CargoWise runs inside 24 of the world’s 25 largest freight forwarders, yet the company that built it has lost nearly half its market value in 2026. WiseTech Global (ASX: WTC) has shed approximately 45.89% year-to-date as of 24 May 2026, a collapse driven by governance scandal, earnings guidance disappointment, and a violent derating of high-multiple ASX technology stocks. Yet the most recently reported annual revenue reached $1,042 million with a 27.1% three-year compound annual growth rate (CAGR), gross margins of 84%, and FY26 guidance pointing to revenue of US$1.39-1.44 billion.

The gap between operational dominance and the WiseTech Global share price is the question facing Australian investors right now. What follows works through the data needed to distinguish a genuine buying opportunity from a structural re-rating: what drove the crash, why business fundamentals remain intact, how to read the current valuation, and where the real risks sit.

How a logistics software monopoly lost half its value in months

The share price decline did not arrive in a single event. It compounded across three converging pressures: a governance shock that eroded institutional confidence, earnings guidance that repeatedly fell below market expectations, and a broader sell-off in high-multiple ASX technology names that left WiseTech, previously one of the most expensive stocks on the exchange, acutely exposed.

The governance sequence unfolded over more than a year:

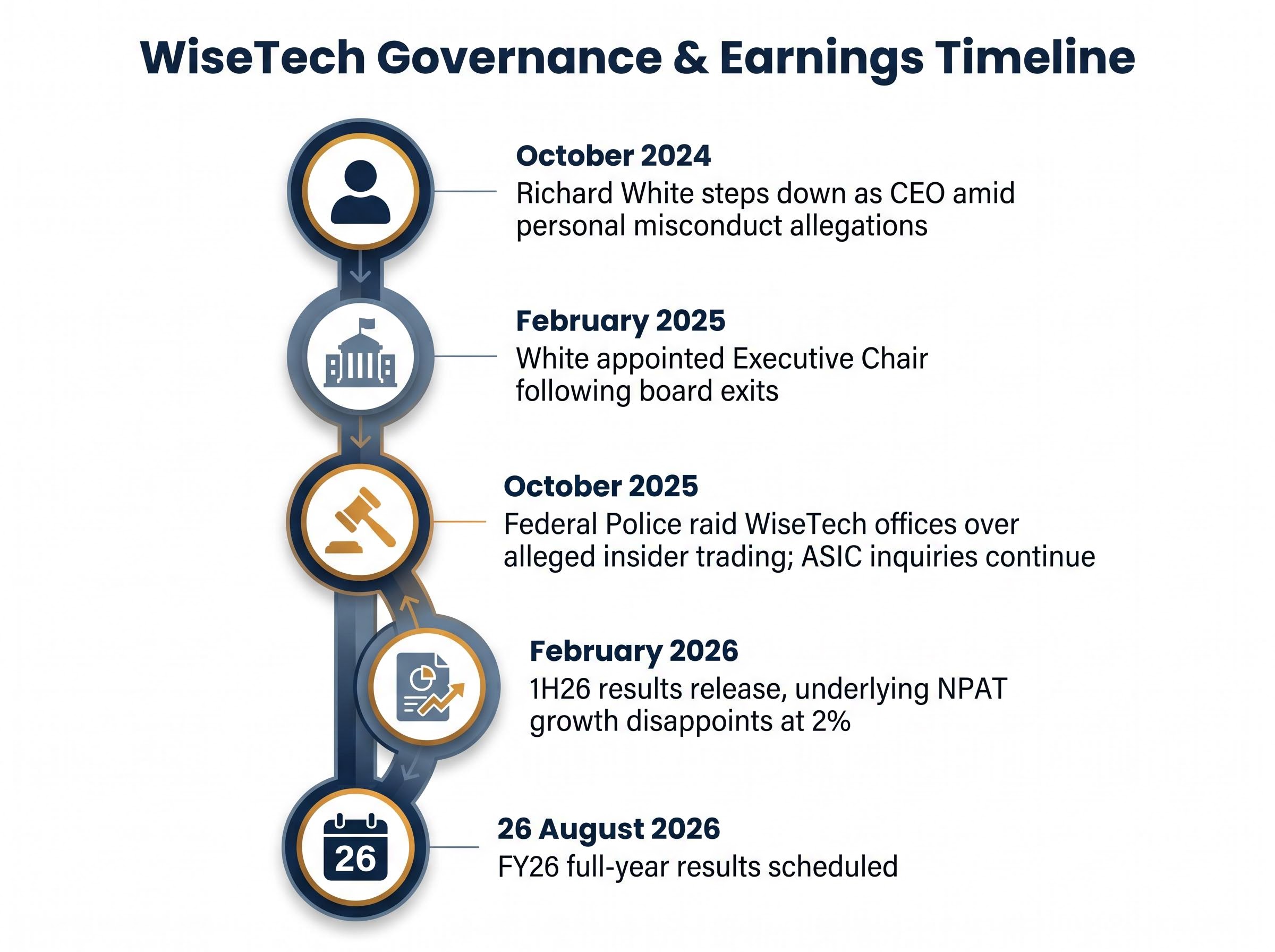

- October 2024: Richard White stepped down as CEO amid personal misconduct allegations

