Crude Drops 4% on Hormuz Hopes, but the Deal Isn’t Done

4 hrs ago

The latest Virtu Financial earnings update triggered a dramatic pre-market response on 29 April 2026, with shares jumping 5.81% to $51.75. Wall Street had originally anticipated a moderate quarterly performance, pricing in standard seasonal volume adjustments across global equities. The actual results completely shattered those projections, delivering nearly double the anticipated top-line revenue and forcing institutional analysts to rapidly adjust their forward valuation models. This magnitude of financial outperformance demands a rigorous examination of the underlying mechanics driving the firm’s profitability.

Investors navigating this complex financial environment require clarity on how these exceptional yields were generated, and whether the underlying strategy can sustain this trajectory throughout the remainder of the year. What follows is a detailed analysis of the specific capital deployments, divisional performances, and contrarian talent strategies that engineered this historic first quarter.

The sheer scale of the financial surprise provides the necessary foundation for understanding the company’s current valuation premium. Management reported total revenues of $1.095 billion for the first quarter of 2026, representing a 30.7% year-over-year increase. This figure decisively eclipsed the pre-earnings Wall Street expectation of $593.11 million, demonstrating a massive gap between external forecasting and internal execution.

The official first quarter 8-K regulatory filing confirms this robust financial momentum, detailing how the massive revenue jump cascaded directly into the firm’s expanded operational margins.

Bottom-line profitability metrics showcased even more pronounced expansion. Normalized adjusted earnings per share reached $2.24, beating the $1.51 consensus estimate by 48%. Overall net income surged to $346.6 million, an 82.8% year-over-year increase that easily outpaced prior projections capping the quarter at $310 million.

Operational efficiency scaled alongside revenue, resulting in impressive adjusted EBITDA margin expansion. The firm generated an adjusted EBITDA of $520.6 million, translating to a 66.2% margin. Investors need to see this raw data cleanly separated from typical market noise to understand that this price jump is driven by fundamental earnings power, not speculative trading momentum.

| First Quarter 2026 Metric | Wall Street Estimate | Actual Reported Figure |

|---|---|---|

| Total Revenues | $593.11 million | $1.095 billion |

| Normalized Adjusted EPS | $1.51 | $2.24 |

| Net Income | $290 million – $310 million | $346.6 million |

To comprehend how the firm achieves these outsized returns, one must understand the fundamental mechanics of automated liquidity provision. Market makers do not generate profit by taking directional bets on whether an asset will rise or fall. Instead, they capture the bid-ask spread, buying at a slightly lower price and selling at a slightly higher price millions of times per day.

Sustained market volatility serves as a powerful tailwind for this execution services model. When markets fluctuate rapidly, trading volumes increase, and spreads often widen. This environment allows high-frequency trading operations to process more transactions at wider margins, turning market anxiety into predictable cash flow.

Empirical research on high-frequency trading validates this structural dynamic, showing that while automated algorithms typically provide baseline liquidity, their execution systems actively monetise the spread discrepancies that occur during volatility spikes.

