BlackRock Raises AI and Tech Decoupling to Top Risk Tier

16 hrs ago

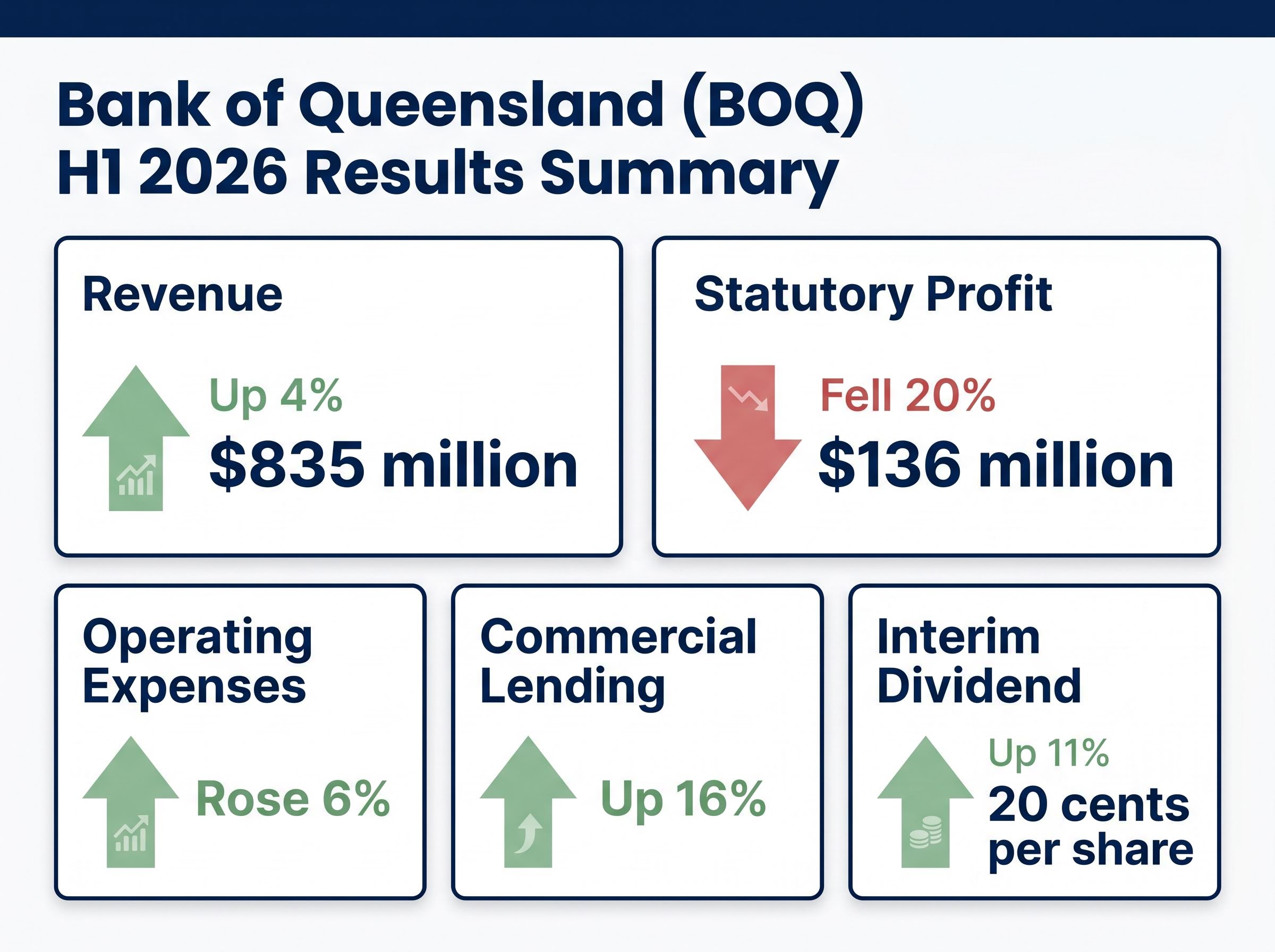

Bank of Queensland saw its share price drop 7.3% on 22 April 2026, the morning its half-year results landed. Revenue was up 4%. That divergence is the story.

The lender is in the middle of a deliberate, multi-year strategic reset. Statutory profit fell 20% to $136 million in the first half of the 2026 financial year, operating expenses rose 6%, and housing loan volumes shrank by design. At the same time, management announced a $300 million capital return, a fully franked dividend increase of 11%, and 16% commercial lending growth.

For retail investors evaluating Bank of Queensland stock, the challenge is not a lack of information but competing signals pointing in opposite directions. This analysis unpacks each pillar of the transformation, examines the financial reality behind the strategic narrative, and helps investors think clearly about what the evidence actually supports heading into the 2027 financial year.

