Fed Holds at 3.75% as Warsh’s First Press Conference Begins

2 hrs ago

The Dow Jones Industrial Average closed at a record 51,999.67 on Tuesday, 16 June 2026, the same afternoon the Nasdaq Composite fell more than 1%. That divergence, the sharpest single-session split between the two indices in weeks, captured a market caught between Monday’s 3.1% Nasdaq surge and the Federal Reserve’s two-day meeting beginning that same day. What follows is a breakdown of which sectors won and lost, which semiconductor names led the decline, and what moved after hours, including SpaceX’s $60 billion acquisition of Anysphere and Lionsgate Studios’ reversal on Netflix deal news.

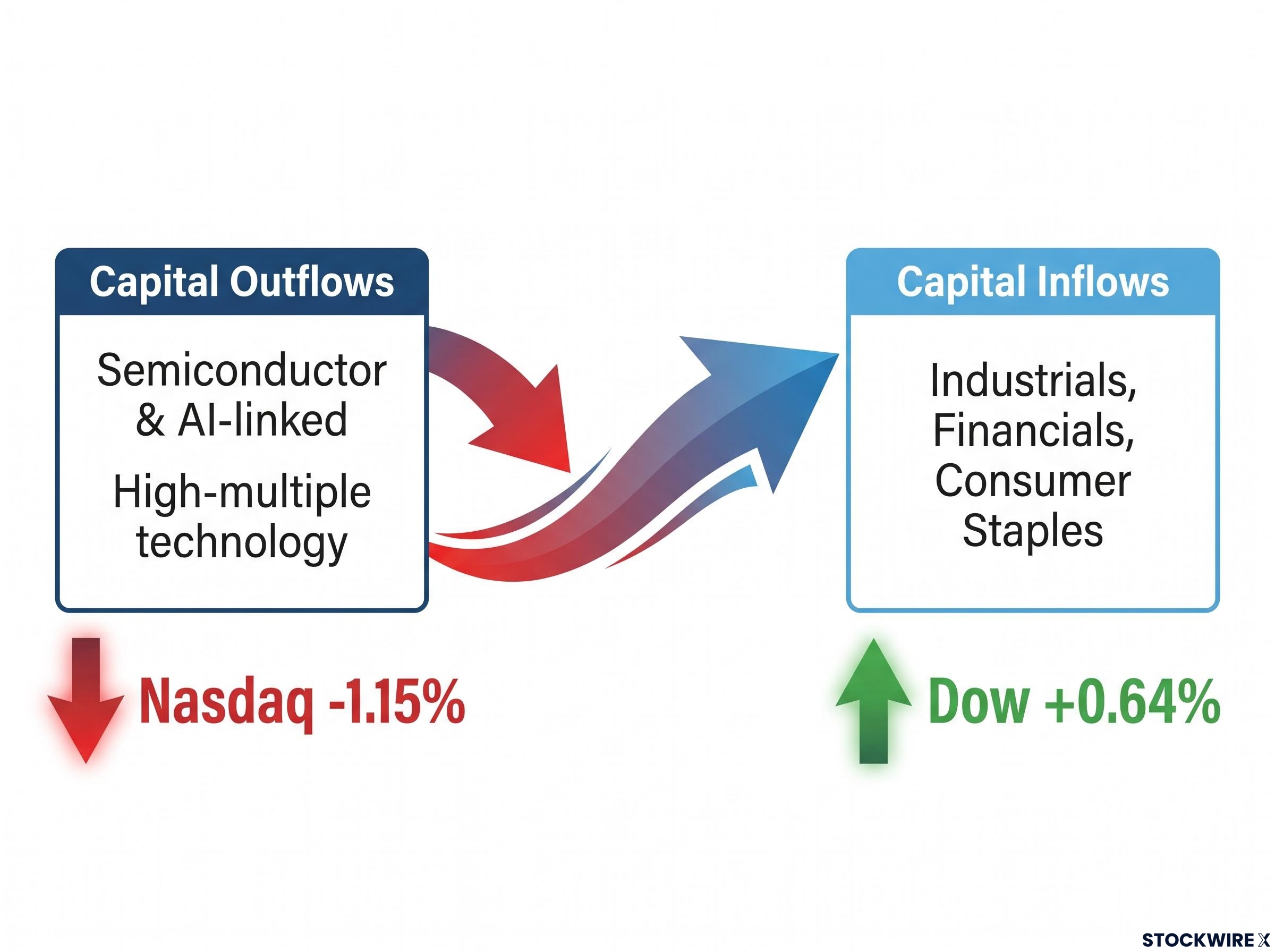

The Dow’s 328.64-point gain to 51,999.67 was not a broad market endorsement. It was a destination marker: capital leaving one part of the market and arriving in another.

