Kogan Share Price Surges 15% as Earnings Beat Expectations

4 hrs ago

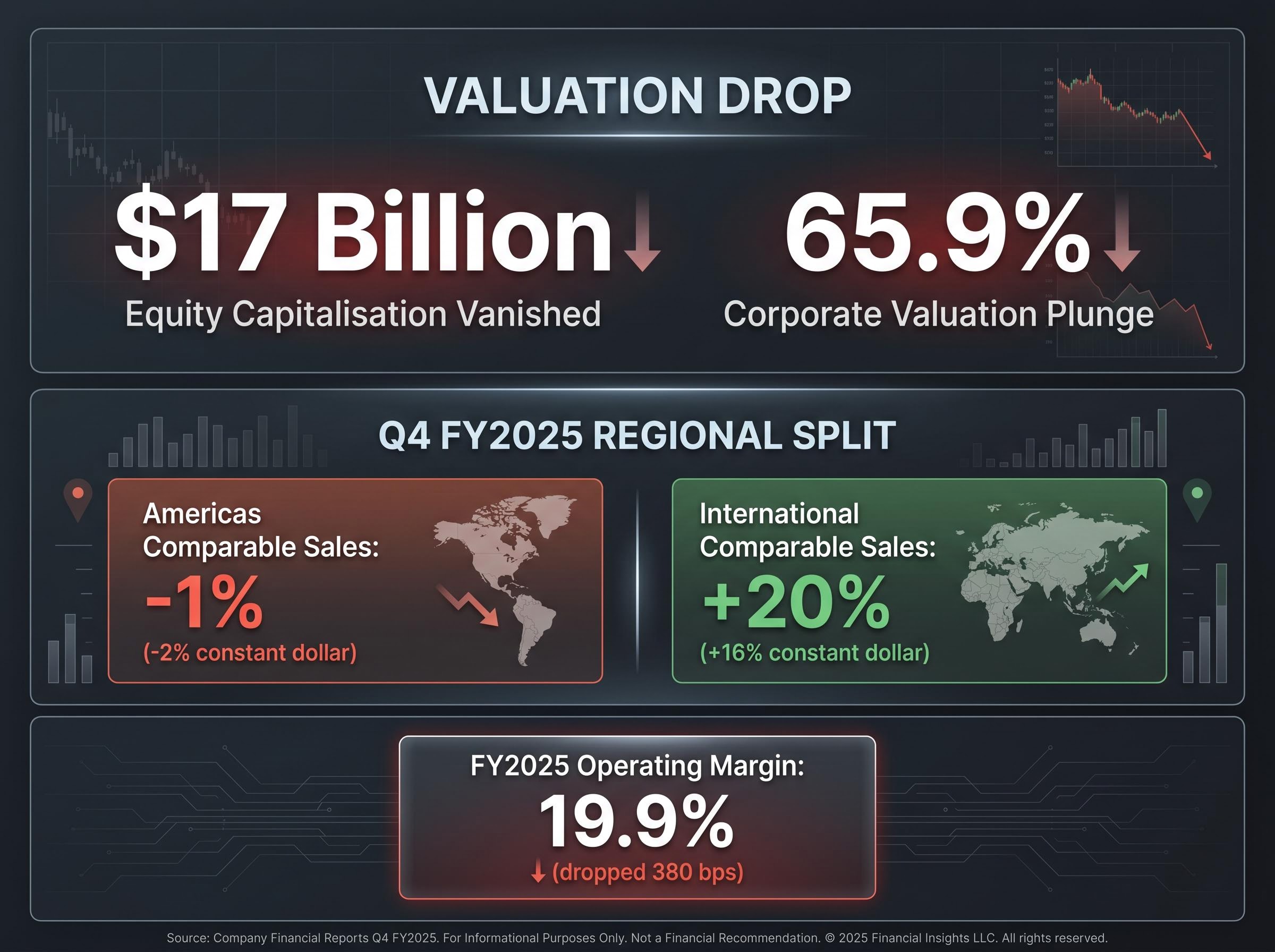

According to market data, roughly $17 billion of equity capitalisation has vanished from Lululemon over the preceding five years. This erosion culminated in a 65.9 percent corporate valuation plunge over an almost two-year timeframe, reflecting a severe market recalibration of the athletic apparel provider.

As of 29 April 2026, the company faces the compounding pressures of stagnant or shrinking North American retail revenue. Simultaneously, a highly publicised Lululemon proxy battle dominates financial headlines, pitting the founder against the current board.

