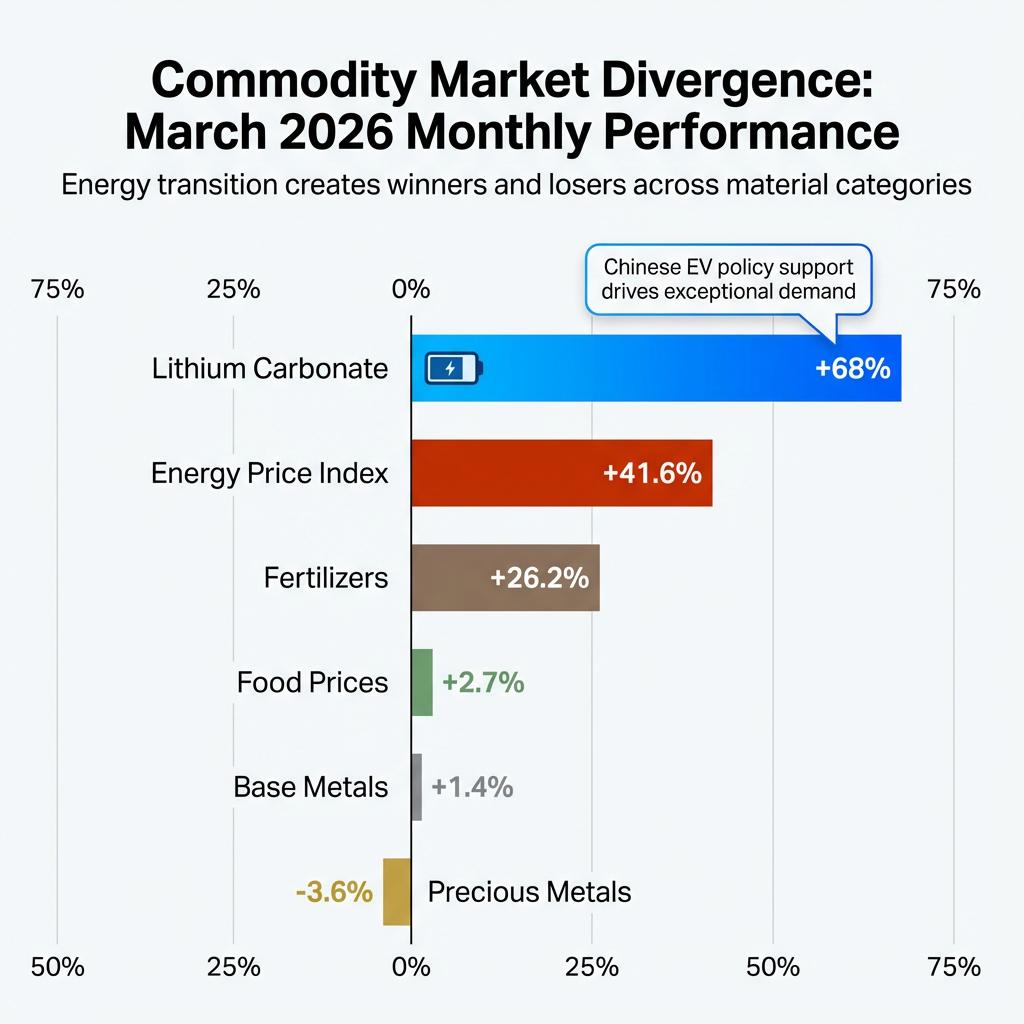

The World Bank’s energy price index surged 41.6% in March 2026, driven largely by crude oil increasing 40.5% and European natural gas jumping 59.4% as Middle East tensions escalated. This represents a textbook example of war premium inflation, where perceived supply threats push prices well beyond levels justified by actual supply and demand fundamentals. The swift April correction demonstrates how rapidly these premiums can evaporate when the underlying threat diminishes.

