Record Highs Are Not the Risk Most Investors Think They Are

7 hrs ago

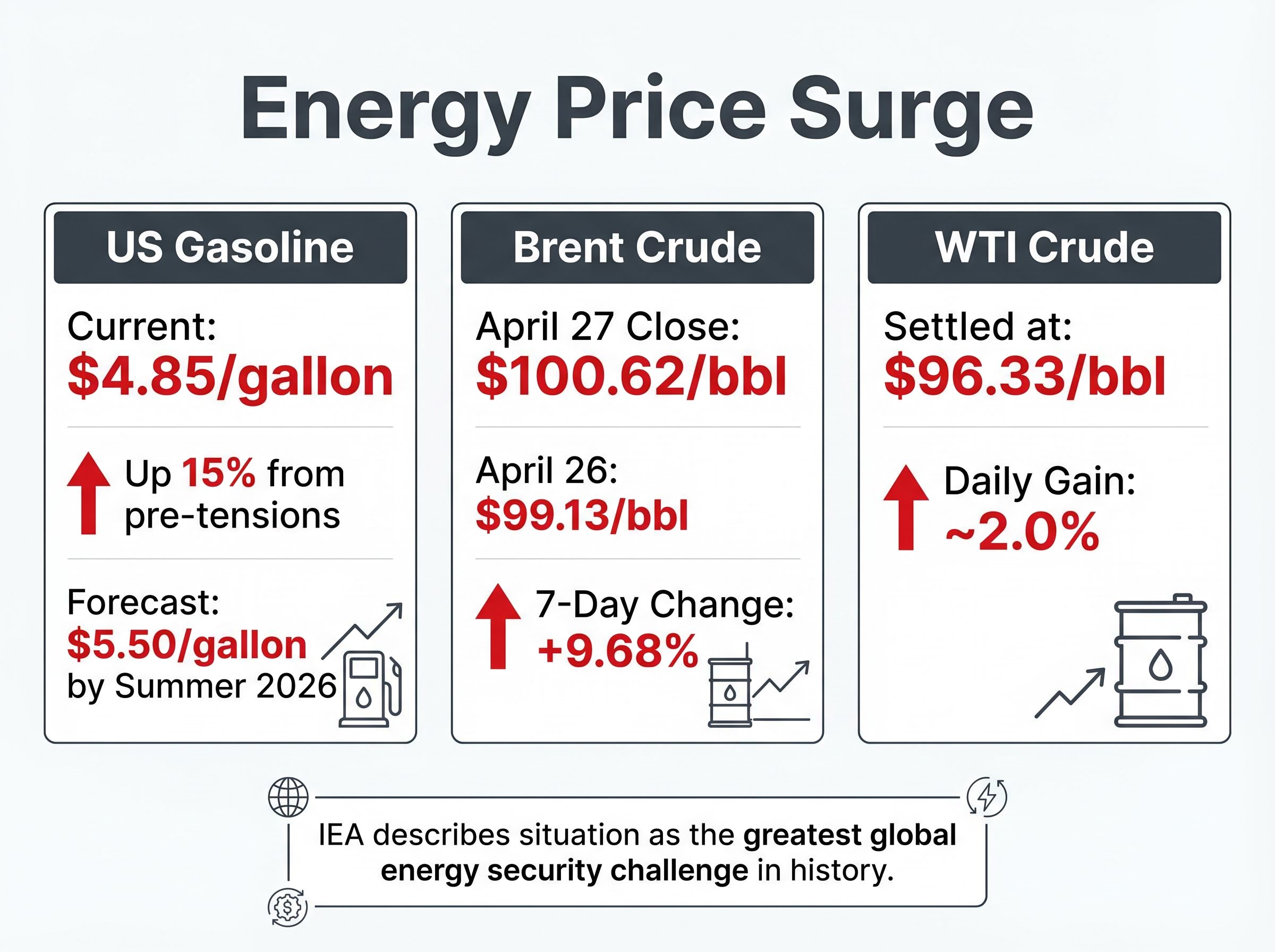

Gasoline hit $4.85 per gallon on Monday as the United States activated a naval blockade of Iranian shipments and nuclear talks in Islamabad collapsed over the weekend, triggering the sharpest geopolitical oil shock since the pandemic. The breakdown of US-Iran negotiations on April 26-27, 2026, has moved the global energy situation from diplomatic uncertainty to active disruption. With the Strait of Hormuz handling roughly 20% of global oil supplies, the stakes extend well beyond crude prices into grocery aisles, pharmacy shelves, and airline fuel tanks.

