How to Value Apple Stock: Metrics, Catalysts, and Risk Factors

Key Takeaways

- Apple posted record Q1 2026 revenue of $143.8 billion — up 16% year-over-year — yet its stock has declined 9% year-to-date, creating a potential valuation disconnect investors should evaluate carefully.

- At a 34x price-to-earnings ratio, Apple's premium valuation requires continued execution excellence, with the Q2 2026 earnings report on 30 April serving as a critical thesis validation point.

- Analysts project $75 to $100 per share in potential value creation from Apple's AI initiatives, including the Google Gemini partnership and a comprehensive Siri refresh, though monetisation timelines remain undefined.

- Apple achieved its best-ever iPhone quarter in China with 38% revenue growth and 19% market share, whilst the broader smartphone market contracted 4%, underscoring strong competitive positioning in a key growth market.

- The consensus analyst price target of $296 implies approximately 10% upside from current levels, with Wedbush's bullish $350 target representing 30% appreciation potential contingent on AI execution and geographic expansion.

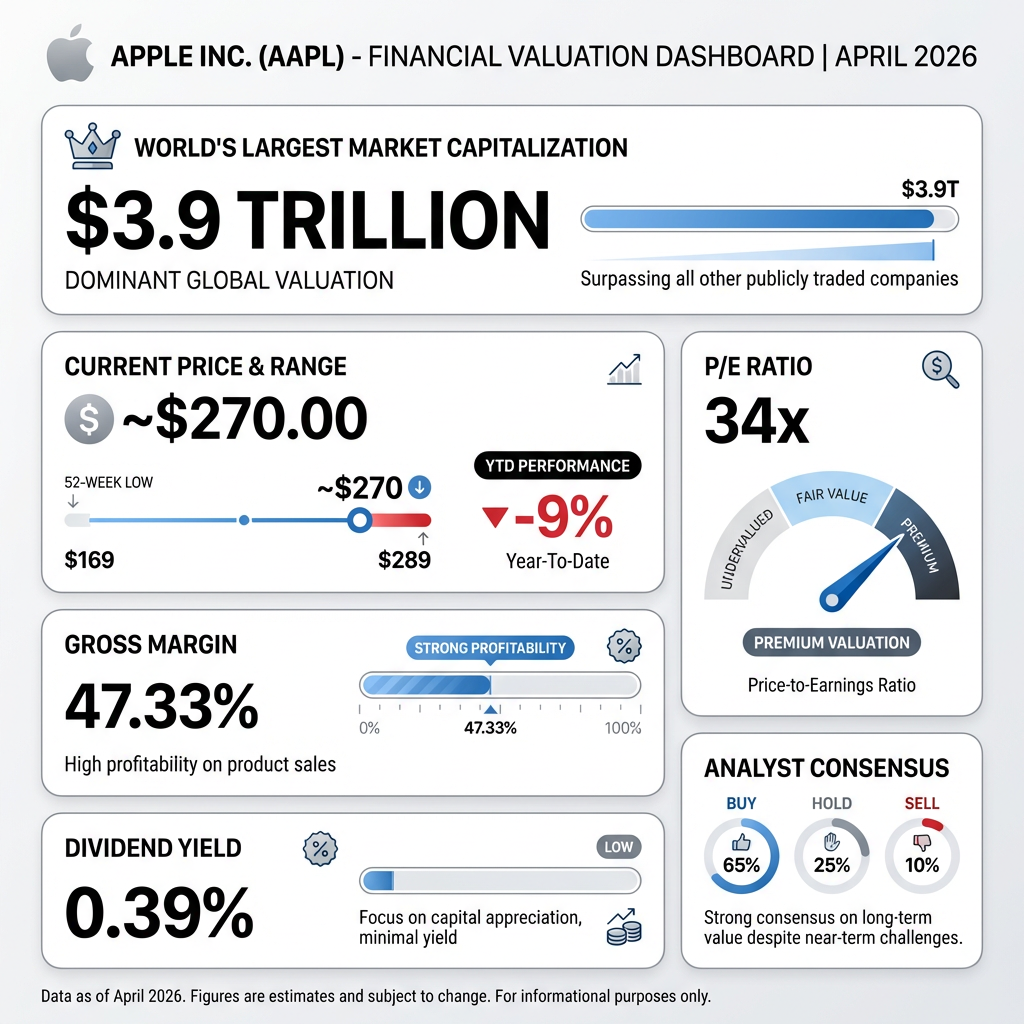

Apple holds the title of the world’s most valuable company with a $3.9 trillion market capitalisation, yet its stock has declined 9% year-to-date in 2026 despite posting record Q1 earnings of $143.8 billion. This disconnect between operational excellence and share price performance raises a critical question for investors: does the current valuation reflect opportunity or appropriate risk pricing?

Understanding Apple stock valuation requires examining multiple layers of financial data, from traditional metrics like price-to-earnings ratios to forward-looking catalysts such as artificial intelligence initiatives and geographic expansion. This guide provides a comprehensive framework for evaluating whether Apple’s current trading levels represent fair value, combining Q1 2026 results with analyst projections and strategic growth drivers. Investors will gain actionable insights into the metrics that matter, the catalysts that could drive shares higher, and the risks that warrant careful monitoring.

Understanding Stock Valuation: Key Metrics for Apple Investors

Stock valuation analysis determines whether a company’s share price accurately reflects its intrinsic value based on financial performance, growth prospects, and competitive positioning. For Apple investors, mastering core valuation metrics provides the foundation for informed decision-making about entry points, position sizing, and portfolio allocation.

The CFA Institute’s equity valuation framework provides the professional standard for interpreting price-to-earnings ratios and fundamental analysis techniques used by investment professionals globally.