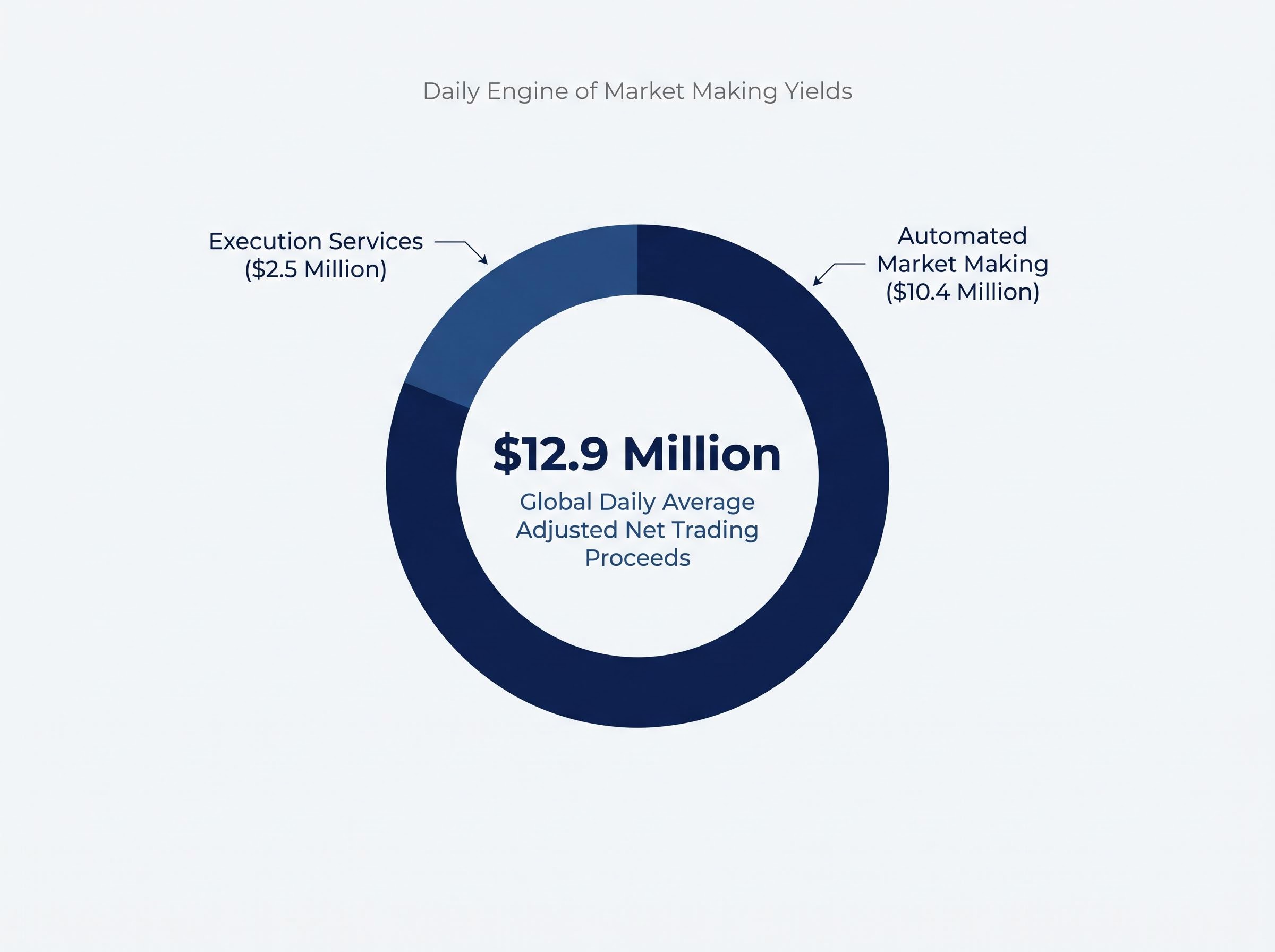

This structural advantage becomes evident when examining the company’s specific daily net trading proceeds across its primary divisions. According to company data, global daily adjusted net trading proceeds averaged $12.9 million throughout the quarter.

Automated Market Making: According to company data, the proprietary trading sector specifically generated $10.4 million in daily net trading proceeds. Execution Services: According to company data, client transaction execution produced a steady $2.5 million daily.

This breakdown empowers readers to grasp the actual mechanics of how the firm monetises daily market activity. Understanding this baseline is highly significant for contextualising the aggressive capital deployment strategy that amplified these core returns.

The current windfall is not a random byproduct of favourable market conditions, but the engineered outcome of deliberate financial architecture. Throughout 2025, leadership made the strategic decision to raise and deploy over $500 million in new trading capital. This expanded monetary base directly amplified the firm’s capacity to capture expanded market opportunities in early 2026.

The addition of this active trading capital specifically enhanced the firm’s capacity to navigate complex options market expansions. Institutional analysis indicates that this expanded base allowed algorithms to hold slightly larger inventory positions during intraday volatility spikes. This structural readiness ensured the firm could process larger order flows without exceeding internal risk parameters.

Because extreme index concentration in major technology stocks often amplifies sudden volatility spikes, this expanded liquidity pool provides a crucial buffer for algorithms absorbing unpredictable retail order surges.

According to company data, total deployed capital measured $2.6 billion by the end of March 2026. According to company data, remarkably, the firm preserved a massive 107% average yield on deployed capital over the trailing twelve months, proving that the additional funds did not dilute overall return efficiency. According to company data, alongside this aggressive capital deployment, the company maintained its commitment to returning direct value to shareholders, keeping disbursements fixed at $0.24 per share.

Strategic Capital Allocation Perspective Financial experts highlight the successful integration of the expanded trading capital as a deliberate shift in the broader corporate strategy, directly enabling the firm to capture outsized returns during periods of heightened options market activity.