What follows covers the sequence of events that broke the talks, how oil and equity markets have responded, what Washington’s countermeasures can and cannot achieve, why the Strait of Hormuz translates so directly into consumer price pressure, and which signals investors should watch in the days ahead.

The speed of the escalation is what separates this week from every prior round of US-Iran tension. Four steps took the situation from scheduled diplomacy to active naval enforcement in under 72 hours:

The circular logic of the impasse is the detail that matters most. Iran will not negotiate while the blockade persists. Washington will not lift the blockade without concessions on Iran’s nuclear programme. Neither side has offered a mechanism to break the loop.

Iran’s Foreign Minister Abbas Araghchi did not wait for Washington to reconsider. On April 27, he began a regional diplomatic tour with stops in Russia (meeting President Putin), Pakistan, and Oman. The itinerary signals that Tehran is pursuing parallel diplomatic channels rather than conceding to US preconditions.

Pakistan continues to position itself as mediator, though the probability of a near-term breakthrough remains low given the structural deadlock.

Iran’s reopening proposal and the White House Situation Room response, triggered on April 27 after Tehran submitted a new offer through Pakistani intermediaries, represent the only active de-escalation thread in a situation where four prior diplomatic attempts have already failed.

Brent crude closed at $100.62 per barrel on April 27, up approximately 1.50% on the day. WTI crude settled at $96.33 per barrel, gaining roughly 2.0%. The numbers are significant, but the market’s reaction has been measured rather than panicked, a gap that itself carries information about how traders are pricing this crisis.

| Benchmark | April 26 Price | April 27 Price | 7-Day Change |

|---|---|---|---|

| Brent Crude | $99.13/bbl | $100.62/bbl | +9.68% |

| WTI Crude | — | $96.33/bbl | +~2.0% (daily) |

The consumer impact is already tangible. The US national gasoline average reached $4.85 per gallon as of April 27, up 15% from pre-tensions levels. Analysts forecast prices could reach $5.50 per gallon by summer 2026 if the blockade persists.

The head of the International Energy Agency (IEA) described the Strait of Hormuz situation as “the greatest global energy security challenge in history.”

The US government has layered three responses in rapid succession:

The Department of Energy Strategic Petroleum Reserve capacity and release authority sets the total inventory ceiling at 714 million barrels, which frames the 50-million-barrel draw authorised on April 25 as roughly 7% of maximum holdings, a measure calibrated to signal policy resolve rather than structurally offset a prolonged supply disruption.

Each measure has a specific function. Together, they represent a toolkit rather than a solution.

The 50 million barrels authorised from the SPR sounds substantial in isolation. Against global consumption of approximately 100 million barrels per day, it represents roughly 12 hours of worldwide supply. It is a pressure valve, not a structural fix.

Shale production incentives face a different constraint: time. New drilling activity takes months to translate into additional barrels reaching the market. The gap between policy announcement and physical supply increase is measured in quarters, not weeks.

The Strait of Hormuz is a narrow waterway between Iran and Oman, roughly 21 miles wide at its narrowest point, through which a disproportionate share of the world’s energy supply must pass. Understanding its mechanics explains why a blockade targeting only Iranian ports still sends oil prices above $100.

The EIA data on world oil transit chokepoints identifies the Strait of Hormuz as the single most critical passage in the global energy system, with roughly 20% of all seaborne oil moving through its 21-mile navigable channel, a concentration of supply risk that no pipeline alternative currently comes close to replacing.

Key transit facts:

A chokepoint premium, the additional cost markets add to commodities when strait transit is threatened, is now embedded in every barrel priced off Gulf benchmarks. That premium will not dissipate until the structural risk recedes.

Saudi Arabia’s East-West pipeline and the UAE’s Habshan-Fujairah pipeline offer the only major routes that bypass the strait entirely. Their combined capacity falls well short of the volumes the strait handles daily. These alternatives can soften a disruption for two producers; they cannot replace the strait for the broader region.