Essential valuation metrics include:

- Price-to-Earnings (P/E) Ratio: Measures share price relative to earnings per share, indicating market expectations for future growth. Apple currently trades at a P/E of 34x, reflecting a premium valuation compared to broader market averages.

- Market Capitalisation: Represents total company value calculated by multiplying share price by outstanding shares. Apple’s $3.9 trillion market cap positions it as the world’s most valuable publicly traded company.

- Gross Margin: Indicates profitability by measuring revenue retained after direct production costs. Apple’s gross margin of 47.33% demonstrates strong pricing power and operational efficiency.

- Dividend Yield: Shows annual dividend payments as a percentage of share price. Apple’s current yield of 0.39% reflects modest income generation relative to share price appreciation potential.

- Price-to-Sales Ratio: Compares market value to total revenue, useful for evaluating companies with varying profit margins across business segments.

Analyst price targets provide additional context by projecting future share prices based on fundamental analysis and growth assumptions. The current consensus target of $296 represents approximately 10% upside from recent trading levels around $270, whilst Wedbush’s bullish $350 target implies 30% potential appreciation. These projections incorporate varying assumptions about iPhone sales momentum, artificial intelligence monetisation, and macroeconomic conditions.

When big ASX news breaks, our subscribers know first

Apple’s Current Valuation: Where the Stock Stands in April 2026

As of mid-April 2026, Apple stock presents a complex valuation picture characterised by premium multiples, recent price weakness, and mixed analyst sentiment. The following table summarises key metrics:

| Metric | Current Value |

|---|---|

| Current Price | ~$270 |

| Market Capitalisation | $3.9 trillion |

| P/E Ratio | 34x |

| 52-Week High | $289 |

| 52-Week Low | $169 |

| YTD Performance | -9% |

| Gross Margin | 47.33% |

| Dividend Yield | 0.39% |

The 9% year-to-date decline stands in stark contrast to Apple’s exceptional Q1 2026 operational performance, which delivered record revenue and significant earnings growth. This disconnect reflects broader market concerns about geopolitical tensions, tariff impacts on supply chains, and rising component costs rather than fundamental business deterioration. The Middle East conflict has driven memory chip prices higher, whilst uncertainty around international trade policy has created headwinds for technology hardware companies with complex global manufacturing networks.

