Lululemon Fundamental Analysis: the Price of Brand Dilution

2 hrs ago

Wall Street rarely rewards a company for shrinking its operational footprint, yet a stock surge following recent earnings suggests investors are celebrating exactly that. As of April 29, 2026, the e-commerce sector is experiencing a massive structural realignment. The strategic transaction where Etsy sells Depop to a major rival for $1.2 billion has fundamentally recalibrated market expectations for peer-to-peer retail valuations.

This analysis deconstructs the financial and strategic mechanisms driving this divestiture. Shedding a high-growth asset provides one marketplace with the capital to secure unprecedented core profitability. Simultaneously, the acquisition grants the buyer immediate control over the highly lucrative Gen Z demographic, shifting competitive balances across the digital retail sector.

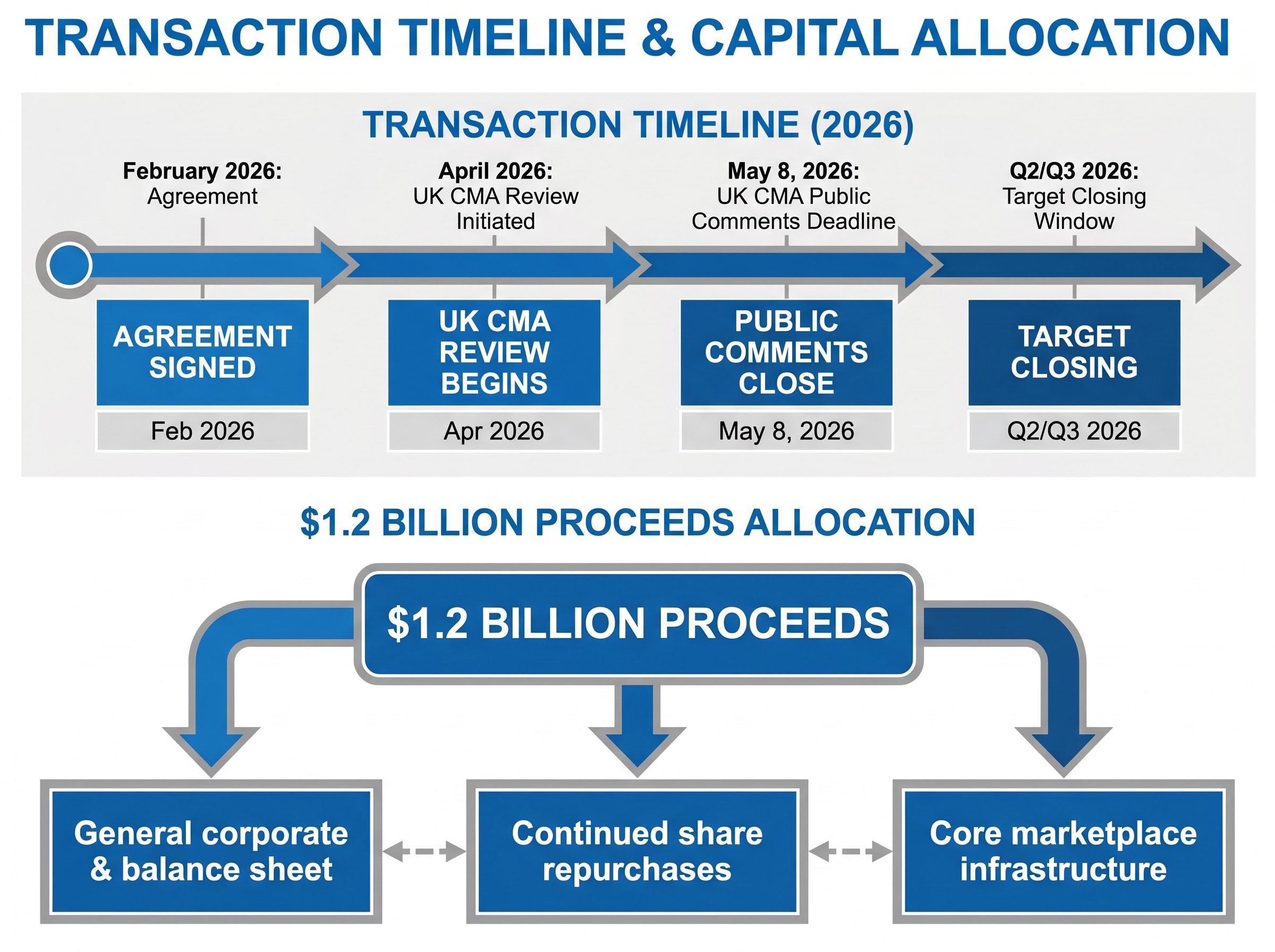

The February 2026 agreement represents a deliberate subtraction engineered to accelerate baseline growth. Securing a $1.2 billion valuation for the fashion subsidiary provides the parent company with a significant liquidity event. Management structured this transaction not as a distress sale, but as a calculated capital reallocation designed to fund highly specific internal priorities.

The stated uses for the $1.2 billion proceeds include:

General corporate purposes and balance sheet reinforcement Continued share repurchase programmes to drive shareholder value * Direct investment into the core marketplace infrastructure for creative goods

This divestiture aligns with a historical pattern of platform streamlining. The company previously executed a similar consolidation strategy with its 2025 Reverb transaction, proving that management is willing to exit secondary markets when core platform margins require attention.

Financial analysts view the move as a bullish narrative sharpener. Consensus data from TipRanks and Yahoo Finance indicates the strategy clarifies the company’s long-term market story. The transaction is currently targeting a completion window in Q2 2026, setting up a definitive timeline for capital deployment. Understanding these explicit terms provides the necessary foundation for evaluating why the market responded with such immediate positive sentiment.

The immediate pre-market share surge following the announcement highlighted how strongly capital allocators value the company’s commitment to maintaining elevated profitability ratios over complex portfolio management.

Operating a unified retail platform requires a fundamentally different operational structure than managing a segmented e-commerce portfolio. A unified platform leverages a single technical backend, one consolidated marketing budget, and a uniform customer acquisition strategy. Conversely, a multi-platform portfolio forces a parent company to maintain distinct technical infrastructures and entirely separate marketing campaigns to reach different demographics.

