Five companies dropped out of the S&P/ASX 200 today, and the scale of the declines that put them there tells its own story. Temple and Webster (TPW) has lost roughly 74% of its value over the past 12 months. IDP Education (IEL) is down nearly 56% year-to-date in 2026. Together with Guzman Y Gomez (GYG), Siteminder (SDR), and Web Travel Group (WEB), the five removals span restaurants, education, hotel technology, online retail, and wholesale travel, and every one of them arrived at the same destination: a market capitalisation too small to hold its place in Australia’s benchmark equity index.

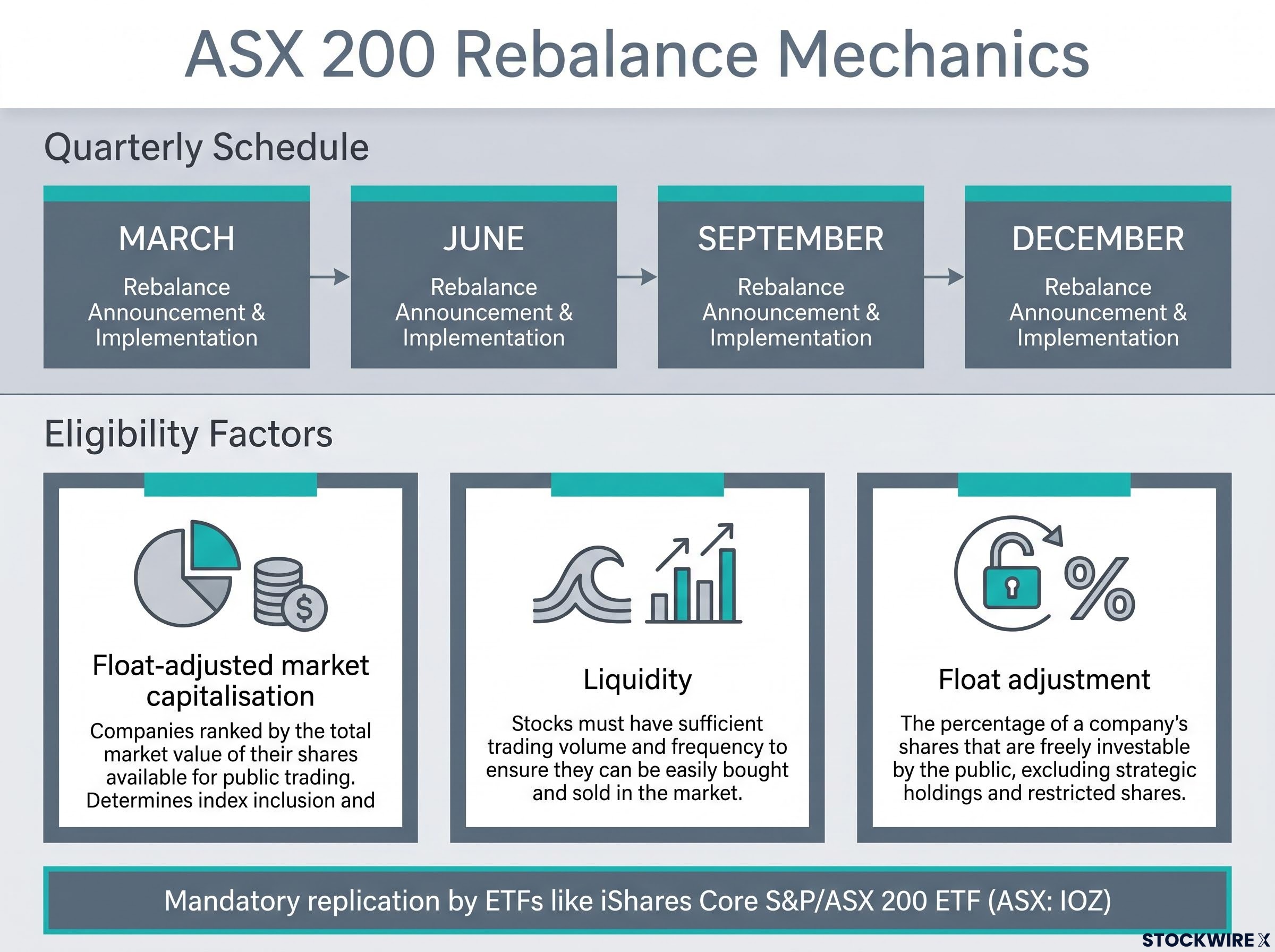

The S&P/ASX 200 completed its June 2026 quarterly rebalance effective 22 June 2026, confirming the five deletions. What follows is a breakdown of what drove each removal, what the departures collectively reveal about where the ASX 200 growth trade stands, and what the changes mean for investors holding the index through ETFs like the iShares Core S&P/ASX 200 ETF (ASX: IOZ).