Understanding the broader technology sector rally to all-time highs in mid-April 2026 provides important context for evaluating whether Apple’s 9% year-to-date decline represents underperformance relative to sector momentum or appropriate risk pricing given company-specific factors.

Apple’s position within the Magnificent Seven stocks provides important context for understanding its valuation relative to mega-cap technology peers that collectively added $2.51 trillion in market capitalisation during April 2026’s historic rally.

Analyst sentiment remains constructive despite recent price weakness. The consensus price target of $296 suggests approximately 10% upside potential from current levels, whilst Wedbush maintains a bullish $350 target representing 30% appreciation potential. Knockout Stocks issued a “strong buy” rating at price levels between $250 and $260, viewing the recent pullback as an attractive entry opportunity for long-term investors. The upcoming Q2 earnings report scheduled for 30 April 2026 represents a critical validation point for assessing whether Q1 momentum can be sustained.

Fiscal Performance Driving Apple’s Valuation Premium

> CEO Tim Cook on iPhone 17 Demand

> “We’re seeing off the chart demand globally. The response to iPhone 17 has been staggering across all major markets.”

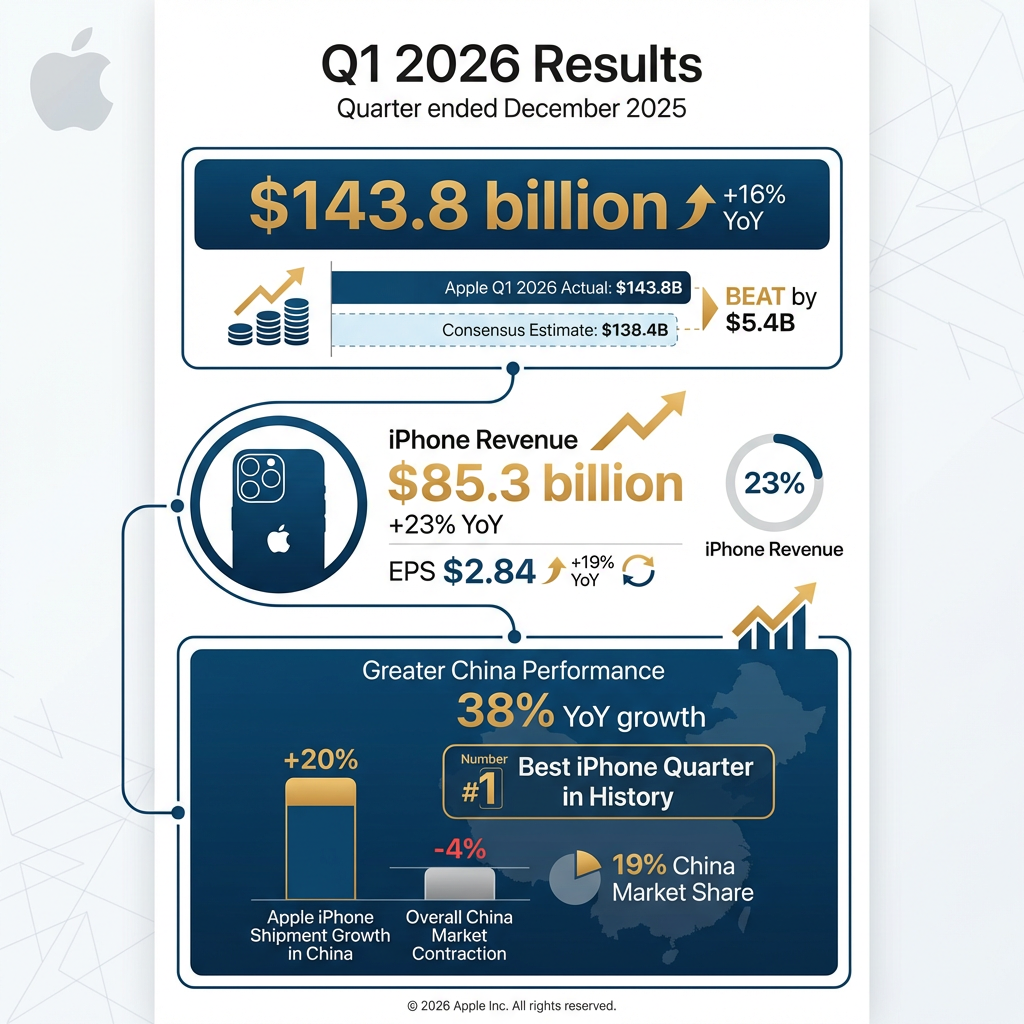

Apple’s Q1 2026 results, covering the quarter ended December 2025, demonstrated the operational strength supporting the company’s premium valuation. Revenue reached a record $143.8 billion, representing 16% year-over-year growth and exceeding consensus estimates of $138.4 billion by $5.4 billion. Earnings per share of $2.84 grew 19% year-over-year, showcasing operating leverage and margin expansion despite cost pressures.

iPhone performance drove the exceptional quarter, with revenue hitting a record $85.3 billion and growing 23% year-over-year. The iPhone 17 launch created significant upgrade momentum as consumers replaced devices purchased during the pandemic era, which are now reaching the end of typical three-year usage cycles. Strong demand occurred across all geographic regions, with Apple’s premium positioning and product durability sustaining average selling prices.

Greater China delivered what management characterised as the “best iPhone quarter in history,” with revenue growing 38% year-over-year. iPhone shipments in China increased 20% during Q1 2026 whilst the overall smartphone market contracted 4%, demonstrating Apple’s competitive strength against local manufacturers. The company achieved 19% market share and an all-time high installed base in the region, positioning it for sustained Services revenue growth. This performance occurred despite geopolitical tensions and competitive pressure from domestic brands, validating Apple’s brand strength and ecosystem advantages in a critical growth market.

