Crude Oil Surges Past $108 as Iran Strike Is Called Off

5 hrs ago

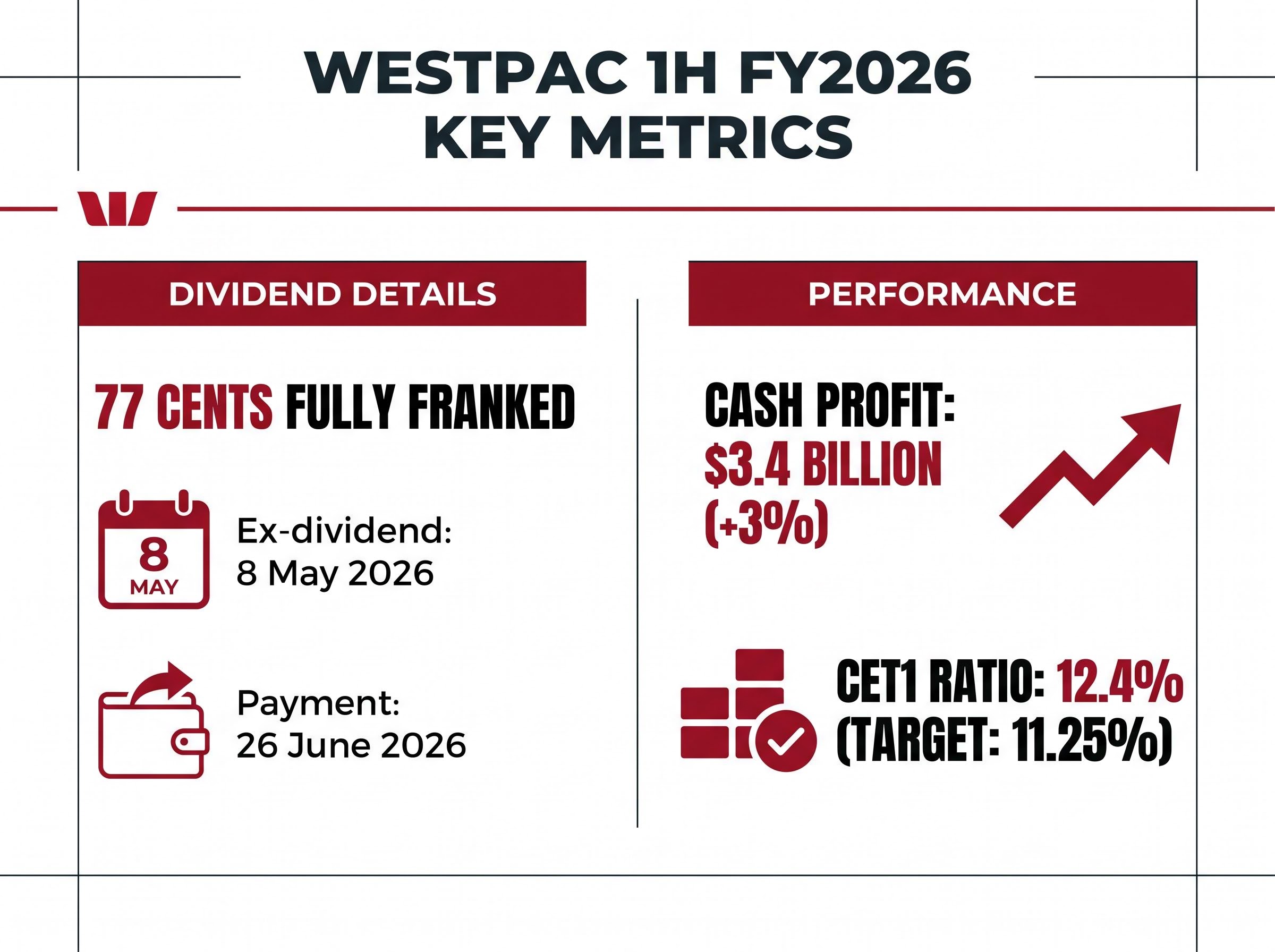

Westpac shareholders have roughly 48 hours to secure a 77-cent fully franked interim dividend. The ex-dividend date falls on 8 May 2026, and investors who do not hold shares before that date will miss the payment entirely.

