Record Highs Are Not the Risk Most Investors Think They Are

5 hrs ago

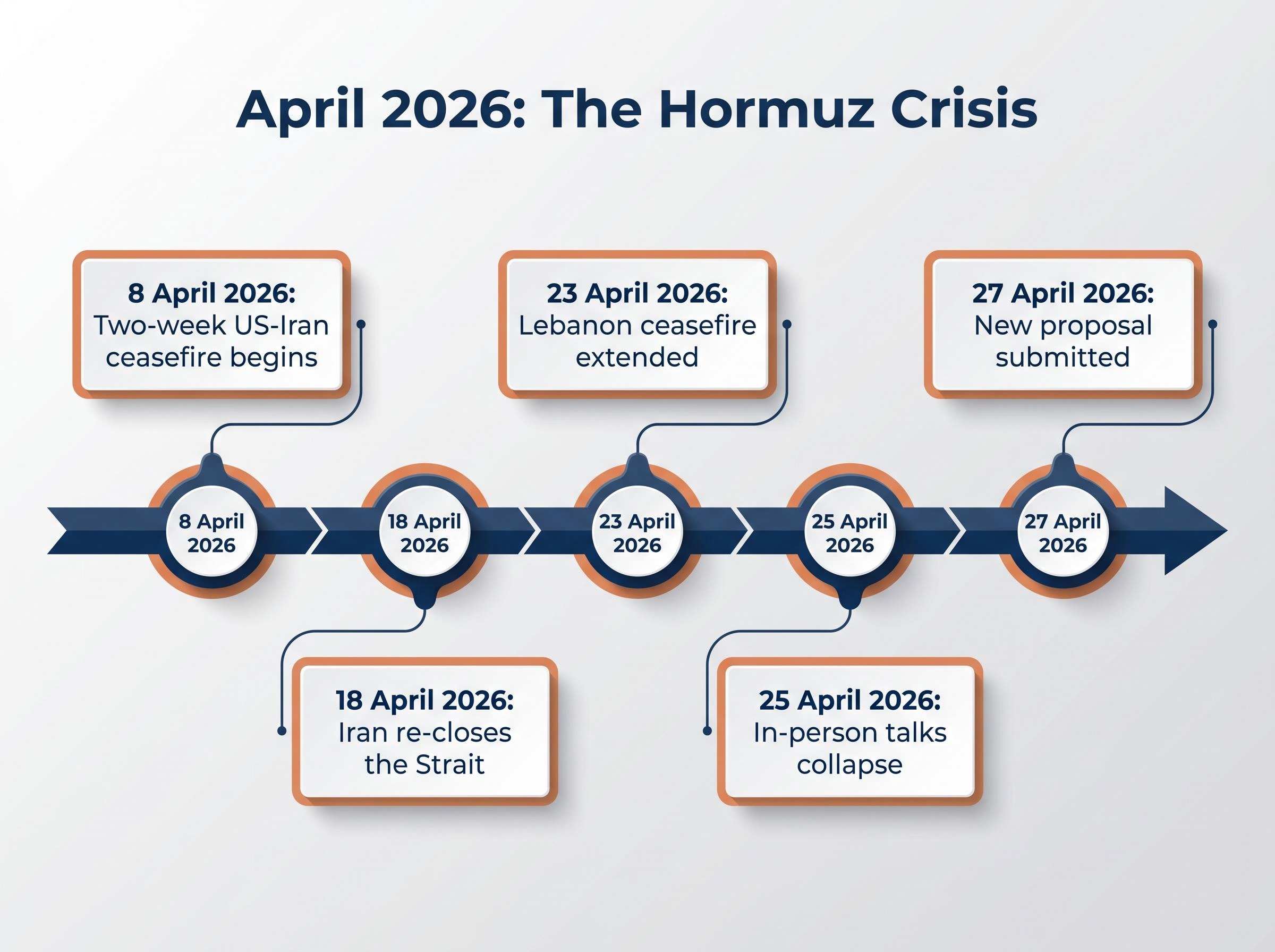

The Strait of Hormuz remains closed to commercial shipping as of 27 April 2026, with Brent crude trading near $95 per barrel and a new Iranian diplomatic proposal sitting unanswered in Tehran. Iran submitted the offer through Pakistani intermediaries on 27 April, outlining a path to reopen the Strait without requiring immediate nuclear concessions. The proposal landed days after in-person peace talks in Islamabad collapsed and President Trump cancelled the US delegation’s trip to Pakistan.

