Goldman Warns CPI Print Could Reprice an Overvalued Market

10 hrs ago

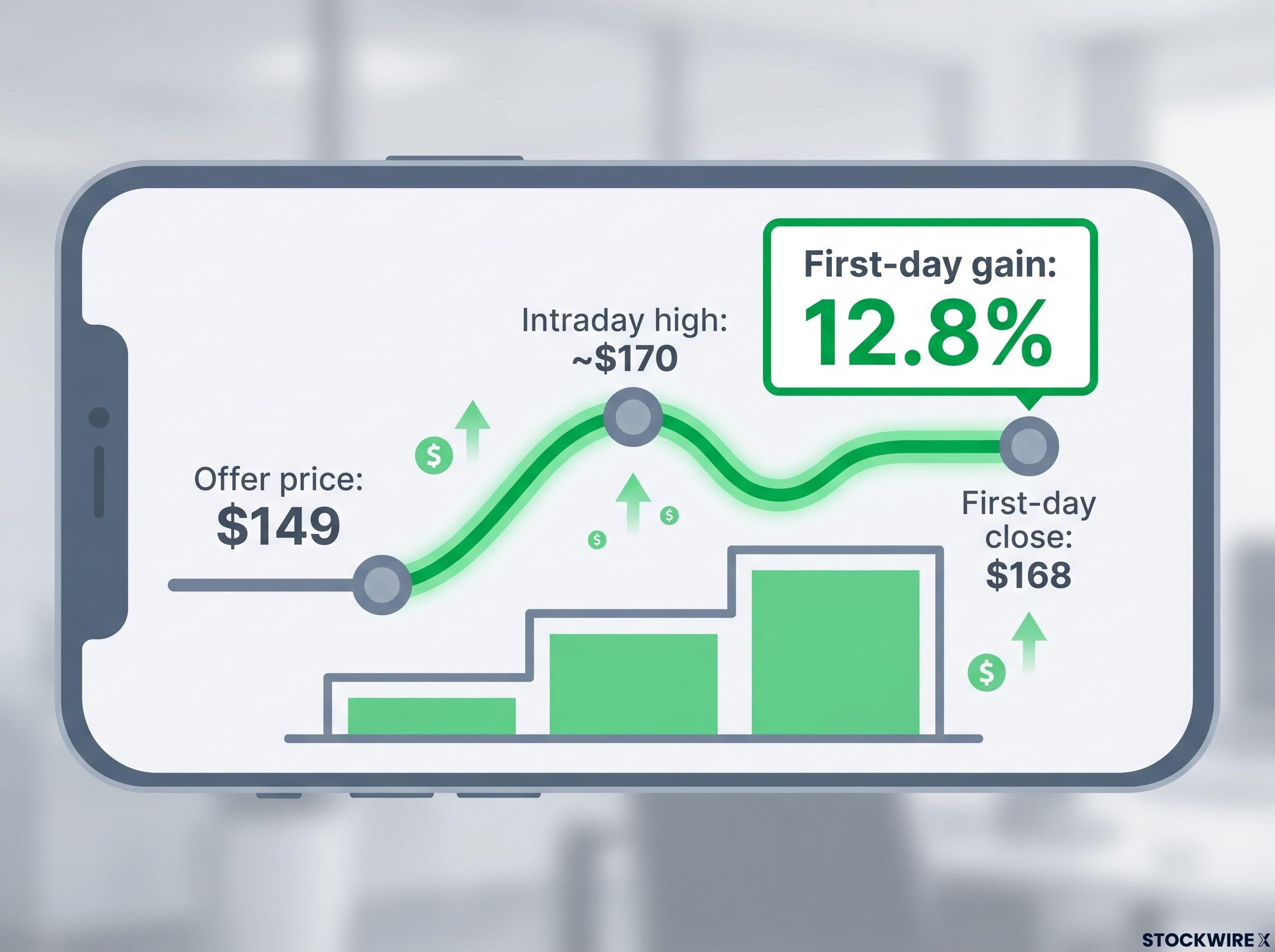

SK Hynix priced 177.9 million American depositary shares at $149 each on Friday, 10 July 2026, raising $26.5 billion before the Nasdaq opening bell and claiming the largest-ever US share sale by a foreign company in a single transaction.