Oil is the headline. The downstream effects are the story that takes longer to arrive but touches more households.

Higher energy costs raise input prices across manufacturing, cold-chain storage, and freight logistics. Those increases propagate through supply chains that deliver food, medicine, and consumer goods to shelves in the United States and globally. Sectors carrying exposure include:

Gulf states themselves depend on the strait for food and medicine imports, illustrating that the chokepoint’s vulnerability runs in both directions.

The European Parliament raised concerns about aviation fuel shortages linked to the broader Middle East conflict in the week of April 17-23, 2026, and France pursued diplomatic efforts to facilitate reopening of the strait, signalling that European supply anxiety is genuine.

For US investors, the inflation implications of a Hormuz disruption extend well beyond the energy component of the Consumer Price Index. Consumer staples, healthcare, and industrials all carry exposure that equity positioning rarely accounts for during early-stage geopolitical shocks.

For investors wanting to model the full inflation transmission mechanism from crude prices to the Consumer Price Index, our full explainer on how the Strait of Hormuz closure is driving US inflation traces each channel in detail, including the 90-basis-point CPI jump recorded in a single month, the Federal Reserve’s eliminated rate-cut expectations, and the Shiller CAPE valuation gap that makes equity markets particularly exposed to a sustained supply shock.

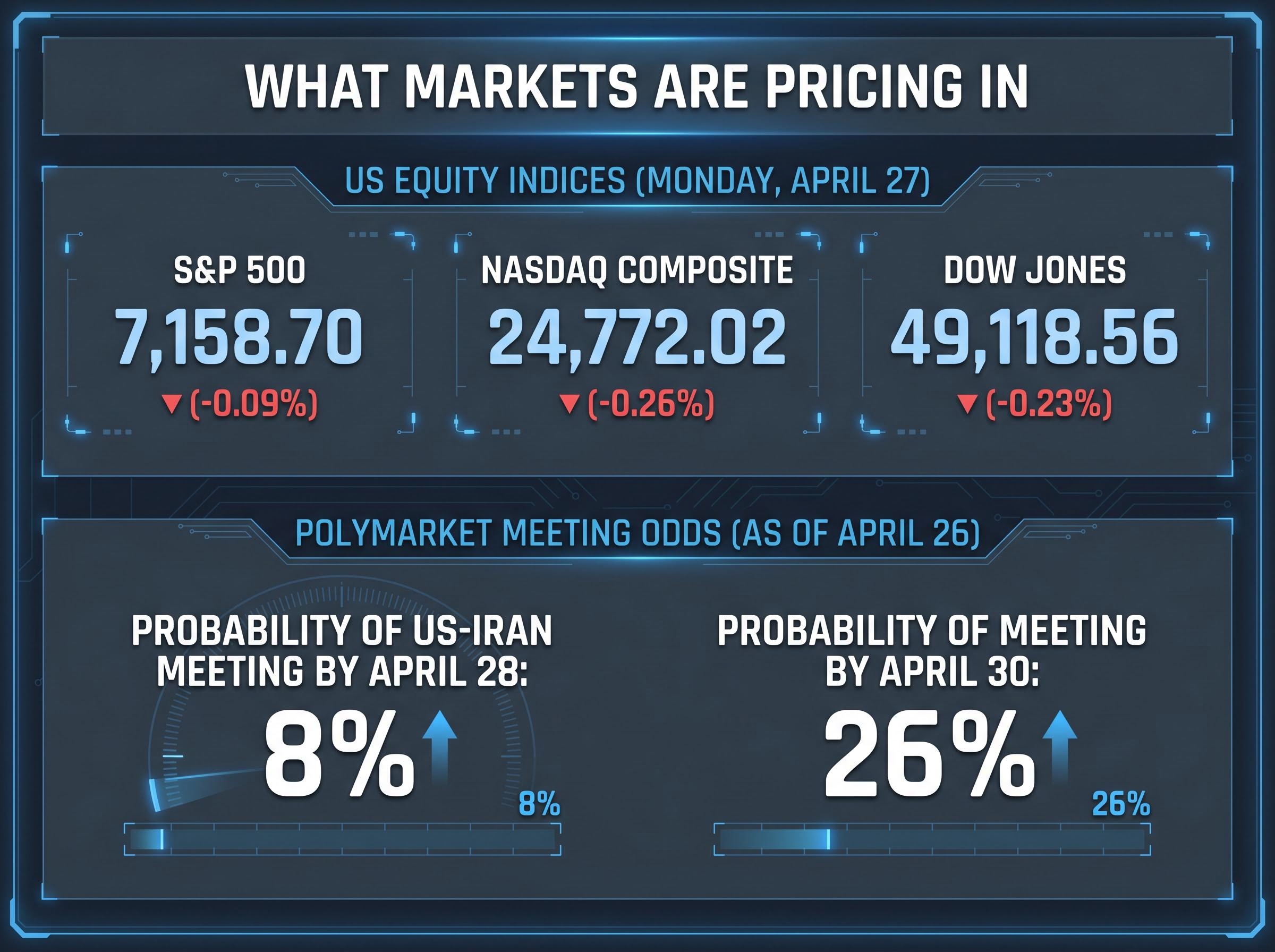

Prediction markets offer one of the clearest reads on whether traders expect a rapid diplomatic resolution. Polymarket odds as of April 26 placed the probability of a US-Iran meeting by April 28 at approximately 8%, rising to only 26% by April 30. Those are not resolution odds. They are odds of the two sides simply being in the same room.

US equity indices reflected caution rather than alarm on Monday. The S&P 500 slipped 0.09% to 7,158.70. The Nasdaq Composite fell 0.26% to 24,772.02. The Dow Jones declined 0.23% to 49,118.56. The modest declines suggest markets are in sustained-disruption pricing mode, not full-escalation mode.

Charu Chanana, chief investment strategist at Saxo Bank, noted that diplomacy had not fully collapsed, meaning markets were not yet pricing the most extreme conflict scenarios.

That gap between current pricing and worst-case scenarios is where investor risk management decisions live this week. Key signals to watch:

