Domino’s Falls 9.6% to 52-Week Low After Q1 Miss on All Metrics

15 hrs ago

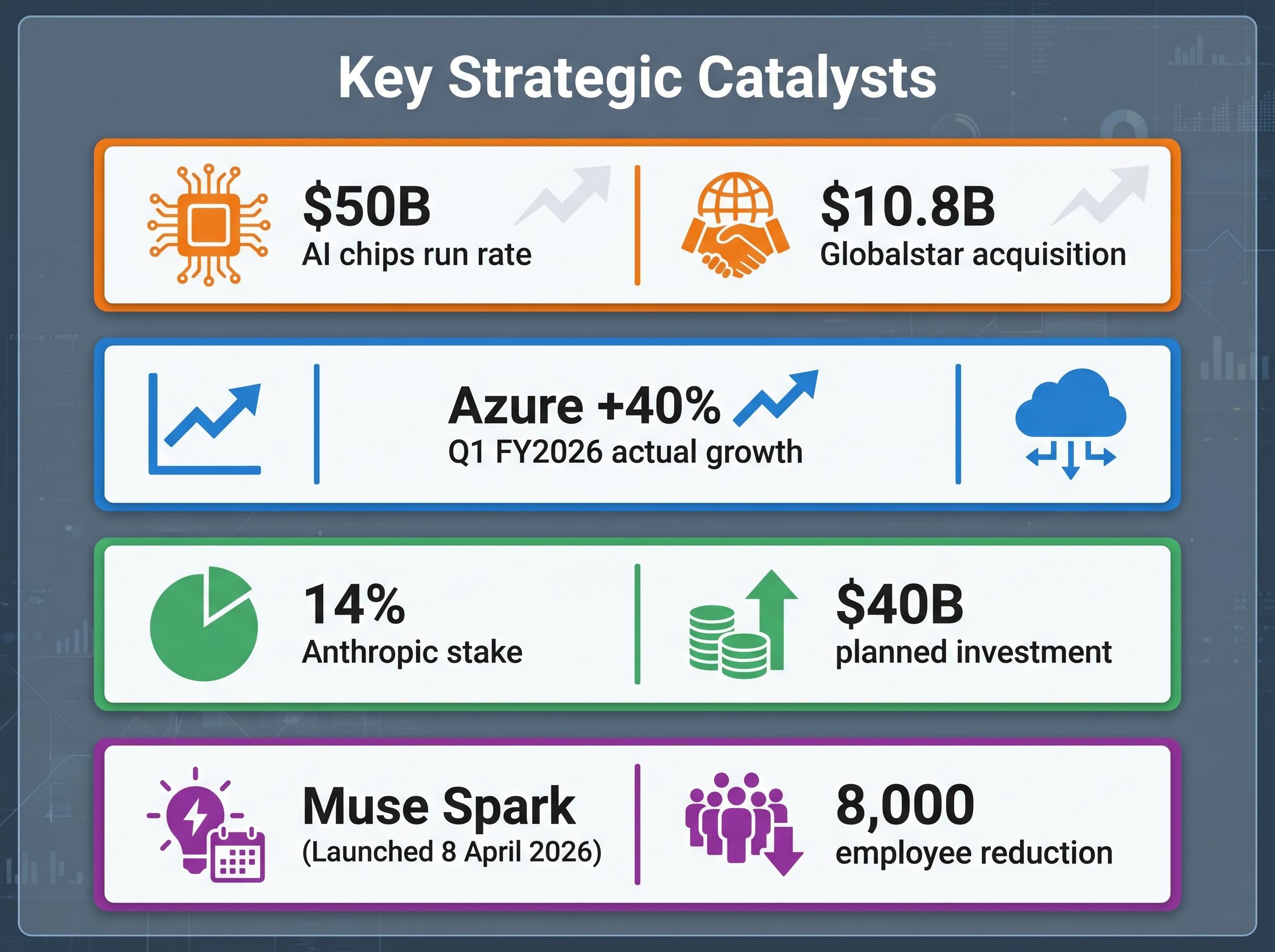

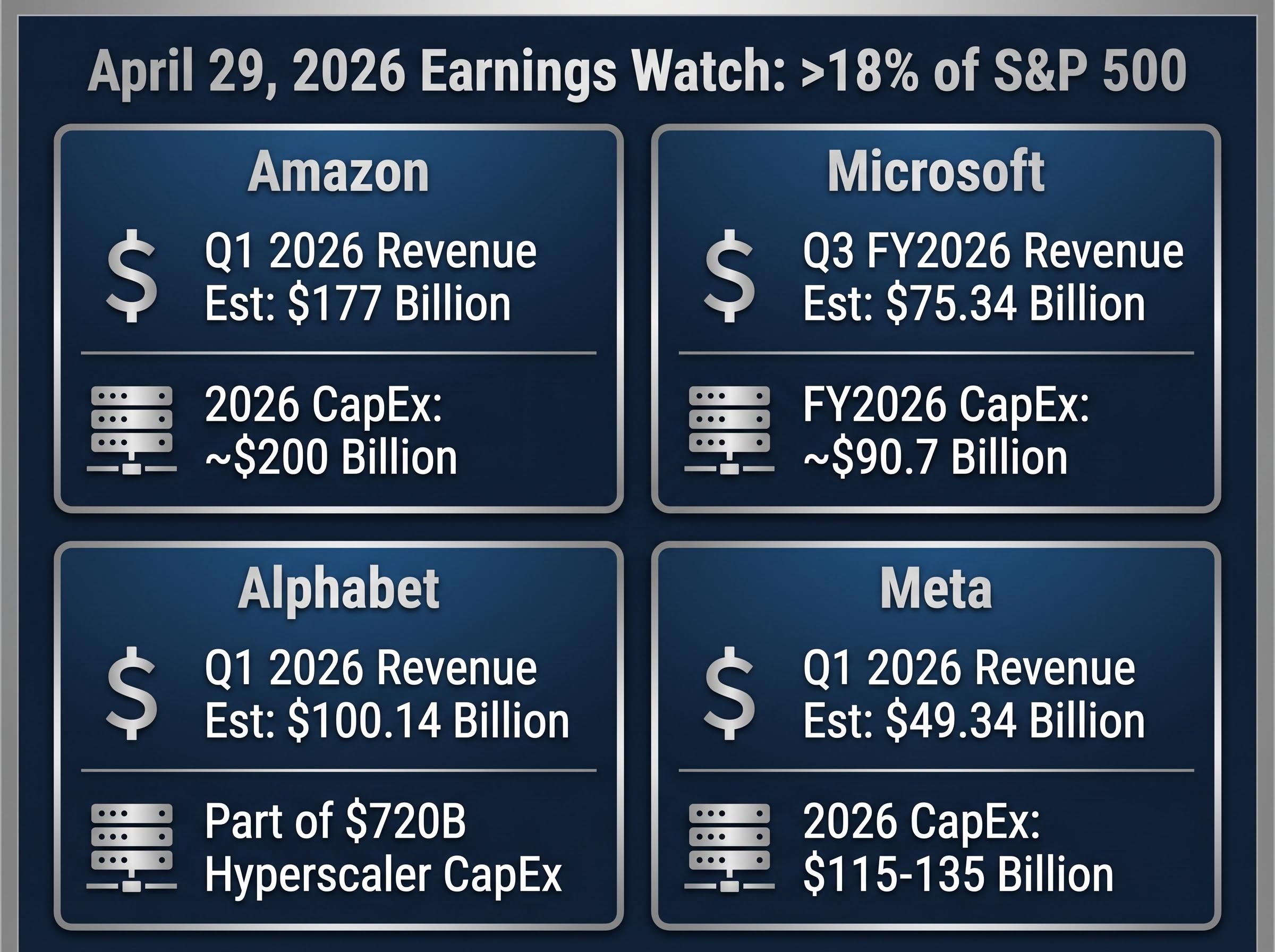

“`json { “fact_checked_full_article”: “Four companies worth more than 18% of the S&P 500 will report earnings after the close on 29 April 2026, making Wednesday the most consequential single evening of the current earnings season. Alphabet, Meta, Amazon, and Microsoft are all releasing results simultaneously, in a week where US equity benchmarks have pushed to record levels after months of AI-driven volatility and geopolitical disruption. Each company faces the same structural tension: artificial intelligence infrastructure spending is accelerating faster than near-term earnings can absorb, reshaping what good results look like for mega-cap tech. This preview breaks down consensus estimates, the narrative catalysts unique to each company, and the specific signals investors should monitor when results land Wednesday night.\n\n## Why Wednesday’s results carry unusual market weight\n\nFour Magnificent Seven members reporting on a single evening is not routine. Their combined weighting in the S&P 500 exceeds 18%, which means any surprise, positive or negative, will ripple well beyond the individual stock price and into index-level moves across ETFs, futures, and options positioning.