Warsh Strips Fed Statement to 130 Words, Drops All Guidance

1 hr ago

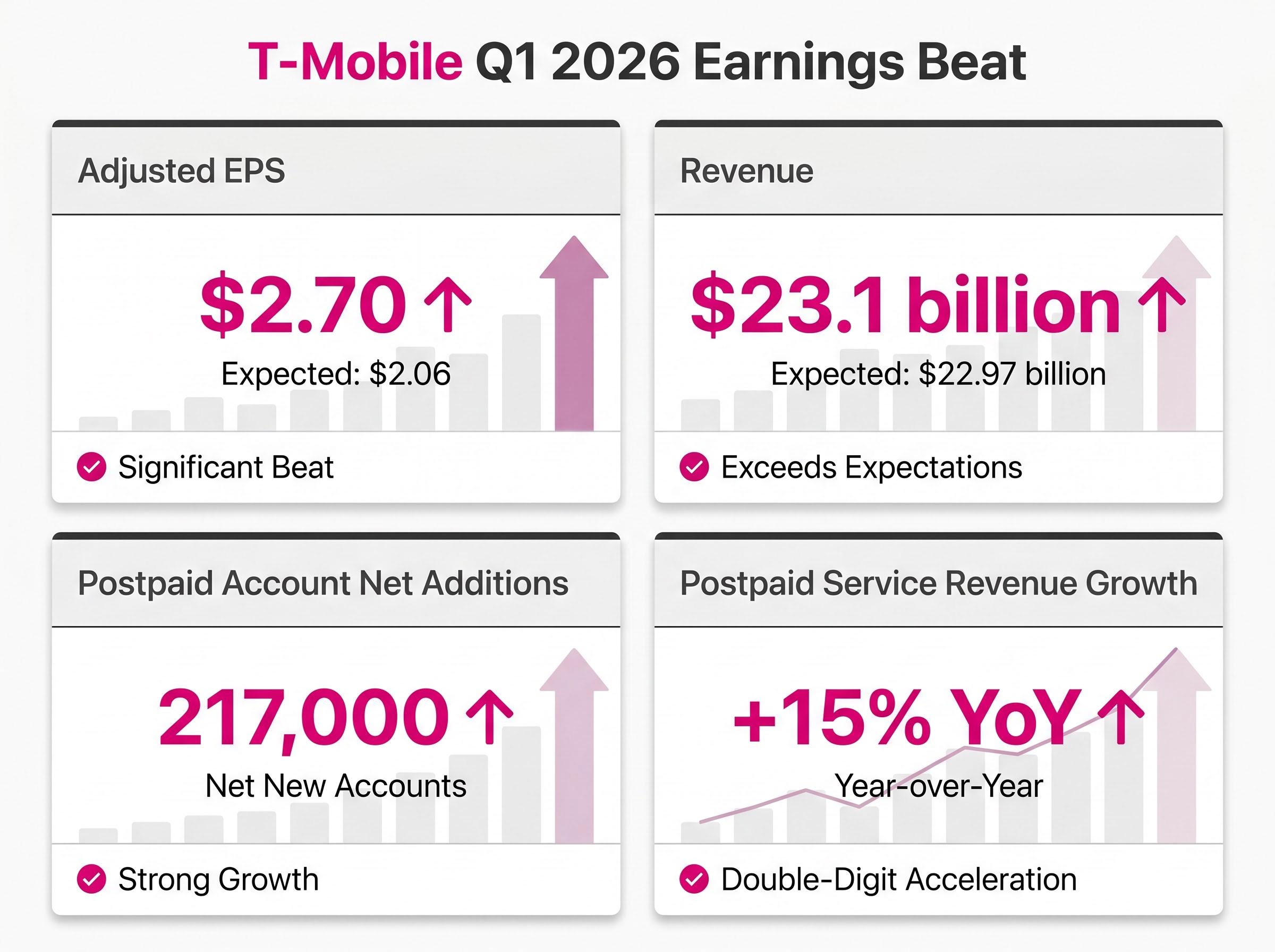

T-Mobile delivered a quarter that beat on every major metric, and Wall Street’s response split cleanly in two. On 29 April 2026, JPMorgan cut its price target from $300 to $275 while Oppenheimer upgraded the stock to Outperform with a $260 target. Both firms remain bullish. Both cite the same earnings report. Yet their reasoning reflects fundamentally different frameworks for valuing TMUS at this stage of its growth cycle.

