Crude Drops 4% on Hormuz Hopes, but the Deal Isn’t Done

9 hrs ago

Between 2019 and early 2024, Celsius Holdings delivered a staggering equity surge that redefined growth expectations within consumer equities. Now in April 2026, the US beverage sector demands a more calculated approach to capital allocation. Investors evaluating the merits of Celsius versus Dutch Bros stock face a choice between two entirely different operational frameworks fighting for consumer share.

Both consumer brands are navigating a crowded market environment where demand curves are flattening for legacy operators. The beverage market in early 2026 is characterised by shifting consumer preferences and rising input costs, making historical growth metrics less reliable for future forecasting. Market participants must distinguish between businesses built on rapid distribution scaling and those reliant on compounding physical assets.

Determining the optimal allocation through 2028 requires looking past surface-level revenue figures to understand the structural mechanisms driving their operations. This comparative analysis examines their distinct growth models, margin profiles, and current market valuations. The objective is to provide a definitive framework for positioning beverage portfolios based on verifiable unit economics rather than historical momentum.

To accurately assess these investments, one must first isolate the core operational architecture separating them. Celsius operates as an asset-light packaged goods distributor, a model that generates rapid market penetration without the capital burden of constructing physical stores. The company leverages third-party distribution networks, placing its inventory directly into convenience stores and fitness channels to capture the ongoing zero-sugar wellness trend.

This structure allows the business to scale its revenue rapidly while maintaining minimal physical infrastructure overhead. By avoiding the heavy capital expenditures associated with property acquisition, the firm can redirect cash flow into aggressive marketing campaigns and strategic brand acquisitions. This agility provides a significant structural advantage during periods of rapidly shifting consumer tastes.

Navigating these changing preferences requires acknowledging the broader economic outlook, where aggregate spending metrics often obscure the severe financial strain and savings drawdowns affecting mass-market consumers.

Dutch Bros, conversely, relies entirely on physical real estate and direct consumer interactions. Their model is heavily capital-intensive, requiring sustained investment to acquire land, construct drive-thru facilities, and train retail staff. The structural advantage of this physical retail approach is the organic brand recognition generated by every new location.

Once a location achieves operational maturity, it functions as an autonomous cash generator with predictable daily foot traffic. The physical presence builds a defensible competitive moat in local markets that packaged goods competitors struggle to replicate through grocery store end-caps alone.

Understanding these opposing structural foundations helps investors grasp why each company operates with vastly different profit margins and risk profiles. Evaluating an asset-light distributor against a physical retail chain requires distinct valuation frameworks. A direct comparison of top-line revenue without accounting for these architectural differences will lead to inaccurate investment conclusions.

Asset-light scaling offers the velocity to capture national market share swiftly when consumer demand aligns with product placement. Celsius has capitalised on this velocity by outsourcing its supply chain friction to established distribution partners. This approach maximises near-term margin expansion but leaves the product highly exposed to supermarket shelf competition.

Physical store construction is inherently slower, constrained by zoning approvals, construction timelines, and labour availability. Yet the strategy creates significant barriers to entry in local markets. A completed retail location secures territorial dominance, generating compounding daily cash flow that is largely insulated from grocery aisle brand switching.