\n\nThe companies reporting on 29 April:\n\n- Alphabet (Q1 2026, calendar Jan-Mar)\n- Meta (Q1 2026, calendar Jan-Mar)\n- Amazon (Q1 2026, calendar Jan-Mar)\n- Microsoft (Q3 FY2026, Jan-Mar)\n\nThe backdrop makes the stakes sharper. The S&P 500 and Nasdaq Composite have recently pushed to record highs despite a volatile first quarter shaped by AI equity rotation, geopolitical pressure from the Iran conflict, and rising energy costs. Wednesday’s results will test whether that optimism is durable or whether the market has moved ahead of the earnings base supporting it.\n\n## The AI capex tension redefining earnings quality for mega-cap tech\n\nBefore interpreting any of Wednesday’s headline numbers, investors need to understand the structural force distorting them. All four companies are committing to AI infrastructure buildout at a scale that inflates capital expenditure, compresses near-term earnings per share, and in some segments pushes cost of goods sold higher than revenue growth.\n\n> The hyperscaler group (Microsoft, Alphabet, Meta, Amazon, and Oracle) is projected to spend approximately $720 billion in combined capital expenditure in 2026.\n\nThat figure reframes the traditional earnings quality lens. Strong revenue growth paired with muted EPS growth is not necessarily a warning sign for these companies; it reflects a deliberate, multi-year strategic choice. Revenue growth rate, cloud services acceleration, and AI monetisation metrics are better near-term performance signals than the EPS headline alone.\n\n

| Company | 2025 CapEx (Est.) | 2026 CapEx (Est./Committed) | Q1 2026 EPS Growth (YoY) |

