According to market data, the S&P 500 gained 84.3% over the last five years, but Norwegian Cruise Line Holdings (NCLH) shares moved sharply in the opposite direction. The maritime operator saw its equity plunge over the same period, leaving the business uniquely vulnerable to an activist investor. By April 2026, this financial stagnation triggered a complete corporate governance overhaul, with Elliott Investment Management officially seizing control of the boardroom to address long-standing underperformance.

While the headline index performance appears incredibly robust, persistent stock market warning signals tied to rising energy costs and geopolitical tension suggest this broad equity growth masks rising risks for fuel-intensive travel operators.

The arrival of institutional intervention transformed a story of broad industry headwinds into a clear example of structural financial restructuring. This boardroom takeover forces a confrontation between the company’s historical capital misallocation and a newly installed board mandate.

Retail investors and institutional analysts are now watching closely. They need to see exactly how billions of dollars in leveraged equity will force management to execute a strategic turnaround.

The Valuation Disconnect and Shareholder Frustration

The inevitability of outside intervention becomes clear when analysing the historical valuation gap between Norwegian Cruise Line Holdings and its direct competitors. The company maintained a premium earnings multiple for years, an anomaly that deeply frustrated shareholders as operational execution continuously lagged behind peers. This structural overvaluation painted a massive target on the company, signalling to the market that current management was failing to capitalise on the pricing power implied by their stock premium.

Institutional firms analysing valuation discounts often target businesses where the gap between perceived market premiums and actual operational execution reveals a clear opportunity for structural reform.

Investor patience fully deteriorated by the beginning of 2026, leading to a rapid rerating of the stock. The trailing price-to-earnings (P/E) multiple contracted severely, eventually settling at 19.34 by late April 2026. This multiple compression revealed a market recalibrating its expectations, pricing in the stark reality of the operator’s fundamental underperformance.

A comparison of industry peers illustrates the true depth of this valuation disconnect.

| Company | Stock Price (Late April 2026) | P/E Ratio (TTM) | Market Capitalisation Context |

|---|---|---|---|

| Norwegian Cruise Line Holdings (NCLH) | $17.79 | 19.34 | $8.104 Billion |

| Carnival Corporation (CCL) | $26.30 | 11.59 | Industry Peer |

| Royal Caribbean Group (RCL) | $255.89 | 16.39 | Industry Peer |

When big ASX news breaks, our subscribers know first

Anatomy of a Boardroom Takeover: The Activist Playbook

Corporate activism operates on a distinct mechanical playbook, leveraging accumulated equity to force strategic shifts without purchasing a company outright. A major financial firm acquires a significant equity stake in an underperforming public company, using that ownership block to demand immediate operational and governance modifications. Once an activist crosses a specific equity threshold, typically over 10 percent, management is legally and practically forced to the negotiating table.

