ASIC Fines Three ASX Companies $1.17m for Missing Annual Reports

11 hrs ago

In late April 2026, two prominent beverage equities are trading below their historical maximums, yet financial markets are pricing their futures with vastly different multiples. Despite both companies posting aggressive top-line revenue growth over the past twelve months, their trajectories diverged sharply following the 2025 Celsius Holdings acquisition of Alani Nu and the relentless domestic unit expansion by Dutch Bros. Evaluating a Celsius vs Dutch Bros stock position requires a clear, data-backed framework to assess whether the deep discount of a portfolio brand outweighs the premium price of a physical drive-thru operator. The current market environment heavily penalises operational friction while rewarding highly visible revenue predictability. This analysis examines the immediate trading realities, fundamental scaling models, and Wall Street consensus for both equities. Investors must navigate complex financial metrics and valuation multiples to determine which growth strategy aligns with their capital allocation tolerance. By triangulating forward projections with structural expansion metrics, market participants can better understand the distinct risk profiles inherent in these two very different beverage distribution models.

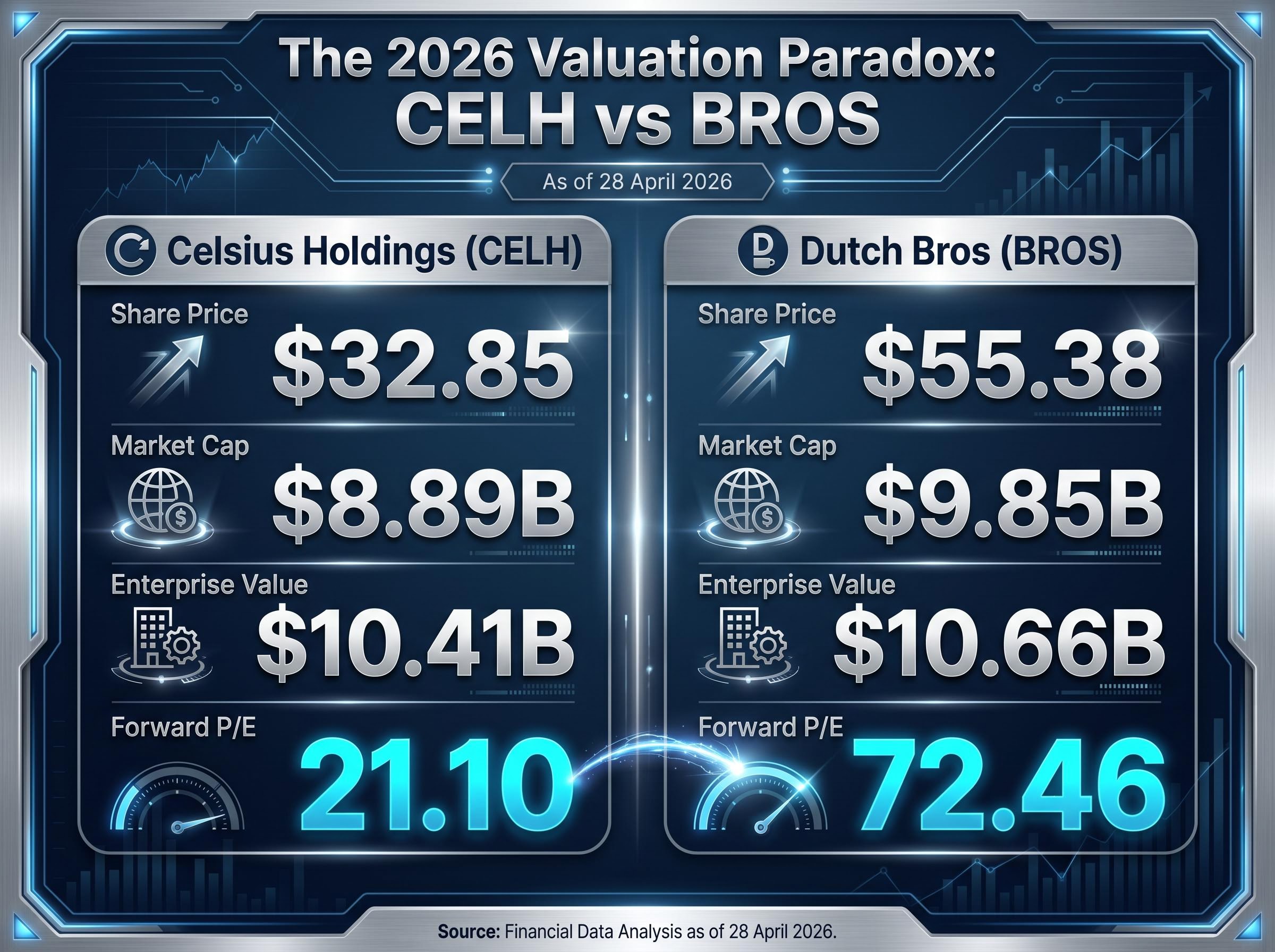

The current trading environment presents a stark contrast in market sentiment between these two beverage entities. Investors are paying heavily for physical growth predictability while heavily discounting wholesale product distribution. As of 28 April 2026, Celsius Holdings (CELH) and Dutch Bros (BROS) trade with a valuation gap that reflects fundamentally different market confidence levels regarding future execution.

Celsius trades at $32.85 with a market capitalisation of $8.89 billion and an enterprise value of $10.41 billion. In contrast, Dutch Bros trades at $55.38, carrying a $9.85 billion market capitalisation and a $10.66 billion enterprise value.

The divergence sharpens significantly when examining forward valuation multiples. Celsius currently trades at a forward P/E of 21.10, with its forward sales multiple sitting at 2.53x, a metric that is currently hovering near a five-year low. Dutch Bros commands a forward P/E of 72.46, representing a massive premium that signals high market expectations for its operational pipeline.

| Company | Share Price | Market Cap | Enterprise Value | Forward P/E |

|---|---|---|---|---|

| Celsius Holdings (CELH) | $32.85 | $8.89B | $10.41B | 21.10 |

| Dutch Bros (BROS) | $55.38 | $9.85B | $10.66B | 72.46 |

Investors need to understand this baseline cost of entry before assessing whether the respective risk profiles justify these specific multiples. The pricing disparity indicates that markets currently view integration risk and structural expansion risk through entirely different analytical lenses.