|---|---|---|---|

| Alphabet | Not disclosed | Part of $720B collective | ~+7% |

| Meta | ~$72.2B | $115-135B | ~+10% |

| Amazon | Not disclosed | ~$200B | Consensus not broken out |

| Microsoft | Not disclosed | ~$90.7B | ~+11% |

\n

\n\nThe gap between revenue acceleration and EPS compression is the defining feature of this earnings cycle for mega-cap tech. Investors applying a conventional earnings quality filter risk misreading the results.\n\n## Amazon and Microsoft: management credibility on trial\n\nBoth companies have made commitments large enough to spook their own shareholders before results were in. Wednesday’s earnings calls are the moment each management team either validates that confidence or deepens the concern.\n\n### Amazon: the $200 billion bet and what Jassy says it will return\n\nAmazon’s Q1 2026 consensus sits at approximately $177 billion in revenue (+14% year-over-year) with EPS of approximately $1.65 (+4% YoY). The revenue line is healthy. The EPS figure reflects the weight of a $200 billion capital expenditure commitment for 2026, the largest single-year infrastructure spend in corporate history.\n\n> In his annual shareholder letter, CEO Andy Jassy characterised the post-capex sell-off as unwarranted, arguing that customer commitments cover nearly the full 2026 capex plan and that investors were underestimating the returns already visible in the pipeline.\n\nJassy pointed to Amazon’s AI chips business reaching a $50 billion annualised revenue run rate, growing at more than 100% year-over-year, as evidence that the spending is converting into revenue faster than the market credits.\n\n- Watch for: AWS AI revenue breakout detail on the call\n- Watch for: Updated customer commitment coverage for the remaining 2026 capex\n- Watch for: Commentary on the $10.8 billion Globalstar acquisition (satellite-to-cellular, targeting a 2028 launch), which signals Amazon’s ambitions extend well beyond cloud\n- Watch for: Free cash flow guidance given the capex drag\n\n### Microsoft: Copilot monetisation and the OpenAI partnership reset\n\nMicrosoft reports Q3 FY2026 with consensus at $75.34 billion in revenue (+15% YoY) and EPS of $3.66 (+11% YoY). The stock is down more than 20% year-to-date, and the forward price-to-earnings ratio has compressed to approximately 22.12x, well below its historical average of roughly 30x. The market is pricing in doubt.\n\nThe most important signal is Copilot. Bloomberg has reported that Microsoft’s standalone Copilot product is meeting aggressive internal sales targets, a development that, if confirmed on the call, could begin to address the \”software obsolescence\” debate: whether AI agents replace existing software revenue or layer on top of it.\n\nThe revised OpenAI partnership adds a second catalyst. Microsoft placed a ceiling on payments received from OpenAI and relinquished exclusive product licensing rights. Investors should listen for management commentary on how the revised revenue-sharing structure affects forward Azure economics.\n\n- Watch for: Copilot standalone revenue or adoption metrics\n- Watch for: Azure growth rate versus the +40% Q1 FY2026 actual (deceleration is priced in; the magnitude matters)\n- Watch for: Management framing of the revised OpenAI terms and their margin impact\n- Watch for: Updated FY2026 capex guidance (currently approximately $90.7 billion, rising to approximately $100 billion in FY2027)\n\n## Alphabet and Meta: growth stories complicated by big spending commitments\n\nBoth companies are delivering strong revenue growth that the capex surge partially obscures. The gap between topline momentum and bottom-line compression is the story in each case, but the catalysts that could close it are different.\n\n### Alphabet: Anthropic stake and TPU strategy in focus\n\nAlphabet’s Q1 2026 consensus projects revenue of approximately $100.14 billion (+13% YoY) alongside EPS of approximately $2.67 (-5% YoY). The revenue growth is among the strongest in the group. The EPS decline is the cost of staying competitive in AI infrastructure.\n\nWhat makes Alphabet’s story richer than the headline numbers is the Anthropic position. Alphabet holds a reported 14% ownership stake, with a planned additional $40 billion investment, and a potential Anthropic initial public offering (an IPO is a company’s first sale of shares to the public) could arrive in 2026. That optionality does not appear in the Q1 EPS figure but would materially change the valuation calculus if it progresses.