This analysis examines the underlying financial decay driving the market capitalisation wipeout. The following sections investigate how strategic misalignment, controversial partnerships, and boardroom dysfunction have eroded the athletic giant’s premium market position. By triangulating the latest earnings data with the corporate governance dispute, investors can assess the viability of a recovery.

The brand built its legacy on absolute pricing power and premium market positioning. Financial reporting for Fiscal 2025 and the fourth quarter indicates this model is fracturing within its most important geographical market. The reported international growth provides a stark contrast to the severe contraction occurring within the core Americas region.

During Q4 FY2025, Americas comparable sales decreased by 1 percent, or 2 percent on a constant dollar basis.

The full-year results exposed significant margin compression across the entire retail operation. The FY2025 operating margin dropped 380 basis points to 19.9 percent, signalling an inability to maintain historical profitability metrics. This contraction is a company-specific crisis rather than a reflection of macroeconomic pressure.

The official SEC 10-K annual disclosure contextualises these falling profitability metrics, illustrating how ballooning selling and administrative expenses have structurally impaired the bottom line even as the brand attempts to pivot internationally.

Over a 12-month window, the stock has underperformed median competitors. This relative weakness drove the 65.9 percent plunge in overall corporate valuation. Investors require visibility into the exact metrics driving this decay to evaluate forward risk. By isolating the North American sales contraction, the mechanical breakdown of the financial model becomes evident.

| Performance Metric | Q4 FY2025 Results | Full-Year FY2025 Results |

|---|---|---|

| Revenue Growth | 1% increase ($3.6B) | 5% increase ($11.1B) |

| Gross Margin | 54.9% (decreased 550 bps) | 56.6% (decreased 260 bps) |

| Operating Margin | 22.3% (decreased 660 bps) | 19.9% (decreased 380 bps) |

| Americas Comparable Sales | Decreased 1% (2% constant dollar) | Data aggregated in full-year mix |

| International Comparable Sales | Increased 20% (16% constant dollar) | Increased 15% (14% constant dollar) |

The release of Fiscal 2026 forward guidance provided little assurance to institutional investors or retail shareholders. Management projected total revenue growth of merely 2 to 4 percent, targeting $11.35 billion to $11.50 billion for the year. This tepid projection signals that the structural issues in North America will likely persist throughout the coming quarters. Analysts read this muted forecast as an admission that management lacks an immediate catalyst to reverse the regional sales slump.