Investors reading only the headline profit decline risk misdiagnosing the bank’s actual operational condition. The divergence between 4% revenue growth, reaching $835 million, and the 20% statutory profit decline to $136 million looks alarming at first glance. It drove the immediate market reaction, sending shares down 7.3% to $6.74 on 22 April 2026.

However, the profit contraction was not caused by a failure to generate income. The underlying driver is a 6% increase in operating expenses during the half. This expense growth is the deliberate consequence of three simultaneous cost pressures:

General inflationary pressures affecting the entire domestic banking sector Heavy capital investment in a multi-year digital systems programme * Targeted expenditure to build out the business banking franchise

Distinguishing the statutory profit headline from these underlying structural costs is the first step in forming a defensible view of the business. Not all metrics moved negatively during the period.

Margin Improvement The bank’s net interest margin improved by 10 basis points to 1.67%, indicating that core lending profitability actually expanded despite the broader earnings contraction.

The 16% commercial lending growth figure is a genuine positive that reflects a significant strategic pivot. The bank is deliberately de-emphasising its housing loan book, which declined over the same period, to allocate capital toward higher-margin business relationships. This is an intentional reshaping of the balance sheet rather than a loss of market share.

The mechanics behind BOQ’s margin improvement are not unique to this lender; BNK Banking’s NIM expansion strategy, which drove a 49 basis point improvement to 1.88% by deliberately tripling its higher-return asset allocation from 15% to 43% of portfolio, illustrates how smaller regional banks can structurally shift their earnings profile through disciplined mix management rather than volume growth.

Commercial loans are strategically preferable to mortgage lending for a regional bank of this size. The margin logic relies on capturing higher yields from business customers while shedding the low-margin residential mortgages that major banks dominate. This pivot also supported a 13% increase in non-interest income, buoyed by business lending fees and branch conversion proceeds.

| Metric | Direction | Strategic Significance |

|---|---|---|

| Commercial Lending | Up 16% | Validates the pivot toward higher-margin business lending. |

| Housing Loans | Declined | Reflects intentional retreat from low-margin mortgage competition. |

| Non-Interest Income | Up 13% | Supported by business fees and structural branch conversions. |

| Asset Quality (Arrears) | Improved | Indicates lending growth has not compromised credit standards. |