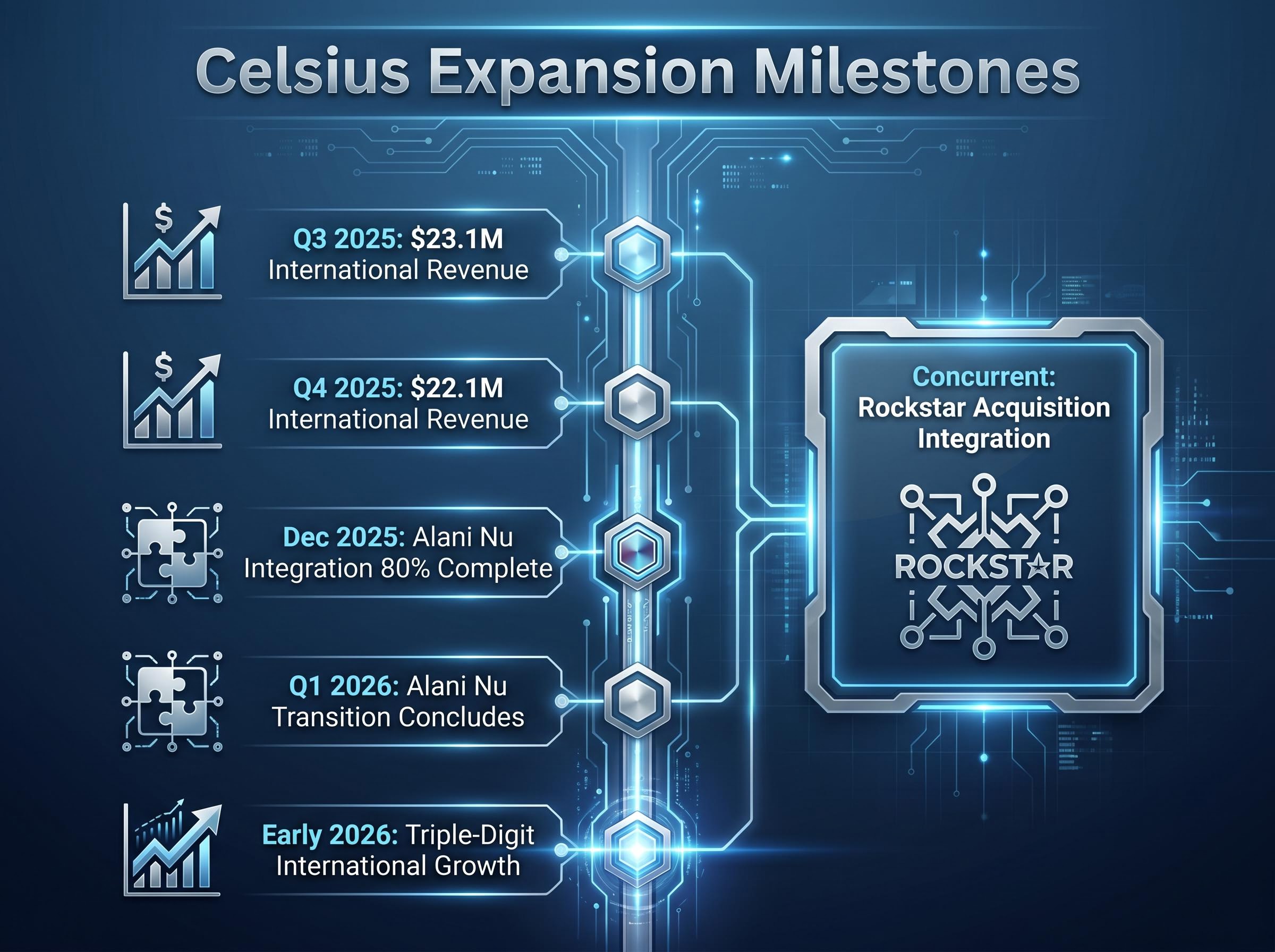

Celsius is actively executing an aggressive growth playbook designed to outpace intensifying sector rivalry. The company is defending its dominant North American base while securing new revenue streams through strategic brand integrations. Industry analysts report that the company’s ongoing mergers and acquisitions strategy is rapidly expanding its footprint across the broader energy drink category.

The execution timeline for this expansion is moving at an accelerated pace across multiple fronts.

Integration of the acquired Alani Nu brand reached 80% completion by December 2025. The final stages of the Alani Nu transition are on track to conclude by the end of Q1 2026. Integration of the Rockstar acquisition is proceeding concurrently to consolidate market share. International revenues climbed to $23.1 million in Q3 2025, before normalising at $22.1 million in Q4 2025.

These overseas initiatives are showing clear momentum in early 2026. The company has reported triple-digit international growth in the first quarter, driven by a deliberate push into European and Australasian markets. Securing shelf space in international supermarkets requires significant upfront capital, but the resulting revenue streams offer higher profit margins once established.

Market consensus suggests these diversification initiatives will translate into substantial bottom-line results. Financial analysts project a jump in diluted per-share profits between 2026 and 2028. This data indicates to investors that the company is actively securing high-margin international revenue rather than relying solely on past domestic performance.

For investors looking to model the specific financial impact of these international initiatives, our detailed coverage of Celsius earnings forecasts breaks down the required synergy realisations and margin expansion targets needed to justify the company’s current valuation.

The growth narrative for Dutch Bros moves at the measured, predictable pace of physical infrastructure development. The company operates a territorial fortressing strategy, systematically densifying its presence in specific regions before expanding outward. According to company data, this deliberate unit growth roadmap reached 1,136 locations by early 2026, a substantial increase from just 671 sites three years prior.

Management plans to open 181 new stores throughout 2026, keeping the company aligned with its medium-term target of 2,029 sites by 2029. Analysts estimate the brand’s theoretical domestic capacity at 7,000 locations. Supporting this footprint expansion is a strategic evolution in how individual stores generate cash.