The S&P 500 fell 0.57% to 7,511.35. The Nasdaq Composite dropped 1.15% to 26,376.34. Three indices told three different stories on the same afternoon.

The Dow’s outperformance traced directly to its composition. Industrials, financials, and consumer-facing names absorbed rotational inflows as investors trimmed exposure to the high-multiple technology stocks that dominate both the Nasdaq and the upper reaches of the S&P 500. The record close was a rotation signal, not a rally.

The S&P 500’s 0.57% decline while the Dow rose reflects a dynamic rooted in megacap tech concentration: four names commanding more than 19% of the index create a structural drag on the headline number whenever those names sell off, even when the broader market, measured by the Dow’s composition, is doing well.

| Index | Closing Level | Change |

|---|---|---|

| Dow Jones Industrial Average | 51,999.67 | +328.64 pts (+0.64%) |

| S&P 500 | 7,511.35 | -0.57% |

| Nasdaq Composite | 26,376.34 | -1.15% |

Monday’s context explains Tuesday’s mechanics. The Nasdaq surged approximately 3.1% on 15 June, powered by Iran-related optimism and broad semiconductor strength. That left chip names stretched heading into Tuesday’s session.

The Nasdaq’s 3.1% Monday surge set the conditions for Tuesday’s pullback. The stocks that ran the hardest were the most exposed to profit-taking once the catalyst faded.

The sell-off concentrated in the names that had benefited most from the prior session’s momentum:

Pre-Fed repositioning compounded the pressure. The Federal Reserve’s two-day meeting began on 16 June, and long-duration growth stocks face specific rate-sensitivity risk when investors anticipate a hawkish tone. High-multiple semiconductor names sit at the intersection of both dynamics: they had run the hardest and carried the most duration exposure. The result was a sell-off that was mechanically predictable rather than fundamentally alarming.

If the Dow hit a record and the Nasdaq fell, are stocks going up or down? The answer depends on which stocks.

Sector rotation is the systematic movement of capital from one category of stocks to another. In this case, money moved from growth-oriented technology names into cyclical and value-oriented sectors: industrials, financials, and consumer staples. The Dow, weighted toward those cyclical sectors, captured the inflows. The Nasdaq, dominated by mega-cap technology and semiconductor names, absorbed the outflows.

The mechanics visible in Tuesday’s session are a textbook application of sector rotation strategy: institutional capital repositioning ahead of a catalyst, in this case the Fed meeting, produces index divergence that looks like contradiction on the surface but follows a consistent internal logic tied to the business cycle phase and duration sensitivity of each sector.

Tuesday’s session illustrates the sequence clearly:

The indices did not contradict each other. They reported on different parts of the same trade. Investors tracking only headline index numbers without understanding the composition behind them risk misreading a directional rotation as a mixed signal.