Growth Catalysts: What Could Drive Apple Stock Higher

Artificial intelligence initiatives represent Apple’s primary long-term valuation catalyst, with analysts projecting $75 to $100 per share in potential value creation. The strategic partnership with Google Gemini advances Apple’s AI capabilities, whilst the comprehensive Siri refresh positions the voice assistant platform to compete more effectively with rivals. Management highlighted significant progress in AI strategy during Q1 earnings discussions, though specific monetisation timelines remain undefined. Services revenue could accelerate as AI features drive increased user engagement and premium subscription adoption.

Whilst AI monetisation uncertainties across the technology sector persist, with institutional investors questioning whether $6 trillion in AI investments will generate proportional returns, Apple’s integrated ecosystem approach may provide competitive advantages over pure-play AI competitors.

Geographic expansion opportunities provide additional upside potential:

- China: 19% market share with all-time high installed base creates foundation for Services growth and continued hardware penetration

- India: 9% market share in rapidly growing smartphone market offers significant expansion runway as middle-class purchasing power increases

- Greater China: Building on 38% revenue growth momentum from best-ever iPhone quarter, with ecosystem lock-in supporting retention

The iPhone supercycle driven by iPhone 17 adoption continues to exceed expectations, supported by premium positioning that commands higher average selling prices and product durability that extends replacement cycles beyond three years. This combination sustains demand whilst maintaining profitability, as consumers view iPhones as long-term investments rather than annual upgrades. Wedbush cited iPhone 17 momentum and upcoming product refreshes as key catalysts supporting its $350 price target, whilst analyst models imply $301 representing 21% upside over a 2.5-year horizon.

The next major ASX story will hit our subscribers first

Risk Factors: Headwinds to Monitor in Your Valuation Analysis

Supply chain and tariff risks present the most immediate challenges to Apple’s valuation sustainability. The Middle East conflict has driven memory chip costs higher, compressing gross margins on hardware products. Geopolitical tensions create uncertainty around international trade relationships, whilst potential tariff escalations could increase component costs or finished goods pricing. Counterpoint Research positioned Apple as “best-equipped” amongst competitors to manage these cost increases, citing superior supply chain management and financial resources.