What follows is a breakdown of the proposal’s contents, why the Strait of Hormuz sits at the centre of global energy supply, what crude oil and equity markets are pricing right now, and what investors should monitor as the diplomatic situation develops.

The current crisis has unfolded across three weeks of escalation, ceasefire, and collapse. The sequence matters because it explains why markets are not treating the latest proposal as a resolution.

The current Hormuz standoff did not emerge in isolation; it is one chapter in the broader Iran conflict that began in February 2026, which drove Brent crude past $120 per barrel, pushed Asian LNG spot prices more than 140% higher after Iran’s attack on Qatar’s Ras Laffan Industrial City, and prompted the IEA to describe the situation as the greatest global energy security challenge in history.

Iran is the actor that closed the Strait, doing so in direct response to US port blockades. Full reopening is tied to Iran’s conditions being met. Pakistan has served as the primary intermediary, and US envoy Steve Witkoff has maintained direct text-message communications with Iranian Foreign Minister Araghchi, a channel Iran itself has confirmed, even as Tehran denies any in-person meetings with US officials.

The proposal follows a two-phase structure: an immediate ceasefire and commercial Strait reopening first, with nuclear issues deferred to a 15-20 day subsequent window.

President Trump characterised Iran’s negotiating tactics as “a little cute,” signalling that Washington views Tehran’s conditional approach with scepticism rather than optimism.

No signed agreement exists. No active face-to-face talks are under way. The pattern of ceasefire followed by re-closure is the baseline investors should use when assessing the latest offer.

