June US Inflation Report Hits as Fed Sits 9-9 on Rate Hikes

10 mins ago

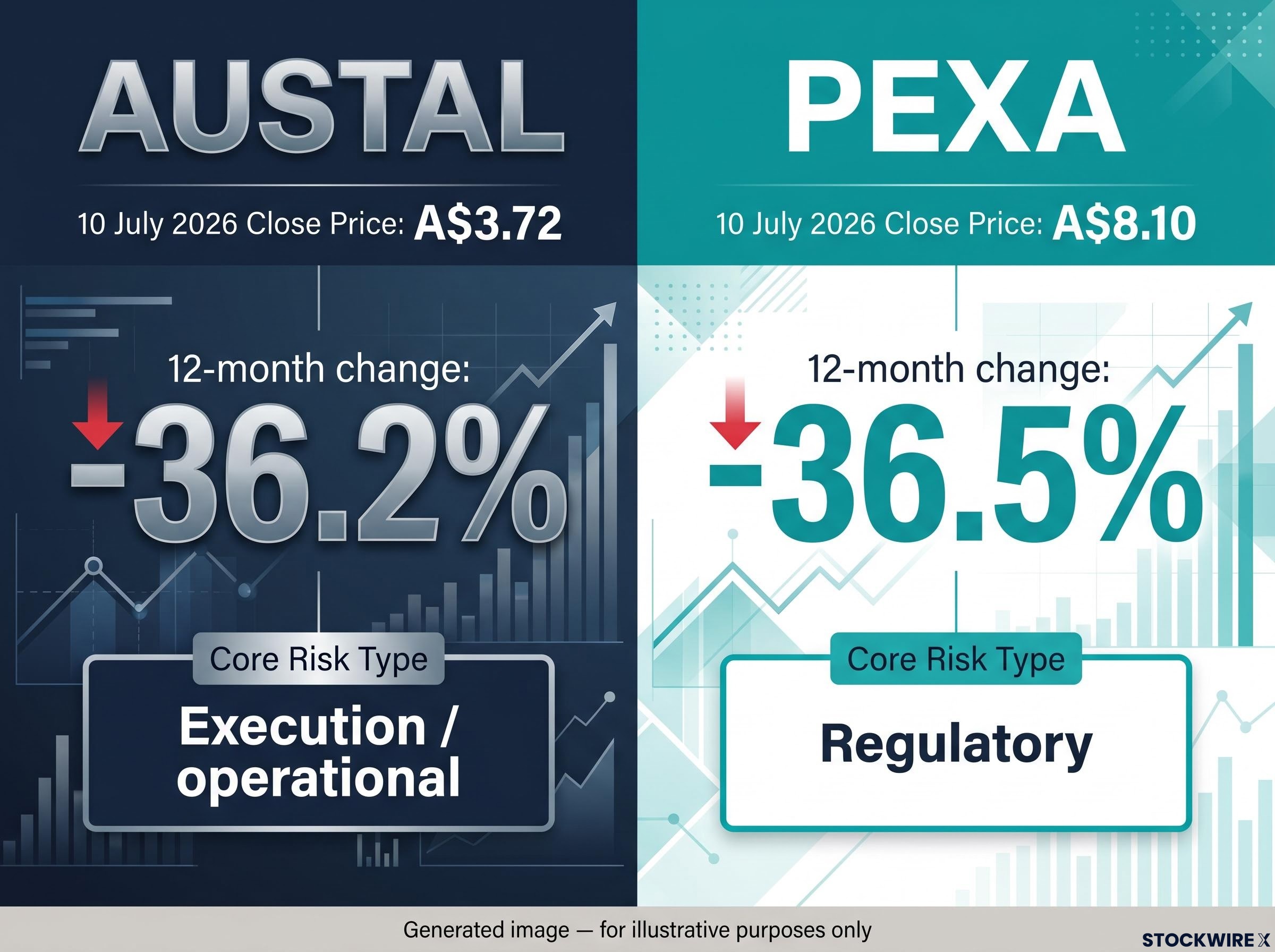

Two ASX 200 stocks. Both down roughly 36% over the past year. Both sitting at or near 52-week lows right now. The similarity ends there.

Austal and PEXA Group arrived at the same destination by very different roads. One faces questions about whether a record order book can actually be turned into earnings. The other absorbed a regulatory shock that sliced directly into the fee revenue its entire business model depends on. For Australian equity investors, the distinction matters enormously, because the playbook for assessing each situation is completely different.

This piece works through both cases with the data now available, giving you a clear view of what is actually driving each decline, what analysts are focused on, and what specific milestones will determine whether these prices represent genuine value or a value trap.

