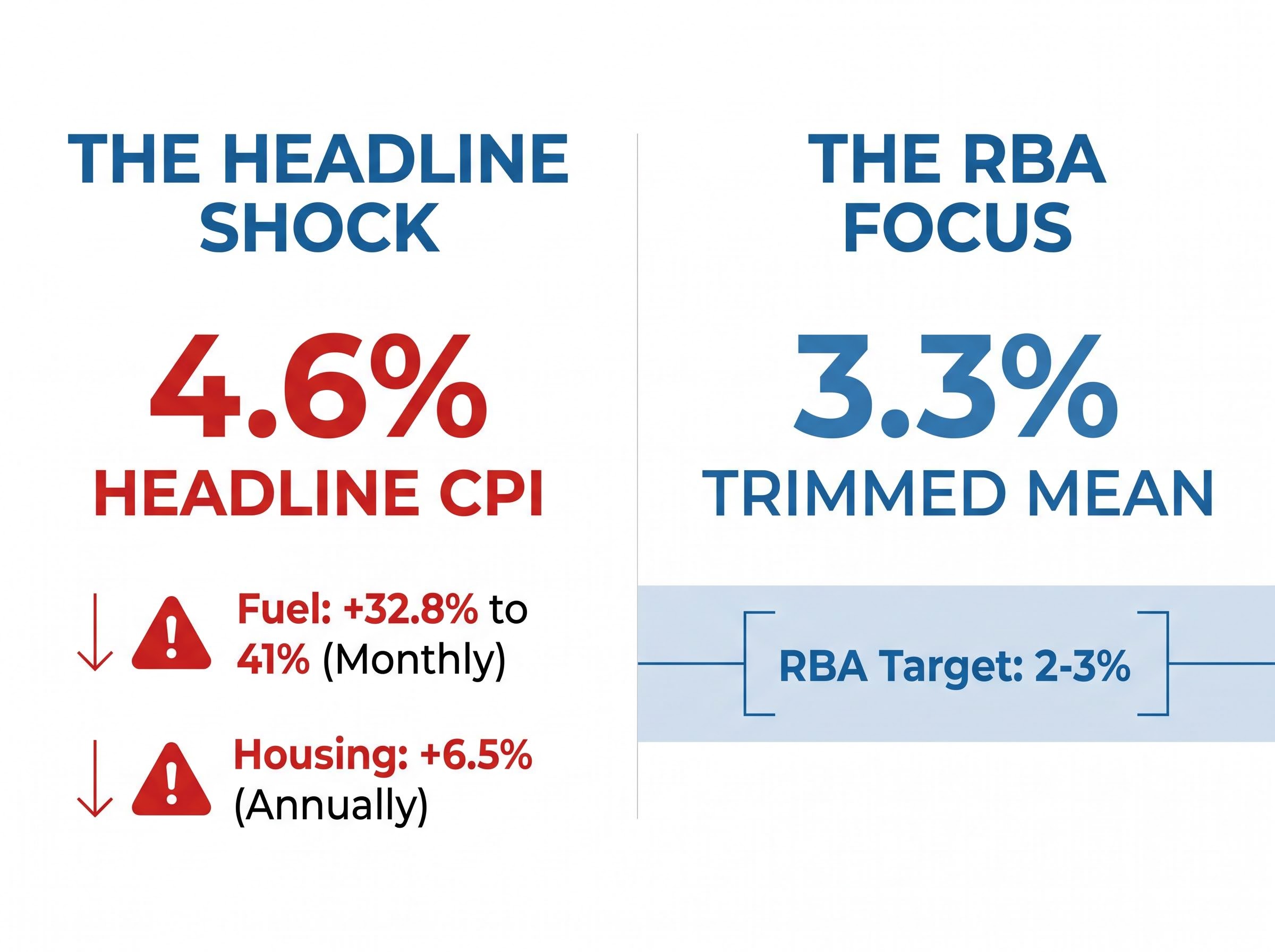

Australia’s annual inflation rate surged to 4.6% in March 2026, its highest reading since late 2023, driven by a 32.8%-41% monthly spike in fuel prices and persistent 6.5% annual growth in housing costs. The data, released on 29 April, landed like a jolt through Australian financial markets, triggering a seven-session losing streak on the ASX 200 and pushing market-implied odds of a 25 basis point RBA rate hike on 5 May to 76%.

