Record Highs Are Not the Risk Most Investors Think They Are

2 hrs ago

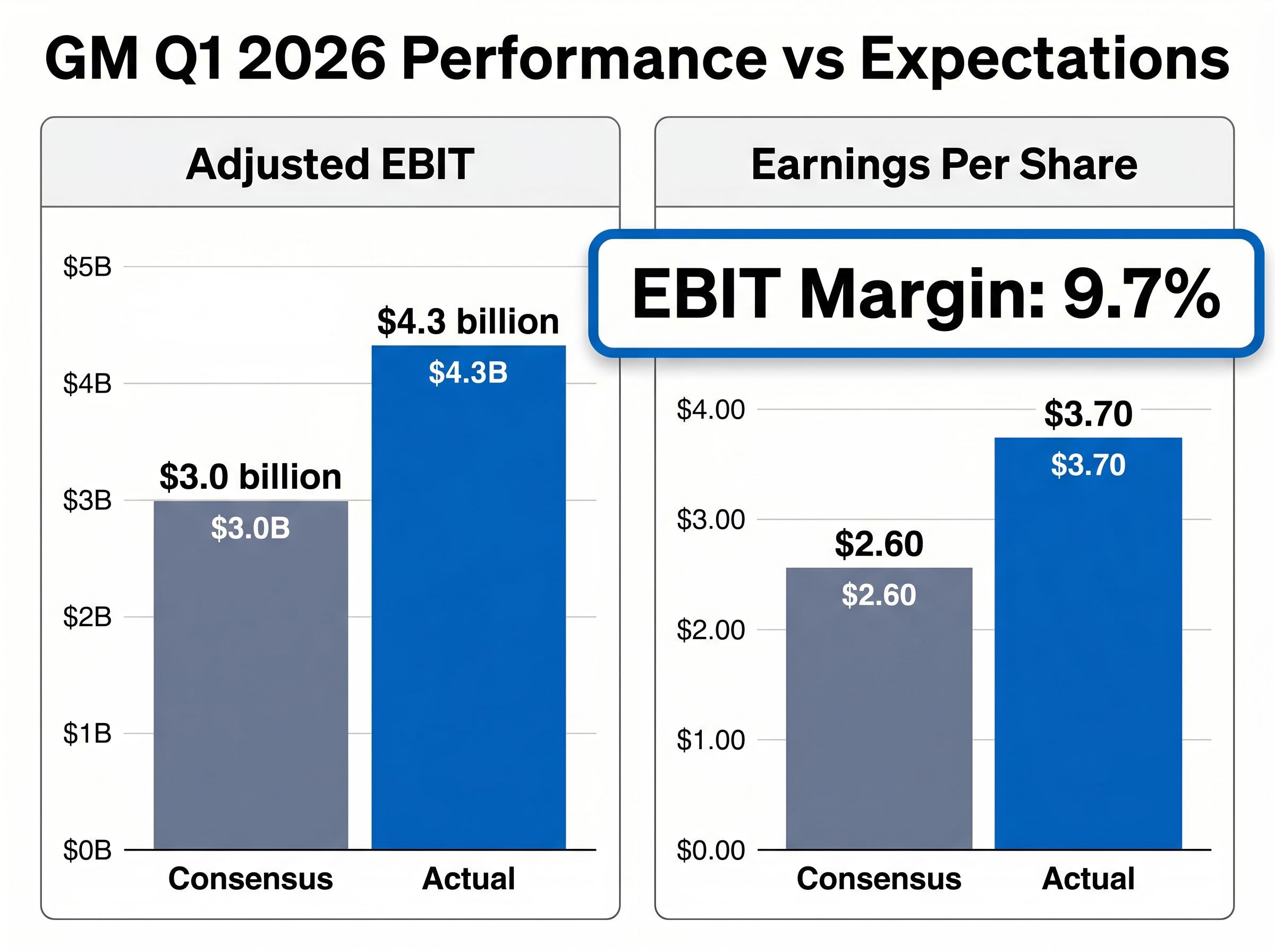

General Motors reported first-quarter 2026 adjusted EBIT of $4.3 billion on 28 April 2026, beating Wall Street’s $3.0 billion consensus by more than $1 billion. Earnings per share came in at $3.70 against expectations of $2.60. The company raised full-year guidance and announced share buybacks during the quarter. GM shares surged on the day, trading around $86, up from a previous close of approximately $77.96 on April 27, 2026, a reaction consistent with the strength of the underlying results. What follows is a breakdown of GM’s Q1 results, what drove the beat, why the stock surged on strong numbers, and what this episode reveals about how earnings actually move share prices.

The gap between what analysts expected and what General Motors delivered was unusually wide. Adjusted EBIT of $4.3 billion exceeded the $3.0 billion consensus by $1.3 billion, while the 9.7% adjusted EBIT margin pointed to operational efficiency rather than simple revenue volume. The earnings-per-share figure of $3.70 was 42% above the $2.60 estimate.