Strategic Shift in Per-Store Revenue The nationwide rollout of an expanded food menu, paired with the new Order Ahead digital system, has fundamentally altered unit economics by capturing a broader variety of dining occasions and driving increased average ticket sizes.

Historically reliant on beverage-only transactions, the operator identified food attachment as a primary mechanism for margin protection. The structural safety of this strategy is evident in the company’s consecutive quarters of comparable location revenue growth. The operator projects total 2026 revenue to land between $2.0 billion and $2.03 billion.

Formal guidance alongside historical comparable store sales figures are documented in the Dutch Bros SEC regulatory filings, giving investors transparent visibility into the capital required to sustain aggressive site expansion.

However, operating physical assets exposes the firm to immediate commodity pressures. To offset elevated coffee prices in early 2026, management has deployed strict cost management tactics across its supply chain. Investors evaluating this asset class must recognise that compounding physical assets offers predictable returns, but it demands continuous capital expenditure.

Corporate strategies ultimately distil into hard financial metrics, and the data separating these two equities is stark. As of April 2026, market pricing reflects the distinct structural differences between asset-light distribution and capital-intensive retail. The valuation profiles demand careful scrutiny from investors positioning portfolios for operational leverage.

Celsius commands an $8.38 billion market capitalisation supported by strong pricing power. The company operates with a trailing twelve-month (TTM) gross margin of 50.4%. Management has established a firm target of returning to low-50% margins by the end of 2026, demonstrating the inherent profitability of outsourcing physical infrastructure.

These profitability metrics are detailed within the Celsius Holdings SEC filings, which outline the financial mechanics of their third-party distribution network and the resulting operational leverage.

Dutch Bros carries a slightly higher market capitalisation of $9.2 billion, but operates with a TTM gross margin of just 25.9%. This lower margin profile is the direct cost of maintaining physical retail sites and managing extensive front-line staffing. In exchange for these compressed margins, the market awards the drive-thru operator a structural safety premium based on its tangible real estate assets and consistent foot traffic.

Consensus forecasts reveal a significant divergence in expected returns.

| Metric Category | Celsius Data | Dutch Bros Data | Margin Profile (TTM) | Projected Upside |

|---|---|---|---|---|

| Core Financials | $32.62 Price / $8.38B Cap | $55.38 Price / $9.2B Cap | 50.4% | 102% |

| Analyst Estimates | $65.89 Consensus Target | $75.65 to $77.17 Target | 25.9% | 36% to 38% |

The massive projected upside for the packaged goods operator reflects its international expansion potential and high operational leverage. The $65.89 target price reflects confidence in the firm’s ability to maintain premium pricing while absorbing acquired brands into its distribution network. The drive-thru chain offers a steadier, more compressed return profile anchored by consistent same-store sales growth.

Capital allocation in the current consumer equity market requires aligning risk tolerance with the specific structural advantages of each business. Celsius offers aggressive margin power, outsized international upside, and a rapid M&A integration timeline. The asset-light framework allows it to generate high returns on invested capital, though it remains exposed to shelf-space competition.

Dutch Bros provides predictable domestic retail scale, compounding the value of its physical real estate over time. The company trades at a lower margin profile but rewards investors with the structural safety of a continuously expanding national footprint. Investors seeking high-velocity growth may favour the packaged goods model, while those prioritising tangible asset compounding are better served by the retail fortressing approach.

These two consumer titans will continue to influence the broader beverage sector through 2028 by pulling market share away from legacy operators. Past performance does not guarantee future results, and financial projections are subject to changing consumer sentiment and market conditions. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

This ongoing market share transition forces established incumbents to implement aggressive legacy operator turnaround strategies focused on digital engagement and store efficiency to defend their remaining footprint.

Celsius operates an asset-light, third-party distribution model for packaged goods like energy drinks, focusing on rapid market penetration, while Dutch Bros employs a capital-intensive physical retail strategy with drive-thru locations.

Celsius Holdings reports a trailing twelve-month gross margin of 50.4%, reflecting its asset-light structure. Dutch Bros, conversely, has a 25.9% gross margin due to the costs associated with maintaining physical retail sites and staffing.

Celsius is pursuing aggressive M&A, with Alani Nu and Rockstar integrations nearing completion, and expanding internationally into European and Australasian markets, aiming for higher profit margins from these new revenue streams.

Dutch Bros aims to reach 2,029 locations by 2029 from 1,136 in early 2026. Improvements in unit economics are expected from a nationwide expanded food menu and the new Order Ahead digital system.

Analysts project a 102% upside for Celsius Holdings to a target price of $65.89, driven by its international potential and operational leverage. Dutch Bros is projected to have a 36% to 38% upside to $75.65-$77.17, offering a more compressed return profile.