Record Highs Are Not the Risk Most Investors Think They Are

5 hrs ago

Wall Street enters one of its most consequential weeks of 2026 with Big Tech earnings poised to either validate or challenge the year’s dominant investment thesis: that artificial intelligence spending is translating into measurable revenue acceleration. On 27 April 2026, Citi analyst Heath Terry offered his pre-earnings read on the major technology names, projecting revenue expansion while characterising capital expenditure shifts as modest rather than structural. Hours later, Nancy Tengler of Laffer Tengler Investments reaffirmed a sustained bullish stance on the technology sector during a CNBC appearance. Both views arrive as Microsoft, Meta, and Amazon prepare to report on 29 April, with Apple following on 30 April. What follows synthesises the analyst expectations, company-level consensus estimates, and the capital expenditure debate framing what investors should watch across this week’s reports.

Terry’s thesis, delivered on CNBC approximately three hours before market close on 27 April, offered a specific baseline: revenue growth is expected across the major technology names, and capital expenditure adjustments will be incremental rather than structural.

Citi’s Pre-Earnings View (Heath Terry, 27 April 2026): Revenue expansion is projected across Big Tech, with capital expenditure changes characterised as modest, not structural shifts.

That framing carries weight because of what investors have been debating for months. The question hanging over every AI-exposed name is whether infrastructure spending is approaching an inflection point that could compress near-term margins. Meta’s 1 GW AI chip deal with Broadcom, announced on 14 April 2026, illustrated the scale of current commitments. When a bulge-bracket analyst then signals that these commitments are not accelerating beyond expectations, it recalibrates how the market is likely to receive guidance commentary later this week.

The tension, however, is real. Specific forward capex figures for Microsoft, Alphabet, Meta, and Amazon have not been confirmed ahead of earnings, meaning management guidance on calls will be the variable that either validates or complicates Terry’s read. His view sets the bar. Wednesday and Thursday will determine whether it holds.

Most investors understand that earnings season matters. Fewer appreciate why Big Tech earnings specifically carry disproportionate weight relative to any other sector grouping.

The Magnificent Seven collectively represent a substantial share of S&P 500 market capitalisation. When these companies report, the results are not confined to individual stock moves; they transmit directly to index-level performance. A beat or miss from Microsoft or Amazon moves portfolios that hold broad index funds, not just portfolios concentrated in technology.

Within that dynamic, the distinction between earnings-per-share beats and revenue growth matters more than usual this cycle. An EPS beat can reflect cost discipline or share buybacks. Revenue acceleration, by contrast, is the signal that AI workloads are generating real commercial demand, which is the thesis the market is pricing.