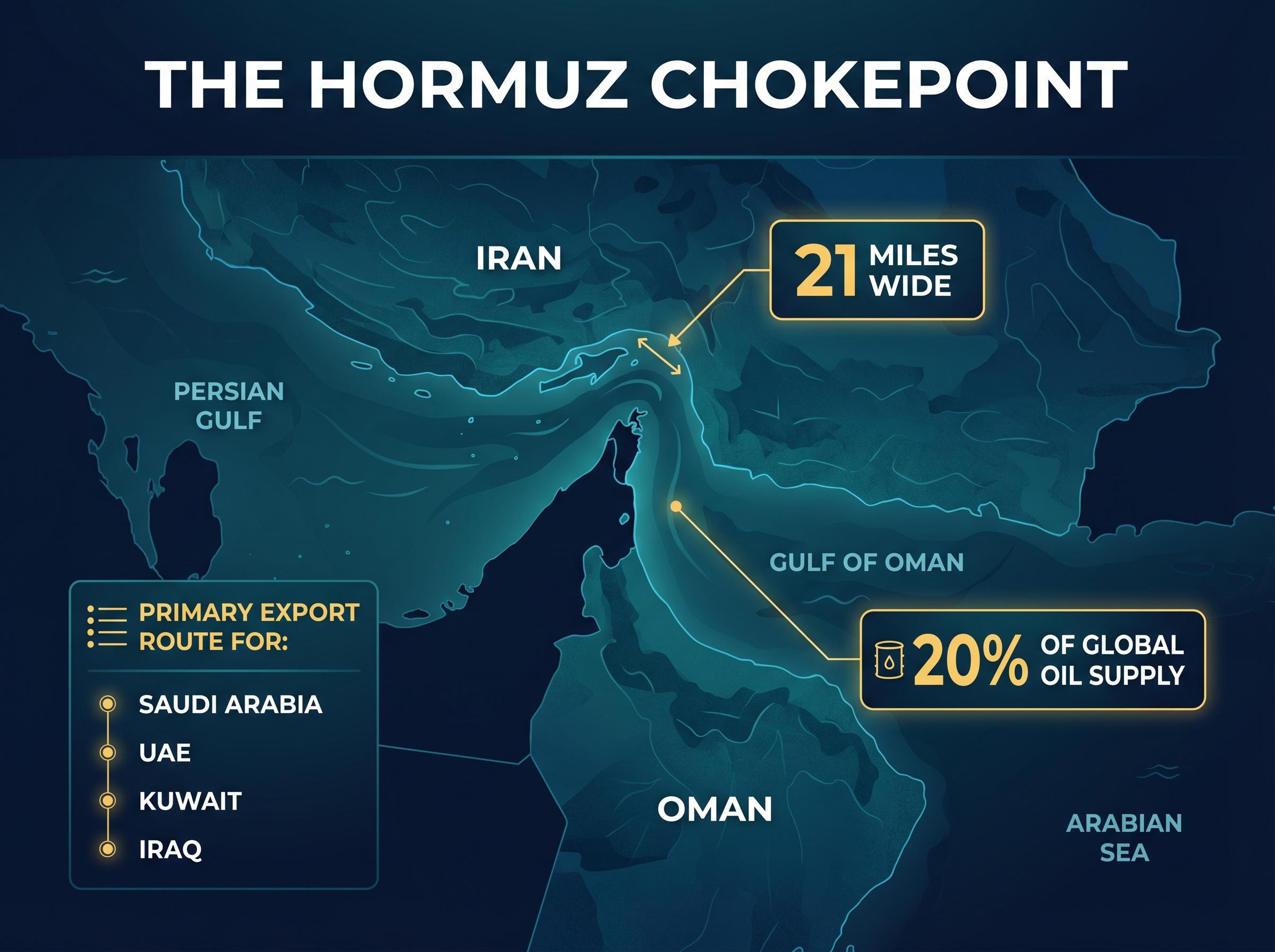

The Strait of Hormuz is a narrow sea passage between Iran and Oman, connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea. Its dimensions alone explain its strategic weight.

EIA data on Strait of Hormuz oil transit volumes places the daily throughput at approximately 20 million barrels, representing roughly 20% of global petroleum liquids consumption and confirming that no comparable alternative route exists for Gulf producers at that scale.

Approximately 20% of the world’s oil supply passes through the Strait of Hormuz, making it the single most consequential chokepoint in global energy infrastructure.

Iran’s leverage derives directly from geography. No alternative route of equivalent capacity exists for Gulf producers. Pipeline bypasses can handle a fraction of the volume; none can substitute for the Strait at scale. This is why even a partial or temporary closure produces immediate price spikes rather than gradual adjustments. The supply shock is structural, not speculative, and it affects every economy that imports Gulf crude, the United States included.

Markets have not waited for diplomats to reach a conclusion. The price of crude oil already encodes the risk that talks will fail.

| Benchmark | Current Price (approx.) | Market Signal |

|---|---|---|

| Brent Crude | $94-96/bbl | Elevated risk pricing |

| WTI Crude | $92-94/bbl | Elevated uncertainty |

Both benchmarks are elevated relative to pre-crisis levels, reflecting ongoing Strait restrictions rather than a single event. Traders are pricing in elevated odds of ceasefire breakdown, and the reasoning is straightforward: in-person talks collapsed on 25 April, Iran has already re-closed the Strait once after a ceasefire period, and no binding agreement exists.

The speed at which the market reacted to the April 8 ceasefire illustrates how rapidly the Iran risk premium can be stripped from crude prices: on 20 April 2026, Brent fell 9.41% in a single session to $82.59 as traders removed the Strait of Hormuz supply disruption premium, even though the Strait had not physically reopened.

Three factors are sustaining upward price pressure:

For investors with exposure to energy equities, commodity exchange-traded funds (ETFs), or inflation-sensitive fixed income, the current price level is a direct consequence of the diplomatic impasse, not a temporary spike.

The S&P 500 closed at approximately 7,157 points on 27 April, down roughly 0.12%. The Nasdaq and Dow posted similarly subdued sessions. Equity futures were edging lower, driven by stalled Iran talks and rising oil prices.