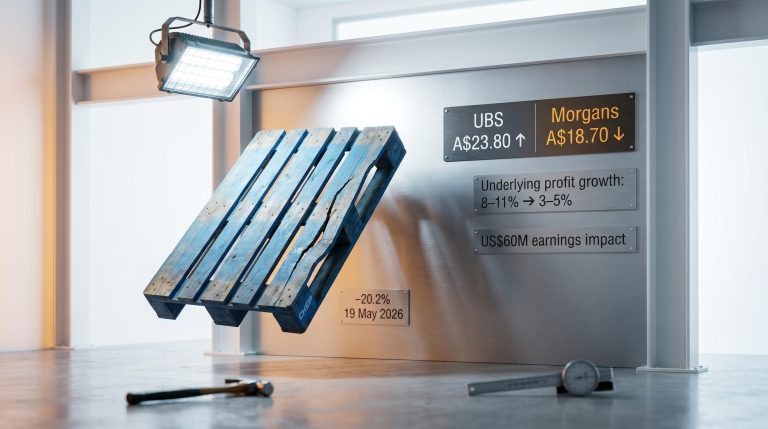

The dividend was declared alongside Westpac’s 1H FY2026 results on 5 May 2026, which showed a 3% cash profit rise to $3.4 billion and a Common Equity Tier 1 (CET1) capital ratio of 12.4%, comfortably above the bank’s own 11.25% target. Despite the solid fundamentals, WBC shares fell approximately 2.3% on results day to close at $37.63.

What follows covers exactly who qualifies for the payment, how the ASX’s T+2 settlement rule determines eligibility, what the fully franked status means in dollar terms for Australian taxpayers, and how Westpac’s dividend reinvestment plan compares to NAB’s rival offering. With the eligibility window closing on Thursday, the mechanics matter.

Westpac’s 1H FY2026 interim dividend is 77 cents per share, fully franked, payable on 26 June 2026. The figure is flat on the preceding half but represents a modest 1.3% increase on the prior year’s interim payout.

Key details at a glance:

The 77.1% statutory payout ratio sits slightly above Westpac’s stated 65-75% medium-term target range, a detail worth monitoring for yield investors assessing whether this level of distribution can be sustained.

That said, the $3.723 billion franking credit balance and $2.7 billion in surplus capital provide a meaningful buffer. The payout ratio is elevated; the balance sheet capacity to support it is not in question.

The ex-dividend date is 8 May 2026. Shares must be purchased before that date for the buyer to receive the 77-cent payment.

The reason comes down to the ASX’s T+2 settlement rule, which has been in place since 2016. It works in three steps:

The ASX T+2 settlement transition rules formalized the shift from a three-day to a two-day settlement cycle in 2016, with the ex-dividend date mechanics for all ASX-listed securities, including WBC, determined directly by this framework.

Because settlement takes two business days, buying on or after the ex-dividend date means the buyer will not be registered as a holder in time. The 77 cents goes to whoever held the shares before the cutoff.

Qualifying for both the cash dividend and the franking credit requires more than purchasing before the ex-dividend date; the 45-day holding rule also applies, meaning shares must be held genuinely at risk for a minimum of 45 days around the ex-dividend date for most investors to claim the credit.

There is conflicting information across secondary sources regarding the exact record date. Investors should verify the precise date via the official Westpac investor centre at westpac.com.au or the ASX company page for WBC before acting.

Selling before 8 May transfers both the shares and the dividend entitlement to the buyer, because the buyer’s name will be registered on the record date after T+2 settlement.

Selling on or after 8 May is a different outcome. In that case, the seller retains the dividend because their name was already locked into the register at the record date. The buyer receives the shares but not the payout.

When Westpac pays a fully franked dividend, it means the company has already paid 30% corporate tax on the profits distributed. Australian resident shareholders receive a franking credit that can be used to offset their personal tax liability, or, for those on lower marginal rates, claimed as a cash refund.