The question for Australian investors is no longer whether rates will rise. It is what tightening from here means for portfolios, mortgage repayments, and the sectors most exposed to a consumer spending pullback. What follows is an analysis of the inflation drivers behind the March CPI print, how the RBA’s rate decision transmits through equities, the Australian dollar, and household budgets, and what the data environment signals for the remainder of 2026.

What the March CPI surge actually tells us about Australian inflation

The headline number is alarming. Annual CPI accelerated to 4.6% in March, up from 3.7% in February, with the monthly reading coming in at +1.1%. Transport prices rose 8.9% year-on-year. But the headline figure overstates the breadth of the inflationary pressure, and understanding why matters for reading what the RBA does next.

The ABS Consumer Price Index release for March 2026 confirmed headline CPI at 4.6% and trimmed mean inflation at 3.3%, with housing costs rising 6.5% annually, data that sits at the centre of the RBA’s May rate deliberations.

The dominant driver was fuel. Monthly fuel prices surged between 32.8% and 41%, an energy-driven shock concentrated in a single volatile input rather than a signal of broad-based demand overheating. Strip that away, and the inflation picture changes materially.

Housing tells a different story. Costs rose 6.5% annually, with rents increasing 0.2% monthly and new dwelling costs up 0.5% in the month. This is the structurally embedded component, the part of the inflation problem that does not resolve when oil prices stabilise.

The fuel shock is the dominant driver of the March headline, but electricity costs and construction inflation add a second layer of structural pressure that is less visible in the CPI table: electricity prices rose 25.4% annually following the lapse of the Energy Bill Relief Fund, and new dwelling construction costs accelerated to 0.48% month-on-month in March, more than triple February’s rate.

| CPI Component | Annual Change | Monthly Change | RBA Classification |

|---|---|---|---|

| Headline CPI | 4.6% | +1.1% | Headline measure |

| Fuel | — | +32.8%-41% | Volatile |

| Transport | +8.9% | — | Volatile |

| Housing | +6.5% | — | Structural |

| Rents | — | +0.2% | Structural |

| New Dwellings | — | +0.5% | Structural |

| Trimmed Mean | 3.3% | — | Core measure |

Why the trimmed mean is the number the RBA actually watches

The trimmed mean strips out the most extreme price movements at both ends of the distribution, removing exactly the kind of fuel-driven spike that inflated the March headline. At 3.3% annually and +0.8% for Q1 2026, it sits above the RBA’s 2-3% target band but tells a far less dramatic story than 4.6%.

This is the figure that sustains the rate hike case. Even if fuel prices normalise over coming months, trimmed mean inflation above the target band gives the RBA grounds to tighten. Investors who track only the headline number risk misjudging both the severity and the likely policy response.

When big ASX news breaks, our subscribers know first

How the RBA cash rate works and why 25 basis points matters

The RBA cash rate is the interest rate on overnight loans between banks. It functions as the benchmark from which commercial lending rates are priced across the economy, and variable-rate mortgages are the most direct transmission mechanism to households.

The chain works in three steps:

- The RBA sets the cash rate target, currently 4.10% (effective 18 March 2026), which determines the cost of interbank lending.

- Banks reprice variable mortgage rates in response, typically passing through the full change within weeks of the decision.

- Higher repayments reduce household disposable income, which in turn constrains consumer spending across the economy.

A 25 basis point increase, from 4.10% to 4.35%, sounds marginal in isolation. For a household with a typical variable-rate mortgage, it adds directly to monthly repayment obligations at a point when budgets are already stretched by fuel and housing costs. The compounding effect matters: rate changes take 12-18 months to work fully through the economy, meaning the impact of the March rate setting has not yet been fully absorbed.