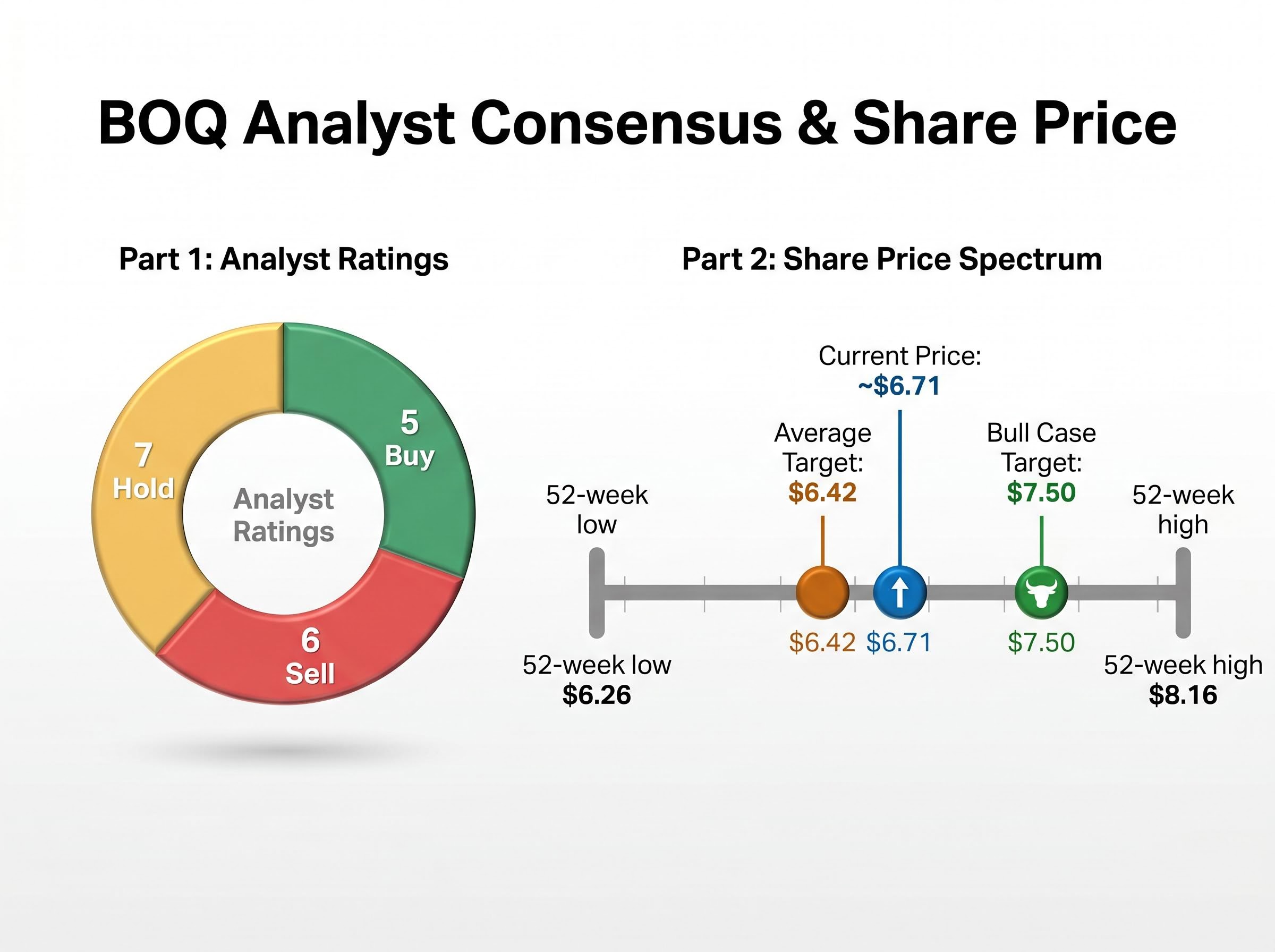

The market remains divided on whether this aggressive commercial growth rate is sustainable. Following the half-year results, the analyst consensus sat at five Buy ratings, seven Hold ratings, and six Sell ratings.

Analysts are explicitly questioning what this growth costs to acquire in a fiercely competitive lending market. Capital redeployment discipline, not just headline commercial loan volume, is the investor-relevant variable. Fund managers are watching for execution milestones that prove the bank can sustain this growth without eroding lending standards or offering uncommercial discounts.

Most retail investors assess bank strategy through earnings headlines, but institutional investors evaluate these choices through the lens of capital allocation and return on equity. With a market capitalisation of approximately $5 billion, the bank operates at a severe scale disadvantage compared to the four major Australian lenders.

This scale disadvantage makes a portfolio pivot a mathematical necessity rather than just a management preference. The logic behind the transition relies on understanding how regulatory capital actually works in the banking sector:

APRA Prudential Standard APS 112 establishes the specific risk weights applied to residential mortgage and commercial property exposures, which is the regulatory mechanism that makes housing loans structurally less capital-efficient for regional lenders competing against major banks with lower funding costs and greater scale.

This foundational logic connects the commercial lending growth directly to the divestiture of the $3.7 billion equipment finance portfolio. Releasing approximately $300 million in capital from that low-returning book provides the specific funding required to write new commercial loans. A rising Reserve Bank of Australia cash rate, which reached 4.10% in March 2026, further amplifies the need to optimise every dollar of capital deployed.

The most concrete near-term benefit from this transformation is the capital return strategy. Announced on 7 April 2026, the sale of the $3.7 billion equipment finance book to Challenger is designed to release approximately $300 million in capital. This transaction is expected to reach completion between late April and early May 2026.

Management characterised the sale as having a minimal profit impact. Because the equipment finance portfolio was a low-profitability asset, the earnings drag from its disposal is highly constrained relative to the substantial capital flexibility it creates. This flexibility allowed the board to signal shareholder confidence immediately.

The bank announced an interim fully franked dividend of 20 cents per share, an 11% increase from the prior period. These two simultaneous signals represent a deliberate strategy to reward patient shareholders while the broader transformation takes hold.

Income Support At the current share price, the increased interim dividend supports an annualised yield of approximately 6%, establishing a clear income floor for investors waiting for the operational turnaround.

However, the transaction carries specific dimensions that require careful monitoring:

The exact timing and final value of the capital release remain subject to final settlement conditions. The earnings impact, while minimal, still removes a defined revenue stream before new commercial loans are fully originated to replace it. * Execution and credit transition risk during the handover to the buyer could create minor short-term friction.

The executive team has implicitly staked its credibility on the 2027 financial year. Retail investors need to understand exactly which conditions must hold simultaneously for this recovery thesis to be validated. Over the past 12 months, the stock has underperformed, dropping approximately 6% while the S&P/ASX 200 benchmark rose approximately 15%.

The recovery thesis relies on three specific levers: the maturation of the digital mortgage platform, disciplined commercial lending growth, and operating cost growth falling below the rate of inflation. Furthermore, the macroeconomic tailwind of the Reserve Bank of Australia cash rate holding at 4.10% offers a potentially supportive environment for net interest margin expansion.

