Record Highs Are Not the Risk Most Investors Think They Are

5 hrs ago

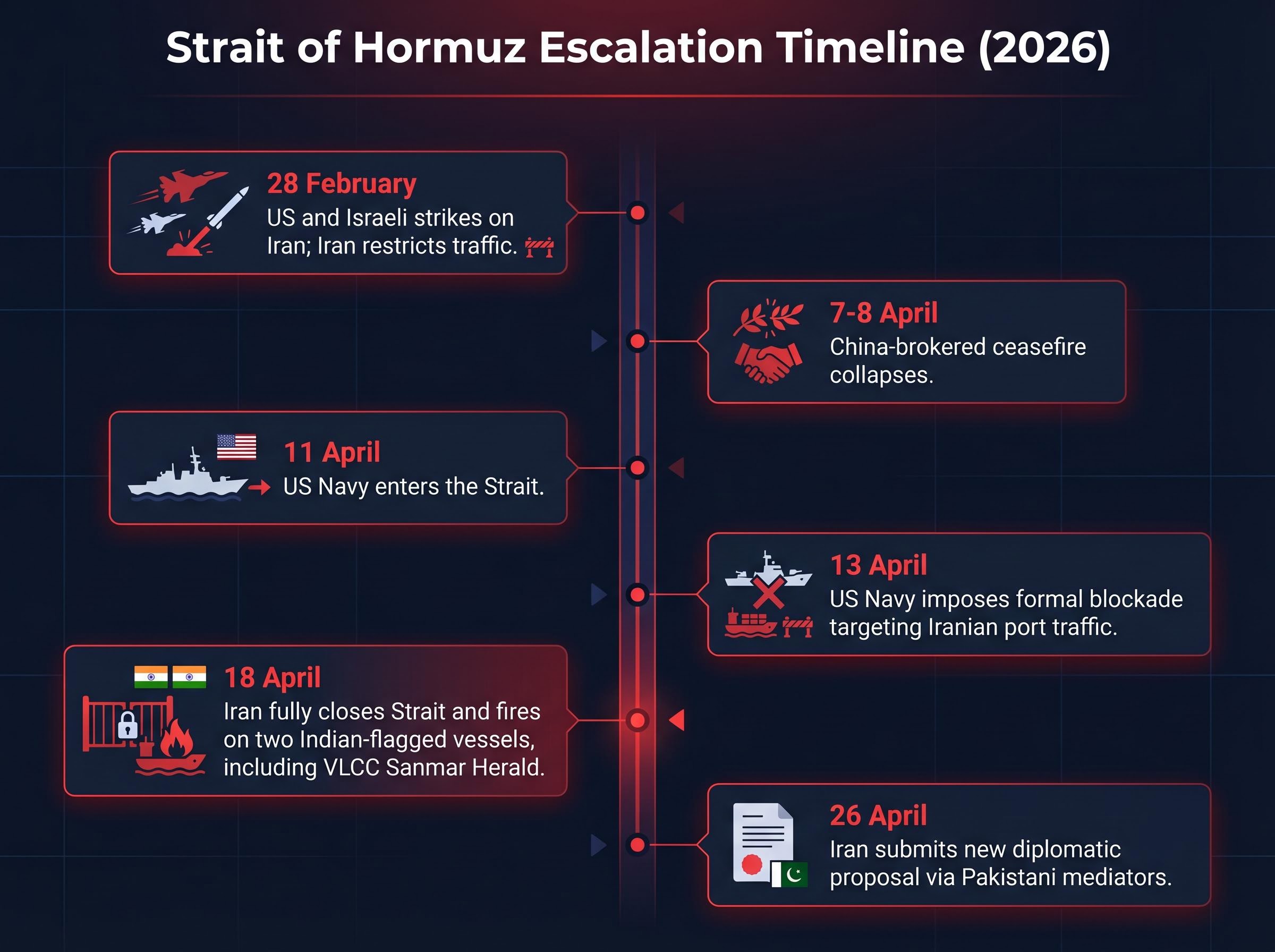

Brent crude crossed $101 per barrel this week as the Strait of Hormuz, the narrow waterway carrying roughly one quarter of the world’s seaborne oil, remains closed to near all traffic following a collapse in US-Iran diplomatic talks. The blockade, which began in late February 2026 after US and Israeli strikes on Iran, has escalated into a dual-blockade structure: Iran has shut the Strait to vessels linked to the US, Israel, and their allies, while the US Navy has imposed its own blockade targeting Iranian port traffic since 13 April. A brief ceasefire in early April collapsed, and Iran’s latest diplomatic overture, submitted via Pakistani mediators on 26 April, has yet to receive a formal US response.

