Barclays Warns of Prolonged Market Volatility Under New Fed Reality

1 hr ago

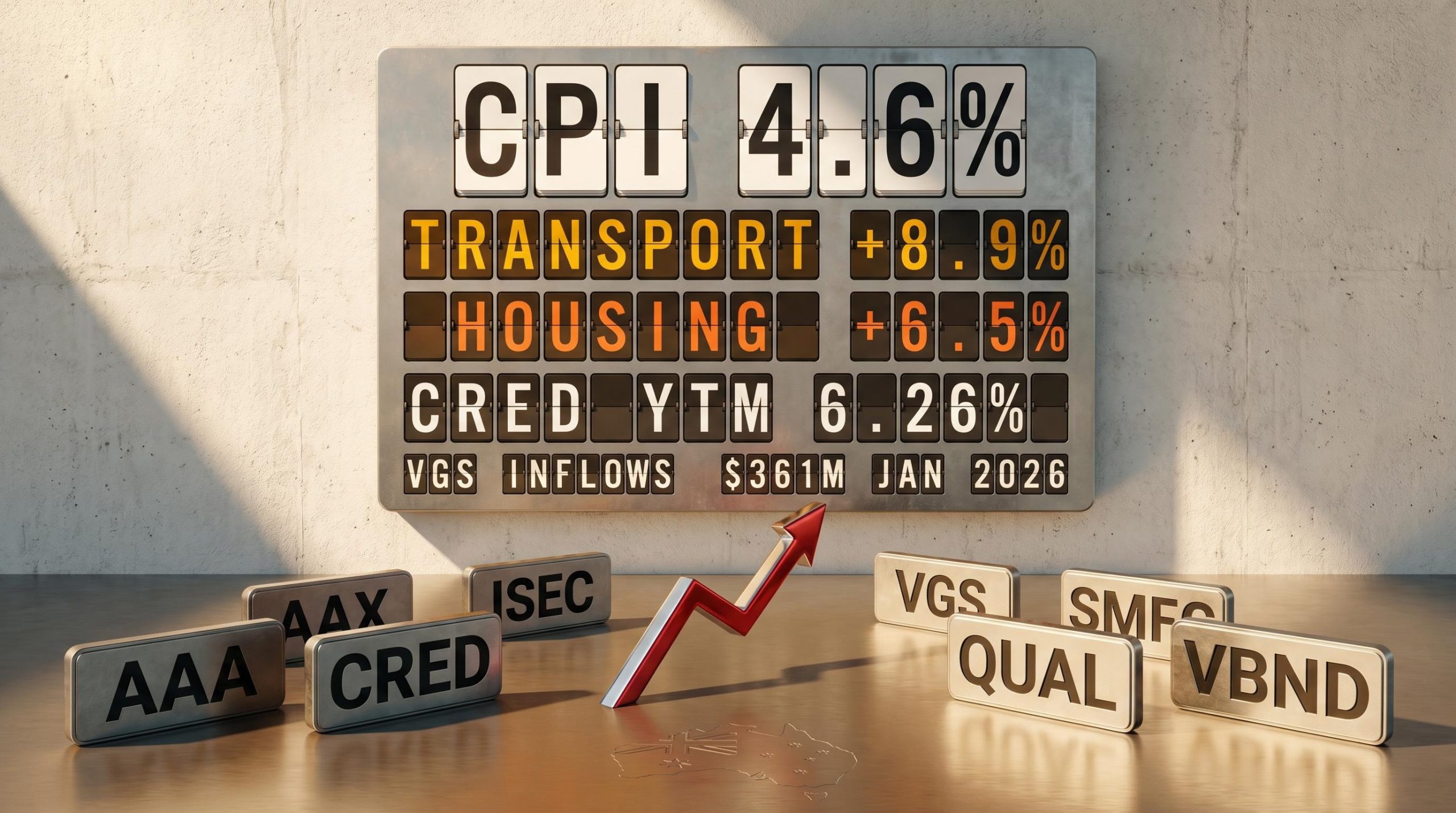

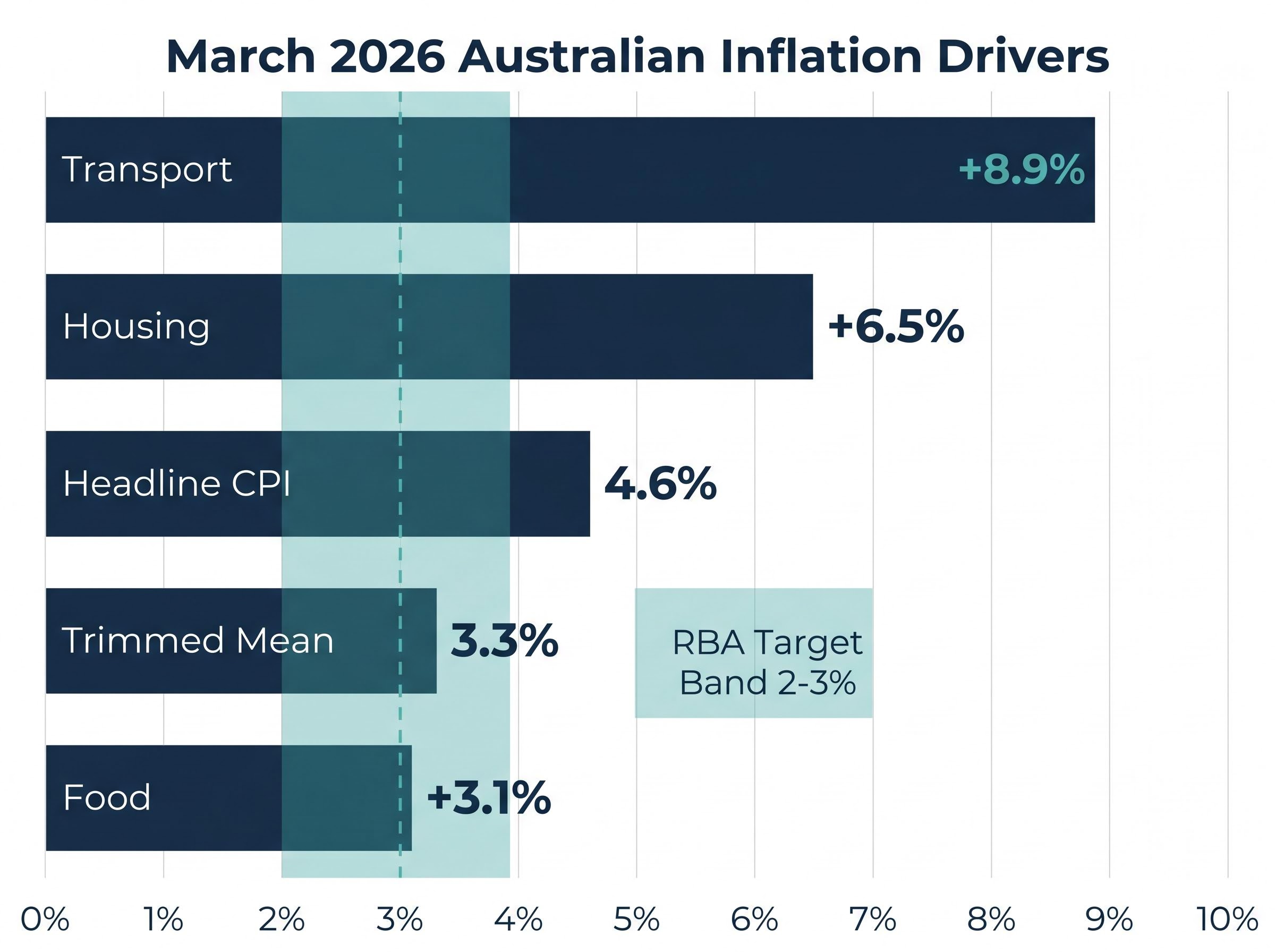

Australia’s headline Consumer Price Index (CPI) hit 4.6% in the March quarter of 2026, up from 3.7% just three months earlier, with transport costs surging 8.9% and housing rising 6.5%. For investors holding cash in standard deposit accounts earning less than inflation, every month of inaction delivers a guaranteed real loss. The acceleration signals that inflation is not fading quietly; oil above $100 per barrel, US tariff uncertainty, and US-Iran geopolitical tension are all feeding into domestic price pressures. The Reserve Bank of Australia (RBA) faces a difficult balancing act, and Australian retail investors cannot afford to wait for policy clarity before making portfolio decisions. This guide covers six ASX-listed ETFs positioned for an inflationary environment in 2026, spanning income generation, global diversification, and capital preservation, with a practical framework for implementing each strategy.