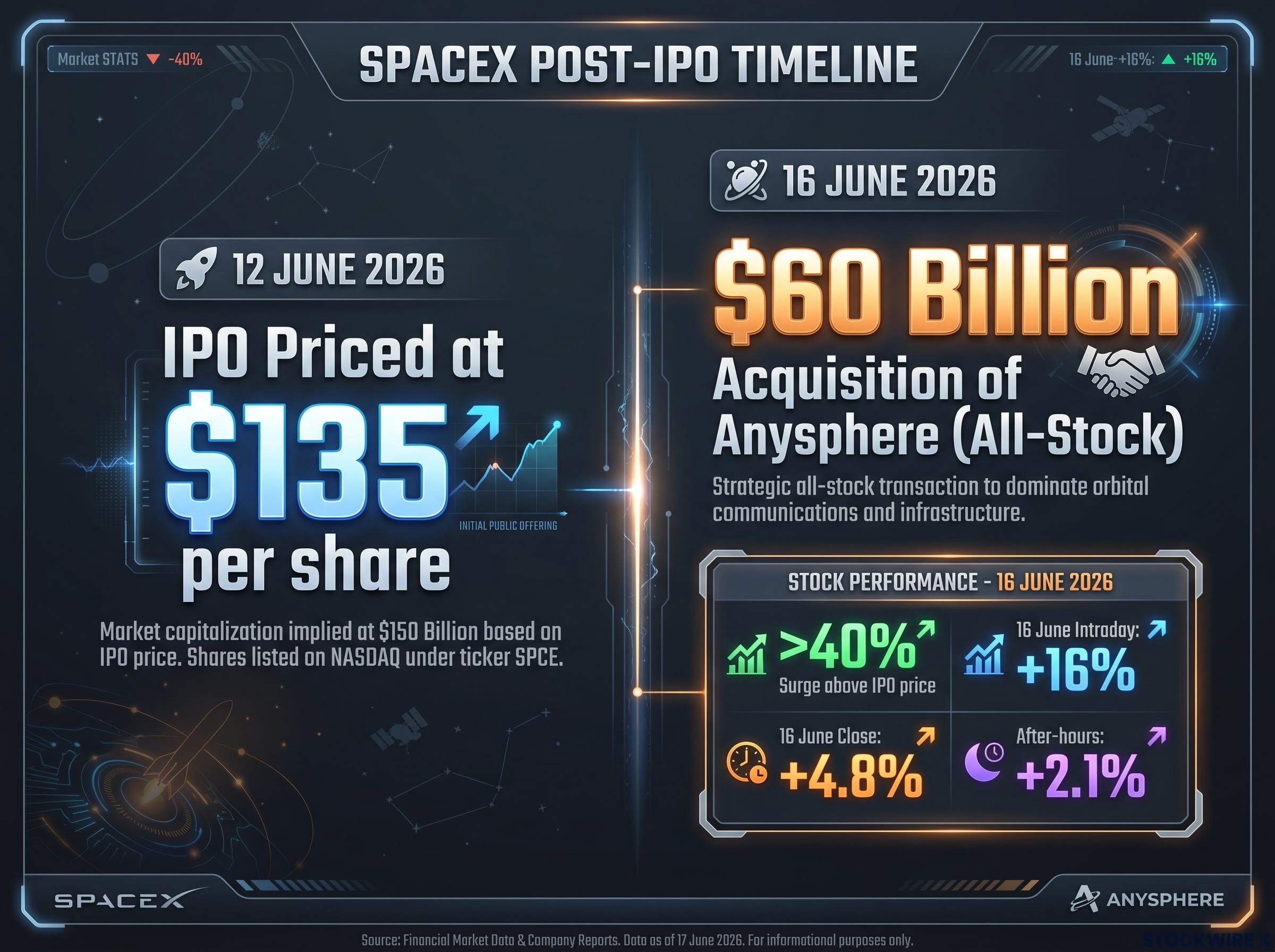

SpaceX agreed to acquire Anysphere, the parent company of AI coding tool Cursor, in an all-stock transaction valued at approximately $60 billion. The deal landed four days after SpaceX priced its initial public offering at $135 per share on 12 June 2026.

By Tuesday’s session, SpaceX shares had already surged more than 40% above the IPO price, making it one of the strongest post-IPO runs of the year.

The intraday trading arc on 16 June told a story of conviction tested and then reaffirmed across multiple timeframes. SpaceX shares rose as much as 16% intraday before settling to close approximately 4.8% higher. In after-hours trading, shares gained an additional 2.1%.

Key details of the Anysphere acquisition:

The closing gain of 4.8% after a 16% intraday high suggests meaningful profit-taking, yet the 2.1% after-hours extension indicates buyers returned once the selling pressure cleared. For a stock just four days into its public life, the pattern points to sustained institutional interest rather than purely speculative momentum.