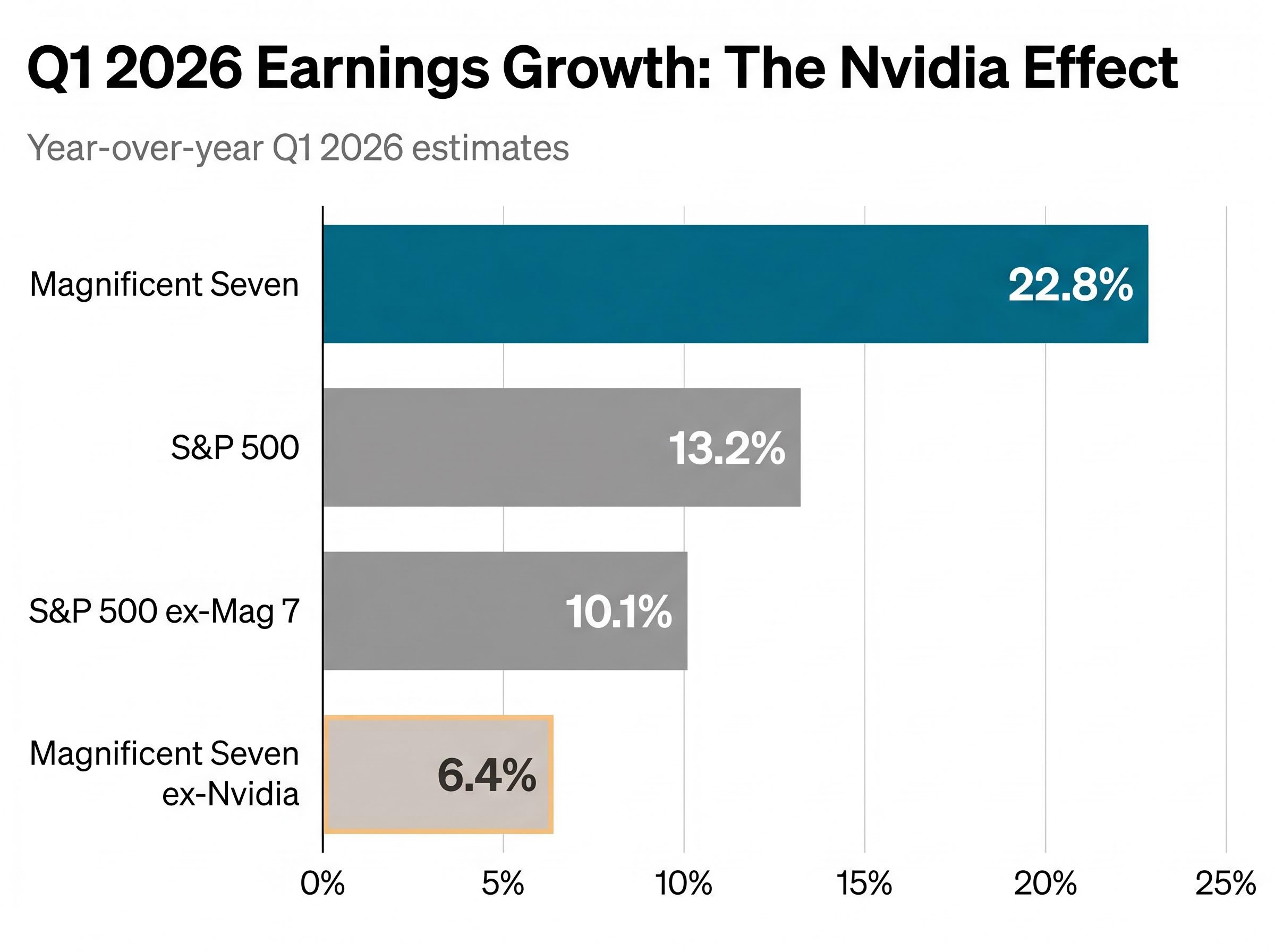

The current cycle carries unusual optimism. 60 S&P 500 companies issued positive EPS guidance for Q1 2026, well above the five-year average of 44 and the ten-year average of 40. The headline growth numbers reinforce that sentiment:

That last number is the most telling. Strip out Nvidia, and the remaining six Magnificent Seven names are growing earnings slower than the rest of the S&P 500.

That concentration dynamic is part of what makes the current setup unusual: a Magnificent Seven valuation analysis published earlier this month found that strip out Nvidia and only Alphabet, at 17x forward earnings, offers a cheap valuation within the group, while Tesla’s 145x forward P/E sits at the other extreme, earning a Sell rating from covering analysts despite strong retail interest.

It reframes the entire narrative. The group’s headline outperformance is concentrated in a single company that does not even report until 20 May. This week’s results will reveal whether the other names can carry their own weight.