What follows is a breakdown of both analyst positions, the valuation mechanics behind JPMorgan’s reset, the specific AI initiatives underpinning Oppenheimer’s thesis, and the competitive data that contextualises both calls. The goal is not to declare a winner, but to isolate the single variable that separates the two frameworks so investors can determine which one better matches their own investment horizon.

The Q1 2026 numbers left little room for debate about operational execution. T-Mobile beat consensus across every headline metric:

A record proportion of new subscribers cited network quality as their primary reason for switching, a qualitative signal that T-Mobile’s 5G coverage advantage is translating directly into competitive wins.

TMUS closed at $186.72, up 2.17% on the day. The market liked the quarter. The question is what comes next, and that is where analysts diverge.

The T-Mobile Q1 2026 earnings release confirmed postpaid account net additions of 217,000, a core adjusted EBITDA beat of approximately 2% against consensus, and raised full-year postpaid account addition guidance to 950,000-1,050,000, providing the definitive source data underpinning both the JPMorgan and Oppenheimer valuation frameworks.

Management raised full-year 2026 postpaid account addition guidance to 950,000-1,050,000, a confidence signal that extends the Q1 momentum into forward expectations. JPMorgan’s own 2026 estimate of 1.035 million postpaid account additions sits near the top of that range, suggesting the bank sees management’s revised target as achievable rather than aspirational.

When Oppenheimer upgraded TMUS from Perform to Outperform on 29 April 2026, it was not a routine target adjustment. It was a directional conviction shift anchored in a specific thesis: that artificial intelligence will give T-Mobile the ability to raise prices without losing subscribers, while simultaneously reducing the cost base.

That thesis rests on programmes already in motion, not speculative roadmaps:

The pricing power angle centres on AI-driven personalisation. If T-Mobile can tailor offers, retention incentives, and service bundles at individual account level, average revenue per user (ARPU) could expand without triggering the churn that typically accompanies price increases.

The cost efficiency angle works differently. AI in network operations and customer service reduces headcount-related expenditure and improves resolution rates, feeding directly into free cash flow (FCF) growth. Oppenheimer’s $260 target reflects a view that both vectors can compound simultaneously, creating an earnings trajectory that FCF-only models may understate.

AI integration in telecom operations is translating into measurable profitability improvements across carriers of different sizes and geographies, with platforms that automate customer onboarding and reduce manual integration steps showing the fastest improvement in unit economics.

JPMorgan’s move from $300 to $275 reads as bearish at first glance. It is not. The cut is the arithmetic output of a disciplined valuation framework, not a change in conviction.

The target derives from three steps:

T-Mobile remains on JPMorgan’s U.S. Equity Analyst Focus List, a designation reserved for high-conviction names. The target cut is a mechanical recalibration; the Overweight rating is the sentiment signal.

The distinction matters for retail investors, who frequently conflate a price target reduction with a downgrade. A target reduction says the maths changed. A rating downgrade says the thesis changed. JPMorgan changed the maths.

| Metric | JPMorgan 2026 Estimate | T-Mobile 2026 Guidance |

|---|---|---|

| Core Adjusted EBITDA | $37.42 billion | $37.1-$37.5 billion |

| Free Cash Flow | $18.43 billion | $18.1-$18.7 billion |

JPMorgan projects FCF per share growing at a compound annual growth rate (CAGR) of approximately 12% through 2028, with EBITDA compounding at approximately 8% over the same period.

Free cash flow measures the actual cash a business generates after covering all capital expenditure. For capital-intensive telecoms like T-Mobile, FCF is the preferred valuation lens because heavy depreciation charges on network infrastructure distort reported earnings, making price-to-earnings (P/E) ratios less reliable.

A comparison across three criteria clarifies why:

Fidelity’s telecom sector valuation analysis establishes that earnings growth is not the most reliable gauge for capital-intensive carriers, precisely because heavy depreciation on network infrastructure creates a persistent and wide gap between reported profit and actual cash generation, which is the same structural argument behind JPMorgan’s preference for a FCF multiple over a P/E-based target.

JPMorgan’s 14.2x FCF multiple implies a moderate growth premium over the broader telecom sector. As a secondary check, T-Mobile currently trades at approximately 7.0x 2027 EV/EBITDA (enterprise value divided by earnings before interest, taxes, depreciation and amortisation) and 9.6x 2027 FCF per share.