The March 2026 energy crisis stemming from Iran conflict created the war premium that inflated crude oil prices above $100 per barrel before the April 17 crash.

The EIA’s Short-Term Energy Outlook on crude oil price projections provides the authoritative U.S. government analysis of global supply-demand balances driving the oversupply conditions that support sustained price weakness.

Market participants had priced in significant supply disruption risk during the conflict period. When ceasefire progress materialised and transport routes reopened, the inflated risk component vanished within a single trading session, triggering the 9.63% crash.

When big ASX news breaks, our subscribers know first

What Drives Commodity Price Crashes

War premiums occur when geopolitical conflicts threaten supply routes or production infrastructure. Traders add risk premiums to commodity prices to compensate for potential shortages, even if actual supply remains unaffected. In March 2026, the World Bank’s energy price index surged 41.6%, primarily due to Middle East tensions affecting the Strait of Hormuz, which handles approximately one-fifth of global oil shipments.

When tensions ease, these premiums disappear rapidly. The April 17 crash illustrates this reversal mechanism perfectly. Once Iran confirmed the Strait was operational and ceasefire negotiations advanced, the perceived supply threat diminished substantially. The war premium that had inflated prices during the conflict period was neutralised within a single trading session, causing the sharp correction from approximately $100 to $90 for Brent crude.

Broader Commodity Market Trends in April 2026

Whilst traditional energy commodities crashed, commodity markets experienced what analysts describe as structural fragmentation rather than uniform weakness. Gold futures rose 0.85% to $4,849.40 on April 17, serving as a safe-haven hedge amid geopolitical uncertainty despite the broader selloff.

March 2026 commodity trends before the crash revealed divergent sector performance:

- Food prices increased 2.7%

- Fertilisers rose 26.2%

- Base metals gained 1.4%

- Precious metals declined 3.6%

- Lithium carbonate surged 68% monthly and 110% year-over-year

The lithium rally stems from Chinese policy changes effective April 2026 supporting electric vehicle production, creating exceptional demand for battery-grade materials. This divergence underscores the structural shift in commodity markets, where energy transition metals experience boom conditions even as traditional energy commodities face bearish pressure. The fragmentation reflects the global transition from fossil fuel dependence toward renewable energy systems, creating winners and losers across different material categories.

Expert Outlook: Why This Decline May Persist

Market analysts view the April price drop as sustainable rather than a temporary correction, supported by fundamental oversupply conditions. The World Bank forecasts aggregate commodity prices will decline 7% in 2026 to six-year lows. J.P. Morgan projects Brent crude will average $60 per barrel in 2026 despite recent geopolitical spikes, citing persistent structural headwinds.

The World Bank’s Commodity Markets Outlook forecasting methodology tracks the Energy Price Index movements cited throughout this analysis and provides the institutional framework for long-term commodity price projections used by global policymakers.

Fundamental factors supporting sustained low prices include:

- Global oil surplus projected at 1.2 million barrels per day

- Robust Americas production providing substantial supply buffer

- Weak global economic growth reducing industrial demand

- China economic slowdown cutting consumption of industrial commodities

Contrary to the bearish energy outlook, IG analysts predict gold could reach $5,000 and silver above $65 in a price discovery phase, suggesting continued divergence between energy commodities and safe-haven precious metals. The sustainability of energy price declines is affirmed by persistent oversupply conditions that existed before the geopolitical tensions and remain intact after the risk premium evaporated.

Implications for Inflation and Federal Reserve Policy

The commodity prices crash signals lower U.S. inflation expectations, as cheaper energy and food inputs reduce cost pressures across the economy. Lower raw material costs support a potential soft landing scenario for transport and manufacturing sectors, which had faced margin compression during the March price surge. Producer prices had climbed reflecting elevated energy costs, but the April correction may reverse some of these inflationary pressures.

Understanding how energy price movements influence inflation dynamics helps explain why the commodity crash signals lower U.S. inflation expectations and potentially shifts Federal Reserve policy calculus.