The deal cleared Alibaba’s 2014 benchmark, landed as the second-largest IPO globally on record behind SpaceX’s June 2026 Nasdaq listing, and then did something that genuinely surprised the capital markets desks watching it unfold. When the first session wrapped, the shares had settled at $168, a gain of close to 13% over the offer price that transformed a record-breaking fundraise into a capital markets moment with consequences far beyond one stock.

Here is what drove that first-day performance, where the $26.5 billion is actually going, and what the outcome signals about the health of the AI-driven IPO pipeline heading into the second half of 2026.

The numbers tell the story in four lines:

That gain looks strong on any listing day. It looks remarkable in context.

IPO access mechanics help explain why the 12.8% first-day gain accrued primarily to institutions allocated at the $149 offer price rather than retail investors who entered in the secondary market, a structural feature of how large offerings are distributed that applies to every deal in the current AI listing cycle.

Nick Einhorn, Director of Research at Renaissance Capital, noted that cross-listings of already-liquid stocks typically trade relatively flat, particularly when the original listing is highly liquid. A mid-teen percentage gain on a deal of this scale is anomalous, not routine.

When the ADSs were priced, they sat at a premium of somewhere between 2.7% and 3% relative to the equivalent value of SK Hynix’s Korean ordinary shares on the prior day’s close, a figure Einhorn cited in his commentary. Through the US session, the Korean shares held steady while the American depositary shares climbed. No home-market dilution. No arbitrage-driven repricing.

That divergence is the detail worth sitting with. US investors were not repositioning existing global exposure. They were expressing genuinely new, incremental demand for dollar-denominated AI memory exposure at a scale the market had not previously tested.

The deal set two records simultaneously, and the precision of the comparison matters because both benchmarks involve names that reshaped their respective eras of capital markets activity.

SK Hynix overtook the benchmark set by Alibaba’s 2014 US listing, which had brought in $21.8 billion on an initial-raise basis. Some methodologies place Alibaba’s total higher depending on how greenshoe exercises are counted, but on an apples-to-apples initial-raise basis, SK Hynix now holds the record for the largest US share sale by a foreign company.

Renaissance Capital data places the offering second on the all-time global IPO leaderboard, with only SpaceX’s approximately $75 billion Nasdaq debut in June 2026 sitting ahead of it.

| Company | Year | Exchange | Amount Raised | Global Rank |

|---|---|---|---|---|

| SpaceX | June 2026 | Nasdaq | ~$75 billion | #1 all-time |

| SK Hynix | July 2026 | Nasdaq | $26.5 billion | #2 all-time |

| Alibaba | 2014 | NYSE | $21.8 billion | Previously #1 foreign US IPO |

What makes the record classification more than trivia is the mechanics behind it. A deal this size cleared cleanly, without discounting and without post-listing weakness, while the underlying Korean listing absorbed the supply event without flinching. That tells you US institutional capacity for AI infrastructure names is not yet showing signs of saturation.

SK Hynix’s market position had already shifted dramatically before the Nasdaq listing arrived, with the company displacing Samsung as South Korea’s most valuable listed company on 22 June 2026, a milestone driven by its estimated 70% share of the global HBM market and record full-year 2025 operating profit.

The market-performance story is one thing. The industrial logic underneath it is what gives the listing its forward-looking weight.