This reveals the foresight of the executive team. Investors can observe that the quarterly beat was an engineered outcome of strategic funding rather than a lucky accident of market timing.

The broader financial technology industry is currently consumed by a rush to integrate generative artificial intelligence into operational workflows. In a market obsessed with cost-cutting via automation, there is currently no verified public information detailing the firm’s specific stance on utilizing generative AI versus hiring premium human talent.

Financial engineering requires absolute precision, an area where experimental generative artificial intelligence currently struggles with probabilistic errors. While competitors rush to automate, maintaining an elite workforce of seasoned developers ensures that every algorithmic adjustment is rigorously stress-tested before touching live markets. According to company data, the proportion of revenues allocated to employee monetary remuneration stands firmly at 22%.

According to company data, total organisational headcount is projected to approach 1,100 individuals throughout 2026. Understanding why a leading technology-driven financial firm explicitly invests heavily in human talent over speculative AI tools provides a unique investment perspective.

The strategy acknowledges that while artificial intelligence offers broad processing power, the nuanced risk management required for global market-making demands human oversight. By maintaining premium compensation packages, the firm locks in the intellectual capital necessary to sustain its technological edge against heightened sector rivalry. This talent density enables the rapid deployment of new execution strategies when unprecedented market events occur.

For readers wanting to explore how this human-centric approach creates a structural moat against automated rivals, our detailed coverage of Virtu’s personnel strategies breaks down the firm’s strict technology framework and specialized hiring allocations.

The immediate euphoria of an unprecedented earnings beat often generates speculative forecasting that requires careful recalibration. Following the pre-market surge, wild rumours circulated suggesting full-year EPS projections could exceed $10.16. The newly established analyst consensus corrects these unsustained figures down to a revised, grounded target of $4.13 for the full year.

Despite this moderation in forward estimates, current trading multiples strongly argue that the equity remains attractively priced. Pre-earnings price targets averaging $48.86 have been adjusted upward, with several institutional models now setting targets up to $61 per share. According to company data, the stock currently trades at a price-to-earnings metric of 9.5 and features a highly compelling price-to-earnings-to-growth indicator of 0.13.

According to company data, the operation also generates a substantial 31% yield on shareholder equity. Readers receiving this data-backed outlook can balance the immediate optimism of the quarterly results with realistic valuation multiples. However, forward momentum is never guaranteed, and specific sector risks must be acknowledged.

Several identified corporate hazards could challenge this forward trajectory over the coming quarters. Fluctuating economic environments and sudden shifts in central bank interest rate policies can unpredictably alter trading volumes. Regulatory shifts regarding electronic market making remain a constant operational threat.

Additionally, the firm faces escalating personnel expenditures as it competes for top-tier talent, alongside heightened rivalry from other high-frequency trading operations. Past performance does not guarantee future results, and financial projections are subject to market conditions and these various risk factors.

Furthermore, because high-frequency trading heavily depends on advanced computing infrastructure, these operations remain indirectly exposed to emerging hardware supply chain vulnerabilities currently threatening the broader technology sector.

The historic first quarter of 2026 was delivered through a potent combination of expanded trading capital and premium human talent. By deploying a $2.6 billion capital base through refined execution algorithms, the firm captured exceptional market-making yields. The current valuation multiples, particularly the 9.5 price-to-earnings ratio, suggest the broader market has not fully priced in this newly established baseline of profitability.

The firm’s contrarian strategies position it uniquely for the remainder of the year. By treating elite quantitative developers as a defensive moat rather than a cost centre, the operation secures the reliability required to navigate unpredictable volatility. As volume metrics continue to shift, this well-capitalised foundation provides clear visibility into sustained cash flow generation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The company's Q1 2026 performance resulted from a strategic deployment of over $500 million in new trading capital throughout 2025, significantly enhancing its ability to capitalize on market opportunities.

Virtu Financial prioritizes human talent over generative AI, allocating 22% of revenues to employee remuneration to ensure precision, robust risk management, and a technological edge in complex financial markets.

Virtu Financial currently trades at a price-to-earnings metric of 9.5 and has a compelling price-to-earnings-to-growth indicator of 0.13, alongside a substantial 31% yield on shareholder equity.

Investors face risks from fluctuating economic environments, shifts in central bank policies, regulatory changes, escalating personnel costs, increased rivalry, and potential hardware supply chain vulnerabilities.