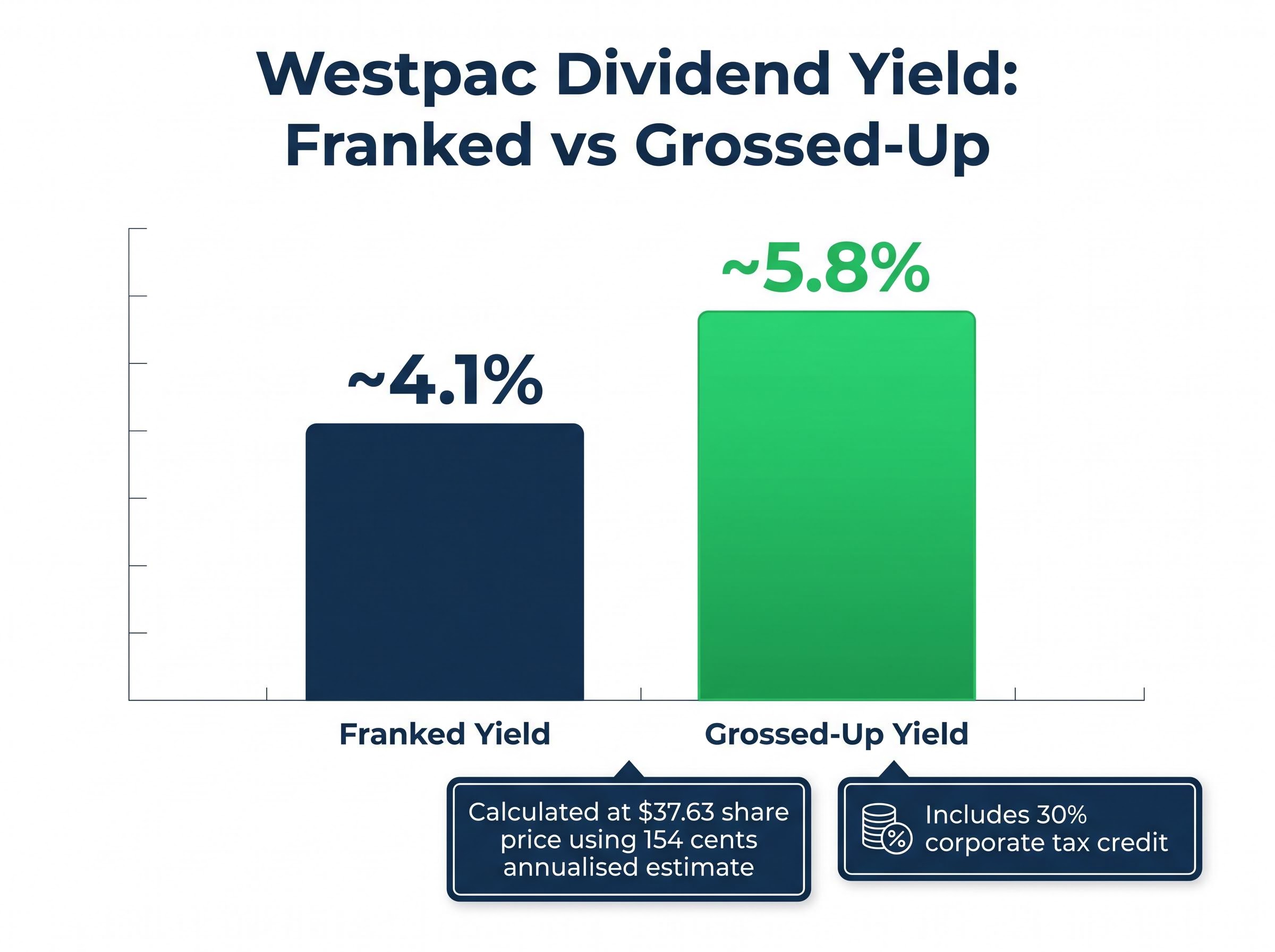

At the 5 May 2026 closing price of $37.63, and using an annualised dividend estimate of approximately 154 cents (two interim payments at 77 cents each), the numbers translate as follows:

| Measure | Yield |

|---|---|

| Franked dividend yield | ~4.1% |

| Grossed-up yield (including franking credits) | ~5.8% |

The grossed-up yield is calculated by dividing the franked yield by (1 minus 0.30), which accounts for the 30% corporate tax already paid.