The Hormuz disruption is a multi-sector economic event, not only an energy story, and the low odds of near-term diplomatic resolution suggest the pressure is unlikely to lift quickly. For US consumers, the touchpoints are direct: gasoline prices already 15% above pre-tensions levels, with food and pharmaceutical cost increases likely to follow if the blockade persists into the summer months.

The week ahead will test whether markets begin pricing a more severe escalation or find reasons to stabilise. The Fed’s commentary, earnings results, and any movement from Araghchi’s diplomatic tour each carry the potential to shift the trajectory. Until one of those catalysts arrives, oil above $100 and gasoline approaching $5 per gallon represent the new baseline.

For US investors managing active positions this week, our deep-dive into the Fed, earnings, and Hormuz convergence facing US investors examines the simultaneous pressure from the April 28-29 FOMC meeting, Alphabet, Amazon, Meta, and Microsoft earnings, and a supply shock that Goldman Sachs flagged as structurally persistent because Iran retains the physical capacity to close the strait again even after any announced reopening.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.

US-Iran nuclear talks collapsed on April 26-27, 2026, in Islamabad, and the United States activated a naval blockade of Iranian shipments, pushing Brent crude above $100 per barrel and US gasoline to $4.85 per gallon, a 15% rise from pre-tensions levels.

The Strait of Hormuz is a 21-mile wide waterway between Iran and Oman through which approximately 20% of global oil supplies pass; any threat to transit through this chokepoint immediately adds a risk premium to crude prices worldwide.

President Trump authorised a release of 50 million barrels from the Strategic Petroleum Reserve on April 25, 2026, and the Energy Secretary announced new shale production incentives, though analysts note these measures provide short-term relief rather than a structural fix.

Analysts forecast US gasoline prices could reach $5.50 per gallon by summer 2026 if the naval blockade persists, compared to the current national average of $4.85 per gallon recorded on April 27, 2026.

Food distribution, pharmaceuticals, aviation, and consumer goods manufacturing all face meaningful exposure because higher crude and freight costs raise input prices across refrigerated transport, pharmaceutical supply chains, jet fuel, and petrochemical feedstocks.