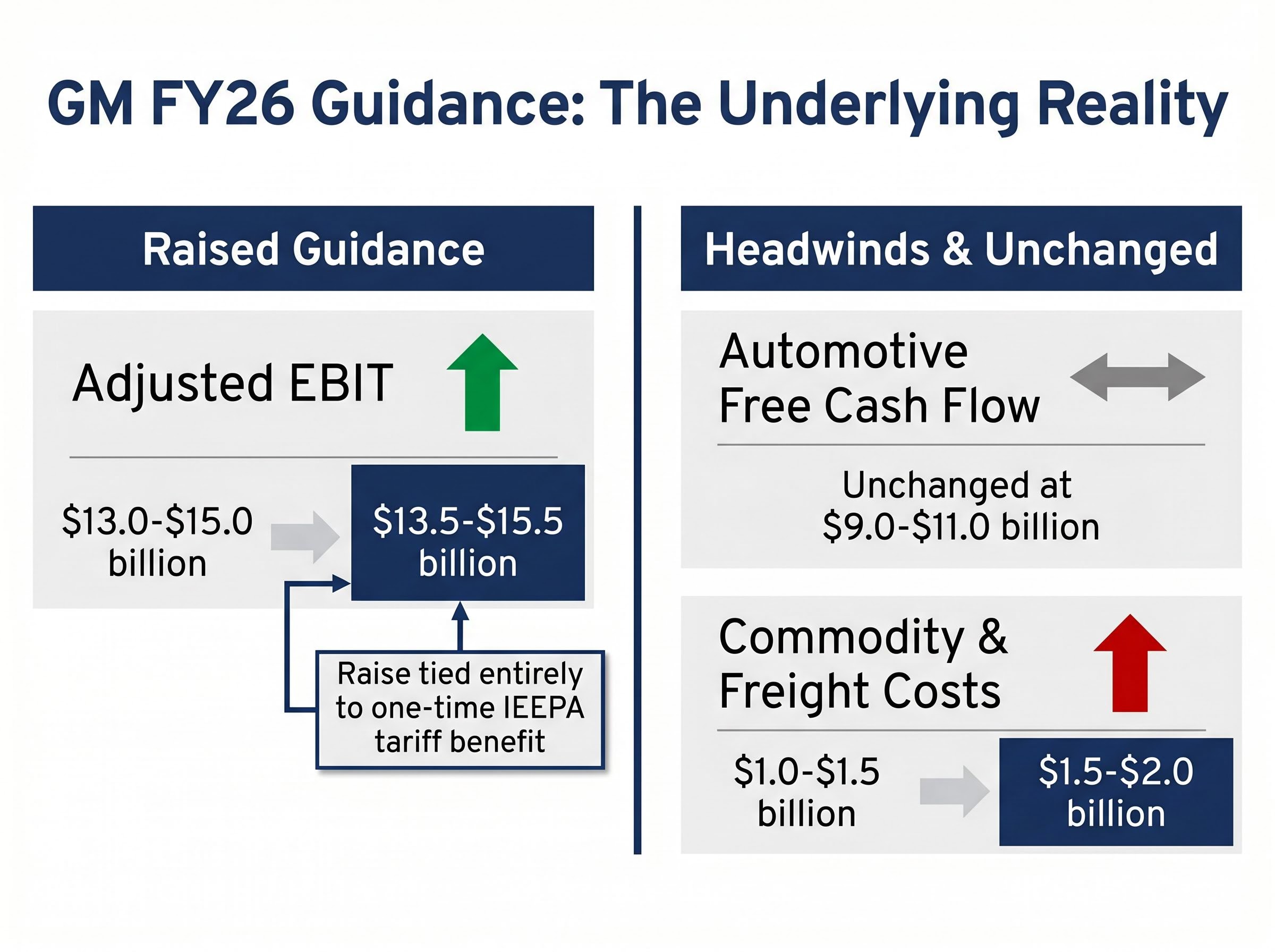

Management raised full-year adjusted EBIT guidance to $13.5-$15.5 billion, up from a prior range of $13.0-$15.0 billion, and confirmed $5.5 billion remaining under the existing share repurchase authorisation.

The key Q1 metrics in context:

| Metric | Q1 2026 Actual | Analyst Consensus |

|---|---|---|

| Adjusted EBIT | $4.3 billion | $3.0 billion |

| EBIT Margin | 9.7% | N/A |

| Earnings Per Share | $3.70 | $2.60 |

By any conventional measure, these were strong results. That scale of outperformance is what makes the share price reaction worth examining closely.

Three factors combined to produce the $1.3 billion EBIT outperformance:

The first two factors represent business performance. The third is where the story turns.

The IEEPA adjustment is a one-time accounting item, not a recurring revenue stream. According to company disclosures, the full-year guidance raise was driven entirely by this tariff benefit rather than underlying operational improvement.

GM’s guidance raise was attributed entirely to the IEEPA tariff benefit, not organic business improvement, per company disclosures.

GM’s own caution was visible in the numbers it chose not to change. Automotive free cash flow guidance remained at $9.0-$11.0 billion, with management citing uncertainty over when IEEPA cash proceeds would actually be received. Meanwhile, commodity and freight cost headwinds were revised higher to $1.5-$2.0 billion for the full year, up from a prior estimate of $1.0-$1.5 billion.

The IEEPA tariff refund process involves a specific CBP portal for claim submissions, meaning the accounting recognition of a benefit and the actual cash receipt can occur in separate reporting periods, which is precisely why GM held its free cash flow guidance flat even as its EBIT guidance moved higher.