\n\nSeparately, Alphabet’s new five-year TPU development agreement with Broadcom signals longer-term positioning in the custom chip race powering Google Cloud.\n\n- Watch for: Any management commentary on Anthropic IPO timeline or valuation\n- Watch for: Google Cloud growth rate and AI services contribution\n- Watch for: Updated capex guidance and return-on-investment framing\n\n### Meta: Muse Spark momentum and the cost of rapid scaling\n\nMeta’s consensus projects Q1 2026 revenue of approximately $49.34 billion (+22% YoY) and EPS of approximately $6.65 (+3% YoY). That contrast, the fastest revenue growth among the four companies yet nearly flat earnings growth, is the capex story made concrete. The $115-135 billion 2026 capex guidance explains the compression.\n\nTwo variables could shift the narrative. Muse Spark, Meta’s multimodal AI model launched on 8 April 2026, now powers AI assistants across WhatsApp and Instagram. Any adoption metrics disclosed on the call would be the first quantitative evidence of Meta’s AI product monetisation trajectory.\n\nThe second variable is cost discipline. Meta announced a workforce reduction of approximately 8,000 employees, roughly 10% of total headcount, in April. The timeline and expected savings run rate could meaningfully alter the forward earnings picture.\n\nRetail sentiment on Meta is notably negative despite the company showing the fastest consensus revenue growth among the four. That sets up an asymmetric reaction if results exceed expectations.\n\n- Watch for: Muse Spark adoption or engagement metrics\n- Watch for: Workforce reduction savings timeline and magnitude\n- Watch for: Management guidance on when capex growth rate moderates\n- Watch for: Reality Labs loss rate and any signs of cost containment\n\n## Five signals that will define how markets react Wednesday night\n\nThe individual company details matter, but five signals will carry the most weight across all four reports:\n\n1. AI capex-to-revenue conversion timeline. Every management team will be asked when the current spending cycle begins producing measurable earnings acceleration. The specificity (or vagueness) of the answers will set the tone for mega-cap tech positioning through to the end of Q2.\n\n2. Azure growth trajectory. Microsoft reported +40% Azure growth in Q1 FY2026. Full-year FY2026 consensus implies approximately +36%, meaning deceleration is expected. Whether the Q3 figure holds above +35% or breaks below it will signal whether Microsoft’s AI cloud premium is compressing.\n\n3. Amazon AWS AI revenue breakout. The $50 billion annualised run rate growing at more than 100% is the proof point. If Amazon provides a formal segment breakout, it becomes the clearest data point on AI services monetisation across any hyperscaler.\n\n4. Alphabet’s Anthropic commentary. Any guidance on IPO timeline, valuation framing, or strategic rationale for the additional $40 billion investment carries immediate implications for how investors value Alphabet’s non-operating assets.\n\n5. Meta’s sentiment mismatch. Consensus projects +22% revenue growth but only +3% EPS growth, and retail sentiment is bearish. If results beat on both lines, the asymmetric setup could produce the largest single-stock after-hours move of the four.\n\n## Conclusion\n\nFor all four companies reporting Wednesday, the gap between revenue growth and earnings-per-share growth is not a malfunction. It reflects a deliberate, multi-year AI infrastructure bet where returns are designed to arrive on a longer timeline than a single quarter can capture. Investors who understand that distinction will be better positioned to interpret the results in real time rather than reacting to headline beats or misses.\n\nNo preview can predict outcomes, but the frameworks and watchpoints outlined above provide the analytical context to evaluate what Wednesday’s numbers and management commentary actually signal. These results are also the first major data point in a broader sequence of AI spend validation tests: Apple reports in early May, and Nvidia reports on 20 May 2026.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.\n\n—” } “`