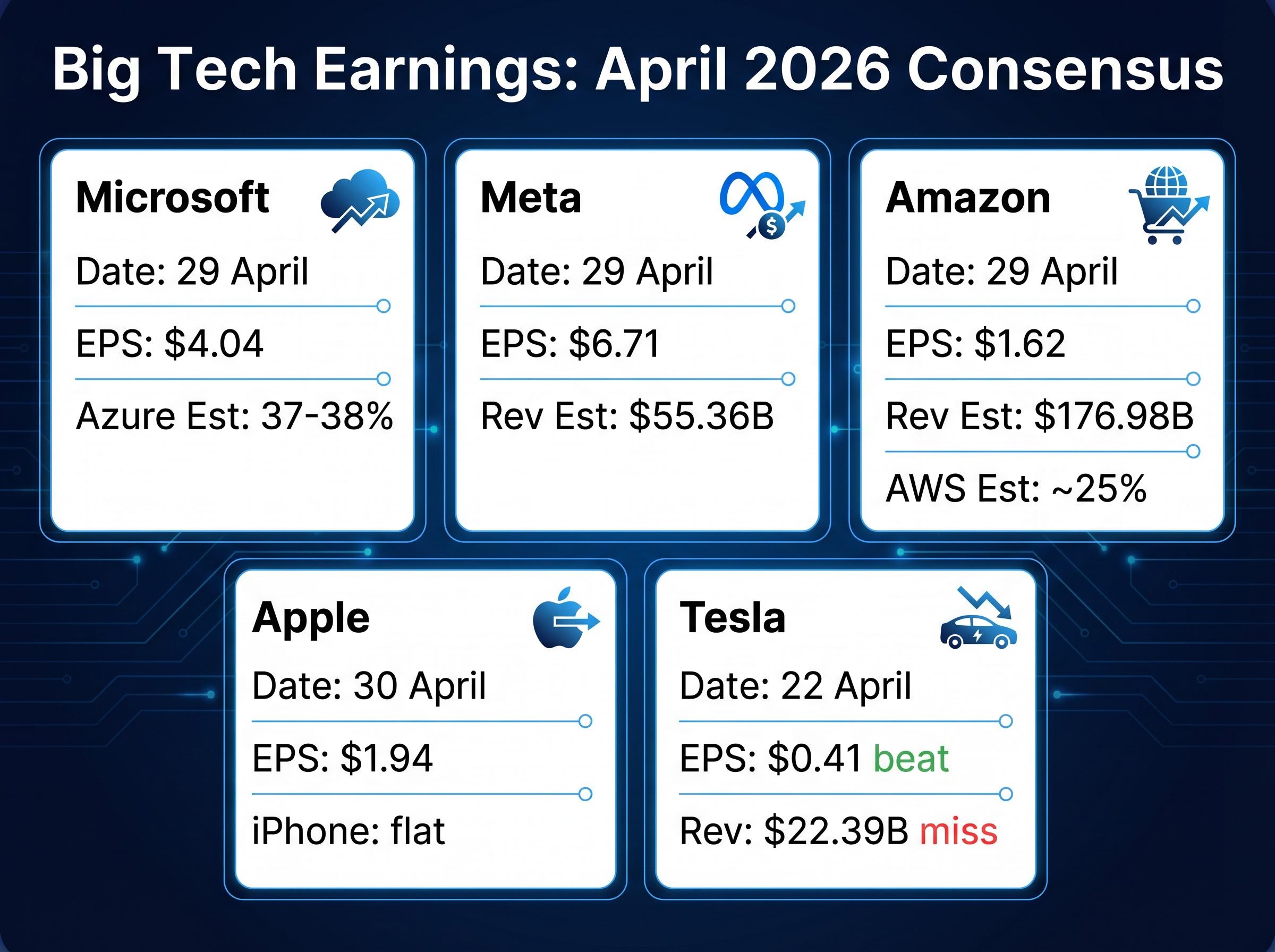

The table below captures the consensus expectations for each company reporting this week, alongside the single metric most likely to drive the stock reaction.

| Company | Report Date | Consensus EPS | Key Revenue Metric | Primary Watch Item |

|---|---|---|---|---|

| Microsoft | 29 April | $4.04 | Azure growth est. 37-38% (constant currency) | AI workload guidance |

| Meta | 29 April | $6.71 | Revenue est. $55.36B | AI ROI and ad pricing |

| Amazon | 29 April | $1.62 | Revenue est. $176.98B; AWS growth est. ~25% YoY | AWS reacceleration |

| Apple | 30 April | $1.94 | iPhone sales expected flat YoY | Tariff exposure commentary |

| Tesla (reported) | 22 April | $0.41 (beat vs. $0.37 est.) | Revenue $22.39B (miss vs. $22.64B) | Mixed result; EPS beat, revenue miss |

Of all the figures in the table, Microsoft Azure’s 37-38% constant currency growth estimate may be the single most consequential metric of the week. Azure has become the primary proxy for enterprise AI adoption. Microsoft’s AI business is projected to reach $25 billion in fiscal 2026 revenue, and the Azure growth rate is the clearest measure of whether that trajectory is holding. If Azure clears the bar, it validates the spending cycle. If it falls short, every other AI-adjacent name will feel the pressure.

For investors wanting the complete pre-earnings picture on the most consequential report of the week, our full explainer on Microsoft’s Azure earnings setup covers Oppenheimer’s $115 price target cut, the 42-of-45 analyst Buy consensus, Copilot seat expansion to 15 million paid users (up 160% year-over-year), and the specific Azure metrics that will determine whether the bull or bear case closes out April in front.

Terry’s pre-earnings thesis, that capex changes will be modest, establishes a baseline. The harder question is whether management teams will use this week’s earnings calls to confirm that baseline or signal something different.

The stakes are specific to this cycle. Investors are trying to determine whether the AI infrastructure build-out is peaking, plateauing, or accelerating. Reported earnings tell the market what happened last quarter. Capex guidance tells the market what management expects to happen next. In an investment cycle of this magnitude, the forward view carries more weight than the backward look.