The arithmetic is straightforward. Any asset yielding below 4.6% is producing a negative real return. A savings account paying 3% is not preserving capital; it is losing purchasing power at roughly 1.6 percentage points per year after inflation. That erosion compounds, and it accelerates when inflation itself is accelerating.

Inflation investing as a discipline distinguishes between assets that merely generate nominal returns and those that produce genuine real returns above the prevailing CPI rate, a distinction that becomes materially important when headline inflation is running at 4.6% and standard deposit accounts are paying 3%.

What makes this inflation episode particularly challenging is its composition. Three categories are doing the heaviest lifting:

The ABS Consumer Price Index release for the March 2026 quarter confirms headline inflation at 4.6%, with Transport rising 8.9%, Housing 6.5%, and trimmed mean inflation at 3.3%, providing the official statistical foundation for every allocation decision discussed in this guide.

Trimmed mean inflation sits at 3.3%, confirming that underlying price pressures remain above the RBA’s 2-3% target band. This is not a transitory spike; it is a sustained structural environment that requires a deliberate portfolio response.

The distinction between oil-driven and housing-driven inflation matters for investment strategy. Oil-linked price pressures have historically resolved within 6-12 months as supply normalises or demand cools. Housing inflation is stickier, tied to years of undersupply in the Australian residential market. That dual nature argues for both short-term defensive positioning and medium-term strategies that seek real returns above the inflation rate.

Rising bond yields are not purely bad news. When central banks raise rates, bond prices fall, but the income available from newly issued bonds and bond ETFs rises. For investors entering the market today, higher yields mean higher ongoing income, a meaningful shift from the near-zero yield environment of the early 2020s.

The RBA cash rate is the key policy lever influencing both fixed income ETF yields and cash ETF returns. For the latest cash rate setting and forward guidance, readers should check the RBA’s monetary policy page at rba.gov.au, as verified data on the current rate was not available at the time of writing.

The RBA Statement on Monetary Policy from February 2026 noted that inflation is expected to remain above target for some time, with the cash rate at 3.85%, a forward guidance stance that directly shapes the yield environment underpinning each ETF’s income profile discussed here.

The concept of duration risk is where the choice between ETFs becomes consequential. Duration measures how sensitive a bond’s price is to changes in interest rates. CRED, the BetaShares Australian Investment Grade Corporate Bond ETF, carries a modified duration of 6.02 years. In practical terms, if interest rates rise by 1 percentage point, CRED’s price would be expected to fall by approximately 6%. A shorter-duration instrument like AAA carries far less of that sensitivity.

The Taylor Rule, a framework central banks reference when setting rates, suggests that rates must rise approximately 1.5 percentage points for every 1 percentage point of inflation overshoot above target to genuinely restrict financial conditions. With trimmed mean inflation at 3.3% against a 2-3% target band, that principle implies rates may have further to climb before policy becomes genuinely restrictive.

The RBA rate hike cycle now has a plausible ceiling: Oxford Economics modelling flags potential back-to-back quarterly GDP contractions in June and September 2026, which historically has caused central banks to pivot from tightening to easing faster than bond markets price in.

Historical precedent offers some comfort. Supply-driven oil shocks have typically lifted rates for only 6-12 months before growth concerns pulled them back down. For investors willing to accept short-term price volatility, locking in current yields may prove well-timed.

| Metric | AAA (Cash ETF) | CRED (Corporate Bond ETF) |

|---|---|---|

| Type | Cash / Fixed Income | Investment Grade Corporate Bonds |

| Distribution Yield | 3.9% (12-month) | 5.2% (12-month) |

| Yield to Maturity | N/A | 6.26% |

| Duration | Minimal | 6.02 years |

| FUM | A$5.19B | A$1.78B |

CRED’s yield to maturity of 6.26% represents the annualised return an investor can expect if the underlying bonds are held to maturity, making it the strongest verified forward income figure among these ETFs.