Five stocks out: the full list and how far each one fell

The numbers speak before the explanations do.

| Company | ASX Code | Sector | 2026 YTD Change | 12-Month Change |

|---|---|---|---|---|

| Guzman Y Gomez | GYG | Consumer Discretionary | -13% | -36% |

| IDP Education | IEL | Education Services | -56% | -33% |

| Siteminder | SDR | Technology (SaaS) | -34% | -12% |

| Temple & Webster | TPW | Online Retail | -59% | -74% |

| Web Travel Group | WEB | Wholesale Travel | -37% | -33% |

TPW’s 74% 12-month decline stands out as the most severe individual stock deterioration among the five, representing one of the sharpest falls recorded by an ASX 200 constituent over the period.

All five sat near the bottom of the index by market capitalisation before their removal. GYG’s exit is notable in its own right: the company listed on the ASX only in 2024 and entered the benchmark shortly after its IPO, making this a round trip of roughly two years from listing to exclusion.

When big ASX news breaks, our subscribers know first

How the ASX 200 rebalance works and why these stocks lost their place

The ASX 200 is not curated by opinion. S&P Dow Jones Indices runs four quarterly rebalances per year, in March, June, September, and December, using a rules-based methodology. Companies are not voted in or out; they either meet the criteria or they do not.

Three factors determine eligibility:

The ASX 200 inclusion criteria are governed not by the ASX itself but by S&P Dow Jones Indices, a distinction that surprises many investors who assume listing on the exchange and appearing in the benchmark are subject to the same rules; the free float minimum alone rises from 20% at listing to 30% for index qualification.

- Float-adjusted market capitalisation: the total market value of a company’s freely tradeable shares must remain above the inclusion threshold

- Liquidity: the stock must trade with sufficient daily volume to allow institutional access

- Float adjustment: only shares available to the public market are counted, excluding locked-up or closely held stock

When a company’s market capitalisation erodes below the threshold, removal is mechanical. ETFs that replicate the index, including the iShares Core S&P/ASX 200 ETF (ASX: IOZ), managed by BlackRock, are then legally required to sell the deleted holdings and purchase the incoming additions at or around the effective date. The fund manager’s own view of the stock’s merit is irrelevant; the mandate is to mirror the index.