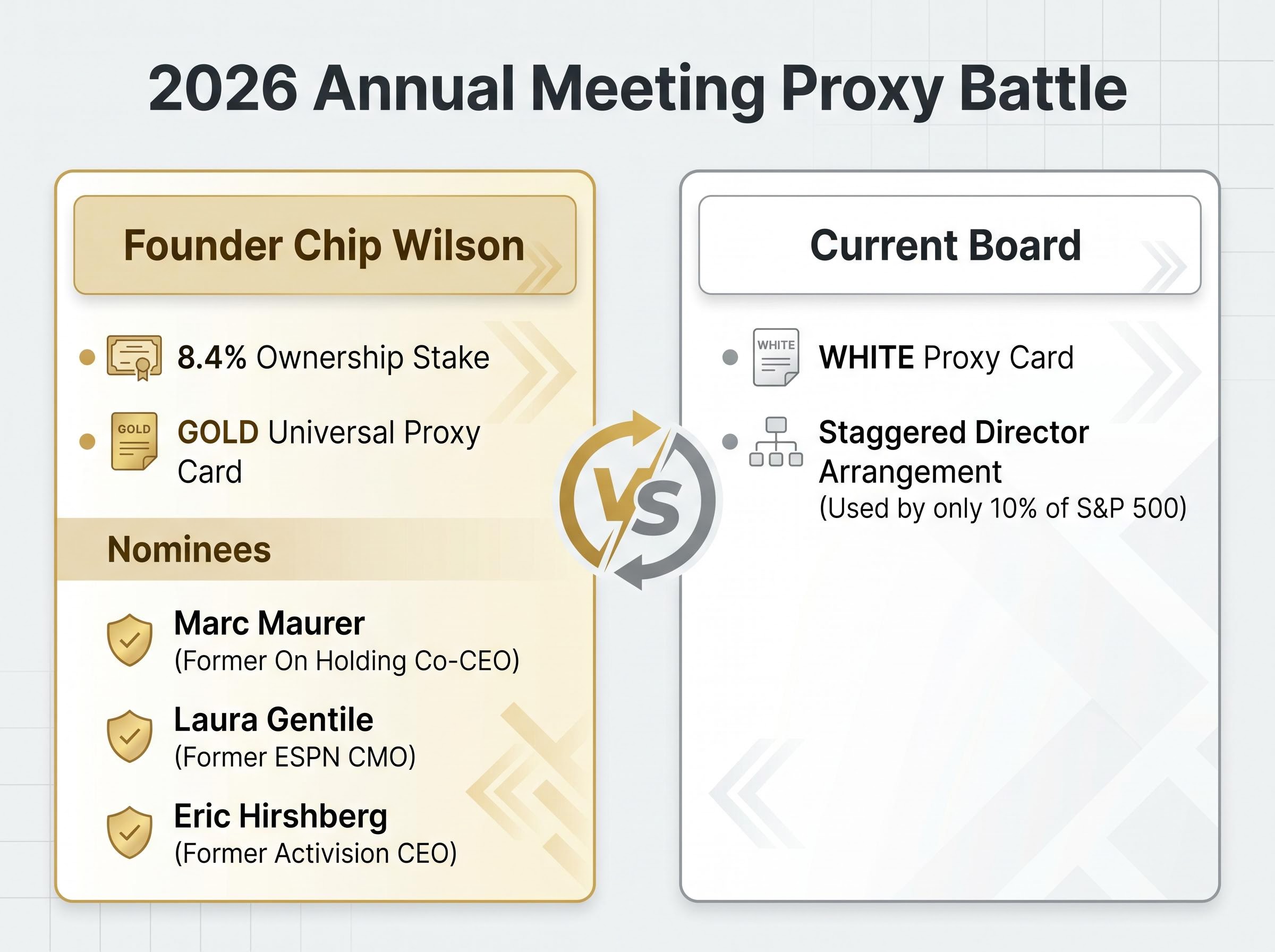

The quantitative deterioration has triggered a direct conflict over corporate control and future strategic direction. Founder Chip Wilson, maintaining an 8.4 percent ownership stake, launched an aggressive campaign to force operational changes from the outside. Wilson is actively nominating three independent directors using a GOLD Universal Proxy Card for the upcoming 2026 annual meeting.

He accused the current board of weak governance, maintaining ties to private equity, and sustaining an outdated staggered director arrangement. According to industry reports, financial analysis indicates that only 10 percent of S&P 500 organisations still use this contested staggered term structure, positioning the board’s defensive posture outside modern governance norms.

Recent Harvard Business School governance research reinforces this shift away from staggered terms, noting that maintaining a classified board significantly limits the ability of shareholders to replace underperforming directors during a single voting cycle.

The board issued a firm defensive response, claiming they engaged in good faith while pushing shareholders toward the WHITE proxy card. Directors also demanded an alleged escrow deposit as a condition for settlement discussions with the dissident faction. This boardroom gridlock forces commercial readers to evaluate the likelihood of an activist-driven turnaround versus continued stagnation.

To execute his proposed strategy, Wilson nominated a specific slate of industry veterans designed to address the company’s weaknesses:

Marc Maurer: Former On Holding Co-CEO, bringing verifiable expertise in premium brand growth and international scaling. Laura Gentile: Former ESPN Chief Marketing Officer, offering specialised experience in women’s sports marketing and audience expansion. * Eric Hirshberg: Former Activision Chief Executive Officer, providing a background in brand engagement and consumer retention.

Corporate governance directly impacts shareholder value, especially during periods of operational distress. Understanding the specific mechanics of this proxy fight equips investors to gauge the severity of the internal fracture.

Market analysts frequently cite “brand harvesting” when diagnosing Lululemon’s current executive strategy and resulting margin compression. Brand harvesting occurs when a company heavily relies on promotional discounts to generate short-term revenue bumps at the expense of long-term pricing power. While discounting functions as a standard retail tactic for inventory clearance, it becomes destructive when applied persistently to premium positioned merchandise.

In contrast to these discounting tactics, sustainable retail growth models in the broader consumer market often rely on targeted geographic expansion and intense brand loyalty to fuel revenue without compressing margins.

Consumers learn to wait for sales, permanently lowering the average transaction value.

The Danger of Brand Harvesting “When premium apparel brands resort to continuous promotional tactics, they risk permanently eroding their premium equity amid broader margin compression. This strategy exchanges long-term pricing power for immediate, low-quality revenue that damages the brand moat.”

This theoretical retail concept connects directly to the ongoing criticisms levelled at current management by the activist campaign. By prioritising temporary volume over pricing integrity, the company has alienated core customers and accelerated the margin compression visible in the FY2025 data. Analysts note that these tactics create a temporary illusion of demand while hollowed-out brand equity struggles to support full-price sales.

