ASIC Fines Three ASX Companies $1.17m for Missing Annual Reports

7 hrs ago

Since early January 2026, the iShares China Large-Cap ETF (ASX: IZZ) has shed approximately 10% of its value. For some ASX investors, that drawdown is a warning sign. For others, it is the entry point they have been watching for.

The tension between those two readings captures the broader question facing Australian retail investors right now. With US-China trade tensions generating reciprocal tariffs of up to 145% and 125% respectively, and the US dollar’s dominance facing its most serious questions in decades, geographic allocation is no longer a set-and-forget decision. Chinese equities, long treated as a satellite bet, are attracting renewed scrutiny as a potential counterweight to US market concentration.

This analysis unpacks what IZZ actually holds, how it has performed, what it costs relative to its ASX peers, what structural risks are embedded in the fund, and how investors should weigh those factors given the current macro environment.

The conversation starts with tariffs, but it does not end there. Through 2025 and into 2026, US-China trade escalation pushed reciprocal duties to levels that would have seemed implausible two years ago.

US tariffs on Chinese goods have reached 145%. China’s retaliatory tariffs on US imports stand at 125%. These figures represent the sharpest bilateral trade barriers between the world’s two largest economies in the modern era.

That escalation has coincided with a broader erosion of confidence in US global institutional leadership, prompting Australian allocators to reconsider portfolios heavily weighted toward US equities. China’s position as the world’s second-largest economy, with stated superpower ambitions and a 2026 GDP growth target of 4.5%-5%, provides the macroeconomic frame.

What sharpens the investment case beyond GDP figures is China’s industrial positioning in the sectors that are likely to define the next decade of global growth:

Beijing has deployed stimulus measures to offset trade headwinds, and that policy support underpins the earnings outlook for the large-cap companies IZZ tracks. The question for ASX investors is whether those credentials translate into portfolio returns, or whether the geopolitical discount absorbs them.