For investors assessing whether the post-IPO surge reflects fundamental conviction or pure momentum, our full explainer on SpaceX’s IPO structure and governance terms covers the dual-class share mechanics, the bypassed institutional roadshow, and the financial disclosures available in the S-1 that shape how institutional buyers have been sizing their positions.

Lionsgate Studios (LION) gained ground during Tuesday’s regular session. Then the after-hours correction arrived.

Shares dropped 5% in extended trading on 16 June after a report confirmed Netflix was not pursuing an acquisition of the studio. The reversal was sharp: intraday gains built on deal speculation evaporated in minutes once the report landed.

The sequence is a familiar one. Acquisition rumours inflate a stock during regular hours; a denial or clarification in the after-market strips those gains back, often with additional downside from disappointed holders exiting positions.

Streaming-sector consolidation speculation has been elevated for months, and studio names like Lionsgate remain frequent subjects of deal rumours. The pattern has persistent market impact because each new rumour carries a plausible strategic logic, even when the specific deal fails to materialise. Tuesday’s Lionsgate reversal was a contained event, secondary to the broader tech-rotation and SpaceX narratives, but it serves as a reminder of the speed at which rumour-driven positions can unwind.

The Federal Reserve’s two-day meeting concludes on 17 June 2026, with a rate decision and statement expected that afternoon. Consensus expectations point to rates held steady.

The Federal Reserve’s FOMC meeting calendar confirms the June 16-17 session as a scheduled two-day policy meeting, with the rate decision statement and press conference materials published to the same official page once proceedings conclude.

The rate decision itself may be secondary to the language surrounding it. For the sectors that moved on Tuesday, three specific signals in the Fed statement and press conference deserve close attention:

The connection to Tuesday’s trade is direct. A hawkish tone validates the rotation into cyclicals and extends the pressure on technology. A neutral or modestly dovish signal could reverse it, allowing semiconductor and AI names to recapture ground. Active investors who repositioned on Tuesday face a binary outcome that will be resolved within hours.

Tuesday’s session resolves into a single coherent story once the mechanics are visible. Profit-taking after Monday’s 3.1% Nasdaq surge, pre-Fed caution concentrated in long-duration growth names, and capital rotating into cyclicals produced entirely predictable index divergence: the Dow up 0.64% to a record 51,999.67, the Nasdaq down 1.15%, the S&P 500 off 0.57%.

This was an orderly, mechanics-driven rotation. It was not a structural breakdown in technology, nor a trend reversal in the AI and semiconductor thesis that has powered much of 2026’s equity performance.

Dow Theory divergence signals offer a longer-dated lens on Tuesday’s index split: the framework holds that a bull market requires confirmation across industrial and transportation averages, meaning the Dow’s record close carries more structural weight if it is accompanied by broader index participation rather than cyclical inflows alone.

The sequel arrives on 17 June with the Fed’s statement and press conference. How the growth-to-cyclical rotation resolves depends on the tone of that communication. Until then, Tuesday’s divergence is best read as the market doing what it does between catalysts: repositioning, not retreating.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Sector rotation is the systematic movement of capital from one category of stocks to another. On 16 June 2026, investors moved money out of high-multiple technology and semiconductor names into cyclicals like industrials and financials, lifting the Dow to a record while the Nasdaq fell 1.15%.

The sell-off followed Monday's 3.1% Nasdaq surge, which left chip names stretched and exposed to profit-taking. Pre-Fed caution also added pressure, as high-multiple semiconductor stocks carry significant duration sensitivity ahead of a potentially hawkish Fed statement.

SpaceX agreed to acquire Anysphere, the parent company of AI coding tool Cursor, in an all-stock deal valued at approximately $60 billion. Shares rose as much as 16% intraday before closing up 4.8%, then gained an additional 2.1% in after-hours trading, extending a post-IPO surge of more than 40% above the $135 IPO price.

Lionsgate shares fell approximately 5% in extended trading after a report confirmed Netflix was not pursuing an acquisition of the studio, reversing intraday gains that had been built on deal speculation during the regular session.

Investors should focus on three signals: any upward revision to the inflation outlook, which would extend pressure on growth stocks; forward guidance on the rate path, which affects high-multiple semiconductor and AI names; and any commentary on balance sheet policy, which influences broader market liquidity conditions.