Analysing current US housing market trends requires looking past headline earnings to understand the structural divergence beneath the surface. Fannie Mae’s first-quarter 2026 financial report presents an apparent contradiction for market observers. The institution missed analyst expectations on the top line, yet underlying operational efficiency drove continued capital accumulation.

According to preliminary reports, total revenue for the quarter reached $7.28 billion, falling short of the projected $7.39 billion. According to preliminary reports, adjusted earnings per share landed at $0.01, significantly missing the $0.63 consensus estimate.

According to preliminary reports, despite these headline misses, overall net profitability climbed to $3.7 billion. This profit growth stems largely from aggressive operational restructuring. According to preliminary reports, corporate overhead spending dropped by 19 percent sequentially, falling to $745 million. This cost discipline helped push the enterprise’s cumulative net worth to $112.7 billion.

CEO Commentary “Our strong profitability this quarter reflects solid balance sheet fundamentals and a disciplined approach to managing risk across our portfolios,” noted Acting CEO Peter Akwaboah.

Headline figures rarely capture the complete operational reality of institutional real estate finance. By unpacking the revenue miss against the actual profit growth, the underlying efficiency of the organisation becomes clear.

The most material revelation in the financial data is the stark performance split between the single-family and multifamily business segments. These two divisions are reacting entirely differently to the current macroeconomic environment.

| Performance Metric | Q4 2025 (Estimated) | Q1 2026 (Actual) |

|---|---|---|

| Corporate Overhead | $920 million | $745 million |

| Single-Family Net Earnings | Data Pending | $3.2 billion |

| Overall Net Profitability | Data Pending | $3.7 billion |

Why Residential and Commercial Property Markets Are Decoupling

The divergence in Fannie Mae’s financial results reflects a fundamental decoupling between consumer-focused and institutional property sectors. Single-family conventional purchases and multifamily asset acquisitions operate on entirely different financial mechanics. Understanding these structural differences clarifies why one interest rate environment can stimulate household buyers while straining commercial operators.

Single-family residential mortgages primarily serve individual homeowners seeking long-term housing stability. These consumers rely heavily on 30-year fixed-rate products. Once secured, this fixed structure insulates the homeowner from ongoing market volatility and rising borrowing costs.

Multifamily commercial financing operates on an entirely different premise. Institutional landlords and developers acquire these assets to generate yield, typically relying on shorter-term financing structures. This makes commercial operators highly sensitive to interest rate fluctuations throughout the lifecycle of their investment.

The Mechanics of Maturity Walls

This interest rate sensitivity peaks when commercial properties encounter maturity walls. A maturity wall refers to the scheduled date when a large volume of short-term commercial loans becomes due and requires immediate refinancing.

When these deadlines arrive in a higher-rate environment, property owners are forced to refinance their debt at current, potentially unfavourable terms. This timing mechanism puts severe pressure on asset valuations and operating margins, regardless of how well the property is performing in terms of tenant occupancy or rental income.

The Mortgage Bankers Association debt projections indicate that $875 billion in commercial loans will mature throughout 2026, creating a massive refinancing bottleneck for institutional operators right as borrowing costs peak.