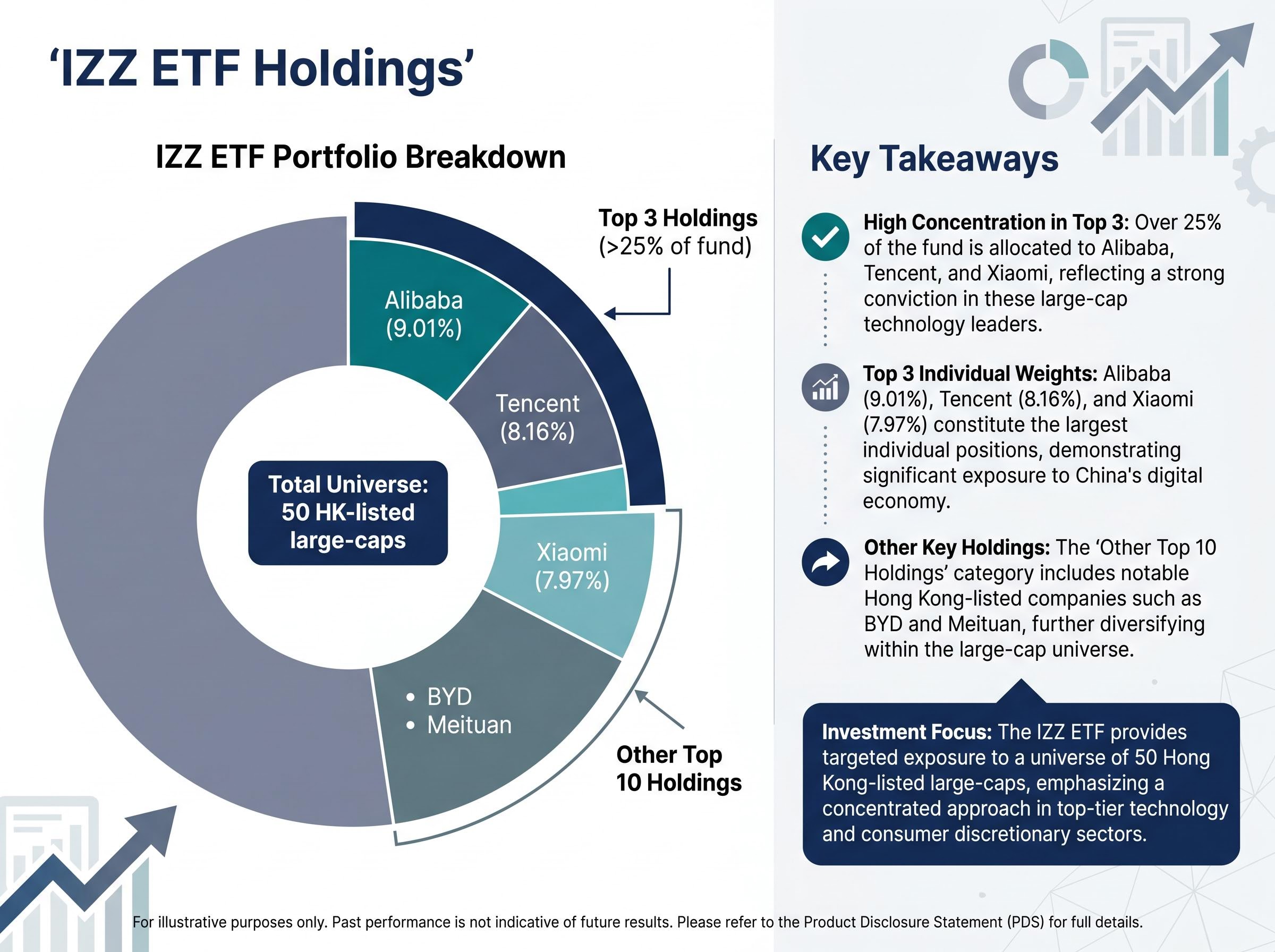

IZZ tracks 50 of China’s largest companies listed on the Hong Kong Stock Exchange. That distinction matters. This is not mainland A-share exposure, where companies trade on the Shanghai or Shenzhen exchanges under tighter capital controls. Hong Kong-listed Chinese large-caps are accessible to international capital flows, dual-listed in many cases, and subject to Hong Kong’s regulatory framework alongside mainland obligations.

The portfolio’s character becomes clearer through its largest positions.

| Holding | Approximate portfolio weight |

|---|---|

| Alibaba | 9.01% |

| Tencent | 8.16% |

| Xiaomi | 7.97% |

| BYD | Top 10 holding |

| Meituan | Top 10 holding |

The top three names alone account for more than 25% of the fund, giving IZZ a meaningful concentration in Chinese technology and consumer platforms. Investors familiar with these businesses through global media coverage will recognise the portfolio’s tilt toward China’s digital and industrial economy.

Key fund mechanics at a glance:

Over 22 years of operation, IZZ has delivered an annualised return of 5.63% to 31 March 2026.

5.63% annualised since 2004. That figure captures multiple cycles of Chinese market volatility, including the 2008 global financial crisis, the 2015 mainland equity sell-off, the COVID-19 drawdown, and the regulatory crackdowns of 2021. It is a reference point for long-run expectations, not a guarantee.

That baseline establishes IZZ as a fund with a meaningful, if moderate, track record of compounding returns across dramatically different market environments. The 2.15% trailing yield adds an income component that supplements capital returns.

The gap between that long-run average and recent performance is sharp. In early January 2026, IZZ’s unit price closed at approximately $58.27. By early April 2026, prices ranged between approximately $50.64 and $52.28, representing a drawdown of approximately 10.3% in under three months.

The year-to-date total return as of 28 April 2026 stood at approximately -5.59%.

As of 30 April 2026, the unit price sat at approximately $51.10, against a net asset value (NAV) of $50.18 as of 28 April 2026. That narrow premium to NAV is a practical data point for investors evaluating whether the current market price reflects fair value or whether the drawdown has created a discount worth acting on. The difference between $51.10 and $50.18 suggests the market is pricing IZZ close to its underlying portfolio value, with no significant premium or discount distortion.