Six ETFs span three functional categories that address different inflation-environment needs: income and capital preservation, global diversification and growth, and global fixed income hedged to AUD. Each serves a distinct purpose, and the choice between them depends on the investor’s time horizon, income requirements, and risk tolerance.

| ETF Ticker | Category | Inflation Strategy Role | Key Yield / Return | FUM |

|---|---|---|---|---|

| AAA | Income / Preservation | Liquid defensive cash holding with monthly income | 4.19% net yield | A$5.19B |

| CRED | Income / Preservation | Above-inflation yield with moderate duration risk | 5.2% distribution; 6.26% YTM | A$1.78B |

| ISEC | Income / Preservation | Short-duration income above standard deposits | Check iShares Australia* | Check iShares Australia* |

| VGS | Growth / Diversification | Broad global equity exposure across 1,000+ large caps | ~2.5% yield (indicative) | ~A$14B (indicative) |

| QUAL | Growth / Diversification | Pricing-power companies with low debt, high profitability | Check VanEck Australia* | Check VanEck Australia* |

| VBND | Global Fixed Income | AUD-hedged global bond diversification | Check Vanguard Australia* | Check Vanguard Australia* |

ISEC, QUAL, and VBND data was not verified from live sources at the time of writing. Readers should check the relevant provider pages for current metrics before making allocation decisions.

AAA serves as a liquid, monthly-income defensive holding. Its 4.19% net yield sits marginally below headline CPI at 4.6%, but it remains a valuable instrument for capital preservation and cash-flow needs, particularly for investors who require predictable monthly distributions. With A$5.19 billion in funds under management, its scale reflects an established role in Australian defensive portfolios.

CRED is the only ETF in this group with a verified yield clearly above headline CPI. Its 5.2% twelve-month distribution yield and 6.26% yield to maturity make the strongest verified case for above-inflation fixed income. The trade-off is its 6.02-year modified duration, which introduces meaningful price sensitivity if rates continue to rise.

ISEC, the iShares Enhanced Cash ETF, occupies a middle ground between AAA and CRED on the yield and duration spectrum, offering yields modestly above standard deposit ETFs with short-duration exposure. Current metrics should be confirmed directly via iShares Australia.

VGS, the Vanguard MSCI Index International Shares ETF, provides broad global equity exposure across more than 1,000 large-cap companies. It topped ASX ETF inflows in January 2026 at approximately $361 million, signalling strong institutional and retail conviction in global diversification. Its exposure to US technology and AI-driven earnings growth offers a return pathway that is largely independent of domestic Australian inflation dynamics.

QUAL, the VanEck MSCI International Quality ETF, focuses on profitable, low-debt companies with pricing power. In an inflationary environment, companies that can pass rising input costs through to customers tend to maintain margins more effectively. Live yield and FUM data should be verified via VanEck Australia.

VBND, the Vanguard Global Aggregate Bond Index (Hedged) ETF, provides international fixed income exposure hedged to AUD, reducing currency risk while accessing global government and investment-grade corporate bond yields. It serves as a complement to CRED for investors seeking geographic diversification within their fixed income allocation. Current figures should be confirmed via Vanguard Australia.

Knowing what to own is one decision. Knowing how to deploy capital in a volatile, inflationary market is another.

Dollar-cost averaging (DCA) is the practice of investing a fixed dollar amount at regular intervals regardless of price. When prices fall, the same dollar amount purchases more units. When prices rise, it purchases fewer. Over time, this mechanical discipline reduces the average cost basis of the position without requiring the investor to predict short-term price movements.

Consider a simple example: an investor allocating $500 per month to VGS. If the unit price drops from $100 to $80 mid-year, that month’s contribution buys 6.25 units instead of 5. The investor accumulates more units precisely when the market offers them at a discount.

Holding a cash position during market dislocations is not a permanent defensive strategy. It is optionality capital, funds kept in an instrument like AAA (earning 4.19% while waiting) that can be deployed into high-conviction positions when sell-offs create discounted entry points. During the US-Iran tension period in early 2026, ASX futures showed fragile sentiment and risk-off behaviour, precisely the type of dislocation that creates asymmetric entry opportunities for disciplined investors.

The implementation is straightforward:

Automation removes the emotional friction of timing decisions. Investors who participate from the earliest stages of a recovery capture gains that those waiting for confirmation miss entirely.

Reactive trading behaviour, the impulse to sell during sell-offs and buy after recoveries have already run, is one of the primary destroyers of long-run retail investor returns; the mechanical discipline of a fixed periodic contribution schedule removes the decision entirely from the equation.