On the surface, the numbers are almost interchangeable. Austal (ASB) closed at A$3.72 on 10 July 2026, down 11.2% for the week and 36.2% over twelve months. PEXA Group (PXA) closed at A$8.10 the same day, down 5.2% for the week and 36.5% over twelve months. Both stocks hit or tested new 52-week lows in the same week.

That is where the parallel stops.

| Metric | Austal (ASB) | PEXA (PXA) |

|---|---|---|

| Close price (10 July 2026) | A$3.72 | A$8.10 |

| Weekly change | -11.2% | -5.2% |

| 12-month change | -36.2% | -36.5% |

| Key catalyst | Bell Potter target cut; prior accounting overstatement | IPART draft ruling on ELNO fees |

| Core risk type | Execution / operational | Regulatory |

The near-identical percentage declines could easily mislead you into treating these as equivalent situations. They are not. Austal’s problem is internal: can management deliver a massive order book at acceptable margins? PEXA’s problem is external: a government tribunal has proposed cutting its core fee revenue by roughly 20%. The forward-looking questions, the monitoring checklists, and the exit or entry criteria for each stock are entirely different.

Start with what looks like strength. Austal’s reported order backlog stands at A$17.7 billion, a record, anchored by US naval programmes and defence contracts. That is genuine, confirmed revenue visibility stretching out for years. For a company trading at A$3.72, the top-line picture looks compelling.

Backlog analysis in defence contracting requires separating funded from unfunded obligations and tracking the book-to-bill ratio over successive periods; a record headline backlog number, as Austal’s A$17.7 billion figure illustrates, tells investors the revenue ceiling without confirming that contracts will convert to earnings at acceptable margins.

Now look at what sits underneath it.

Bell Potter cut its price target for Austal to A$4.10, down from A$6.30, a reduction of roughly 35% in a single revision. The broker pointed to the considerable operational challenges facing Austal as it takes on a growing portfolio of complex steel shipbuilding programmes in the United States while at the same time pressing ahead with facility expansion at its Henderson yards in Western Australia.

Bell Potter’s revised target of A$4.10, down from A$6.30, represents a roughly 35% cut, one of the sharpest single-revision downgrades the stock has received.

That reassessment did not arrive in a vacuum. In February 2026, Austal disclosed an accounting overstatement and cut its FY26 EBIT guidance to approximately A$110 million. The stock was trading near A$8.80-9.00 at the time; the current price of A$3.72 represents a drawdown of more than 50% from that peak. The February event structurally altered how the market interprets Austal’s disclosures and forward guidance.

The execution risks are specific and identifiable:

For you as an investor evaluating Austal at current prices, the order book tells you the revenue ceiling. It says nothing about where margins land. And after February’s governance event, the market will require demonstrated delivery before repricing the stock higher.