Four days earlier, the picture looked different. Both the S&P 500 and Nasdaq closed at record highs on 23 April 2026, when the Lebanon ceasefire extension briefly suggested broader diplomatic momentum. The gap between those highs and the current tone captures the market’s sensitivity to each development in the Hormuz situation.

Analyst sentiment suggests an equity market surge could follow a confirmed peace agreement, with energy cost relief and restored shipping confidence expected to drive broad-based buying across sectors.

The asymmetry runs in both directions:

Markets have been broadly downplaying the economic impact of the US-Iran conflict, with US bank earnings data indicating consumers remain in a healthy financial position. That underlying resilience supports the case for a strong recovery rally if a deal materialises. It also means the repricing risk from a sharp deterioration may be larger than the current subdued price action suggests, precisely because a worst-case escalation has not been fully priced in.

Iran’s proposal ties Strait reopening to three stated conditions:

The two-phase structure, with an immediate ceasefire and commercial reopening first and nuclear issues deferred to a 15-20 day subsequent window, represents Iran’s strongest offer to date. It is also the source of US hesitation. Deferring nuclear issues means Washington would need to offer de-escalation before resolving its core strategic concern, an arrangement that runs counter to the Trump administration’s stated posture.

White House statements on the Strait of Hormuz closure and ceasefire framework characterised the closure as completely unacceptable under the terms of the original ceasefire, a position that clarifies why the Trump administration has resisted Iran’s two-phase proposal despite the active backchannel communications that both sides have acknowledged.

The collapse of in-person talks does not mean all communication has stopped. Several channels remain active:

Geopolitical analysts assess a low likelihood of immediate success without a firm Iranian commitment. The gap between Iran’s conditions and the current US posture explains why traders are not treating this proposal as a near-term resolution event. Investors should monitor State Department press briefings and diplomatic reporting for the next confirmed development rather than treating the proposal as a concluded deal.

This situation carries material upside and downside scenarios that remain unresolved. A formal proposal exists. Backchannel communications continue. But no binding agreement has been reached, and the Strait remains restricted as of 27 April 2026. For investors tracking energy costs, equity market direction, and geopolitical risk, this is a developing story where the next confirmed diplomatic milestone, whether progress or breakdown, could move commodity and equity markets sharply. State Department briefings, Energy Information Administration (EIA) disruption reports, and Reuters diplomatic updates are the sources to watch.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and diplomatic outcomes.

The Strait of Hormuz is a narrow sea passage between Iran and Oman through which approximately 20% of the world's daily oil supply transits, making it the single most consequential chokepoint in global energy infrastructure. Any closure or restriction immediately tightens physical supply and drives crude prices higher, as no alternative route of equivalent capacity exists for Gulf producers.

Iran's latest proposal ties Strait reopening to three conditions: an end to US blockades of Iranian ports, broader ceasefires including the Lebanon ceasefire, and no requirement for immediate nuclear concessions in the early phases of any agreement. The two-phase structure defers nuclear issues to a 15-20 day subsequent window after an initial commercial reopening.

As of 27 April 2026, Brent crude is trading near $94-96 per barrel and WTI near $92-94 per barrel, both elevated relative to pre-crisis levels as markets price in the ongoing supply disruption. Traders are not treating Iran's latest proposal as a near-term resolution, given that in-person talks collapsed on 25 April and Iran has already re-closed the Strait once following a prior ceasefire.

Investors should watch State Department press briefings, Energy Information Administration disruption reports, and diplomatic reporting from Reuters for the next confirmed milestone in US-Iran negotiations. Key channels still active include direct text-message communications between US envoy Steve Witkoff and Iranian Foreign Minister Araghchi, as well as Pakistan's continued role as primary intermediary.

A confirmed reopening agreement would likely trigger a broad equity market rally, with falling energy costs expected to improve margins across transport, manufacturing, and consumer sectors, while energy equities could face price pressure as crude falls. Conversely, further escalation or a collapse of the current proposal could sharply reprice markets, as a worst-case scenario has not been fully priced into current equity valuations.