When big ASX news breaks, our subscribers know first

The Consumer Response to Stabilising Mortgage Rates

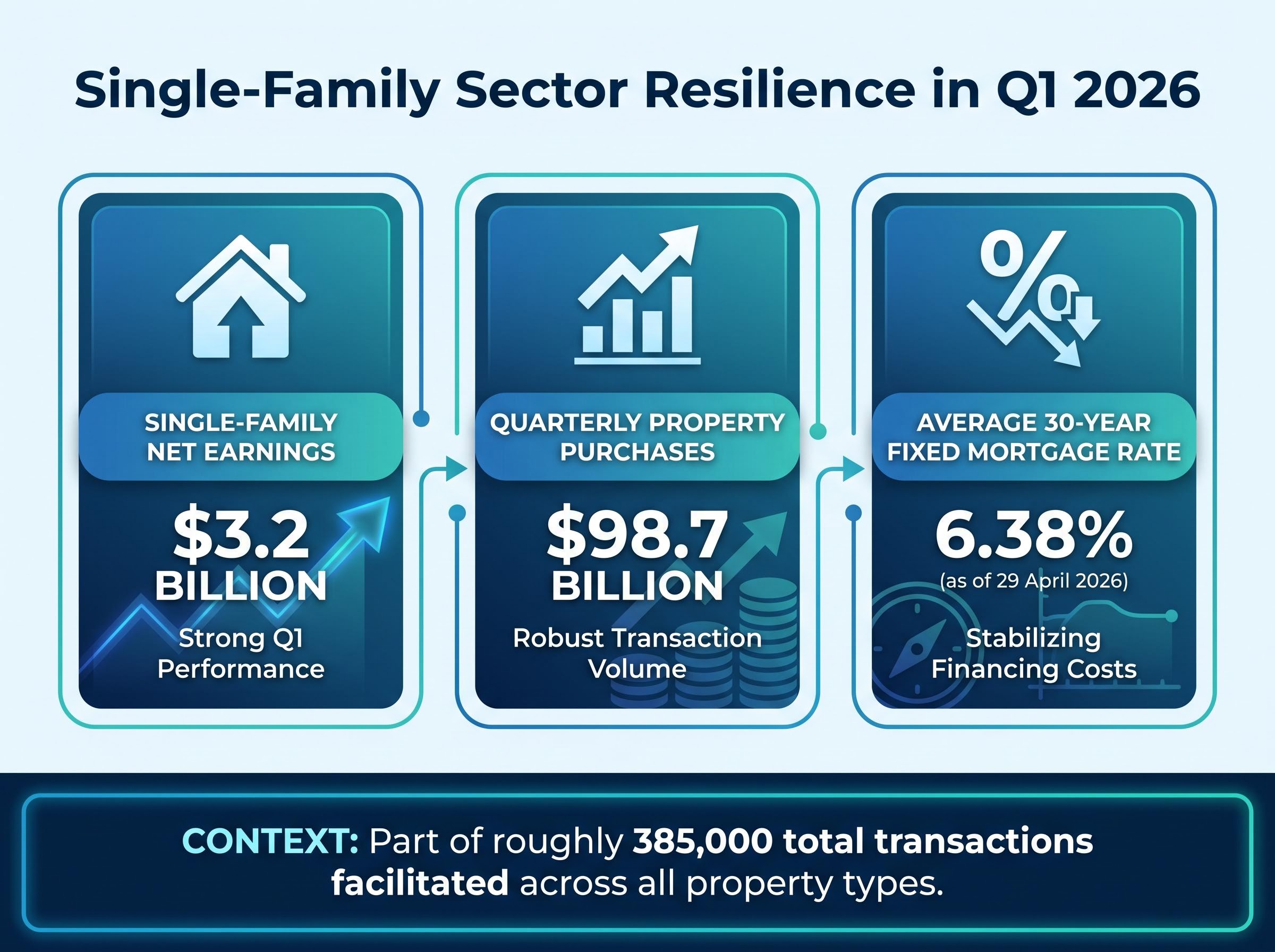

Consumer households are successfully navigating the current rate environment through strategic financial moves. The single-family division reported net earnings of $3.2 billion, driven heavily by renewed borrower activity. Single-family property purchases grew to $98.7 billion during the quarter.

A significant portion of this growth stems from an expected expansion in refinancing transactions, with specific data pending release. Homeowners are actively managing their debt obligations as the macroeconomic picture shifts, finding strategic relief through loan modifications.

Several specific macroeconomic drivers are stimulating this single-family refinancing surge:

The average US 30-year fixed mortgage rate stabilised at 6.38 percent as of 29 April 2026. Cooling inflation data has provided consumers with increased confidence regarding future purchasing power. * Recent Federal Reserve signals indicate a shift toward potential rate cuts, encouraging borrowers to lock in lower payments.

This refinancing activity translates directly into consumer resilience. Data on single-family severe payment delinquency metrics is pending release. The ability to secure more favourable financing terms allows homeowners to maintain their mortgage obligations despite broader economic pressures.

For investors wanting to explore the vulnerabilities underlying this apparent household stability, our deep-dive into US consumer recession risk examines how rapid savings depletion and historic lows in sentiment complicate the broader consumption narrative.

Cracks in the Foundation of Multifamily Investments

While consumer households display strong resilience, the commercial sector faces mounting systemic risk. The latest metrics reveal compounding pressures on multifamily properties across the market, signalling potential vulnerabilities for institutional capital.

Multifamily acquisitions fell sharply, with specific data pending release. This contraction in acquisition volume demonstrates widespread caution among institutional investors. Simultaneously, data on severe payment delinquencies in the sector is pending release.

The finalized SEC corporate financial disclosures quantify this contraction in multifamily acquisitions, providing the precise figures that were initially delayed during preliminary reporting.