These elevated specific multiples leave growth equities uniquely exposed to broader stock market warning signals, as heavily priced assets frequently face the sharpest corrections during macroeconomic contractions.

Before analysing specific equities, it helps to understand the fundamental mechanics separating a brand aggregation model from a controlled physical retail model. Scaling a brand portfolio involves acquiring and integrating external labels to capture broader consumer demographics and retail shelf space. Through the consolidation of CELSIUS, Rockstar, and Alani Nu, the company now commands approximately 20% of the tracked US energy drink category share.

Executing a successful multi-brand strategy at this scale requires continuous product innovation to prevent internal cannibalisation while defending premium supermarket placements against established global competitors.

Scaling a physical retail model operates differently, relying on geographic unit expansion and menu integration rather than wholesale distribution dominance. Growth in this retail category is driven by the compounding value of same-store sales growth combined with aggressive physical footprint expansion.

Financial markets assign higher structural safety premiums to physical unit expansion because owned retail locations build geographic economic moats. Wholesale beverage distribution faces fierce sector rivalry on third-party retail shelves, whereas owned drive-thrus capture dedicated customer traffic.

These distinct growth engines carry specific operational liabilities:

Brand Aggregation Risk: Profit margins can compress rapidly due to external label integration costs, supply chain consolidation, and intense competition for limited supermarket shelf space. Physical Expansion Risk: Top-line growth depends on heavy capital expenditure for new real estate, construction delays, and the challenge of replicating successful unit economics in unproven geographic territories.

The recent market punishment of Celsius stems directly from the financial impact of the 2025 Alani Nu acquisition. Integration friction has temporarily suppressed operating margins, causing the stock to plunge 35.6% over a recent three-month period and drop 8.41% over a trailing 30-day stretch. This severe selloff reflects immediate market concerns over supply chain consolidation and margin compression.

Despite this operational volatility, the forward revenue and profit projections present a compelling value-recovery scenario for patient capital. The company posted FY25 revenue of $2.52 billion, representing an 85.5% year-over-year increase that highlights underlying consumer demand.

The financial disclosures within the official Celsius SEC annual report confirm these growth figures while providing granular detail on the specific supply chain consolidation expenses that have temporarily suppressed operating margins.