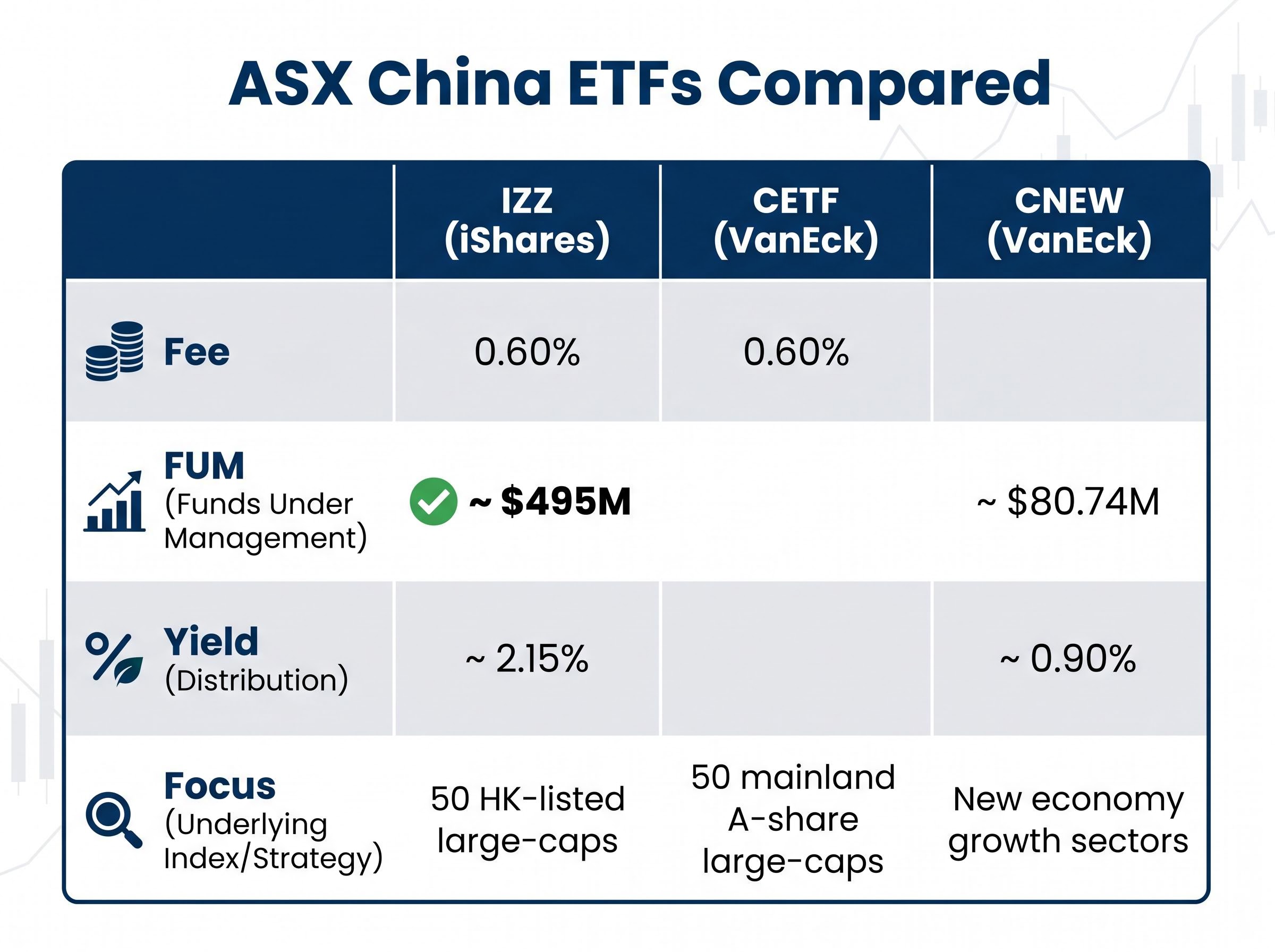

Australian investors searching for China exposure on the ASX will encounter three primary options. The structural differences between them are more significant than the headline fees suggest.

| Fund | Management fee | FUM (approx.) | Dividend yield (approx.) | Index universe |

|---|---|---|---|---|

| IZZ (iShares) | 0.60% | $495M | 2.15% | 50 HK-listed large-caps |

| CETF (VanEck) | 0.60% | Not disclosed | Not disclosed | 50 mainland A-share large-caps |

| CNEW (VanEck) | Not disclosed | $80.74M | 0.90% | New economy growth sectors |

IZZ and CETF both charge 0.60%, but they track entirely different universes. IZZ holds Hong Kong-listed giants like Alibaba and Tencent; CETF holds the 50 largest mainland A-share companies, which trade under different capital controls and regulatory structures. Fee parity alone is a misleading comparison criterion.