RBA research on monetary policy transmission lags confirms that the peak effect of a rate change typically materialises after one to two years, which means the cumulative tightening already in place continues to work through household budgets and credit conditions well beyond the May decision.

CommBank characterised the May decision as “finely balanced,” acknowledging elevated inflation and higher energy prices alongside softer consumer confidence (CommBank, April 2026 research).

Markets, as of 28-30 April 2026, are pricing a 76% probability that the RBA proceeds with the hike. The decision lands on 5 May.

What a rate hike would do to Australian equities

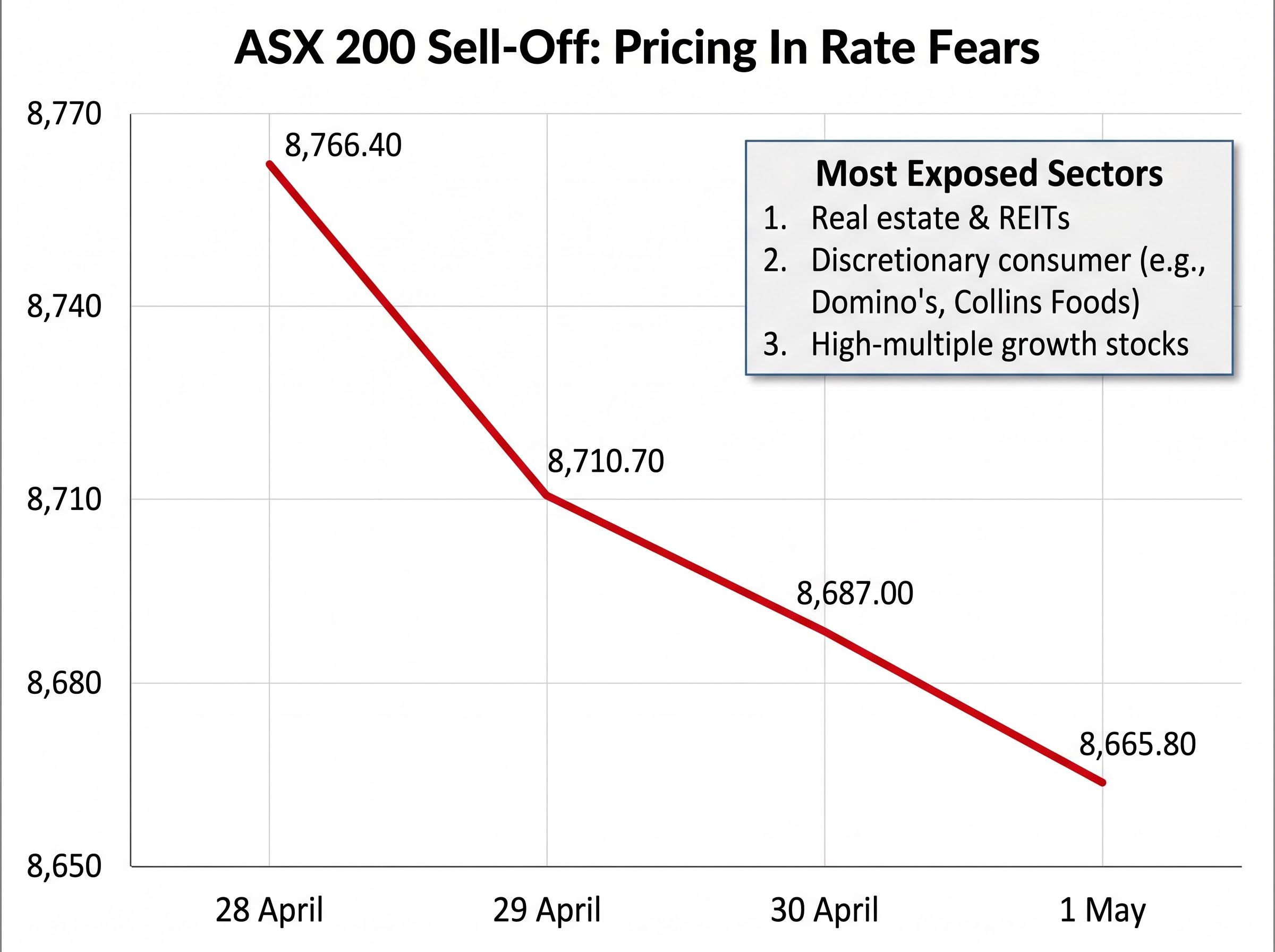

The ASX 200 did not wait for the RBA. From its 28 April close of 8,766.40, the index fell across four consecutive sessions: 8,710.70 on 29 April, 8,687.00 on 30 April, and 8,665.80 on 1 May. The seven-session losing streak confirmed through 29 April represents the market’s attempt to price in a rate environment that shifted materially with a single CPI release.

This is not generic risk-off sentiment. It is a domestic rate repricing story, and its effects are not evenly distributed across sectors.

Which sectors face the most pressure in a higher-rate environment

Three sectors stand most exposed to a rate increase, ranked by the directness of the impact:

The rate repricing story on the ASX has a mirror image: while REITs and discretionary stocks face the headwinds described above, ASX energy sector performance has been the inverse, with Woodside, Santos, and Karoon Energy posting gains of approximately 40% year-to-date as oil-indexed LNG revenues track Brent crude higher.

- Real estate and REITs face the most immediate pressure. Higher interest rates expand capitalisation rates, which compresses property valuations mechanically. REITs carrying variable-rate debt also face rising financing costs.

- Discretionary consumer stocks are already showing early behavioural signals. Share prices in Domino’s and Collins Foods declined in the sessions following the CPI release, reflecting investor expectations that household spending will contract further under higher rates and elevated living costs.

- High-multiple growth stocks face valuation pressure as higher discount rates reduce the present value of future earnings. Companies priced on long-duration cash flow expectations are most sensitive to shifts in the rate outlook.