T-Mobile’s projected FCF per share CAGR of approximately 12% through 2028 is the single most investor-relevant forward metric in JPMorgan’s coverage, as it underpins both the target derivation and the Overweight conviction.

The stock has declined approximately 8% year to date against an S&P 500 gain of approximately 4.7%, with a $2.7 billion cost reduction target by 2027 providing additional support for the FCF trajectory.

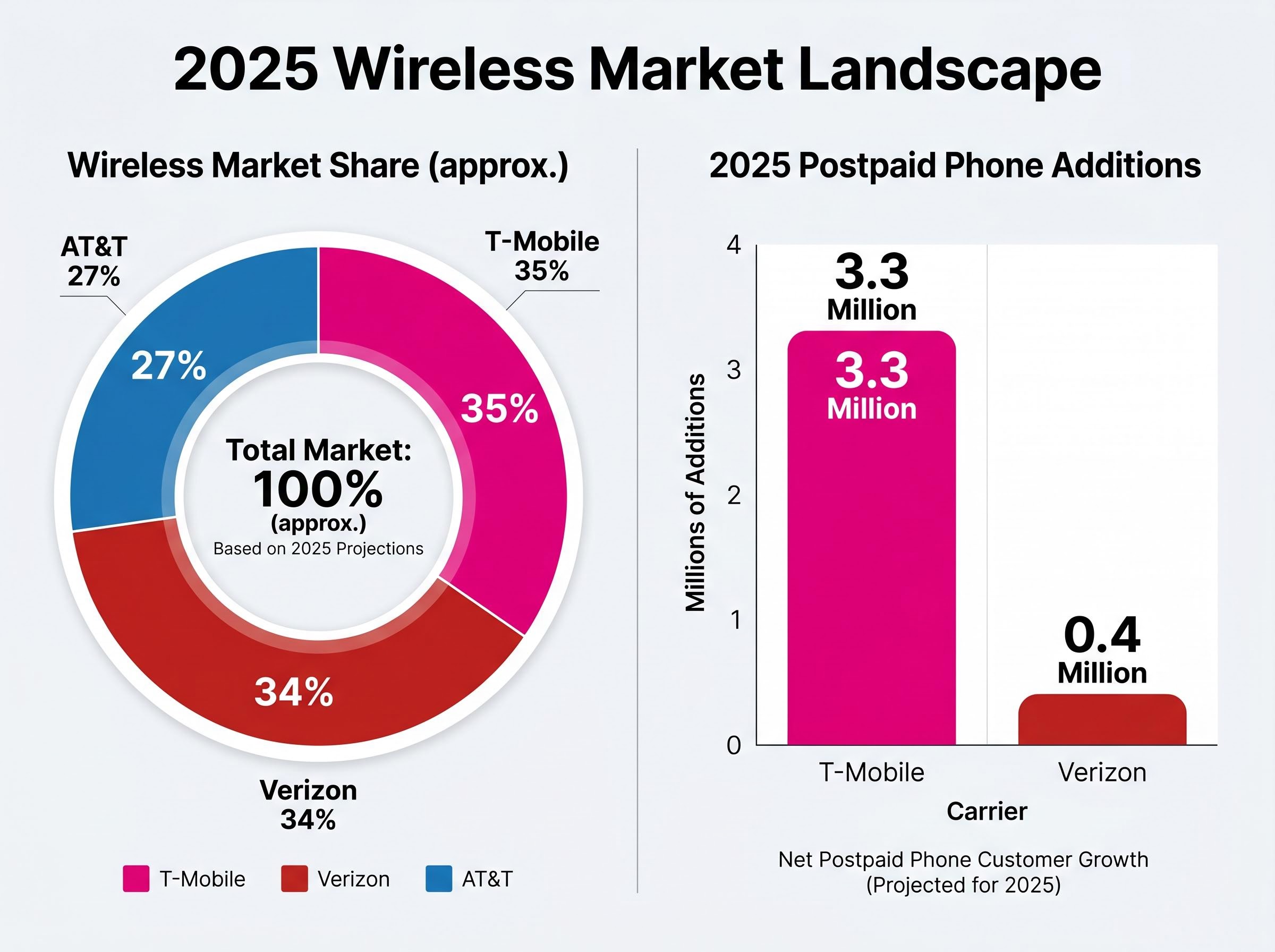

In 2025, T-Mobile added 3.3 million postpaid phone customers. Verizon added 0.4 million. That single datapoint captures the competitive gap more precisely than any analyst commentary.