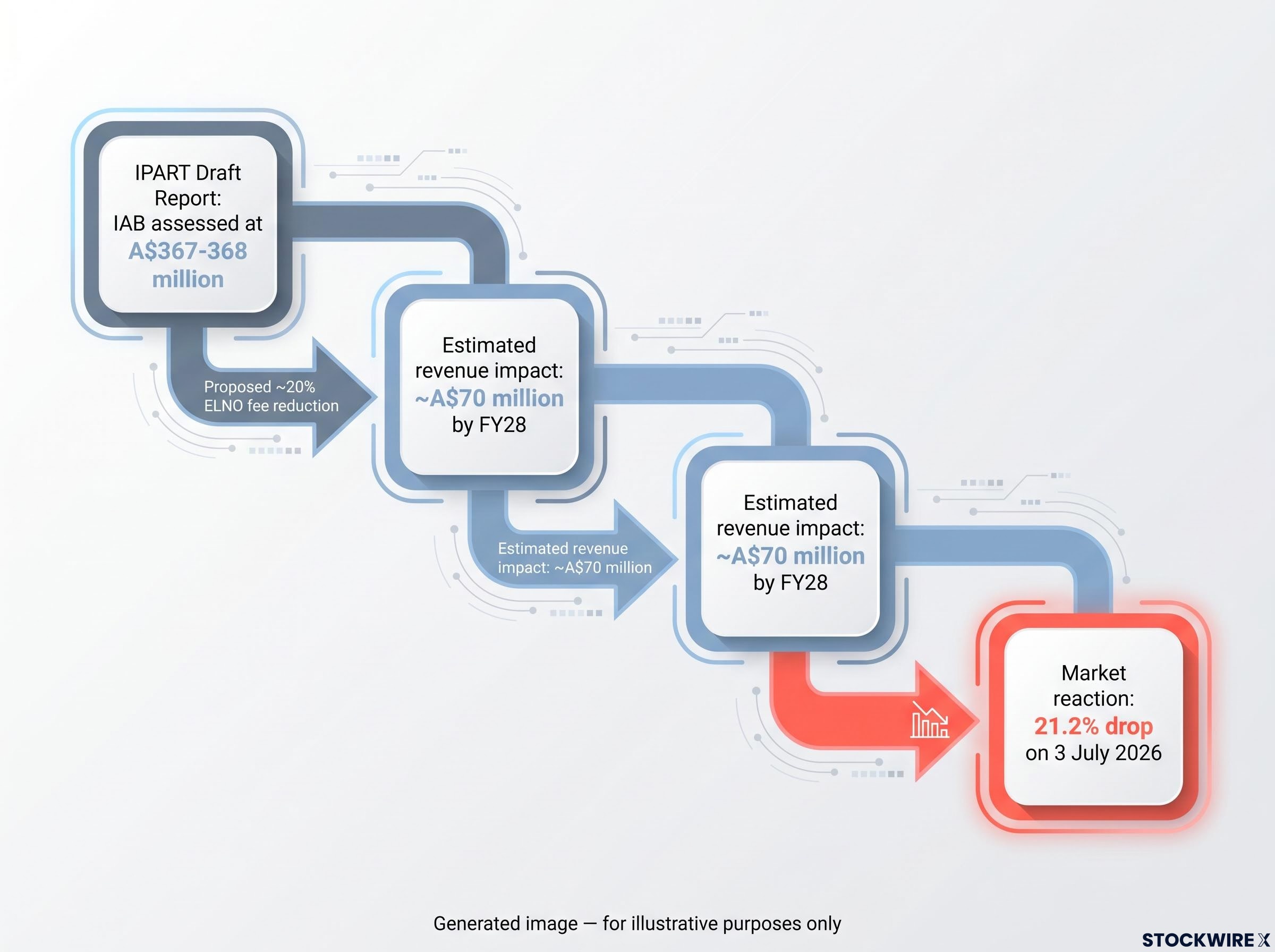

PEXA Group’s share price dropped 21.2% during the session on 3 July 2026, representing one of the most severe single-session sell-offs the company has experienced since listing.

A 21.2% single-day decline on 3 July 2026, triggered by IPART’s draft report, marked one of the sharpest one-day falls in PEXA’s time as a listed company.

The catalyst was a draft report from IPART (the Independent Pricing and Regulatory Tribunal), which put forward a reduction to regulated ELNO transfer fees of around 20%, a steeper outcome than the market had anticipated and one that IPART’s own modelling linked primarily to its assessment of a lower initial asset base than analysts had assumed. The estimated revenue impact: approximately A$70 million over the regulatory determination period to FY28.

Why did a sophisticated market not see this coming? The answer sits in a technical input called the initial asset base, or IAB. The IAB is the value IPART assigns to the regulated assets that underpin PEXA’s fee structure. A lower IAB produces a lower allowable revenue base, which directly drives the recommended fee reduction. IPART’s IAB assessment came in at approximately A$367-368 million, materially below many broker assumptions.

That gap between what analysts modelled and what IPART delivered is what produced the shock. Broker models had been calibrated to a softer outcome. The IAB is not a bureaucratic footnote; it is the engine of the entire pricing model. Until you understand why IPART landed where it did on asset valuation, you cannot assess whether management’s pushback has a credible chance of shifting the final determination.

The stock continued declining after the initial drop, reaching A$8.10 by 10 July 2026. PEXA management has publicly contested the draft through three channels:

PEXA’s situation illustrates something important: quasi-monopoly positioning does not insulate a business from regulatory repricing. The technical details of a single regulatory submission moved this stock by more than 20% in a single session.

Policy-driven market risk can compress months of earnings repricing into a single session, as PEXA’s 21.2% decline on 3 July 2026 demonstrates; mapping regulatory exposure before a determination arrives, rather than reacting after the session closes, is the structural habit that separates investors who absorb the shock from those who anticipated it.

The draft report is not the final word. IPART’s process moves from draft to final determination after formal submissions, and there is a meaningful difference between the two stages.

Complete reversals of IPART draft positions are rare. That is worth stating plainly. But adjustments to timing, calibration, and phase-in arrangements are documented precedents in Australian regulatory history. On the phase-in question, PEXA management has made its preference clear: it wants any fee reduction spread across four years, rather than landing all at once.

That third point matters more than it might first appear. PEXA’s fee revenue depends on both the per-transaction fee rate and the number of transactions processed. Higher Australian property transaction volumes can partially offset lower per-transaction fees. The net earnings impact of the IPART ruling will depend in part on property market conditions over the determination period, a variable outside PEXA’s control but one that works in both directions.