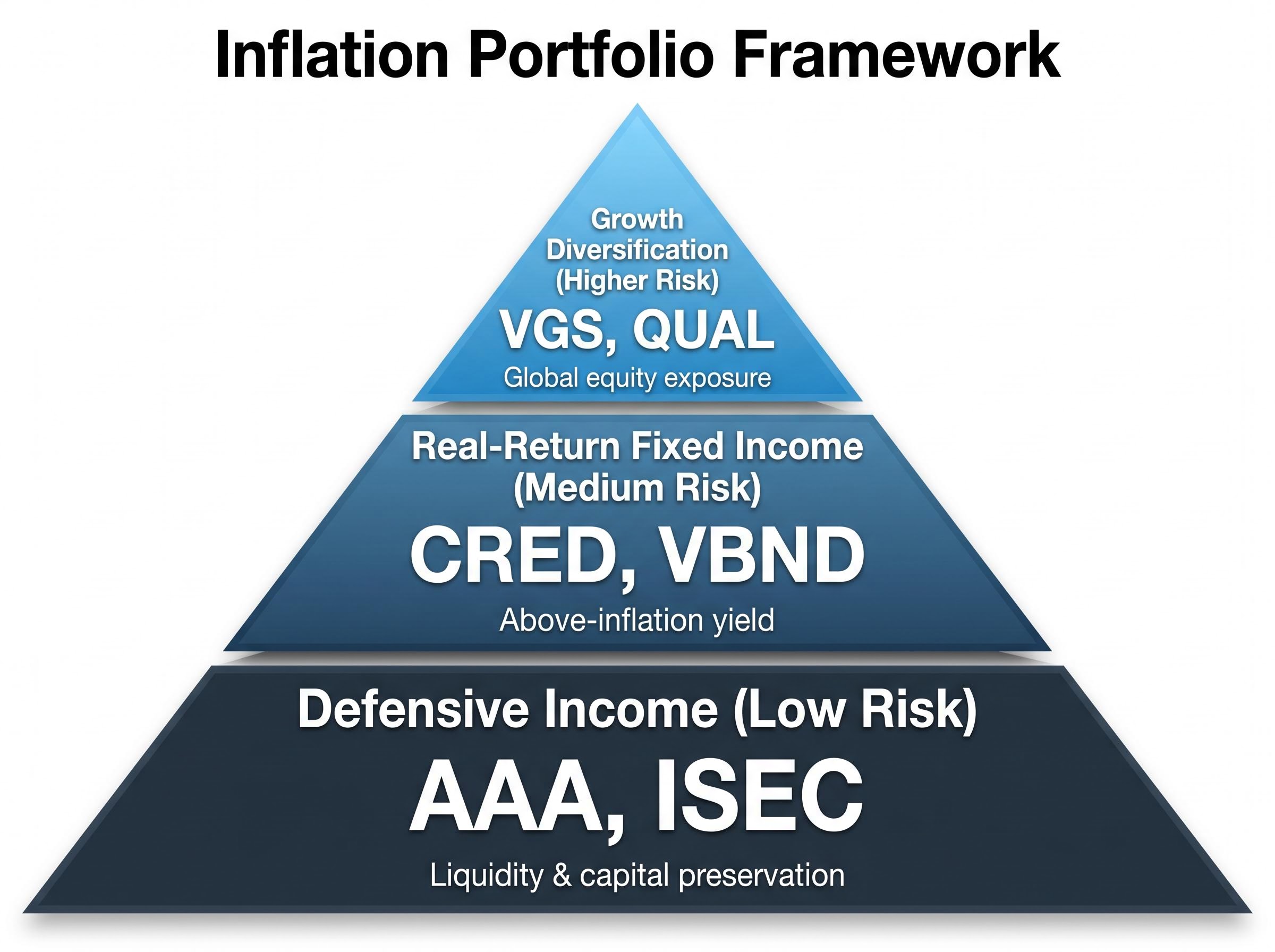

A layered portfolio framework helps investors move from a list of instruments to an architecture that reflects their own circumstances. In an inflationary environment, three layers serve distinct purposes.

| Layer | ETFs | Role in Inflationary Environment | Risk Level |

|---|---|---|---|

| Defensive Income | AAA, ISEC | Liquidity, monthly cash flow, capital preservation | Low |

| Real-Return Fixed Income | CRED, VBND | Above-inflation yield with moderate duration exposure | Medium |

| Growth Diversification | VGS, QUAL | Global equity exposure, long-term capital growth | Higher |

The proportions across these three layers depend on individual circumstances. Three principles guide the allocation decision:

CRED’s 5.2% distribution yield versus 4.6% CPI makes it the only verified above-inflation fixed income option in this group. VGS’s $361 million in January 2026 inflows reflects broad market conviction in the global equity diversification thesis. AAA’s A$5.19 billion FUM confirms its established role as Australia’s default defensive cash instrument.