Nvidia’s earnings on 20 May 2026 represent the next major validation point for the AI infrastructure thesis after Wednesday’s results: the company projects a $1 trillion revenue opportunity from its Blackwell and Vera Rubin product families over 2026-2027, meaning the hyperscaler capex commitments announced Wednesday will translate directly into Nvidia demand forecasts when it reports three weeks later.

The AI capex-to-revenue conversion timeline across the hyperscaler group is broadly projected to inflect in the late 2026 to 2027 period, when inference workloads are expected to overtake training as the dominant compute demand and drive a step-change in revenue utilisation per dollar of installed capacity.

Microsoft’s compressed forward valuation, with the stock trading at approximately 22x forward earnings against a historical average near 30x and a PEG ratio of 0.92, has created one of the widest gaps between current price and consensus analyst targets among large-cap technology stocks heading into this earnings report.

For readers wanting to situate Wednesday’s reports within the broader earnings season context for mega-cap tech, our dedicated guide to the week’s full earnings landscape covers the Azure growth rate benchmark of 37-38% in constant currency that analysts treat as the key AI adoption proxy, the macro headwinds from rising inflation expectations, and the Q2 and Q3 2026 S&P 500 growth rate projections that will set the bar management guidance is measured against.

Inc. Magazine coverage of Alphabet’s $40 billion Anthropic investment terms, drawing on reporting from The Wall Street Journal and CNBC, details how the deal was structured ahead of a widely anticipated Anthropic IPO and contextualises why Alphabet’s 14% ownership stake carries valuation implications that go well beyond the Q1 earnings headline.

Motley Fool analysis of hyperscaler AI capital expenditure projections for 2026 places the combined figure at approximately $720 billion across Meta, Amazon, Microsoft, Alphabet, and Oracle, a concentration of infrastructure spending with no modern precedent in corporate history.

The Magnificent Seven are a group of the largest US technology companies whose earnings reports carry outsized market weight because their combined S&P 500 weighting exceeds 18%, meaning any significant beat or miss ripples across ETFs, futures, and broader index positioning.

Alphabet, Meta, Amazon, and Microsoft all report after market close on 29 April 2026, covering Q1 2026 results for Alphabet, Meta, and Amazon, and Q3 FY2026 results for Microsoft.

The hyperscaler group including Microsoft, Alphabet, Meta, Amazon, and Oracle is projected to spend approximately $720 billion in combined capital expenditure in 2026, inflating costs faster than near-term revenue can absorb them and suppressing EPS growth even as revenue grows strongly.

The most important signals from Microsoft's call are Copilot standalone adoption metrics, the Azure growth rate relative to the prior quarter's 40% figure, and management commentary on how the revised OpenAI partnership terms affect forward Azure economics and margins.

Meta is projected to post the fastest revenue growth among the four companies at approximately 22% year over year, yet EPS growth of only around 3%, a gap explained by its $115-135 billion 2026 capital expenditure commitment, which creates an asymmetric setup where a beat on both lines could trigger a larger-than-average after-hours move.