For investors, monitoring discount frequency provides a clearer metric of underlying distress than top-line revenue alone. Understanding this mechanism transforms a common retail practice into an early warning indicator for equity valuation.

The search for new leadership concluded on 22 April 2026, ending an unstable 300-day executive vacancy. The board announced the appointment of Heidi O’Neill as Chief Executive Officer, effective 8 September 2026. O’Neill brings nearly 30 years of experience from Nike, presenting a legacy sportswear background to a brand built entirely on athleisure and yoga apparel.

Rather than stabilising the stock, the announcement acted as an escalating risk factor for current shareholders. The market reaction was distinctly negative, with the share price dropping between 13.3 and 15 percent on the day of the announcement. This immediate sell-off indicates that investors view a legacy athletic executive as ill-equipped to manage a fundamentally different business model.

This scrutinized leadership transition amplified existing shareholder anxieties, as the abrupt shift from prior leadership to a legacy footwear executive highlighted the broader strategic confusion at the board level.

Institutional investors immediately expressed doubts regarding O’Neill’s capacity to resolve the core North American sales issues. The prevailing concern centres on whether strategies developed at a mass-market footwear giant can translate to a highly specialised, premium apparel retailer. Wilson amplified this market scepticism, criticising the appointment as a reactive measure to his proxy campaign.

He argued that her operational background lacks the necessary creative, product-focused leadership required to restore the company’s premium positioning. While some analysts at institutions like Barclays maintained cautious optimism about her ability to drive organisational change, the severe market rejection stands out.

Leadership changes are primary catalysts for stock movement, and this specific appointment has forced investors to heavily weigh execution risks ahead of her September start date.

Boardroom dysfunction ultimately translates into tangible consumer missteps at the retail level. The controversial November 2024 partnership with Disney exemplifies the total disconnect between a premium athletic image and broad-appeal entertainment merchandise.

The 34-piece dual-gender Disney apparel collection generated immediate sales among theme park fanbases but severely diluted the brand’s exclusive positioning. Financial market professionals noted the confusing nature of this corporate alignment, questioning how cartoon-branded merchandise fits within a high-performance athletic portfolio.

Analyst Commentary “The Disney collaboration created significant financial market confusion. This partnership represented a severe departure from the core performance-focused identity that originally justified the brand’s premium price points.”

This strategic drift extends beyond external collaborations into internal product development. Recent category expansions into footwear and beauty failed to resonate with the core consumer base. These new divisions absorbed significant capital without delivering proportional market share gains or revenue support.

These operational decisions reflect the broader misalignment cited in the proxy campaign. They prove to commercial analysts that the financial stagnation is rooted in observable product failures that have materially diluted the brand’s competitive moat.

Restoring shareholder value requires fixing the product assortment before adjusting the marketing strategy.

For investors wanting to understand how agile merchandising could potentially repair this product assortment, our detailed coverage of Lululemon’s brand dilution explores the 2026 Action Plan and evaluates whether aggressive international expansion can offset North American stagnation.

Lululemon faces a critical convergence of a contested leadership transition, the upcoming 2026 annual meeting vote, and a persistent regional sales slump. The core challenge remains restoring the brand’s premium North American positioning while navigating extreme internal friction. Management must halt the brand harvesting tactics before the pricing power erosion becomes permanent.

Market data from other consumer brand turnaround strategies demonstrates that reversing domestic sales slumps typically requires a delicate balance of product innovation and targeted customer re-engagement without sacrificing core pricing power.

Investors must monitor upcoming quarterly margin reports and the frequency of promotional discounting to determine if a turnaround is viable under the incoming chief executive. The outcome of the proxy vote will likely dictate whether the company pursues an activist-led restructuring or attempts to correct its operational drift under the current board’s direction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The Lululemon proxy battle involves founder Chip Wilson, who holds an 8.4 percent stake, nominating three independent directors to challenge the current board over strategic direction and corporate governance issues.

Lululemon's financial performance shows a 65.9 percent valuation plunge, a 1 percent decrease in Americas comparable sales for Q4 FY2025, and a 380 basis point drop in operating margin for FY2025, indicating significant challenges.

The market reacted negatively to Heidi O'Neill's appointment as CEO, causing a 13.3 to 15 percent share price drop, due to investor skepticism that her background at mass-market Nike aligns with Lululemon's premium athleisure model.

Brand harvesting occurs when a company uses heavy promotional discounts for short-term revenue, which analysts accuse Lululemon of doing, potentially eroding its long-term pricing power and premium equity.