Financials occupy a more complex position. Banks often benefit from wider net interest margins in the near term following a rate hike, as variable lending rates reprice faster than deposit rates. A prior RBA rate decision in the current tightening cycle saw the ASX 200 settle 0.2% lower on decision day, consistent with equity markets absorbing rate moves as a net negative at the index level even when individual sectors benefit.

The Australian dollar in a rising rate environment

Conventional logic holds that a rate hike should strengthen the Australian dollar. Higher domestic rates attract capital from investors seeking yield, widening the interest rate differential against peers and supporting demand for the currency. The logic is sound. It is also incomplete.

The AUD functions as a risk-sensitive currency, heavily influenced by global risk appetite and commodity prices. A rate hike driven by an energy supply shock introduces competing forces:

- Interest rate differential: Supportive of AUD strength if the RBA tightens while other major central banks hold.

- Global risk appetite: Variable, and currently uncertain given the geopolitical dynamics underlying the energy price spike.

- Commodity price outlook: Linked directly to the same energy shock driving Australian inflation, creating a feedback loop rather than a clean supportive signal.

As of 1 May 2026, AUD/USD was trading in the 0.7191-0.7203 range.

Key technical levels (attributed to Vantage Markets analyst Hebe Chen): Support at 0.7160 (former resistance, now converted). A break above 0.7230 targets 0.7300 at the upper channel boundary. Downside support sits at 0.7095 (20-day SMA) and then 0.6985.

The rising channel structure remains intact, but a rate decision alone is unlikely to resolve the competing pressures on the currency. For investors with offshore holdings or currency-hedged fund exposure, the AUD’s direction will depend as much on global commodity dynamics as on the RBA’s next move.

What stretched household budgets mean for the broader economy

The numbers stack up quickly. A variable-rate mortgage holder already absorbing the 4.10% cash rate faces fuel prices that rose 32.8%-41% in a single month, housing costs running 6.5% higher annually, and rents climbing 0.2% each month. A further 25 basis point increase adds directly to that burden.

