Marvell Technology Surges 22% on Nvidia CEO’s Trillion-Dollar Call

7 hrs ago

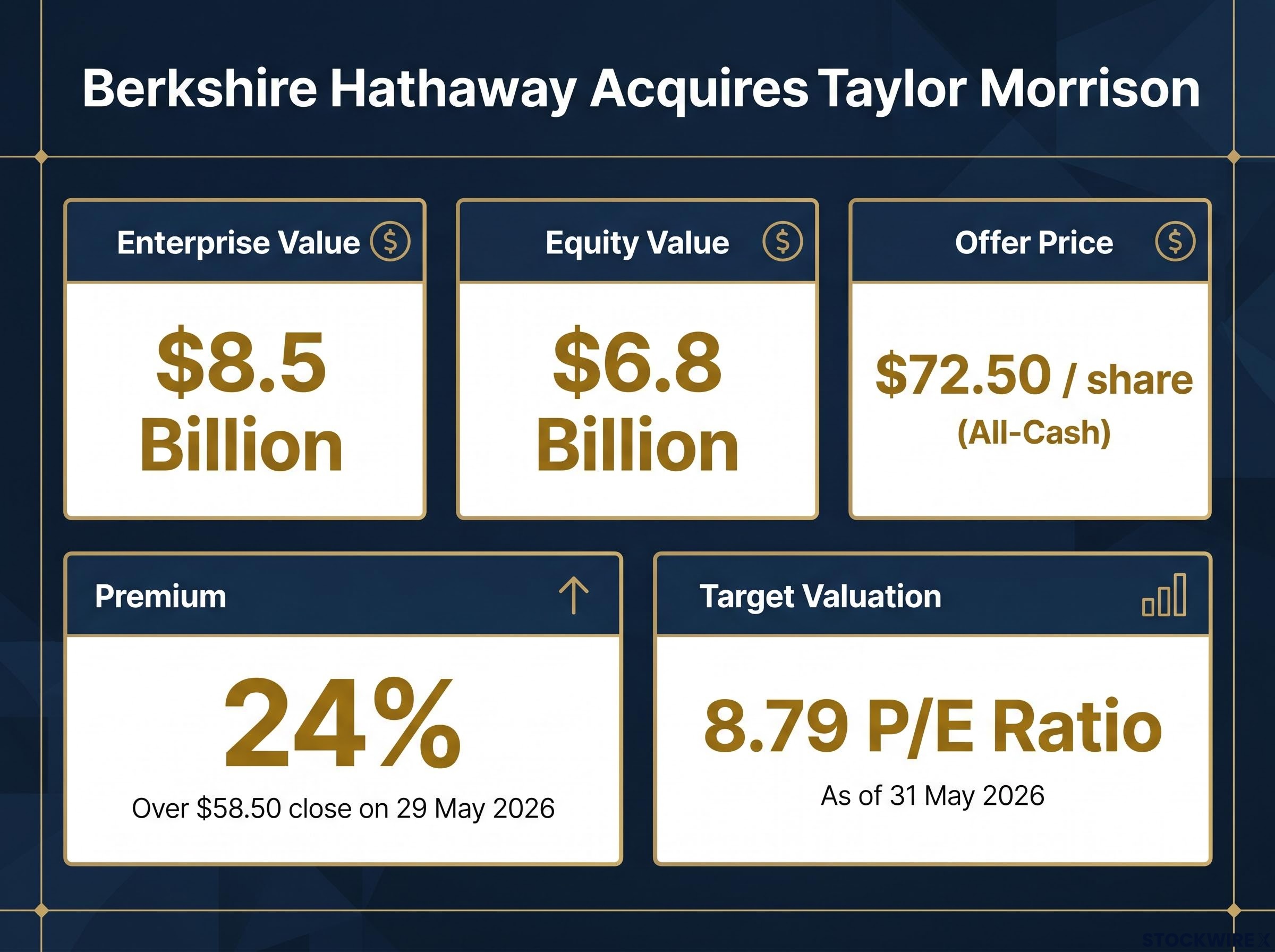

Berkshire Hathaway has agreed to acquire Taylor Morrison Home for $72.50 per share in cash, a 24% premium to the homebuilder’s closing price of $58.50 on 29 May 2026. The deal, valued at approximately $8.5 billion in enterprise terms, is the largest acquisition Greg Abel has made since succeeding Warren Buffett as chief executive earlier this year. It lands at a moment when tight resale inventory across U.S. metropolitan areas continues to funnel demand toward new construction, and homebuilder stocks trade at single-digit earnings multiples. What follows covers the deal terms, the asset Berkshire is acquiring, the housing market conditions that frame the timing, and what the broader homebuilder sector should take from the signal.