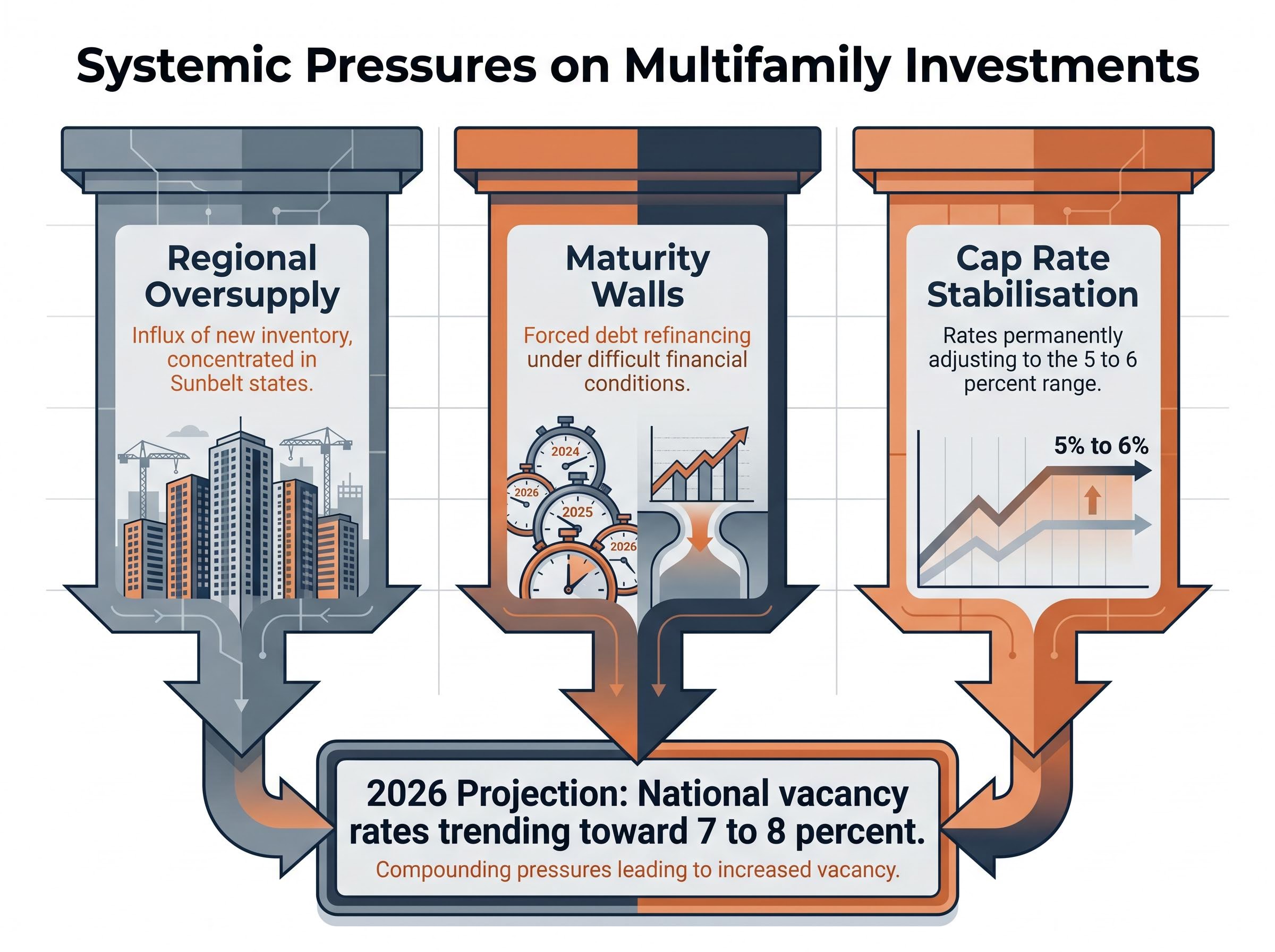

This growing market stress stems from three primary drivers:

- A significant influx of new multifamily inventory has created regional oversupply, particularly across the Sunbelt states where developers previously accelerated construction.

- Approaching maturity walls are forcing property owners to refinance debt under increasingly difficult financial conditions, squeezing operational margins.

- Capitalisation rates are stabilising in the 5 to 6 percent range, forcing developers and investors to permanently adjust their return expectations.

These headwinds are materially impacting asset performance. Industry projections indicate that national vacancy rates will continue trending toward 7 to 8 percent throughout 2026.

Understanding these specific stress points helps identify which real estate investment trusts or development sectors might face prolonged operational difficulties. While single-family homes enjoy price support from constrained supply, multifamily assets must contend with an oversupplied market precisely when borrowing costs are biting hardest.

Reading the Leading Indicators for Real Estate Through 2026

The divergence between single-family strength and multifamily weakness serves as an important leading indicator for the broader economy. According to preliminary reports, the facilitation of roughly 385,000 transactions across all property types in the quarter demonstrates that the housing ecosystem remains highly active, albeit highly segmented.

The localised stress in commercial residential properties does not indicate a systemic collapse of the wider real estate sector. Instead, it highlights a structural transition where institutional capital must recalibrate its pricing models while consumer capital benefits from stabilising rates. The single-family market’s resilience acts as a buffer against commercial vulnerability.

Institutional investors are currently maintaining a wait-and-see approach as they digest the new April 2026 metrics. Post-release analysis from major financial institutions will likely formalise this sector divergence into updated asset allocation strategies. Investors watching these leading indicators can anticipate broader economic shifts and potential monetary policy impacts as the year progresses.

These sector-specific real estate metrics must be weighed against broader US recession probabilities, particularly as external energy shocks threaten to disrupt the timeline for monetary policy normalization.

The True State of American Housing Resilience

The current market is experiencing a tale of two sectors rather than a uniform directional trend. Consumer stability provides a strong, reliable foundation for the broader financial system, effectively balancing the growing headwinds in the commercial property space.

This household stability remains a critical buffer against historical stock market downturns, which are frequently triggered when elevated energy costs deplete consumer discretionary spending power.

Moving forward, the most material dynamic to monitor is the race between future Federal Reserve rate cuts and impending commercial maturity walls. If monetary policy easing arrives before the largest tranches of multifamily debt require refinancing, the commercial stress may remain contained. Conversely, delayed rate cuts could amplify the delinquency trends already visible in institutional portfolios.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.