A headline beat built partly on a non-recurring item, paired with rising cost pressures and unchanged cash flow guidance, gives the market reason to look beyond the top-line figure.

GM’s share surge on 28 April 2026, a day when the company reported numbers well above expectations, illustrates one of the most instructive dynamics in equity markets. Share prices do not move on results in absolute terms. They move on the gap between what the market expected and what the results change about the future.

The mechanism works in three steps:

Options-implied earnings volatility across the Q1 2026 season ran well above historical norms, with JPMorgan flagging above-average projected swings on individual stocks in the same week GM reported; that elevated implied-move environment meant institutional positioning ahead of results was unusually consequential in determining day-one price action.

Markets price the future, not the present. A strong quarter only moves a stock higher if it materially changes what investors expect to happen next.

Deutsche Bank upgraded GM to Buy with a price target of $90 (up from $83) following the results, a signal that institutional views on forward value can diverge from day-one price action. The upgrade reflected confidence in GM’s operational trajectory even as some profit-taking occurred on the session. Short-term trading reactions and longer-term valuation assessments operate on different timeframes, and a single day’s movement rarely captures the full institutional response.

The professional analyst community weighed the same set of facts and reached varying conclusions, which is itself instructive.

According to coverage of the results, the guidance raise was driven entirely by the IEEPA tariff benefit, not organic improvement, a framing that represents the key tension in institutional coverage of the results.