Franking credit mechanics work differently across investor types: a superannuation fund in accumulation phase pays 15% tax and uses the credit to reduce that liability, while an SMSF in pension phase and eligible low-income retirees receive the full credit as a cash refund from the ATO, converting a $70 cash dividend into $100 of total value at the 30% corporate tax rate.

For self-managed super fund (SMSF) investors in the pension phase and low-income individuals, the grossed-up yield of approximately 5.8% is the more meaningful figure, because excess franking credits can be received as a cash refund from the Australian Taxation Office.

Westpac’s dividend reinvestment plan (DRP) prices new shares at the five-day volume-weighted average price (VWAP) with no discount applied, as confirmed in the 5 May 2026 ASX release. Participants receive shares at market value rather than below it.

NAB’s DRP, announced on approximately 28 April 2026, offers a 1.5% discount on its five-day VWAP pricing post ex-dividend. That structural difference compounds over time.

| Feature | Westpac DRP | NAB DRP |

|---|---|---|

| Pricing method | 5-day VWAP | 5-day VWAP (post ex-dividend) |

| Discount | Nil | 1.5% |

| VWAP window | 5 trading days | 5 trading days |

| Election deadline | Aligned with record date (confirm via Westpac investor centre) | Aligned with record date |

The distinction matters most for investors who reinvest at every cycle. Westpac’s DRP suits holders who want to avoid brokerage on small additional share purchases. NAB’s discount structure favours yield-compounders who prioritise long-run share accumulation at favourable prices. Over multiple dividends, a 1.5% structural discount produces a measurable difference in total shares acquired.

WBC shares closed at $37.63 on 5 May 2026, down approximately 2.3% from the previous close of $38.50. The market’s response was cautious, but the underlying numbers tell a more nuanced story.

The headline figures:

The statutory decline reflects items that sit outside core operating performance. On a cash basis, which strips out those effects, profit grew. The 12.4% CET1 ratio and $2.7 billion capital surplus suggest the balance sheet is in a position of strength, not strain, regardless of the headline profit direction.

ASX big four bank dividends carry a structural tension that is relevant to any income investor holding WBC: Morgans has issued sell ratings on all four banks, with Westpac’s payout ratio of approximately 76% sitting above its own stated target range and flagged as one of the higher-risk profiles in the sector.

Australian mortgage volumes grew at 1.2 times system rate (excluding RAMS), with business and institutional lending also rising over the prior year period. Operating costs declined relative to the preceding half, supporting margin stability and providing room for the dividend payout to be maintained at current levels.

A share price dip on results day often unsettles retail investors. In this case, the capital metrics and lending growth trends indicate the market priced in caution rather than concern.

The eligibility window is closing. Three steps can convert the detail above into decisions:

Investors should verify all dates directly via the official Westpac investor centre or the ASX WBC company page before making any decisions based on this article.

The 77-cent payment arrives on 26 June 2026. At yesterday’s close of $37.63, the grossed-up yield sits at approximately 5.8% for eligible Australian taxpayers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The Westpac dividend ex-dividend date is 8 May 2026. Investors must hold shares before this date under the ASX T+2 settlement rule to be registered as eligible for the 77-cent fully franked payment.

Fully franked means Westpac has already paid 30% corporate tax on the profits being distributed, so Australian resident shareholders receive a franking credit they can use to offset personal tax or claim as a cash refund if their marginal rate is lower than 30%.

To qualify, you must purchase WBC shares at least two business days before the ex-dividend date of 8 May 2026 to allow for T+2 settlement, ensuring your name appears on the shareholder register by the record date.

Based on the 5 May 2026 closing price of $37.63 and an annualised estimate of 154 cents per share, the grossed-up yield including franking credits is approximately 5.8%, which is the most relevant figure for SMSF pension-phase investors who can receive excess franking credits as a cash refund.

Westpac's DRP prices new shares at the five-day VWAP with no discount, while NAB's DRP offers a 1.5% discount on its equivalent VWAP pricing, meaning NAB's plan is more favourable for long-term investors focused on accumulating shares at below-market prices over multiple dividend cycles.