Integrating completely different user bases often dilutes aggregate profit margins. A niche subsidiary may generate rapid top-line revenue growth, but the bespoke marketing spend required to maintain that growth frequently outpaces the returns. When an e-commerce giant acquires a high-growth startup, it typically seeks to scale the platform rapidly before spinning it off once the capital requirements conflict with the parent company’s profitability targets.

Financial Valuation Perspective Institutional investors frequently apply a valuation discount to multi-brand retail ecosystems, favouring the predictable margin expansion of a singular, integrated marketplace over the complex capital allocation required to support disparate user bases.

This dynamic explains why institutional capital prefers pure-play profitability over complex ecosystem management. Shedding a high-maintenance subsidiary allows executives to redirect engineering and marketing resources exclusively toward their most profitable user base. For retail investors, this translates into higher margins, simplified earnings reports, and a clearer pathway to sustained dividend growth or share buybacks.

The April 29, 2026, earnings release provided immediate numerical validation for the simplified operating model. Operating on a continuing operations basis that excluded the offloaded subsidiary, the core marketplace demonstrated marked efficiency improvements. The company successfully expanded active merchant numbers, acquired fresh consumers, and increased average spending per individual user in a single quarter.

This positive metric shift is particularly significant for shareholders, officially ending a 24-month stagnation in active shopper growth and indicating that the core platform is recovering its organic appeal.

This renewed transaction volume growth directly correlates with the subsequent stock valuation increase. The market absorbed the data and rewarded the demonstrated ability to generate higher margins from a leaner operational base.

| Metric | Actual Result | Wall Street Estimate | Variance |

|---|---|---|---|

| Top-Line Revenue | $631 million | $620.9 million | Beat by 1.6% |

| Adjusted EBITDA Margin | Not Specified | Margin Expansion | |

| Transaction Volume | Not Specified | Up 5.5% Annual | |

| Adjusted Per-Share Profit | $0.61 | Miss by $0.01 |

Management provided optimistic operational forecasts for the remainder of the calendar year based on the Q1 momentum. According to reports, the company projects Q2 transaction volume to reach between $2.48 billion and $2.53 billion. Furthermore, executives anticipate full-year adjusted EBITDA margins will remain elevated, stabilizing between 28% and 30% as the core platform absorbs the benefits of redirected capital.