Every first major acquisition a new chief executive makes carries more weight than the dollars involved. For Abel, who stepped into the most scrutinised capital allocation seat in global markets, this deal is a statement of intent written in an $8.5 billion cheque.

The Berkshire succession dynamics that positioned Abel for this moment are well documented: he formally assumed the CEO role at the start of 2026, led his first annual meeting on 2 May, and entered the chair with a record cash reserve of nearly $400 billion that the market was watching him deploy.

No direct quotation from Abel tied to the transaction has surfaced as of 1 June 2026. The deal structure speaks for itself: all-cash, no financing condition, a defined premium, and a target that fits the Berkshire template of durable, cash-generating businesses acquired at reasonable multiples.

24% premium: Berkshire’s offer of $72.50 per share represents a 24% premium to Taylor Morrison’s 29 May 2026 closing price, the clearest measure of how much Berkshire was willing to pay above market consensus for this asset.

The core deal metrics at a glance:

Taylor Morrison operates across 11 states, with a brand portfolio spanning entry-level homes through to luxury segments. That geographic and demographic breadth is not incidental; the joint press release with Berkshire specifically called out the company’s diversified footprint as a strategic attribute.

A builder with national reach and multi-segment exposure is structurally different from one concentrated in a single price band or region. When mortgage rates compress demand at the entry level, luxury absorbs the slack. When one state’s permitting pipeline slows, ten others keep the order backlog moving.

Berkshire is paying a premium, but the underlying asset was priced modestly relative to earnings before the announcement:

An 8.79x earnings multiple for a national-scale homebuilder with diversified operations suggests Berkshire identified a gap between market pricing and intrinsic value, a pattern consistent with the conglomerate’s long-standing acquisition philosophy.

The official deal rationale centres on Taylor Morrison’s scale and diversification, not on rate-cycle timing or macroeconomic forecasting. The housing market backdrop, however, makes the strategic logic more legible.

Persistent supply shortfalls across U.S. metropolitan areas have redirected buyer demand toward new construction for several years running. Elevated mortgage rates have created affordability pressure, yet they have not resolved the underlying inventory deficit. Builders with strong order backlogs and margin discipline have continued to benefit from this structural imbalance, and Taylor Morrison fits that description.

New construction demand dynamics in 2026 are shaped by a specific structural condition: resale inventory has remained so constrained that buyers who would ordinarily purchase existing homes have been redirected toward builders, sustaining order volumes even as mortgage affordability pressure has reduced the pool of rate-sensitive buyers.

The broader economic environment at the time of announcement adds context. The Institute for Supply Management’s manufacturing PMI rose to 54 in May 2026, a four-year high, suggesting a resilient macro backdrop. The May nonfarm payrolls release, expected on 6 June 2026, was identified as the next closely watched data point for market participants.

| Structural tailwind | Mitigating risk factor |

|---|---|

| Persistent resale inventory shortfall redirecting demand to new builds | Elevated mortgage rates compressing affordability for entry-level buyers |

| Strong builder order backlogs and margins sustained through 2025-2026 | Rate-sensitive demand segments remain vulnerable to further tightening |

| ISM manufacturing PMI at 54 (four-year high) signals resilient macro conditions | Mixed economic data and upcoming payrolls release introduce near-term uncertainty |

The supply deficit is not a forecast; it is the observable condition that has sustained builder revenues through a period of elevated borrowing costs. That condition is what makes Taylor Morrison’s margin profile durable enough to justify an $8.5 billion commitment.