The Middle East conflict that escalated in February 2026 has created significant supply chain disruptions across global technology manufacturing, particularly affecting memory chip availability and pricing that directly impacts Apple’s component costs.

Key risk factors requiring ongoing monitoring include:

- Tariff escalation impacting supply chain costs and component pricing across Asia-Pacific manufacturing network

- Memory chip cost increases from Middle East conflict reducing gross margin percentage

- Consumer spending pressures from persistent inflation potentially delaying upgrade cycles in mature markets

- Smartphone market saturation in developed economies limiting addressable market growth

- China market volatility evidenced by February shipment decline of 7.7% year-over-year following strong Q1 performance

- Competitive dynamics in key markets as rivals adjust pricing and feature sets

Apple’s competitive advantages partially mitigate these risks through superior cost management capabilities, premium brand positioning that maintains pricing power, and ecosystem strength that reduces customer churn. Whilst competitors like Xiaomi suffered 35% shipment declines in China during challenging periods, Apple sustained growth through brand loyalty and product differentiation. The company’s balance sheet strength and operational scale provide flexibility to navigate temporary margin pressures without compromising long-term strategic investments in AI and geographic expansion.

Investment Framework: How to Approach Apple Stock Valuation

Apple’s current valuation reflects a premium positioning supported by record fundamental performance, identifiable growth catalysts in artificial intelligence and geographic expansion, and competitive advantages in brand strength and ecosystem lock-in. The 9% year-to-date decline creates a potential entry opportunity if Q2 results validate the sustainability of Q1 momentum, particularly in China where month-to-month volatility requires careful monitoring.

Investors evaluating Apple stock valuation should monitor these critical data points:

- Q2 2026 results (reporting 30 April) for confirmation of sustained revenue growth and margin stability

- China performance trends beyond Q1’s exceptional 38% growth, watching for consistency in monthly shipment data

- AI monetisation progress through Services segment growth and feature adoption metrics

- Tariff and supply chain developments impacting component costs and gross margin percentages

- Services segment resilience providing earnings stability during hardware market fluctuations

The consensus analyst target of $296 represents approximately 10% upside from current levels, whilst bullish scenarios reaching $350 imply 30% appreciation potential contingent on successful AI execution and sustained geographic momentum. Position sizing should reflect both the opportunity presented by recent weakness and the risks associated with macroeconomic uncertainty and premium valuation multiples. The P/E ratio of 34x requires continued execution excellence to justify, making upcoming quarterly results critical validation points for investment thesis reassessment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is Apple's current stock valuation in 2026?

As of mid-April 2026, Apple trades at approximately $270 per share with a price-to-earnings ratio of 34x and a market capitalisation of $3.9 trillion, making it the world's most valuable publicly traded company despite a 9% year-to-date decline.

Why has Apple stock declined in 2026 despite record earnings?

Apple's 9% year-to-date decline reflects macroeconomic headwinds including geopolitical tensions, tariff uncertainty, and rising memory chip costs from the Middle East conflict, rather than fundamental business deterioration — the company posted record Q1 2026 revenue of $143.8 billion with 16% year-over-year growth.

What is the analyst price target for Apple stock?

The consensus analyst price target for Apple is $296, representing approximately 10% upside from recent trading levels around $270, while Wedbush maintains a more bullish $350 target implying 30% potential appreciation.

How should investors evaluate Apple stock valuation before Q2 2026 earnings?

Investors should monitor the Q2 2026 earnings report scheduled for 30 April 2026 as a critical validation point, focusing on China revenue trends, Services segment growth, gross margin stability, and early signals of AI monetisation progress.

What are the biggest risks to Apple's valuation in 2026?

The primary risks include tariff escalation affecting supply chain costs, memory chip price increases from Middle East tensions compressing gross margins, consumer spending pressures delaying upgrade cycles, and month-to-month volatility in China shipment data following Q1's exceptional 38% revenue growth.