For eBay, the acquiring entity, this transaction represents a calculated strike to guarantee future relevance in the consumer-to-consumer apparel sector. The acquisition immediately secures 7 million active buyers, with 90% of that demographic falling under the age of 34.

The acquired platform generated $1 billion in annual Gross Merchandise Sales (GMS) in 2025, demonstrating nearly 60% year-over-year growth in the US market. This momentum synergises effectively with the buyer’s existing infrastructure. The acquiring platform already commands over $10 billion in annual fashion Gross Merchandise Volume (GMV).

| Platform | Active User Base | Gen Z Focus Percentage | Annual GMV / Revenue |

|---|---|---|---|

| Depop | 10M (7M Buyers, 3M Sellers) | 90% (Under 34 years old) | $1B GMS (2025) |

| eBay Fashion | Not Separately Disclosed | Broad Demographic Integration | $10B GMV (2025) |

| Vinted | 105M Registered Globally | Broad Demographic Integration | $1.1B Revenue (2025) |

Integrating these assets provides specific structural advantages for the parent company:

By absorbing a primary competitor, the buyer strengthens its defensive position against European rivals like Vinted, which boasts 105 million global users. Investors assessing the highly lucrative secondhand apparel market can evaluate this consolidation as a definitive shift in sector power dynamics.

For readers wanting to examine the broader industry implications, our comprehensive walkthrough of the Depop divestiture explores the strategic bifurcation of the digital retail market and details the potential breakup fees involved if regulatory hurdles block the deal.

Despite the strategic alignment between the two corporations, the transaction faces expected bureaucratic friction before the projected close. As of late April 2026, the apparent lack of US Federal Trade Commission delays contrasts sharply with active scrutiny occurring in European markets. International competition watchdogs frequently impact completion timelines for US-based corporate mergers, requiring investors to monitor overseas developments closely.

The UK Competition and Markets Authority (CMA) officially initiated a review of the acquisition in April 2026. This regulatory process introduces a necessary reality check for shareholders modeling immediate capital deployment.

The updated CMA merger control jurisdiction and procedures grant regulators expanded oversight regarding how international technology consolidations impact digital retail competition. This rigorous framework requires parent companies to provide extensive compliance documentation before securing final approval for cross-border asset transfers.

Regulatory Milestone Watch The UK CMA has established May 8, 2026, as the deadline for public comments regarding potential competition impacts. This date serves as the next critical milestone for assessing deal completion risks.

Despite this overseas review, both companies have confirmed that the Q2 2026 closing target remains official.

This $1.2 billion transfer of assets signals a broader trend of specialisation across the US e-commerce sector. The transaction functions as a dual-win mechanism, allowing one platform to achieve required profitability margins while the other secures necessary demographic growth. The $631 million Q1 core revenue beat serves as immediate proof of concept that subtraction can drive valuation multiples.

Moving forward, the Gen Z demographic shift will continue to dictate the future of recommerce. As the Q3 2026 closing deadline approaches, market participants will monitor the CMA regulatory timeline to confirm the final transfer of capital.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Etsy sold Depop for $1.2 billion to simplify its operational footprint, focus on core platform profitability, and reallocate capital towards general corporate purposes, share repurchase programs, and core marketplace infrastructure.

The sale provides Etsy with significant liquidity, enabling investments in its core business and continued share buybacks, which management projects will lead to elevated full-year adjusted EBITDA margins between 28% and 30%.

eBay acquired Depop for $1.2 billion to secure a dominant position in the Gen Z recommerce sector, gaining 7 million active buyers under 34 years old and expanding its fashion Gross Merchandise Volume.

The transaction is under scrutiny by international competition watchdogs, specifically the UK Competition and Markets Authority (CMA), which has initiated a review with a public comment deadline of May 8, 2026.