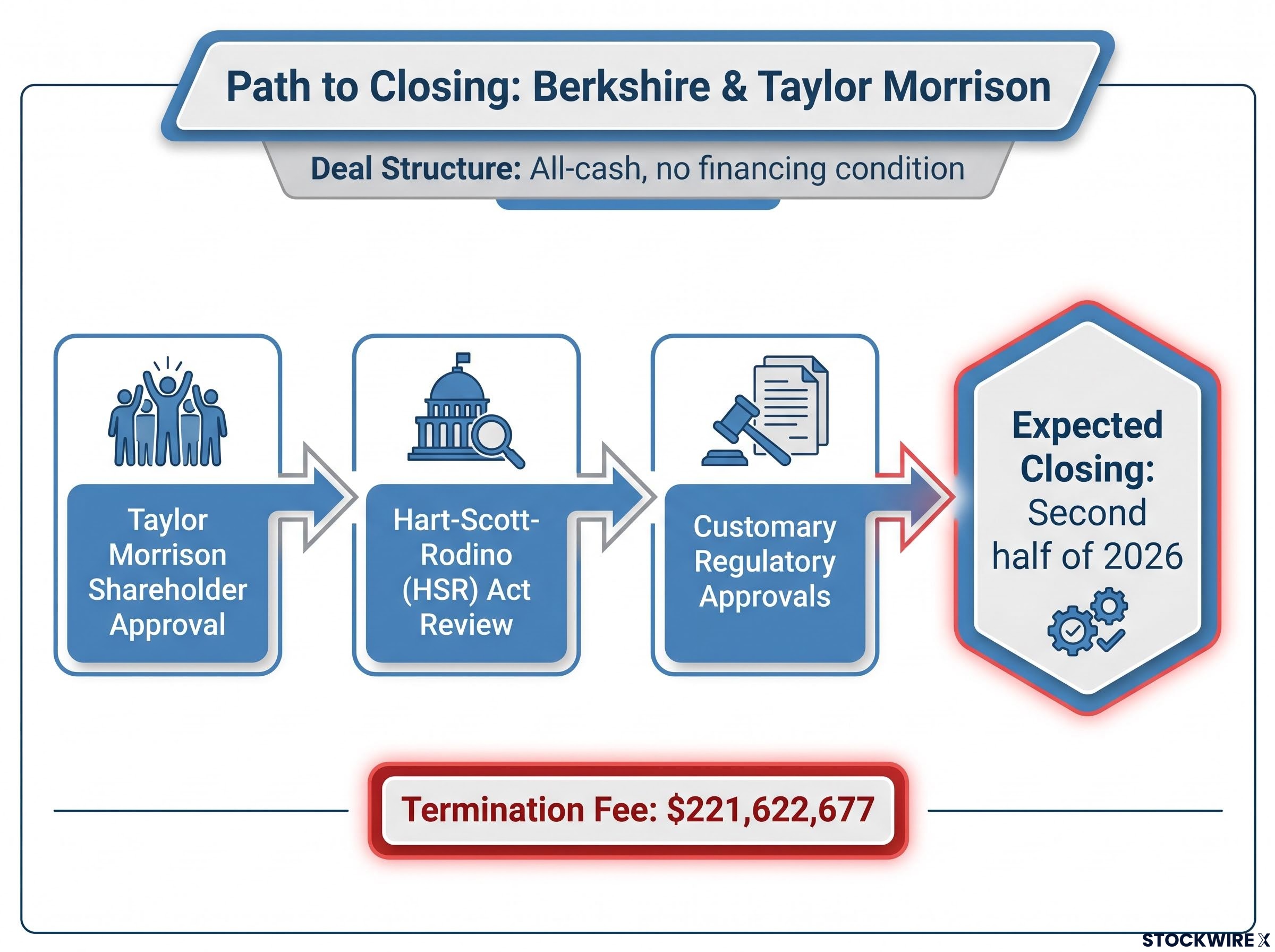

The merger agreement is structured as an all-cash acquisition with no financing condition attached. Berkshire has not disclosed whether it will deploy existing cash reserves or issue debt to fund the transaction.

Closing is subject to a defined sequence of conditions:

The Hart-Scott-Rodino premerger notification program requires parties to large transactions to file with the FTC and the Department of Justice and observe a statutory waiting period before closing, giving regulators the opportunity to assess competitive effects before the deal is consummated.

Termination fee: $221,622,677. Taylor Morrison has agreed to pay this amount to Berkshire in defined circumstances, including a change of board recommendation or acceptance of a superior proposal.