What follows covers the diplomatic breakdown, how the dual blockade took shape, why the Strait carries so much weight in global energy markets, what the disruption means for commodity prices and equity positioning, and what a resolution path might require.

President Trump cancelled the dispatch of US negotiators to Pakistan on Sunday, stating that Iran should initiate contact given Washington’s negotiating strength. The decision came hours after Axios reported that Iran had submitted a new proposal via Pakistani mediators on 26 April 2026, citing a US official and two sources with direct knowledge of the offer.

Iran’s proposal centres on three elements: reopen the Strait of Hormuz, end hostilities, and defer nuclear discussions to a later stage.

No formal US response had been confirmed as of 27 April 2026. Trump has stated that any deal must be comprehensive and backed by all Iranian domestic factions, not a partial agreement on the Strait alone. A situation room meeting with his national security team has been scheduled to review options.

The gap between Iran’s offer and Washington’s preconditions is wide, but it is also familiar. Each prior negotiation attempt has ended the same way:

For investors, the pattern carries a practical signal. Each failed round has corresponded with an upward leg in crude prices, making the diplomatic timeline a market-moving indicator in its own right.

The current crisis is not a single event but two overlapping disruptions that have compounded into a near-total halt in Strait traffic.

US and Israeli strikes on 28 February 2026 triggered Iran’s initial restriction of Strait of Hormuz traffic. This first phase established the baseline disruption, cutting vessel movements and sending insurance premiums higher before any US naval response.

The US Navy entered the Strait on 11 April and formally imposed a naval blockade targeting Iranian port traffic from 13 April, according to CENTCOM. Iran responded by imposing tolls exceeding $1 million per vessel on those still attempting transit.

On 18 April, Iran reversed a short-lived partial reopening and fully closed the Strait. Iranian forces opened fire on two Indian-flagged vessels, including the VLCC Sanmar Herald, despite prior Iranian authorisation to transit. Both vessels turned back.

The 18 April partial reopening, which briefly allowed around 20 vessels through, proved short-lived; zero commercial tanker transits recorded on 19 April after the US Navy seized the Iranian cargo ship Touska, a sequence that foreshadowed the full closure formalised days later.

Iran has since prohibited all vessels travelling to or from the US, Israel, or their allies from transiting the Strait, enforcing the closure with drones, naval mines, and small boats, according to CSIS analysis.

The dual-blockade structure, as CSIS describes it, means Iran disrupts Gulf traffic broadly while the US specifically targets Iranian port-bound vessels. A single policy change by either side is unlikely to restore traffic; both blockades would need to be lifted.

| Date | Actor | Action | Market consequence |

|---|---|---|---|

| 28 February | US / Israel | Strikes on Iranian targets | Iran restricts Strait traffic; oil prices begin climbing |

| 7-8 April | China (mediator) | Brokered ceasefire; subsequently collapsed | Brief relief in crude prices reversed within days |

| 11-13 April | US Navy / CENTCOM | Entered Strait; formal blockade of Iranian port traffic | Dual-blockade structure established; shipping uncertainty intensified |

| 18 April | Iran | Full Strait closure; fired on two Indian-flagged vessels | Near-total halt in transits; Brent pushed above $101 |