Meta’s 1 GW AI chip deal with Broadcom illustrates the scale involved. That single commitment, announced on 14 April 2026, represents sustained nine-figure-plus infrastructure investment from one company alone. Across the sector, S&P 500 IT revenue is projected to surge 45%, the highest sectoral growth figure in the current cycle.

AI infrastructure spending translating into cloud revenue is the central question for both Azure and AWS this week: S&P 500 IT sector revenue is projected to grow 45% in the current cycle, the highest sectoral growth rate on record, yet 72% of CIOs report barely breaking even on AI deployments, which is precisely why the reacceleration signals from Azure and AWS will carry more interpretive weight than the headline growth percentages suggest.

S&P 500 IT sector revenue is projected to grow 45%, the highest sectoral growth rate of the current earnings cycle.

Five specific items will drive stock reactions beyond headline EPS numbers:

What management says about 2026 capex trajectories on Wednesday and Thursday calls will matter more to long-term investors than whether EPS cleared consensus by a few cents. Terry’s modest-adjustment thesis is the benchmark. Actual guidance will determine whether it holds.

Nancy Tengler, chief executive and chief investment officer at Laffer Tengler Investments, reaffirmed a sustained bullish position on the technology sector during an appearance on CNBC’s “The Exchange” on 27 April 2026. The stance reflects institutional conviction that the earnings trajectory and AI monetisation thesis remain intact.

That conviction, however, exists alongside macro crosscurrents that complicate the clean bullish narrative:

These data points do not invalidate the bullish tech thesis, but they define the environment in which it must deliver. Corporate earnings optimism and consumer-level macro stress are running in parallel, and the tension between them is part of the investment picture.

Forward earnings estimates suggest Wall Street’s optimism extends well beyond this single reporting window. The S&P 500 consensus projects 19.1% earnings growth in Q2 2026 and 21.2% in Q3 2026. Revenue growth is on track for 9.7%, the highest since Q3 2022. The trajectory is positive. The macro friction is real.

This week’s Big Tech reports arrive with Citi projecting revenue growth and limited capex surprises, Laffer Tengler holding a sustained bullish tech position, and consensus estimates that set a high but achievable bar for Microsoft, Meta, Amazon, and Apple. The results will reveal whether the AI monetisation thesis is translating into real revenue acceleration across the sector’s largest names.

Three items deserve particular focus: Azure growth relative to the 37-38% constant currency estimate, Meta’s AI return-on-investment signals, and any capex guidance language that contradicts or confirms Terry’s modest-adjustment thesis. Nvidia, the single largest contributor to Magnificent Seven group-level outperformance, does not report until 20 May, meaning this week’s results will not close the AI earnings narrative.

Forward estimates of 19.1% in Q2 and 21.2% in Q3 suggest the market’s optimism extends well beyond this reporting window. For investors following the earnings calls in real time, management commentary around AI spending trajectories may prove more consequential than whether EPS numbers clear consensus by a narrow margin.

Hyperscaler free cash flow trajectory into late 2026 is the metric that will determine whether this week’s guidance prints shift investor positioning: Societe Generale projects free cash flow turning negative by late 2026 before recovering in Q1 2027, and if management teams signal capex acceleration rather than Terry’s projected moderation, that timeline compresses in a direction the market is not currently pricing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including earnings estimates and growth projections, are subject to change based on market developments and company performance.

Consensus estimates project Microsoft EPS of $4.04 with Azure growth of 37-38%, Meta EPS of $6.71 with revenue of $55.36B, Amazon EPS of $1.62 with AWS growth of approximately 25% year-over-year, and Apple EPS of $1.94 with iPhone sales expected flat year-over-year.

The Magnificent Seven collectively represent a substantial share of S&P 500 market capitalisation, meaning beats or misses from companies like Microsoft and Amazon transmit directly to index-level performance and affect portfolios holding broad index funds, not just technology-focused investors.

Azure cloud revenue growth is the single most consequential metric, with consensus expecting 37-38% constant currency growth; Azure has become the primary proxy for enterprise AI adoption, and Microsoft's AI business is projected to reach $25 billion in fiscal 2026 revenue.

On 27 April 2026, Heath Terry projected revenue expansion across major technology names while characterising capital expenditure changes as modest and incremental rather than structural shifts, setting a baseline that Wednesday and Thursday guidance commentary will either confirm or complicate.

Stripping out Nvidia, the remaining six Magnificent Seven companies are projected to grow earnings at just 6.4% in Q1 2026, which actually trails the broader S&P 500 ex-Magnificent Seven figure of 10.1%, revealing that the group's headline outperformance is concentrated in a single company that does not report until 20 May.