The agreement includes a no-shop covenant restricting Taylor Morrison from soliciting alternative acquisition proposals, though a fiduciary-out provision permits the board to consider a genuinely superior offer. Taylor Morrison must operate in the ordinary course of business prior to closing.

Upon completion, Taylor Morrison will become a wholly owned subsidiary of Berkshire Hathaway. Its common stock will be delisted from the NYSE and will cease to be publicly traded. Closing remains expected in the second half of 2026.

Taylor Morrison shares surged 22.3% on 1 June 2026, closing near the offer price as the market priced in the acquisition premium. Berkshire Hathaway Class B shares fell approximately 1.1% on the same day, a standard market read on capital deployment by an acquirer at a defined premium.

Specific post-announcement price moves for peer homebuilders, including D.R. Horton, Lennar, PulteGroup, and NVR, have not yet been captured in attributed reporting as of 1 June 2026.

The absence of sourced peer data does not diminish the directional signal. When the world’s most scrutinised capital allocator commits $8.5 billion to a homebuilder trading at 8.79x earnings, it validates a sector-level thesis: that homebuilder equities may be underpriced relative to the durability of their earnings streams under current supply conditions.

If Taylor Morrison’s pre-deal multiple is representative of peer valuations, the gap between market pricing and the price Berkshire was willing to pay suggests room for re-rating across the sector. That is not a guarantee; it is a data point institutional and retail investors will recalibrate against.

This deal operates on two levels simultaneously. For Berkshire, it is the first concrete evidence of how Abel deploys capital at scale: all-cash, no financing contingency, a defined premium for a business with national reach and multi-segment durability. The structure is disciplined. The target is knowable. The thesis is grounded in observable supply conditions rather than rate-cycle speculation.

For the homebuilder sector, it is a validation that arrived in the form of a price tag. As long as resale inventory remains constrained, builders with diversified geography and brand portfolios are positioned to sustain margins in ways that pure entry-level operators may not. Berkshire’s willingness to pay $8.5 billion for that positioning sends a signal that single-digit earnings multiples across the sector may not reflect the asset quality underneath.

Abel’s investment criteria are becoming legible across the two largest capital moves of his tenure: the $2.65 billion Delta Air Lines stake disclosed in the May 13F filing and this $8.5 billion homebuilder acquisition both share the same valuation profile, low single-digit or low-teens earnings multiples, strong free cash flow generation, and businesses operating in structurally constrained competitive environments.

What to watch from here: the shareholder vote outcome, the HSR clearance timeline, and whether Abel provides further commentary that sharpens the picture of his investment philosophy as Berkshire’s post-Buffett chapter takes shape.

Investors wanting to convert this acquisition signal into a broader portfolio positioning framework will find our comprehensive walkthrough of Berkshire’s deployment signal framework, which covers how to monitor 13F filings on SEC EDGAR, how to interpret net-buying reversals after extended selling streaks, and how to build a pre-researched watchlist with intrinsic value estimates that can act on Berkshire moves as they occur rather than after the fact.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Berkshire Hathaway agreed to acquire Taylor Morrison Home for $72.50 per share in an all-cash deal valued at approximately $8.5 billion in enterprise terms, representing a 24% premium to Taylor Morrison's closing price on 29 May 2026.

Berkshire identified Taylor Morrison as undervalued relative to its earnings and cash flow, with a pre-deal price-to-earnings ratio of 8.79x, while the homebuilder's national scale and multi-segment brand portfolio offered durable margins supported by persistent resale inventory shortfalls across U.S. metropolitan areas.

Once the deal closes, expected in the second half of 2026, Taylor Morrison will become a wholly owned subsidiary of Berkshire Hathaway and its common stock will be delisted from the NYSE, ceasing to be publicly traded.

The acquisition signals that homebuilder equities may be underpriced relative to the durability of their earnings streams; with Taylor Morrison acquired at 8.79x earnings and a 24% premium, investors and institutions are likely to scrutinise whether peer builders such as D.R. Horton, Lennar, and PulteGroup carry similar underpricing.

The deal requires Taylor Morrison shareholder approval, expiration or termination of the Hart-Scott-Rodino Act antitrust waiting period, and other customary regulatory approvals before Berkshire can complete the acquisition.