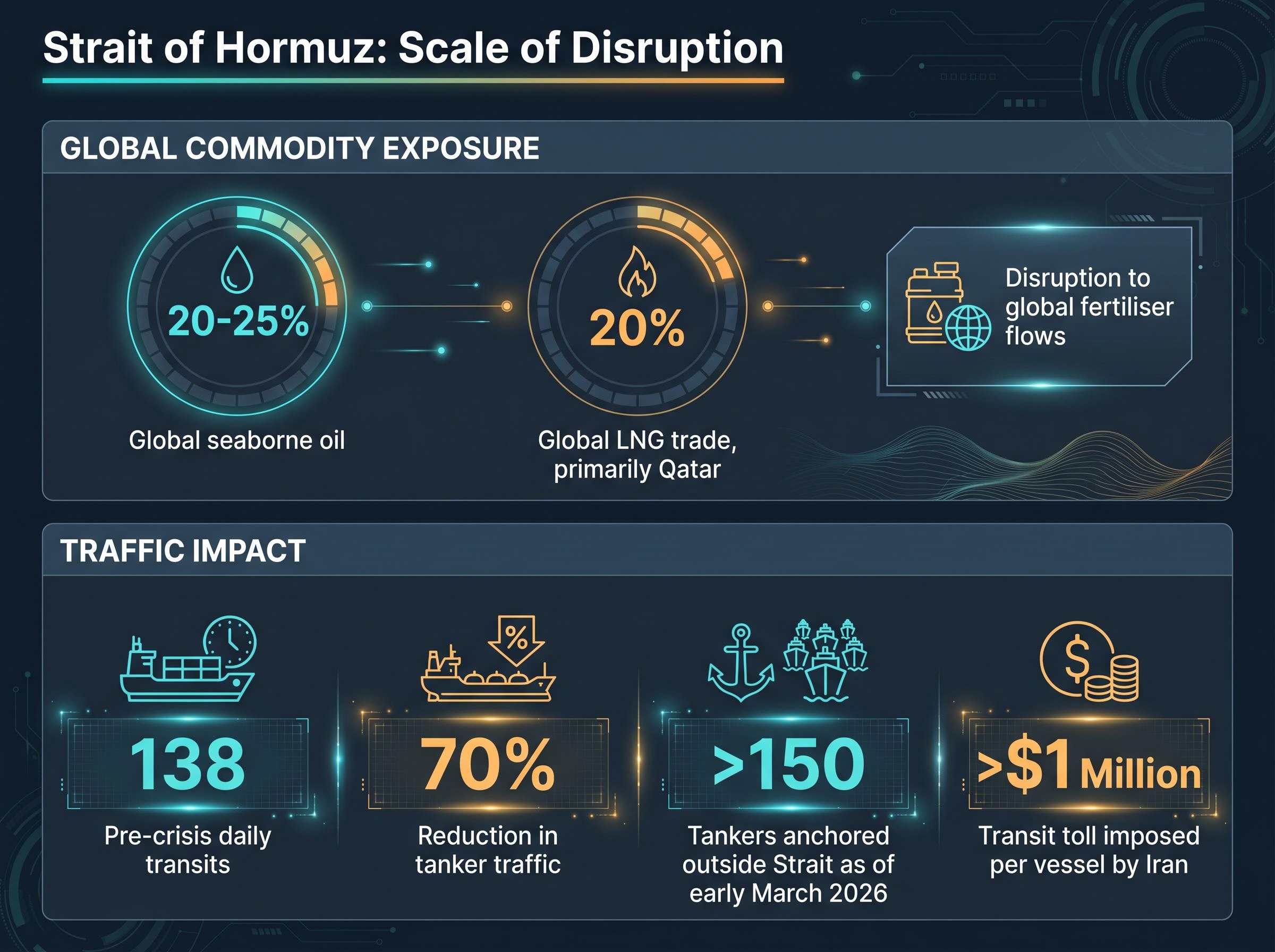

The Strait of Hormuz sits between Iran and Oman at the mouth of the Persian Gulf. At its narrowest point, the shipping lane compresses into a corridor just a few kilometres wide, making it a chokepoint rather than simply a busy sea route. Before the crisis, approximately 138 vessels per day transited the Strait.

Three commodity categories depend on that corridor:

UNCTAD characterises the Strait of Hormuz as carrying approximately a quarter of global seaborne oil, making its closure a supply removal problem rather than a rerouting problem.

The scale of disruption is visible in the numbers. Over 150 tankers, including crude oil carriers and LNG vessels, were anchored outside the Strait as of early March 2026, a congestion pattern consistent with conditions reported through late April. A 70% reduction in tanker traffic has been recorded. Alternative routes, including the Suez Canal and overland pipelines, carry a fraction of the volume the Strait handles, meaning a prolonged closure removes supply from global markets rather than redirecting it.

The EIA’s World Oil Transit Chokepoints analysis establishes the Strait of Hormuz as the single most critical maritime energy corridor globally, noting that no alternative route can absorb the volume it handles, which is why a sustained closure functions as an outright supply removal rather than a logistics detour.

Brent crude was trading at approximately $101.14 per barrel as of 22 April 2026, the last independently verified figure. WTI stood at $96.63 per barrel at the same reference point.

Brent crude above $101 per barrel represents the clearest market signal that traders are pricing in a prolonged disruption rather than a near-term resolution.

The $100 threshold carries weight beyond symbolism. For energy-importing economies, it recalibrates fuel subsidy budgets, industrial input cost assumptions, and inflation expectations simultaneously. The current price reflects a rational supply-risk premium given the near-halt in Strait transits and the absence of a credible diplomatic resolution timeline, rather than speculative momentum alone.