Australian property transaction volumes function as a partial natural hedge within PEXA’s earnings model; when volumes rise, higher transaction counts offset the revenue impact of lower per-transaction fees, linking PEXA’s financial performance to the same property market dynamics that influence A-REIT valuations and direct property investor activity.

PEXA’s UK platform and broader international strategy represent the structural mechanism for reducing reliance on regulated Australian ELNO fees over time. The more material the international business becomes, the less sensitive PEXA’s total earnings profile is to any single IPART ruling. That diversification is not yet large enough to offset the current shock, but it changes the sensitivity calculation for investors looking beyond the next twelve months.

The final determination is the event that matters for PEXA investors, not the draft. Whether management wins any ground on the IAB or the phase-in schedule will determine whether current prices turn out to be an overreaction or a fair new baseline.

A stock hitting its 52-week low is not automatically a buy signal or a sell signal. It is an invitation to ask a specific question: what caused the decline, and has the underlying risk been fully priced?

The distinction between a genuine discount and a value trap is one of the most consequential judgments in ASX equity investing, and value trap recognition depends less on the percentage drawdown itself than on whether the underlying earnings impairment is temporary or structural.

Austal and PEXA illustrate the two most common risk types you will encounter at annual lows, and they require different frameworks:

In both cases, specific, dateable events precipitated the decline. Austal’s accounting overstatement in February 2026 and PEXA’s IPART draft on 3 July 2026 are identifiable catalysts, not sentiment-driven selling or market-wide drawdowns.

The forward milestones worth tracking are equally specific:

The investor who can name the specific risk driving a stock’s annual low, identify who or what resolves it, and set a monitoring schedule around those resolution events is better positioned than one who simply reads the number as a valuation signal.

Austal at A$3.72 trades roughly 10% below Bell Potter’s revised target of A$4.10. That narrow gap tells you the market is not expecting a swift recovery; it is expecting proof. The conditions are specific: successful execution across the steel shipbuilding programmes, clean margin realisation over the next two reporting periods, and no further governance or accounting surprises. Until those conditions are met, the record A$17.7 billion order book remains a revenue ceiling, not an earnings floor.

PEXA at A$8.10 faces a different test entirely. The IPART final determination is the defining near-term catalyst. A ruling that softens the draft’s terms, whether on the IAB methodology or the phase-in schedule, would create room for a re-rating. A ruling that largely confirms the draft locks in a lower earnings base for the regulatory period. Alongside that, the trajectory of UK and international revenue will determine whether PEXA can grow its way toward reduced dependence on the regulated Australian fee structure.

IPART’s draft report on ELNO service fees sets out the full methodology behind the proposed revenue reduction, including the IAB valuation inputs that produced an asset base figure materially below broker assumptions and directly drove the recommended fee cut.

The proof points for each stock:

Neither stock is a straightforward recovery bet. Both require specific milestones to resolve before price recovery has a credible foundation. The 36% drawdown is a statistical coincidence. The investor frameworks for each stock should be entirely distinct.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A 52-week low signals the stock has reached its cheapest point in a year, but it is not automatically a buy signal. The critical question is whether the underlying cause of the decline is temporary or structural, as illustrated by Austal's execution risk and PEXA's regulatory repricing arriving at the same percentage drawdown via completely different paths.

IPART, the Independent Pricing and Regulatory Tribunal, released a draft report on 3 July 2026 proposing a roughly 20% reduction to regulated ELNO transfer fees, with the cut driven by an initial asset base valuation of approximately A$367-368 million, materially below what broker models had assumed, producing an estimated revenue impact of around A$70 million over the regulatory period to FY28.

The initial asset base is the value IPART assigns to the regulated assets underpinning PEXA's fee structure. A lower IAB produces a lower allowable revenue base, which directly drives the recommended fee reduction. IPART's IAB assessment coming in below broker assumptions is precisely what caused the 21.2% single-day share price collapse.

The order book confirms revenue visibility but says nothing about where margins will land. Austal's transition from aluminium to steel shipbuilding, simultaneous facility expansion at Henderson and US yards, and the February 2026 accounting overstatement mean the market requires demonstrated delivery before repricing the stock, making the A$17.7 billion figure a revenue ceiling rather than an earnings floor.

For Austal, the key watchpoints are margin realisation on steel vessel contracts and clean reporting across the next two periods with no further governance events. For PEXA, the defining catalyst is the IPART final determination, specifically whether management wins any ground on the IAB methodology or secures a four-year phase-in of the fee reduction rather than an immediate cut.