- February 2025: White was appointed Executive Chair following board exits

- October 2025: Federal Police raided WiseTech’s offices over alleged insider trading involving White and employees; ASIC inquiries continued

- February 2026: 1H26 results released; FY26 guidance reaffirmed but underlying NPAT growth of just 2% disappointed

- 26 August 2026: FY26 full-year results scheduled, the next major information event

The ASIC and AFP raid on WiseTech in October 2025 centred on allegations of insider trading involving White and employees, adding a formal law enforcement dimension to what had previously been governance and conduct concerns at the board level.

Each event layered fresh uncertainty onto an already fragile valuation. FY25 total revenue rose 14% to US$778.7 million and underlying NPAT grew 30% to US$241.8 million, strong numbers by most standards. But by 1H26, underlying NPAT growth had decelerated to $114.5 million (up just 2%), well below the trajectory the market had priced in.

The 1H26 result also introduced a structural cost story alongside the revenue numbers: WiseTech announced an AI transformation programme targeting up to 2,000 role reductions across key teams, with management flagging material margin benefits expected from FY27 as the workforce reset completes and e2open synergies begin flowing through.

“Market expectations are still too high, creating downside earnings risk.” Macquarie Bank, August 2023

Macquarie’s warning, issued when it cut its WiseTech target from A$90 to A$59, proved prescient. Multiple reporting events since have confirmed the pattern: solid growth that nonetheless fell short of what an extreme multiple demanded.

Multiple compression in ASX growth stocks follows a pattern that predates any single governance event: a stock trading at an extreme earnings multiple becomes disproportionately sensitive to any growth miss, because the entire valuation rests on flawless future execution rather than current-year earnings power.

When big ASX news breaks, our subscribers know first

What WiseTech actually is and why its market position is genuinely unusual

WiseTech’s core product, CargoWise, is a cloud-based platform that covers customs and freight forwarding, landside transport, warehousing, rates and contracts management, and transport management systems across international and domestic logistics. Founded in 1994 by Richard White and Maree Isaacs and listed on the ASX, the company has grown into the dominant operating system for global freight.

The market penetration figures tell that story more precisely than any description of scale.

24 of the 25 largest freight forwarders worldwide run on CargoWise. 46 of the top 50 third-party logistics providers use the platform.

Those numbers sit alongside an 84.0% gross margin, the kind of figure that reflects software economics where incremental revenue carries minimal variable cost, and a 27.1% three-year revenue CAGR. A 46% share price fall looks very different when applied to a near-monopoly platform with structurally high switching costs than it does to a commodity business competing on price.

Why logistics software has unusually high switching costs

Freight forwarders integrate CargoWise into compliance workflows, customs filings, and multi-carrier shipment tracking across dozens of countries simultaneously. The platform is not a standalone tool; it is embedded in regulatory processes that operate under strict legal deadlines.

Migration requires retraining staff, rebuilding data integrations with shipping lines and customs authorities, and accepting operational risk during transition. For a large forwarder running thousands of shipments daily across multiple jurisdictions, that disruption carries direct commercial cost. The result is retention economics that work heavily in WiseTech’s favour.