Research from the International Monetary Fund suggests each additional percentage point of inflation above 3% in a developed economy is associated with a 0.1-0.2 percentage point reduction in real GDP growth, reinforcing the case for assets that actively seek real returns rather than passively accepting erosion.

The oil futures curve offers the first signal worth tracking. Near-term oil futures are currently trading above longer-dated contracts, a structure known as backwardation. This pattern indicates the market views the current supply disruption as temporary. If oil prices normalise, the Transport component of CPI (currently +8.9%) should ease materially, pulling headline inflation lower.

Housing inflation at +6.5% tells a different story. Domestic supply constraints in Australian residential construction are structural, driven by years of underbuilding relative to population growth. This component is unlikely to resolve quickly regardless of RBA policy or global energy markets.

Historical supply-driven oil shocks have followed two resolution pathways: either demand cools and rates come down within 6-12 months, or supply constraints ease and prices normalise independently. Both pathways eventually reduce inflationary pressure, but they carry different implications for portfolio positioning. A demand-led resolution favours longer-duration bonds (CRED benefits). A supply-led resolution favours equities (VGS benefits).

Four signals are worth monitoring on an ongoing basis:

“The ultra-low inflation environment of the 2010s is considered unlikely to return, with 2% appearing to function more as a lower bound than an upper ceiling.”

That structural view suggests inflation-aware investing is not a temporary tactical adjustment. It is a framework Australian investors may need to maintain for years.

In a 4.6% inflation environment, holding undeployed cash in low-yield accounts produces a guaranteed negative real return. The gap between AAA’s 4.19% net yield and headline CPI represents the baseline cost of inaction: a slow, compounding erosion of purchasing power that no future rate cut can retroactively recover.

This guide has presented six named ETFs across three functional categories that address this problem directly. CRED’s 5.2% distribution yield and 6.26% yield to maturity demonstrate that above-inflation fixed income is available on the ASX today. VGS and QUAL provide global equity exposure that captures growth regardless of which inflation resolution pathway plays out. AAA and ISEC preserve capital and generate cash flow while investors build positions.

The DCA and layered portfolio framework removes the need to predict exact RBA timing or oil price movements. A diversified, automated approach ensures participation in recoveries from their earliest stages while maintaining discipline through volatility. Investors who build positions across income, growth, and optionality are positioned to benefit whether inflation subsides through demand cooling or supply normalisation.

The generational shift toward global ETFs in Australia reflects more than inflation hedging; Millennials now allocate approximately 70% of their investment capital to ETFs, with younger cohorts systematically using market volatility as a structured entry-price advantage rather than a reason to defer investment.

Certainty is not a prerequisite for action. Discipline is.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An inflation investment strategy focuses on holding assets that generate real returns above the prevailing CPI rate, rather than nominal returns that lose purchasing power. With Australian headline inflation at 4.6% in March 2026, any asset yielding below that figure is producing a guaranteed negative real return.

Six ASX ETFs are well-positioned for inflation in 2026: AAA and ISEC for defensive income and capital preservation, CRED for above-inflation fixed income with a 5.2% distribution yield and 6.26% yield to maturity, and VGS and QUAL for global equity growth, with VBND providing AUD-hedged global bond diversification.

Dollar-cost averaging involves investing a fixed dollar amount at regular intervals regardless of price, which automatically purchases more units when prices fall and fewer when prices rise, reducing average cost basis without requiring investors to time the market.

Duration risk measures how sensitive a bond or bond ETF's price is to interest rate changes. CRED carries a modified duration of 6.02 years, meaning a 1 percentage point rise in interest rates would be expected to reduce its price by approximately 6%, making it a meaningful consideration for investors entering in a rising-rate environment.

Yes. CRED's 12-month distribution yield of 5.2% and yield to maturity of 6.26% both exceed Australia's March 2026 headline CPI of 4.6%, making it the only verified above-inflation fixed income option among the six ETFs covered in this analysis.