The behavioural signals are already visible. CommBank noted visibly strained household budgets, weaker consumer confidence, and early signs of cracks in the housing market as of April 2026. ANZ pointed to a discretionary spending pullback evident in consumer-facing sectors, with share price declines in Domino’s and Collins Foods reflecting reduced appetite for non-essential spending.

| Cost Category | Current Pressure | Change | Impact Type |

|---|---|---|---|

| Fuel | Severe | +32.8%-41% monthly | Direct household cost |

| Housing | Elevated | +6.5% annually | Direct household cost |

| Rents | Elevated | +0.2% monthly | Direct household cost |

| Mortgage rates | High (potential increase) | 4.10% → 4.35% | Indirect via rates |

The RBA’s impossible calculus

The policy tension is acute. Rate hikes are the RBA’s tool for reducing inflation, but a significant portion of the current inflation is driven by supply-side energy shocks that higher interest rates cannot resolve. Raising rates constrains the spending of households whose budgets are already under pressure from the very price increases the RBA is responding to.

CommBank’s expectation of a pause after May suggests the central bank itself may recognise the limits of further tightening at this point. The risk of over-tightening into a consumer downturn is real, and consumer-facing sectors from retail to hospitality to property are the most exposed if household spending capacity deteriorates further.

For investors wanting to extend the analysis beyond rate decisions into the broader growth picture, our deep-dive into Australia’s recession risk indicators examines the per-capita GDP contraction already underway, the record corporate insolvency rate in 2025, and the Westpac-Melbourne Institute consumer confidence reading of 80.1 in April, the weakest since 1973, to assess whether Australia’s expansion is more fragile than headline GDP suggests.

The next major ASX story will hit our subscribers first

The rate outlook for the rest of 2026 and what investors should watch

CommBank’s base case, drawn from its April 2026 research, points to a 25 basis point hike on 5 May, taking the cash rate to 4.35%, followed by a pause. The pause reflects a judgement that cumulative tightening, elevated energy costs, and weakening consumer confidence argue against further increases absent new data surprises.

Three scenarios frame the rate path for the remainder of 2026:

- Hike then pause (CommBank base case): Cash rate reaches 4.35% in May and holds there as the RBA monitors inflation’s response to prior tightening.

- Hike then further hike: Energy prices remain elevated or wage growth accelerates beyond forecasts, pushing trimmed mean inflation higher and forcing additional tightening.

- No hike, followed by reassessment: Fuel prices normalise sharply before the May decision, allowing the RBA to hold at 4.10% and reassess in subsequent meetings.

The 76% market-implied probability of a hike suggests the first scenario is the consensus expectation, but the second remains a live risk while trimmed mean inflation sits at 3.3%, above the 2-3% target band.

Peak rate forecasts across major Australian banks diverge materially beneath the surface consensus on May: Westpac projects the cash rate reaching 4.85% by August through two further hikes, while NAB holds at 4.60%, a spread that represents a meaningful difference in mortgage repayment obligations for households planning through 2026 and 2027.

Three data releases investors should track post-May: The trimmed mean CPI trajectory (the RBA’s preferred inflation gauge), the Wage Price Index (for signs of a wage-price feedback loop), and the Westpac-Melbourne Institute Consumer Sentiment monthly release (for real-time household confidence readings). These are available through rba.gov.au media releases, ABS CPI releases, and the Westpac-Melbourne Institute monthly publication.

Australia’s inflation test is far from over

The March 2026 CPI print represents a genuine inflection point, not a statistical anomaly. Whether driven by a single volatile input or not, the data has shifted the rate outlook, repriced Australian equities, and placed additional strain on household budgets already absorbing multi-source cost pressures.

For investors, the practical takeaways are clear. Rate-sensitive sectors face headwinds that are now being priced in real time. The Australian dollar has technical support but faces fundamental uncertainty from the same energy dynamics driving inflation. Household spending capacity is under simultaneous pressure from fuel, housing, and the prospect of higher mortgage rates.

The 5 May RBA decision matters, but the statement accompanying it may matter more. The language will signal whether a pause or continued tightening is the base case, making the post-decision commentary as important as the rate move itself.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.