| Carrier | Wireless Market Share (approx.) | 2025 Postpaid Phone Additions |

|---|---|---|

| T-Mobile | ~35% | 3.3 million |

| Verizon | ~34% | 0.4 million |

| AT&T | ~27% | N/A |

T-Mobile’s Q1 2026 postpaid performance extends this trajectory, with the company now effectively level with Verizon at approximately 35% wireless market share. Multiple analyst firms cite this competitive positioning as a direct input to their valuation:

Broadband infrastructure expansion has become a recurring strategic priority for telecoms seeking to diversify revenue beyond mobile, with carriers deploying fibre networks as a hedge against ARPU compression in the core wireless business while simultaneously opening new household penetration vectors.

Subscriber growth momentum is the primary input into long-term FCF projections. If T-Mobile continues to outgrow Verizon at the current rate, both the JPMorgan and Oppenheimer targets may prove conservative.

The instinct when two major firms issue conflicting moves on the same day is to pick a side. The more useful approach is to identify what separates them.

| Dimension | JPMorgan | Oppenheimer |

|---|---|---|

| Rating | Overweight | Outperform |

| Price Target | $275 | $260 |

| Primary Thesis | FCF compounding at ~12% CAGR | AI-driven pricing power and cost efficiency |

| Valuation Method | 14.2x 2027 FCF multiple | Growth re-rating via AI optionality |

| Key Risk | Multiple compression if growth slows | AI initiatives fail to materialise at scale |

Both targets sit below the $260.91 consensus average across 29 analysts (2 Strong Buy, 19 Buy, 8 Hold), with the full range spanning $225 to $310.

From the $186.72 close on 29 April 2026, the consensus average implies approximately 39.8% upside, a gap wide enough to attract attention even from investors sceptical of individual price targets.

Barclays (Hold/$245) and Jefferies (Hold/$235) represent the valuation-concern counterweight, and the stock’s approximately 8% year-to-date decline sharpens the entry point question.

The single variable that separates the two frameworks is whether AI-driven revenue and cost benefits will materialise at sufficient scale to justify multiples above the FCF-anchored target. Investors whose thesis centres on FCF compounding will find JPMorgan’s framework the appropriate reference. Those who believe AI creates a re-rating opportunity have Oppenheimer’s framework to anchor against.

JPMorgan and Oppenheimer disagree on methodology and catalysts but converge on the same conclusion: TMUS warrants a bullish rating. That convergence aligns with the broader 29-analyst Moderate Buy consensus.

The Q1 2026 beat, the raised guidance, the subscriber growth dominance over Verizon and AT&T, and the AI optionality collectively create a multi-thesis investment case. Each investor can anchor to the variable most aligned with their own framework.

The next material test arrives with Q2 2026 reporting, where T-Mobile’s IntentCX platform and operational AI programmes will either show up in ARPU trends and cost reduction milestones, or they will not. That is the quarter where the JPMorgan and Oppenheimer frameworks begin to resolve.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

JPMorgan reduced its price target from $300 to $275 as a mechanical recalibration of its valuation model, applying a 14.2x multiple to updated 2027 free cash flow estimates. The Overweight rating was maintained, meaning the investment thesis did not change, only the arithmetic inputs.

A free cash flow multiple values a company relative to the cash it generates after capital expenditure, rather than reported accounting profit. Telecoms like T-Mobile are valued this way because heavy depreciation on network infrastructure creates a wide gap between reported earnings and actual cash generation, making price-to-earnings ratios less reliable.

Oppenheimer points to four programmes already in motion: the IntentCX platform developed with OpenAI for personalised customer experience, AI-powered real-time call translation integrated into 5G networks in February 2026, a 6G Innovation Hub with Deutsche Telekom, and generative AI deployed across back-office operations via Amdocs.

In 2025, T-Mobile added 3.3 million postpaid phone customers compared to Verizon's 0.4 million, and the company now holds approximately 35% wireless market share, effectively equal to Verizon and well ahead of AT&T's roughly 27%.

Across 29 analysts, TMUS carries a Moderate Buy consensus with a price target average of $260.91, which implies approximately 39.8% upside from the $186.72 close on 29 April 2026, with individual targets ranging from $225 to $310.