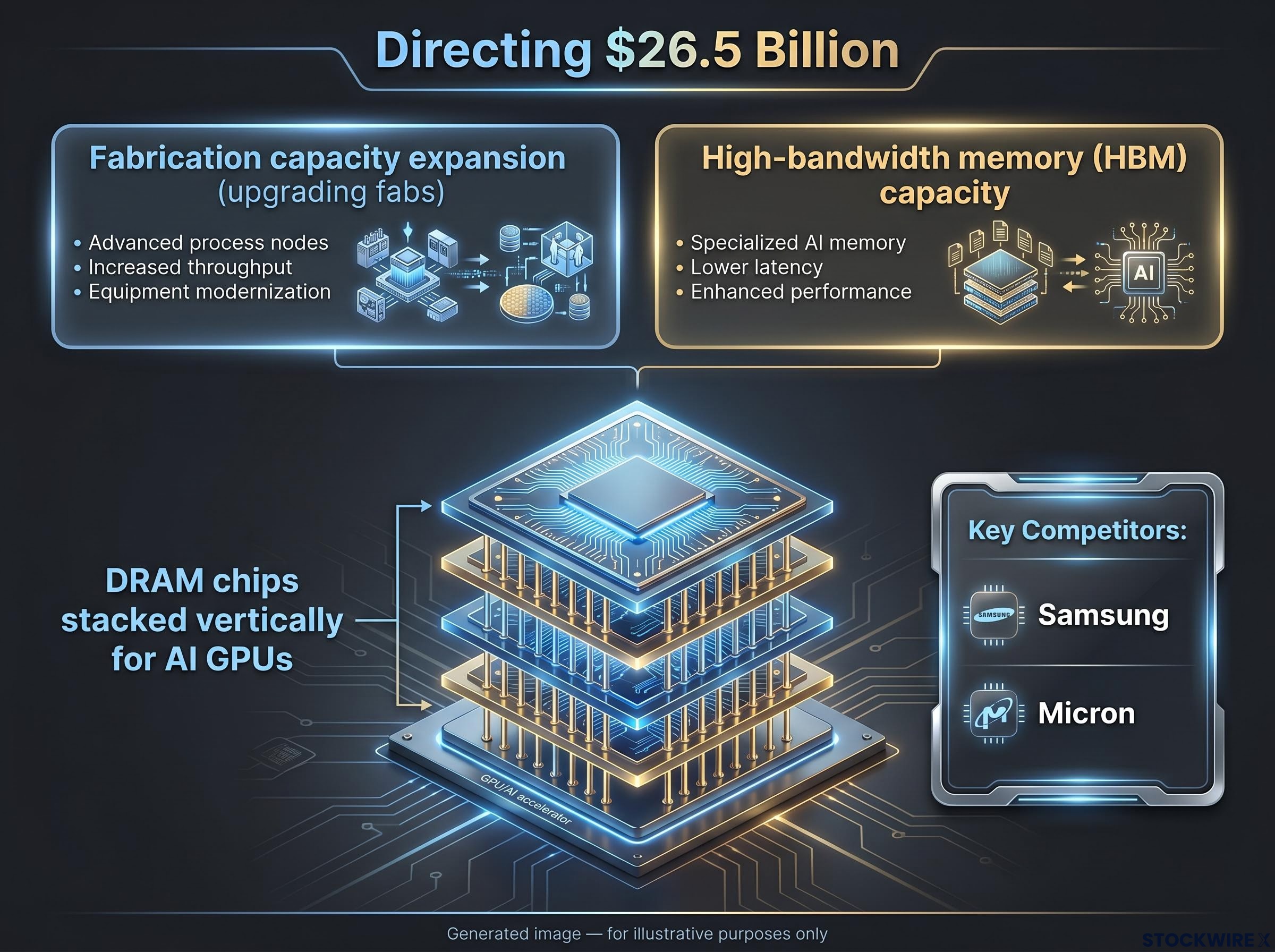

According to reporting from Morningstar’s Tom Lauricella, Senior Editorial Director for Global Markets (published 13 July 2026), proceeds are directed toward two categories of capital expenditure:

The programme is described across reporting as one of the most capital-intensive in the semiconductor industry. The US listing also opens a durable, large-scale fundraising channel in the world’s deepest equity market, diversifying SK Hynix’s financing away from Korean mechanisms alone.

HBM, or high-bandwidth memory, is a memory architecture that stacks DRAM chips vertically to deliver dramatically higher data transfer speeds than conventional memory. That speed is what AI chips need when processing the enormous datasets that power neural network workloads.

GPU clusters in data centres, the physical infrastructure running large-scale AI models, rely on HBM to move data fast enough to keep the processors fed. SK Hynix is among the leading global suppliers of this specific product category, which is why HBM capacity, rather than commodity DRAM, is the strategic priority for this capital deployment.

For investors assessing the AI memory supply chain, this allocation means SK Hynix is making a multi-billion-dollar bet that HBM demand will sustain at scale. That has direct competitive implications for Samsung and Micron, the two other major players in this space.

HBM supply chain dynamics extend well beyond the memory producers themselves, with Bernstein projecting 2-2.5x contract price increases for 2027 that amplify approximately fourfold at the hyperscaler purchase level once GPU vendors apply margin preservation, a cascade that reaches every layer of the AI infrastructure stack.