Consensus estimates for FY26 project aggregate revenue scaling further to between $3.21 billion and $3.38 billion. Furthermore, according to external estimates, forward forecasts show a 55% improvement in diluted per-share profits spanning 2026 through 2028.

The current trading position represents a potential value-recovery play for investors willing to absorb short-term operational volatility. Analyst consensus views the stock as deeply undervalued relative to its historical sales multiples.

Analyst Consensus and Fair Value Assessment Fair value estimates currently sit at $55.43, with a Wall Street mean target of $66 and high-end estimates reaching $85, suggesting a clear disconnect between the company’s top-line growth and its punished stock price.

Unpacking this valuation disconnect helps investors identify whether the recent selloff represents a structural decline or a mathematically sound entry point. The reality of its deep discount provides a measurable margin of safety against further multiple compression.

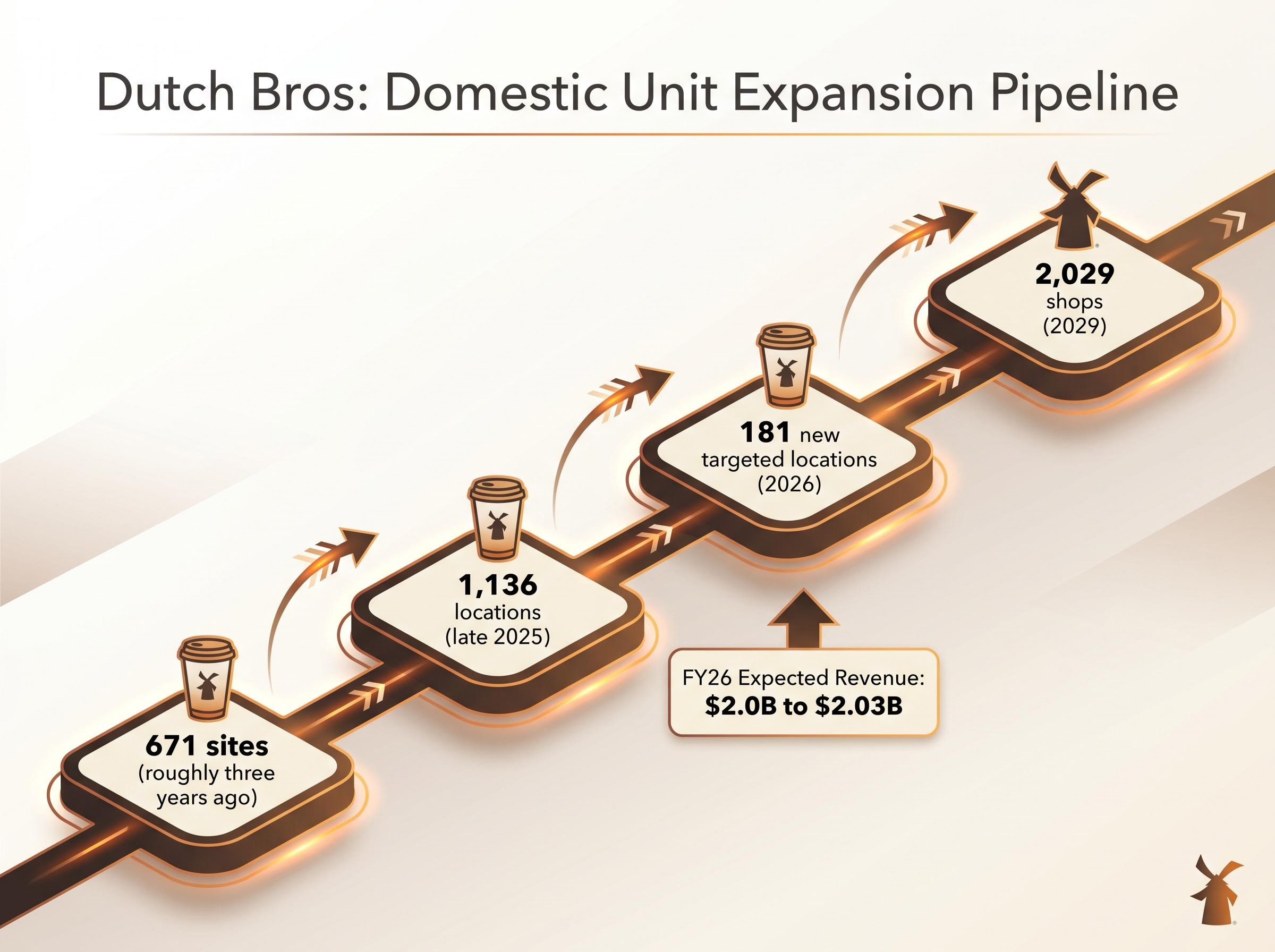

The justification for a 72.46 forward P/E lies in the highly visible, structurally safer growth pipeline of physical retail. Dutch Bros is executing an aggressive domestic unit expansion strategy that directly fuels predictable top-line momentum across its geographic footprint. By controlling the entire retail environment, the company isolates its revenue streams from the wholesale shelf-space competition affecting traditional beverage manufacturers.

Food integration and proprietary loyalty programmes serve as primary catalysts for driving comparable retail transactions. These specific menu enhancements and customer retention initiatives are expected to generate same-store sales growth of 3% to 5% in 2026.

This compounding effect of adding new units while increasing the transaction yield of existing locations creates a highly visible revenue trajectory. The company projects FY26 revenue of $2.0 billion to $2.03 billion, rewarding investors with tangible operational metrics that prevent the momentum stock from being classified as a speculative bubble.

The sequential growth targets outline the exact mechanics of this physical expansion strategy:

For readers wanting to understand how this massive physical footprint impacts profitability, our detailed coverage of Dutch Bros’ unit economics examines the capital expenditure requirements, commodity inflation risks, and margin structures underlying the 2029 expansion targets.

Allocating capital between these two equities requires weighing the immediate margin risks of brand integration against the execution risks of maintaining elevated valuation premiums. Celsius offers a highly discounted entry point, but investors must tolerate the operational friction of the Alani Nu integration process. Dutch Bros provides a safer physical expansion runway, yet buyers must pay a premium earnings multiple that leaves little room for quarterly revenue misses.