The transmission from crude prices into consumer inflation has been faster than many models anticipated: US gasoline prices surged 37% to $4.11 per gallon within seven weeks, pushing the Consumer Price Index up 90 basis points in a single month and effectively eliminating Federal Reserve rate cut expectations for 2026.

Real-time crude price data from Bloomberg, Reuters, or the Energy Information Administration (EIA) remains the most reliable source for tracking intraday movements beyond the 22 April confirmed figure.

European equity markets opened on 27 April with a muted, cautious tone consistent with investor uncertainty rather than directional conviction:

CSIS notes that Iran’s tactics impose ongoing uncertainty on energy markets despite US countermeasures, a dynamic visible in the flat-to-cautious equity positioning.

Two European equity outliers reflected company-specific developments rather than the broader geopolitical picture: Nordex shares gained more than 9% on a Q1 earnings beat, while Forvia rose over 3% following the sale of its interiors unit to Apollo for 1.82 billion euros.

Iran’s 26 April proposal offers a staged approach: reopen the Strait and end hostilities first, defer the nuclear file to a later round. The US position requires the opposite, a comprehensive deal covering all outstanding issues, backed by all Iranian domestic factions, before any concession on the blockade.

That structural gap is the primary obstacle. Pakistan remains the most active mediator, having facilitated the delivery of Iran’s latest offer. China applied pressure that produced the short-lived 7-8 April ceasefire, and may retain leverage for a future attempt. Neither channel has delivered a durable outcome.

Three specific developments would signal meaningful movement toward resolution:

No new multilateral sanctions or coordinated maritime security measures have been reported in the post-18 April period. The dual-blockade structure, as CSIS frames it, means both sides must act for traffic to resume, and Iran’s enforcement capability persists regardless of diplomatic developments.

Near-term resolution appears unlikely without a significant shift in one side’s position. Investors tracking energy, shipping, or commodity-exposed positions should monitor the diplomatic indicators above rather than headline noise alone.

The Strait of Hormuz blockade is not a single crisis but an accumulation of failed de-escalation attempts, each leaving the situation more entrenched. With Brent crude above $100, tanker traffic near a standstill, and both sides maintaining incompatible preconditions, the supply shock to global energy and LNG markets shows no near-term sign of easing.

Iran’s proposal via Pakistan gives diplomacy one more opening, but the gap between a partial Strait deal and a comprehensive, faction-unified agreement is wide. Markets will be watching for a formal US response as the most immediate signal of whether that gap narrows or holds.

Investors seeking a structured framework for portfolio positioning in this environment will find our deep-dive into sector rotation strategy during the Iran oil shock, which examines the roughly 10 percentage point performance gap between energy and non-energy stocks since February, historical recovery patterns from comparable supply shocks, and the specific conditions that have preceded durable market recoveries.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding diplomatic outcomes and commodity prices are speculative and subject to change based on geopolitical developments and market conditions.

The Strait of Hormuz blockade refers to the near-total halt in commercial shipping through the narrow waterway connecting the Persian Gulf to global ocean routes. It matters because roughly one quarter of the world's seaborne oil and approximately 20% of global LNG trade passes through it, meaning a sustained closure removes supply from global markets rather than simply rerouting it.

The dual blockade formed in two phases: Iran restricted Strait traffic following US and Israeli strikes on 28 February 2026, then the US Navy imposed its own blockade targeting Iranian port traffic from 13 April 2026, creating two overlapping disruptions that together produced a near-total halt in commercial tanker transits.

Brent crude was trading at approximately $101.14 per barrel as of 22 April 2026, with WTI at $96.63 per barrel at the same reference point, reflecting a sustained supply-risk premium priced in by traders expecting a prolonged disruption rather than a near-term diplomatic resolution.

Resolution would require both sides to act, as the dual-blockade structure means Iran's closure and the US naval blockade must each be lifted for traffic to resume. Key signals to watch include a formal US response to Iran's 26 April proposal, evidence of intra-Iranian factional alignment on a unified negotiating position, and any confirmed multilateral diplomatic initiative.

The closure pushed Brent crude above $101 per barrel and contributed to a 37% surge in US gasoline prices to $4.11 per gallon within seven weeks, lifting the Consumer Price Index by 90 basis points in a single month and effectively eliminating Federal Reserve rate cut expectations for 2026.