Despite the equity market rally following the oil crash, fixed-income markets remained sceptical. The 10-year Treasury yield finished at 4.244%, well above the February 27 pre-conflict low of 3.961%. Bond traders appear unconvinced the Federal Reserve will cut rates in the near term, given oil remains more than 50% above December levels and producer prices have climbed during the recent volatility.

The bond market’s cautious stance reflects why elevated oil prices dampened Fed rate cut expectations earlier in 2026, even as the April crash may shift this calculus for future policy decisions.

Reduced commodity-driven inflation provides the Fed with greater policy flexibility, but sustained lower prices would be needed before rate cut expectations materially shift. The divergence between equity market optimism (celebrating lower input costs) and bond market caution (questioning inflation trajectory) reflects ongoing uncertainty about whether the price decline represents a durable trend or temporary correction vulnerable to renewed geopolitical instability.

The next major ASX story will hit our subscribers first

Industry Winners and Losers from the Commodity Crash

The commodity prices crash creates divergent impacts across U.S. industries. Commodity-dependent sectors gain from lower input costs, whilst producers face revenue pressure and margin compression.

Industries benefiting from lower commodity prices:

- Manufacturing and transport sectors gain from reduced energy and materials costs

- U.S. farmers benefit from easing agricultural commodity prices and moderating fertiliser costs (after March’s 26.2% spike)

- Consumer goods companies see lower raw material expenses

- Battery and electric vehicle supply chains benefit from improved lithium availability

Industries facing headwinds:

- Energy majors face significant pressure from oil glut and price crash (though Americas production provides some buffer for U.S. firms)

- Mining companies in base and precious metals see margin compression

- Resource-exporting regions face revenue challenges

What to Watch Next in Commodity Markets

Several factors will determine whether the price decline continues or reverses in coming months:

- Persian Gulf ceasefire negotiations and durability of the agreement

- China economic data indicating demand recovery or continued slowdown

- Americas oil production levels sustaining current surplus conditions

- Federal Reserve communications on inflation outlook and policy direction

- Any new supply disruptions that could reinstate geopolitical risk premiums

Prices have not stabilised or rebounded based on available data through mid-April 2026. Future significant price impacts would require geopolitical escalation substantial enough to overcome current surplus conditions. The structural oversupply, projected at 1.2 million barrels per day, suggests the bearish trend has fundamental support beyond temporary geopolitical factors.

For investors positioning portfolios amid divergent commodity performance and geopolitical uncertainty, understanding investment strategies for navigating commodity market volatility can help capitalize on the structural shifts between energy, precious metals, and battery materials.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What caused the commodity prices crash on April 17, 2026?

The crash was triggered by Iran confirming the Strait of Hormuz had reopened and progress in Persian Gulf ceasefire negotiations, which eliminated the war risk premium that had inflated energy prices for weeks.

What is a war premium in commodity markets?

A war premium is the additional cost traders build into commodity prices to account for potential supply disruptions caused by geopolitical conflicts, even when actual supply remains unaffected — when the threat eases, the premium evaporates rapidly.

How far did oil prices fall on April 17, 2026?

Brent crude dropped from approximately $100 per barrel on Thursday to roughly $90 on Friday, a decline of 9.63%, though oil still remained more than 50% above its December 2025 levels.

How does the commodity prices crash affect Federal Reserve rate cut expectations?

Lower energy and raw material costs reduce inflationary pressure, giving the Fed more flexibility to cut rates, but bond markets remain cautious as the 10-year Treasury yield stayed at 4.244% — well above pre-conflict lows — signalling scepticism about near-term cuts.

Which commodities are rising despite the broader commodity prices crash?

Gold rose 0.85% to $4,849.40 on April 17 as a safe-haven asset, and lithium carbonate surged 68% in March and 110% year-over-year due to Chinese policy changes supporting electric vehicle production.