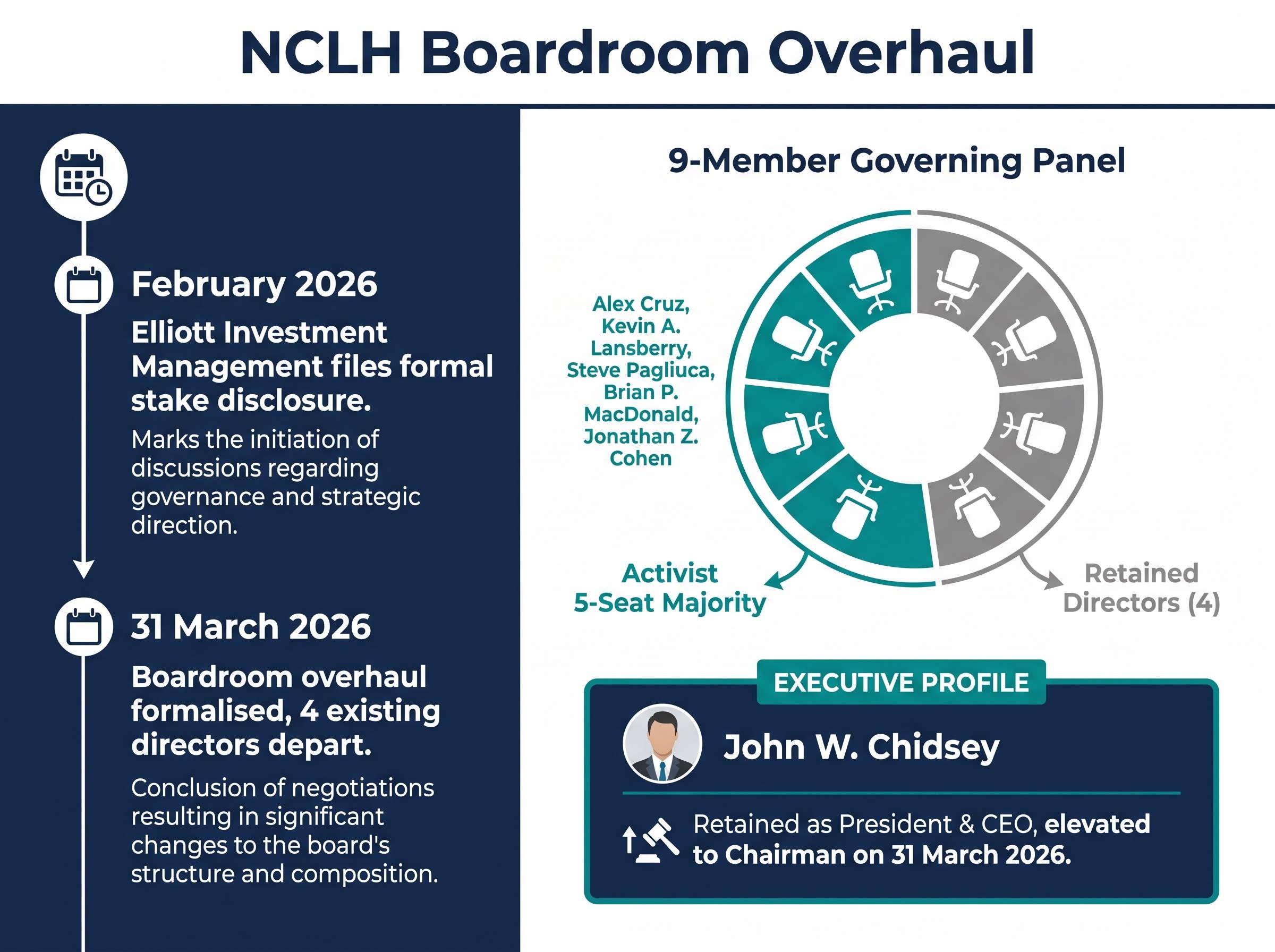

Elliott Investment Management executed this exact strategy, filing a formal stake disclosure in February 2026 that initiated the hostile intervention process. To avoid a highly public and expensive proxy fight, companies often sign a “cooperation agreement” that grants the activist immediate boardroom representation. This mechanism bypasses traditional shareholder voting cycles, granting the instigating firm direct oversight of executive decisions.

A recent Harvard Law School governance review notes that these rapid settlements have become the dominant corporate strategy for avoiding protracted public battles over company control.

Following the agreement, activists typically advocate for specific turnaround measures designed to boost near-term cash flow. The primary strategic modifications demanded in this specific intervention include:

Reduced operational outlays to improve baseline profit margins and free cash flow generation. Upgraded marketing and promotional tactics to drive organic revenue growth across the fleet. * Enhanced passenger accommodations designed to increase per-ticket pricing power and onboard spending.

Restructuring the Helm: New Directors and Executive Continuity

The boardroom overhaul formalised on 31 March 2026 demonstrates the tactical balance between injecting fresh operational expertise and maintaining executive preservation. According to reports, the March cooperation agreement resulted in the immediate departure of four existing directors, making way for a slate of highly credentialed replacements. Crucially, the activist firm successfully secured a five-seat majority on the newly expanded nine-member governing panel.

The NCLH March 2026 Form 8-K filing outlines the precise terms of this boardroom transition, cementing the legally binding governance restructuring between the cruise operator and the activist fund.