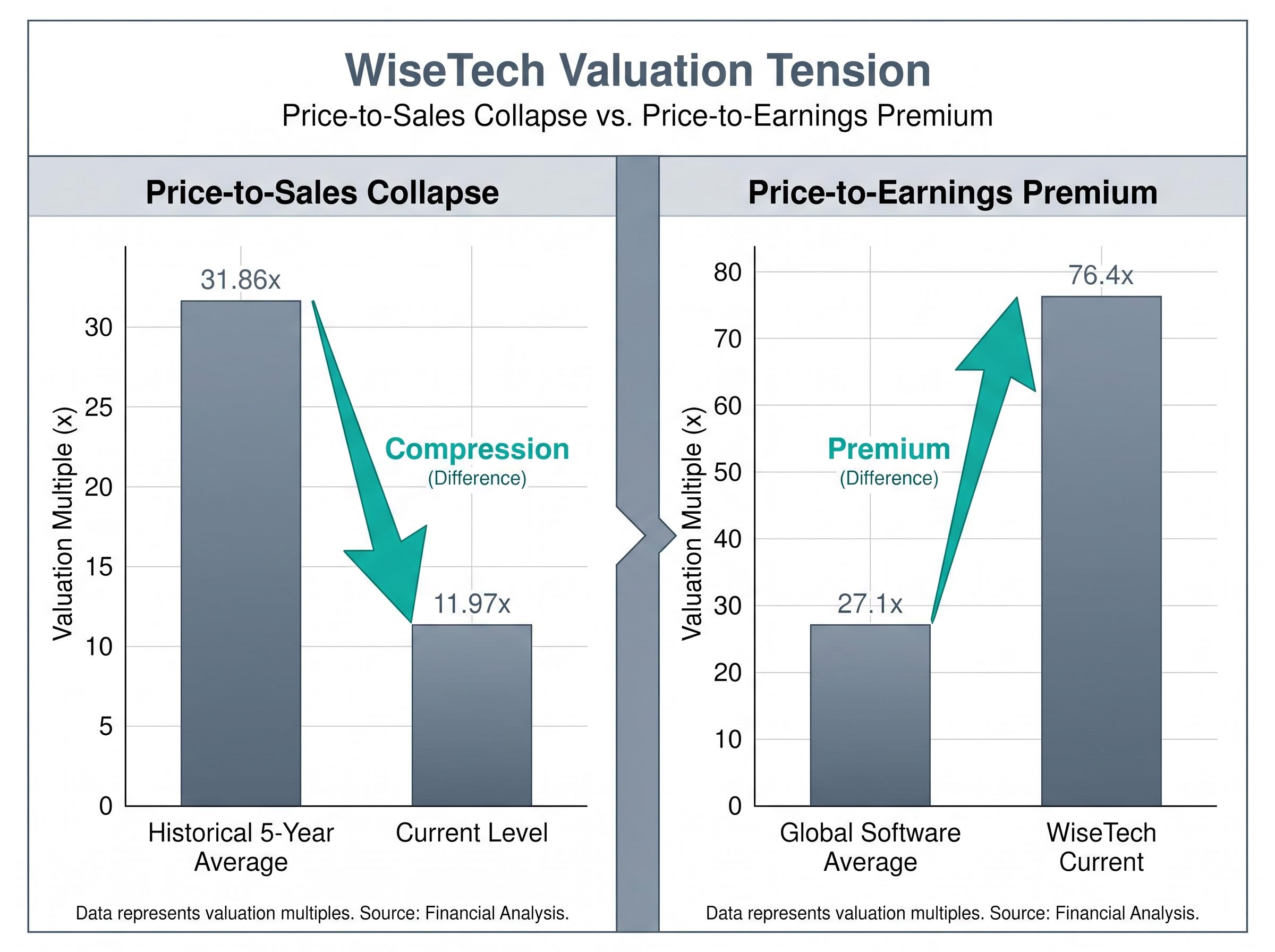

Reading the valuation: what a price-to-sales collapse from 31x to 12x actually means

The price-to-sales (P/S) ratio measures how much investors pay per dollar of a company’s revenue. It is widely used for growth-stage software companies because these businesses often prioritise reinvestment over near-term profit, making traditional price-to-earnings (P/E) ratios less useful as a standalone gauge.

WiseTech’s current P/S multiple is 11.97x. Its five-year average is 31.86x.

Two forces drove that compression simultaneously. The share price fell roughly 46%, and revenue kept growing at a 27.1% CAGR. The numerator shrank while the denominator expanded, producing a multiple that is less than forty per cent of its historical average.

| Metric | Historical / Peer Level | Current WTC Level | Implication |

|---|---|---|---|

| Price-to-Sales | 31.86x (5-year average) | 11.97x | Multiple compression of over 60% |

| Price-to-Earnings | 27.1x (global software average) | 76.4x | Still expensive in absolute terms |

| Broker Consensus Target (Dec 2025) | A$109.91 average | A$70.51 (then-current price) | Approximately 55.9% implied upside |

Webull and Fintel analysis produced a discounted cash flow (DCF) fair value estimate of A$113.39 when the stock was trading near A$68.74, labelling it undervalued on a long-term basis. Macquarie upgraded to Outperform in December 2025 with a target near A$108.50, reversing the Neutral stance it had held since mid-2023.

As of December 2025, covering brokers’ consensus average target of A$109.91 implied approximately 55.9% upside from a price of A$70.51.

The P/S ratio tells a story of a stock that has cheapened dramatically relative to its own history. The P/E of 76.4x, nearly triple the global software average of 27.1x, tells a different story: even after the crash, the market still prices in significant future growth. Both readings are accurate. The tension between them is the central valuation question.