CNEW takes a thematic approach, targeting China’s new economy growth sectors. Its FUM of approximately $80.74 million is a fraction of IZZ’s $495 million, and its yield of approximately 0.90% reflects a growth-oriented portfolio that prioritises capital appreciation over income.

IZZ’s scale advantage matters for ASX retail investors. Higher FUM typically correlates with tighter bid-ask spreads and greater institutional adoption, both of which reduce friction for investors entering or exiting positions.

Chinese-listed companies operate under governance obligations that differ from the frameworks ASX investors apply to domestic or US holdings. Businesses are required to prioritise state directives, which can influence dividend policy, capital allocation decisions, and strategic direction in ways that may not align with minority shareholder interests.

This is not a temporary regulatory environment. It is a structural feature of investing in Chinese equities. For ETF holders, it means the companies in IZZ’s portfolio may redirect capital toward state priorities even when shareholder returns would be better served by alternative uses.

Non-citizens cannot hold direct ownership stakes in Chinese-listed companies. ETF investors hold indirect exposure through the fund structure, which limits shareholder recourse in ways that differ from holding ASX-listed equities directly.

China’s securities regulator (CSRC) has outlined a 2026 reform agenda that encompasses market liberalisation and the development of stablecoin regulations in Hong Kong. Recent legislative changes have also reduced entry barriers for foreign fund investors.

These reforms represent both opportunity and uncertainty:

Investors who understand these risks can size their allocation appropriately. Those who overlook them may find their risk-adjusted return assumptions tested.

The analytical threads converge on a practical question: does IZZ belong in an Australian investor’s portfolio, and if so, how much?

The bull case anchors:

The bear case anchors:

IZZ functions as a satellite allocation rather than a core holding. The appropriate sizing depends on an investor’s existing US and domestic equity concentration, risk tolerance, and view on the trajectory of US-China trade relations through 2026 and beyond. The 2028 US presidential election represents a potential inflection point in that trajectory, for better or worse.

IZZ is a well-constructed, liquid, and cost-competitive vehicle for gaining exposure to China’s largest companies. Its 22-year track record, $495 million in funds under management, and 2.15% yield give it credible standing among ASX-listed China ETFs.

The structural governance risks and macro volatility mean it demands active portfolio positioning rather than passive treatment. The fund’s 10.3% drawdown since January and ongoing tariff uncertainty make current entry timing a live question. The NAV versus unit price relationship ($50.18 versus $51.10) is a practical data point to monitor in the weeks ahead.

Australian investors who already hold US-heavy equity portfolios and want a non-correlated, large-cap Asian allocation have a credible option in IZZ, provided they have digested the governance and geopolitical risk profile. Comparing IZZ against CETF and CNEW using the framework above, and reviewing IZZ’s latest product disclosure statement and BlackRock fund page for current holdings and distribution announcements, would be a sound next step before making an allocation decision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The iShares China Large-Cap ETF (ASX: IZZ) is an exchange-traded fund that tracks 50 of China's largest companies listed on the Hong Kong Stock Exchange, with top holdings including Alibaba, Tencent, and Xiaomi, and a management fee of 0.60% per annum.

IZZ has had a difficult start to 2026, falling approximately 10.3% from its January peak of around $58.27 to a range of $50.64-$52.28 by early April, with a year-to-date total return of approximately -5.59% as of 28 April 2026.

The key risks include structural governance obligations that require Chinese companies to prioritise state directives over shareholder returns, ongoing US-China trade tensions with tariffs reaching up to 145%, and an evolving regulatory environment that could change within 12-18 months in ways that may not favour foreign investors.

IZZ is the largest ASX-listed China ETF with approximately $495 million in funds under management and a 2.15% yield, while VanEck's CETF tracks mainland A-share companies at the same 0.60% fee, and VanEck's CNEW focuses on new economy growth sectors with only $80.74 million in FUM and a 0.90% yield.

IZZ is best suited as a satellite allocation rather than a core holding, appropriate for investors who already hold US-heavy equity portfolios and want a non-correlated large-cap Asian allocation, provided they understand the governance and geopolitical risk profile.