The pedigree of the incoming independent directors signals a sharp pivot toward stringent financial oversight and complex operational logistics. The newly appointed board members include:

- Alex Cruz, former Chairman and CEO of British Airways, now serving as Lead Independent Director.

- Kevin A. Lansberry, former Executive Vice President and CFO of Disney Experiences.

- Steve Pagliuca, former Managing Partner and Co-Chairman of Bain Capital.

- Brian P. MacDonald, President and CEO of CDK Global.

- Jonathan Z. Cohen, Founder, CEO, and President of Hepco Capital Management LLC.

Aligning Leadership Incentives

Despite the sweeping board changes, the activist coalition chose to retain President and CEO John W. Chidsey. The board elevated Chidsey to Chairman on March 31, 2026, pairing this promotion with a newly structured employment and equity award agreement.

This new contract relies heavily on performance-based equity compensation, directly tethering the chief executive’s personal wealth to measurable shareholder returns. Specific granular operational adjustments have not yet been publicly released by executive leadership. The newly constituted board is currently prioritising broad structural realignment before announcing detailed cost-cutting measures to the broader market.

Stagnating Yields: The Operational Challenge Ahead

Beneath the boardroom drama, surface-level revenue growth masks the stagnant per-passenger yield metrics that expose the underlying business flaws. According to company data, the operator recorded total proceeds of $9.8 billion in 2025, representing a 3.8 percent growth when excluding exchange rate impacts. However, passenger capacity utilisation simultaneously dropped over the same operational period.

This inverse relationship between top-line revenue and capacity utilisation underscores the absolute urgency of the board overhaul. According to company reports, earnings per available daily passenger capacity landed at $301.52, which represented a 2.4 percent expansion last year but is currently flatlining. The most pressing issue facing the new governing panel is the concerning projection of zero growth in per-passenger profitability for the current fiscal year.

“As NCLH’s largest investor, we see the potential for significant value creation ahead under John’s leadership, and we believe the experience and credibility of this newly appointed Board will help restore investor confidence and return the Company to best-in-class financial performance,” stated Elliott partners John Pike and Bobby Xu on 27 March 2026.

Retail investors must monitor these specific utilisation metrics in upcoming quarterly filings. Reversing the yield stagnation remains the only mathematical pathway to driving the stock price upward and fulfilling the activist’s mandate.

For investors exploring how fleet maintenance costs impact profitability, our detailed coverage of maritime operator capital structures examines the severe margin differences between asset-heavy passenger vessels and capital-light marine service providers.