The RBA rate cycle trajectory carries asymmetric implications for BOQ’s NIM outlook; if the supply-shock-driven inflation impulse proves temporary and the cash rate peaks earlier than current pricing implies, the margin expansion tailwind that underpins the FY27 recovery thesis would compress faster than management’s forward projections account for.

| Metric | Current State | FY27 Condition Required | Risk to Thesis |

|---|---|---|---|

| Net Interest Margin | 1.67% | Sustained expansion | Intense deposit competition eroding gains. |

| Operating Costs | Growing at 6% | Growth falls below inflation | Digital transformation delays require more capital. |

| Commercial Lending | Growing at 16% | Sustained disciplined growth | Margin compression from aggressive pricing. |

| Home Lending | Declining balances | Platform-driven recovery | Franchise conversion fails to attract volume. |

There is clear tension between management’s optimism and the institutional view. The average analyst price target sits at $6.42, which implies modest downside from the current share price of approximately $6.71.

This consensus suggests that institutional investors are pricing in elevated execution risk rather than assuming the 2027 targets are a certainty. The high price target of $7.50 represents the bull case, mapping out where the valuation could land if all execution conditions are met simultaneously and without delay.

Evaluating a mid-tier lender halfway through a structural overhaul requires separating strategic intent from demonstrated results. The strategic logic behind the transition is coherent, but the financial results have not yet validated it. The timeline to that validation remains anchored to the 2027 financial year at the earliest.

Analysis from Morningstar on 22 April 2026 emphasised that strict cost control and flawless digital execution are critical prerequisites for profit recovery. Similarly, Investor Daily reporting highlighted intensifying competition as a persistent structural risk to the margin profile. With the stock trading at approximately $6.71, sitting in the lower half of its $6.26 to $8.16 52-week range, the evidence supports three distinct investor positions:

The Income Case: Anchored by the 6% fully franked yield, this position assumes the dividend is safe and compensates for a patient holding period while the business restructures. The Speculative Recovery Case: Focused on the upside potential if operating expense growth genuinely falls below inflation and the new digital platform successfully scales home lending by 2027. * The Cautious Case: Guided by the analyst consensus implying downside risk, this view waits for concrete proof of commercial margin sustainability before committing capital.

The income case built around BOQ’s franked dividend yield does not sit in isolation; across the broader Australian banking sector, Morgans has issued sell ratings on all four major lenders despite grossed-up yields reaching as high as 6.06%, raising the question of whether fully franked income is sufficient compensation for capital risk when the analyst consensus implies double-digit downside across the sector.

The execution risks identified by analysts are tangible and immediate. The operating expense trajectory must break its current upward trend for the productivity thesis to hold water.

The strategic direction of the enterprise reflects a highly rational response to the structural disadvantages facing regional banks competing against scale-heavy majors. The commercial lending pivot, portfolio simplification, and heavy digital investments are the correct levers to pull. However, the gap between strategic intent and demonstrated financial reality cannot be ignored.

The $300 million capital return remains the most tangible near-term value delivery, supporting the 11% dividend increase. That approximately 6% yield provides an income floor, while the $6.26 to $8.16 historical range indicates meaningful upside optionality if the transformation milestones are met. The 2027 financial year will be the first genuine test of whether this thesis can be validated by actual earnings growth.

For investors wanting to situate BOQ’s valuation discount within the broader sector context, our deep-dive into ASX bank sector valuation in 2026 examines how the Big Four’s price momentum has diverged sharply from analyst consensus, with unanimous sell ratings on CBA and implied downside of up to 25.5% raising important questions about whether the sector-wide re-rating that would lift regional bank sentiment is actually achievable in the current environment.

The ultimate framing question for any portfolio allocation is straightforward. Investors must decide if the dividend yield and the optionality on a successful transformation offer sufficient compensation for the execution risk and the institutional consensus implying near-term downside.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

BOQ shares dropped 7.3% to $6.74 on 22 April 2026 because statutory profit fell 20% to $136 million, driven by a 6% rise in operating expenses from digital investment and business banking build-out, despite revenue growing 4% to $835 million.

BOQ announced a $300 million capital return funded by the sale of its $3.7 billion equipment finance portfolio to Challenger, with completion expected between late April and early May 2026, releasing capital that had been tied up in a low-profitability asset.

At the share price following the April 2026 results, BOQ's increased interim fully franked dividend of 20 cents per share supports an annualised yield of approximately 6%, providing an income floor for investors waiting for the operational turnaround to materialise.

As of the April 2026 half-year results, the analyst consensus sat at five Buy ratings, seven Hold ratings, and six Sell ratings, with the average price target of $6.42 implying modest downside from the then-current share price of approximately $6.71.

The recovery thesis requires the digital mortgage platform to mature and attract home lending volume, commercial lending growth to continue without margin compression, and operating cost growth to fall below the rate of inflation, all while the RBA cash rate remains supportive of net interest margin expansion.