Deutsche Bank’s upgrade focused on GM’s operational execution and forward positioning. Commentary focused on whether the headline numbers overstate the underlying earnings trajectory. Both assessments used the same Q1 data. The divergence illustrates how analytical frameworks shape conclusions, and why reading multiple institutional perspectives provides a more complete picture than relying on any single rating.

The pattern of forward guidance driving post-earnings moves more than headline EPS figures was a consistent theme across Q1 2026 reporting, with Magnificent Seven names facing particular scrutiny over AI investment return timelines rather than backward-looking profitability metrics, a dynamic that parallels the quality-of-earnings questions raised by GM’s tariff-adjusted guidance raise.

The revised FY26 guidance lays out management’s expectations for the remainder of the year:

| Guidance Metric | Prior Range | Updated Range |

|---|---|---|

| Adjusted EBIT | $13.0-$15.0 billion | $13.5-$15.5 billion |

| EPS | N/A | $11-$13 |

| Net Income | N/A | $10.3-$11.7 billion |

| Automotive Free Cash Flow | $9.0-$11.0 billion | $9.0-$11.0 billion (unchanged) |

The $500 million EBIT guidance raise maps directly to the IEEPA tariff benefit. Strip that out, and the underlying guidance is unchanged.

Across the Q1 2026 season, the principle that guidance quality over headline results drives durable price moves showed up repeatedly; Intel’s more-than-20% after-hours surge on confident Q2 revenue guidance, reported the same week as GM’s results, illustrated how forward-looking statements can override a mixed backward-looking print in determining investor conviction.

Several headwinds GM flagged for the remainder of FY26 warrant attention:

Management’s decision to hold free cash flow guidance steady, even while raising EBIT guidance, signals caution about whether the tariff benefit translates into actual cash in the near term.

The variables that will determine whether Q1’s operational strength is sustained or proves to be a one-quarter tailwind include:

The broader auto sector context adds a layer. Ford (F) was trading at approximately $12.49 on 28 April, while Stellantis (STLA) traded at approximately $7.99, down on the day. The S&P 500 was up approximately 0.80%, suggesting GM’s surge was company-specific rather than a reflection of broad market weakness.

GM’s Q1 results offer a worked example of a principle that applies to every earnings season: a strong report only moves a stock higher if it changes forward expectations materially and durably.

Three filters help investors evaluate any earnings beat:

NBER research on earnings quality and stock returns finds that accrual-heavy earnings, where reported income diverges from cash generation, consistently predict weaker forward stock performance, a pattern that frames the relevance of GM’s unchanged free cash flow guidance alongside its raised EBIT figure.

A strong quarter tells investors where a company has been. The share price reflects where the market believes it is going.

Applied together, these three questions explain the nuances in GM’s share price reaction despite a $1.3 billion EBIT beat. The magnitude of the results was clear. The durability of the earnings quality was not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

General Motors reported Q1 2026 adjusted EBIT of $4.3 billion, beating the $3.0 billion analyst consensus by $1.3 billion, with earnings per share of $3.70 against expectations of $2.60.

GM shares surged to around $86 on April 28, 2026, from a prior close of approximately $77.96, because the company's results significantly exceeded analyst expectations on every key metric, and management raised full-year guidance.

The IEEPA (International Emergency Economic Powers Act) tariff adjustment was a one-time accounting benefit that flowed through in Q1 2026; according to company disclosures, GM's full-year guidance raise was driven entirely by this non-recurring item rather than organic business improvement.

Yes, GM raised its full-year adjusted EBIT guidance to $13.5-$15.5 billion from $13.0-$15.0 billion, but automotive free cash flow guidance remained unchanged at $9.0-$11.0 billion, reflecting uncertainty over when the IEEPA tariff cash proceeds would actually be received.

Investors should ask three questions: whether the beat was operational or one-time, whether it materially changes the forward earnings trajectory, and whether the positive outcome was already priced into the stock before results arrived.