Balance sheet and cash flow strength: assessing WiseTech’s capacity to absorb uncertainty

For investors evaluating a stock that has halved in price, balance sheet health is a gating question. A distressed balance sheet would change the thesis entirely. WiseTech’s does not suggest distress.

The three headline metrics:

- Net debt: Negative $19 million, meaning cash holdings exceed all borrowings

- Debt-to-equity ratio: 4.7%, confirming minimal leverage and no meaningful refinancing risk

- Return on equity (ROE): 12.8% in FY24

Cash flow generation reinforces the earnings quality argument:

- FY25 free cash flow grew 31%, alongside underlying NPAT growth of 30% to US$241.8 million

- 1H26 free cash flow reached $153.6 million, up 24%, even as NPAT growth decelerated to 2%

Annual profit of $263 million compares to approximately $108 million three years prior, implying a profit CAGR of 34.5%. The cash flow trajectory confirms that WiseTech’s reported earnings are backed by real cash generation, not accounting artefacts.

This is not a business at risk of financial implosion. The question for investors is not solvency; it is whether the growth trajectory justifies the valuation the market still assigns.

The risks that remain: why “cheap relative to history” is not a buy signal on its own

The P/S compression tells a compelling story. The risks that follow tell a necessary counter-story, and investors need both before reaching any conclusion.

The three distinct risk categories:

- Valuation risk: WiseTech’s P/E of approximately 76.4x sits well above the global software average of 27.1x and an analyst-estimated fair ratio of 49.2x. A stock trading at nearly three times its peer group’s earnings multiple is still priced for strong execution. A further derating remains possible if growth expectations disappoint again.

- Governance and regulatory risk: Richard White’s continued role as Executive Chair, ongoing ASIC inquiries, and the Federal Police investigation into alleged insider trading represent unresolved headline risks. IG Bank Switzerland noted that governance concerns and environmental, social, and governance (ESG) factors have prompted some institutional exits. White’s collar transaction over part of his holding was described as landing “at a tricky moment for sentiment.”

- Organic growth deceleration risk: The 7% organic revenue growth reported in 1H26 sits far below the 76% reported growth figure, with the gap largely attributable to acquisitions. FY26 guidance of 79-85% revenue growth (US$1.39-1.44 billion) and EBITDA of US$550-585 million (44-53% growth) relies heavily on acquisition contributions. Whether the headline guidance flatters the underlying organic trajectory is a legitimate question.

IG Bank Switzerland described WiseTech as appealing for “patient investors willing to navigate governance concerns and short-term volatility.”

That framing captures the conditional nature of the opportunity. The risks are not theoretical; they are active, unresolved, and capable of triggering further selling.

WiseTech at 12x sales: reset or still priced for perfection?

Two competing readings of the data have emerged, and both carry weight.

The P/S compression from 31.86x to 11.97x, combined with a 27.1% revenue CAGR and 84% gross margin, makes a credible case that the market has overshot to the downside. The December 2025 broker consensus implied approximately 55.9% upside. Macquarie’s trajectory illustrates how dramatically the analytical consensus shifted: from a target of A$59 on a Neutral rating in August 2023 to approximately A$108.50 on an Outperform rating in December 2025, a near-reversal driven entirely by the price falling to levels that made the growth story investable again.

Macquarie cut its WiseTech target to A$59 (Neutral) in August 2023, then upgraded to approximately A$108.50 (Outperform) by December 2025, a shift that tracks the derating rather than any change in the underlying business.

The counterargument is equally direct. A P/E of 76.4x means the stock still demands that the growth story holds. The governance situation is unresolved. Organic growth of 7% in 1H26 raises questions about what happens when acquisition contributions normalise. Simply Wall St data suggests insiders have been net buyers in recent months, though this remains unverified through independent sources.

For patient, long-horizon investors comfortable with governance risk and willing to accept ongoing volatility, the data supports a closer look. For investors requiring near-term certainty or clean governance, the risks remain material. The honest position is that both readings coexist.

Investors wanting to stress-test the bull thesis against the most recent price data will find our deep-dive into WiseTech’s mispricing case examines analyst targets ranging from A$78 to A$138, walks through the three distinct forces behind the 58% peak-to-trough collapse, and assesses what the organic growth trajectory needs to look like for those targets to be achievable.

What to watch before the August results

The 26 August 2026 full-year results represent the next major information event. Three data points will determine whether the current share price reflects opportunity or continued risk:

- Organic revenue growth rate: Whether it accelerates beyond the 7% reported in 1H26, or whether the headline growth figure continues to rely primarily on acquisition contributions

- Governance developments: Any further regulatory actions involving White, ASIC outcomes, or changes to leadership structure

- EBITDA margin trajectory: Whether the guided approximately 40-41% margin holds, confirming that scale economics and integration of acquisitions are progressing as management expects

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.