Pull the lens back from the single listing and the sequence becomes the story.

In June 2026, SpaceX listed on Nasdaq at approximately $75 billion. One month later, US markets committed another $26.5 billion to an AI infrastructure name. Both cleared at premium. Both were significantly oversubscribed, according to Bloomberg commentary on the SK Hynix transaction. Neither showed the post-listing weakness that typically accompanies supply shocks of this magnitude.

That is not a coincidence. It is a data point on structural demand.

Nick Einhorn of Renaissance Capital judged the SK Hynix listing a clear success, pointing out that the company brought in substantial funds for its capital expenditure programme, generated strong opening-day returns for US investors, and did so without putting any pressure on the Korean-listed shares.

The pattern reinforces a broader shift in how non-US technology companies access capital. The US market is increasingly the primary global hub where AI-related capital formation happens. SK Hynix choosing Nasdaq, and Nasdaq absorbing the deal at this scale, strengthens that gravitational pull.

Two consecutive mega-scale AI infrastructure listings clearing at premium in back-to-back months is the clearest signal yet that US institutional demand in this sector is structural, not situational. That has real implications for which companies choose to list where going forward.

SK Hynix’s debut answered one question convincingly. Whether it answers the next one is far less certain.

Nick Einhorn at Renaissance Capital identified data centre company Csquare as the next name poised to test the market, with the company expected to price during the week of 14-18 July 2026, putting it in the position of being the first issuer to either benefit from or strain against the momentum SK Hynix created.

The distinction between the two is not subtle:

Einhorn has been direct that the distinction between an established global leader like SK Hynix and later-stage names is the critical variable for assessing pipeline read-through. A record-setting debut from a world-leading semiconductor manufacturer does not automatically validate premium pricing for every AI-adjacent company behind it in the queue.

Whether you are watching as an investor or as a company weighing a US listing, Csquare’s debut will tell you more about the durability of the AI IPO window than SK Hynix’s own record-setting day did.

SK Hynix secured the largest US share sale ever by a foreign company, delivered a 12.8% first-day return that defied cross-listing norms, and validated the US market’s position as the primary global venue for AI capital formation at the largest scale. By the metrics that matter for a deal of this ambition, the listing succeeded.

What remains open is whether the conditions that made this possible extend beyond marquee names. Whether HBM demand sustains at the level the capital expenditure programme assumes. Whether the ADS premium to Korean shares persists as the US line seasons. Whether pipeline names like Csquare carry the same institutional conviction or expose the limits of the current appetite.

Memory cycle reversal risks form the counterargument to the structural demand thesis, with the $39 billion swing in SK Hynix operating profit from trough to peak illustrating both the upside the AI buildout has delivered and the magnitude of downside that a supply-driven reversal would produce if the 60% capacity expansion targets the wrong phase of the cycle.

The weeks following 10 July will be more informative than the record-breaking day itself, because they will reveal whether the AI IPO tailwind is structural enough to carry names that lack SK Hynix’s gravity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance.

—

SK Hynix priced 177.9 million American depositary shares at $149 each on 10 July 2026, raising $26.5 billion before the Nasdaq opening bell, making it the largest US share sale ever completed by a foreign company in a single transaction.

SK Hynix ADS shares closed at $168 on their first trading day, a gain of approximately 12.8% over the $149 offer price, with an intraday high of around $170, a result that Renaissance Capital described as anomalous for a cross-listing of an already-liquid stock.

Proceeds are directed toward fabrication capacity expansion and scaling high-bandwidth memory (HBM) production, the specific memory architecture that AI accelerator chips and data centre GPU clusters depend on to process large-scale neural network workloads.

Alibaba's 2014 NYSE listing raised $21.8 billion on an initial-raise basis and had held the record for the largest US share sale by a foreign company; SK Hynix's $26.5 billion Nasdaq deal surpassed it outright on the same apples-to-apples measure.

The deal cleared at a premium, was significantly oversubscribed, and produced no post-listing weakness in either the ADS or the underlying Korean shares, confirming structural institutional demand for AI infrastructure names, though Renaissance Capital analyst Nick Einhorn cautioned that this does not automatically validate premium pricing for smaller, less-proven pipeline companies like Csquare.