Wall Street analysts maintain strong buy ratings for both equities, though for entirely different structural reasons. DA Davidson maintains a $70 target for BROS, indicating 26% upside, while other consensus estimates sit at $68 (23% upside) with high estimates reaching $85 (53% upside).

This bullish Wall Street coverage on Dutch Bros frequently cites sustained same-store sales momentum and successful geographic scaling as the primary catalysts for maintaining premium valuation multiples.

Conversely, the CELH consensus features a Wall Street mean target of $66, with high-end estimates also peaking at $85. The comparative thesis centres on choosing between a momentum operator priced for perfection and a value-recovery asset punished for temporary integration friction.

Investors must base their final decision on their tolerance for volatility versus their appetite for paying premium multiples. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The decision between these two equities ultimately comes down to a choice between a deeply discounted energy drink manufacturer and a premium-priced coffee operator. Both entities represent significant growth assets trading well below their absolute historical peaks.

This premium pricing in the coffee space faces emerging threats, particularly as legacy competitors implement a multi-faceted turnaround strategy focused on digital engagement and enhanced loyalty programmes to reclaim lost market share.

Upcoming catalysts have the potential to shift current pricing dynamics and valuation multiples in the near term. Market participants should monitor the scheduled 13 May 2026 shareholder meeting for Dutch Bros, which may provide further visibility into the pace of their domestic expansion.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Celsius employs a brand aggregation model, scaling through acquisitions like Alani Nu and managing a multi-brand portfolio for wholesale distribution. Dutch Bros focuses on a physical retail model, expanding its footprint through new drive-thru locations and increasing same-store sales.

Celsius's stock dropped due to immediate market concerns over integration friction and suppressed operating margins following its 2025 acquisition of Alani Nu. Despite this, the company posted an 85.5% year-over-year revenue increase in FY25.

Investors should note Celsius's forward P/E of 21.10 and Dutch Bros' forward P/E of 72.46 as of April 2026. This significant disparity reflects differing market confidence in their respective growth models and risk profiles.

Dutch Bros is executing an aggressive domestic unit expansion, targeting 181 new drive-thru locations in 2026 and aiming for a long-term operational target of 2,029 shops by 2029. This strategy fuels predictable top-line momentum.