Wall Street’s Verdict versus Activist Ambition

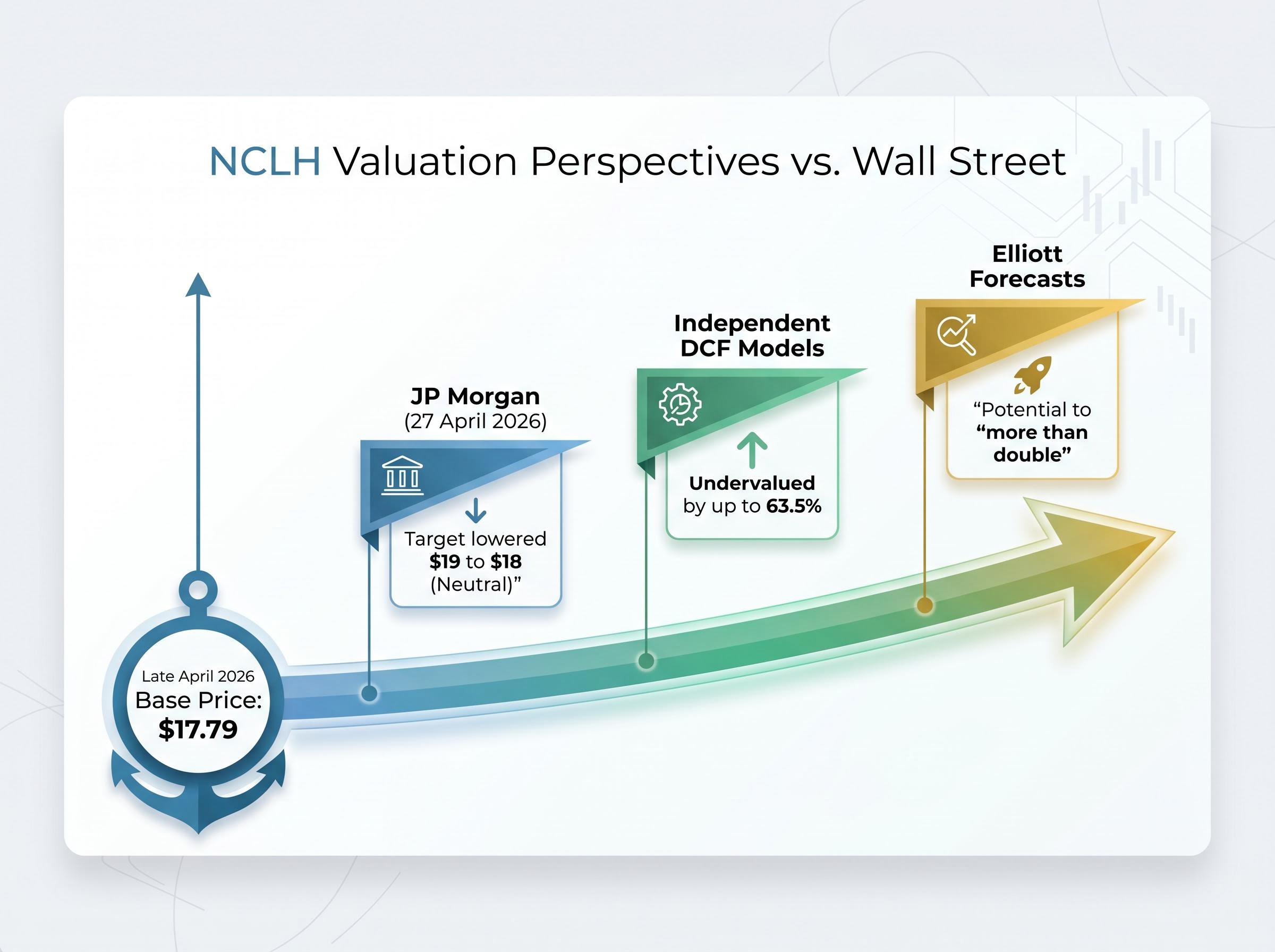

A palpable tension exists between Elliott’s massive upside projections and Wall Street’s cautious downgrade of the maritime operator. Internal forecasts from the activist firm suggest the stock has the potential to “more than double” from its recent trading levels. Conversely, major financial institutions offer a far more tepid reading of the current market positioning, demanding proof of execution before upgrading the equity.

The broader market is clearly waiting for concrete cost-cutting measures rather than simply reacting to executive personnel announcements.

Institutional Projections and Target Prices

Banking analysts are actively hedging their bets on the cruise line’s turnaround potential. JP Morgan maintained a “Neutral” rating and actively lowered its price target from $19 to $18 as of 27 April 2026. Wolfe Research similarly reiterated its current rating, refusing to upgrade the stock based on governance changes alone.

Conversely, mathematical models suggest the stock might still be fundamentally mispriced despite the recent institutional caution. Independent Discounted Cash Flow (DCF) models indicate the equity may be undervalued by as much as 63.5 percent. This stark disconnect between institutional hesitation and baseline technical valuation models leaves investors weighing proven historical underperformance against massive theoretical upside.

Charting a New Course for Shareholder Value

The core conflict defining Norwegian Cruise Line Holdings remains the gap between its premium peer valuation and its consistently lagging operational execution. Securing a five-seat majority on the governing panel represents only the first phase of this highly public intervention. The actual mechanical work of structurally reforming fleet operations and restoring lost pricing power lies entirely ahead of the new board.

While some transport operators choose the path of divesting discretionary tourism assets to reduce debt, the newly constituted Norwegian Cruise Line board must instead extract higher margins from their existing capital-heavy fleet.

With the stock price hovering near $17.79 in late April 2026, the mandate to restore investor confidence requires flawless, immediate execution. Investors should meticulously monitor upcoming quarterly reports for specific cost-reduction initiatives, focusing entirely on improvements in per-passenger yields.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.