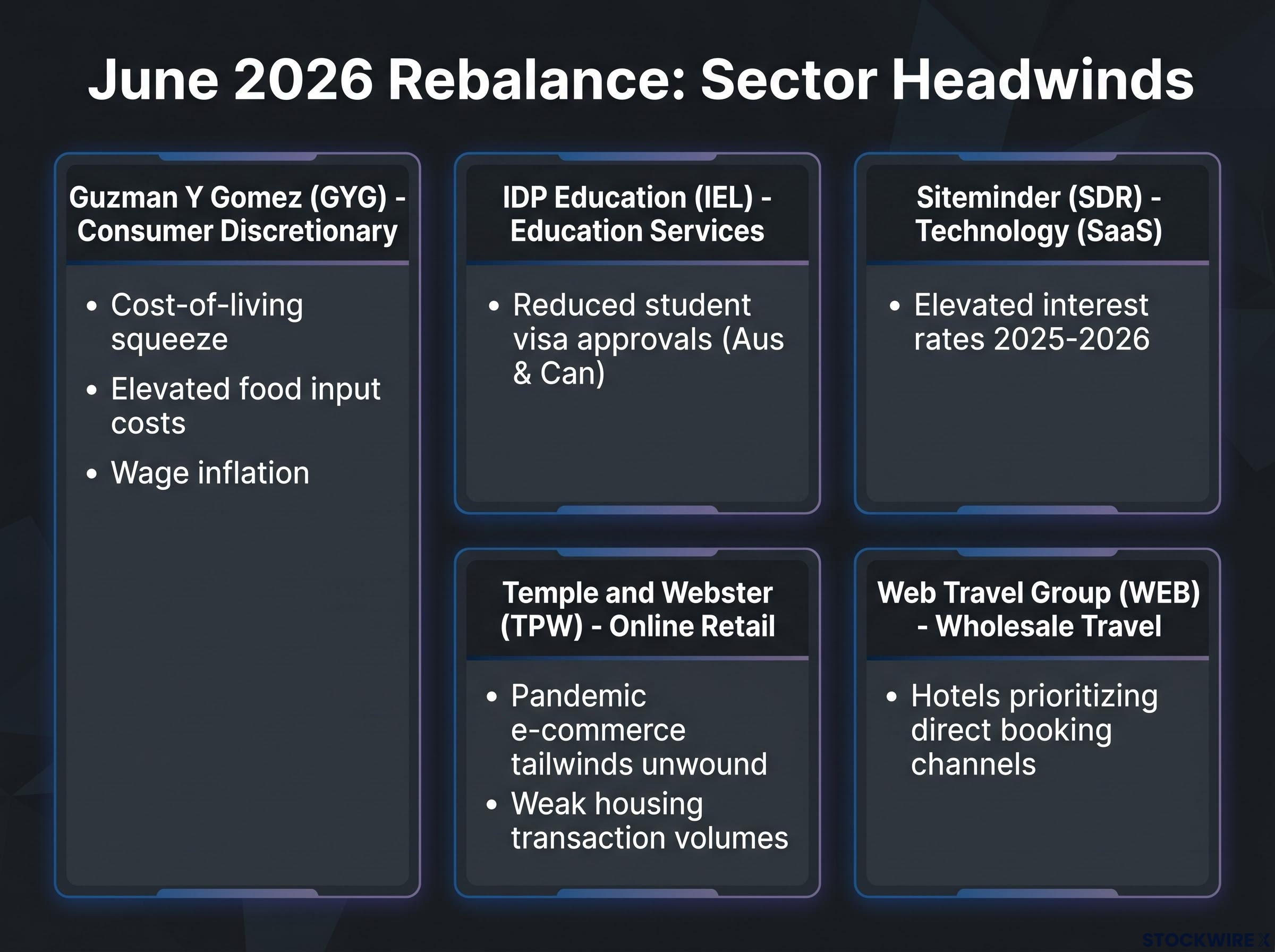

What went wrong at each company

Guzman Y Gomez (GYG)

GYG arrived on the ASX in 2024 carrying a growth premium built on rapid store expansion and consumer enthusiasm for its quick-service restaurant model. That premium has not survived the cost-of-living environment. Elevated food input costs and wage inflation have squeezed margins, while Australian consumers have pulled back on discretionary dining.

The stock has fallen approximately 36% over 12 months. For a company removed from the index within roughly two years of listing, the trajectory illustrates how quickly IPO-era valuations can unwind when the consumer environment shifts.

IDP Education (IEL)

IEL’s decline is structural, not cyclical. Both the Australian and Canadian governments have reduced international student visa approvals and tightened net migration targets, directly compressing the student placement market that forms IEL’s core business.

Canada’s 2025 international student cap, which reduced provincial and territorial allocations by 10% from 2024 levels and extended the cap to include master’s and doctoral students, represents one of the two legislative constraints that have directly compressed IEL’s addressable market in its largest offshore placement corridors.

The damage compounds across revenue lines: IELTS testing volumes are closely tied to student application activity, meaning policy-driven demand destruction hits both placement fees and testing income simultaneously. The approximately 56% year-to-date fall, the steepest among the five on a 2026 basis, reflects a company whose addressable market has been legislated smaller.

Siteminder (SDR)

SDR operates a cloud-based distribution and property management platform for hotels, a SaaS subscription model whose valuation is sensitive to the discount rates applied to future cash flows. As interest rates remained elevated through 2025-2026, the multi-year derating that has compressed ASX-listed technology names since 2022 continued to weigh on the stock.

Competitive pressure from global players and point-solution rivals in the hotel technology segment has added to the headwinds. The 34% year-to-date decline leaves SDR below the market capitalisation floor.

Temple and Webster (TPW)

TPW’s 74% 12-month fall is the most extreme among the five, and the cause is direct: the pandemic-era e-commerce tailwinds that powered the stock have fully unwound.

During lockdowns, forced home-spending and the structural pull-forward of online furniture adoption inflated both revenues and the stock’s growth rating. The normalisation of physical retail removed one support. Prolonged weakness in Australian housing transaction volumes, which correlate strongly with furniture and homewares demand, removed the other. What remains is a business trading at a fraction of its pandemic-era valuation in a market where big-ticket discretionary purchases face sustained consumer caution.

Web Travel Group (WEB)

Global leisure travel has recovered strongly since the pandemic. The margin environment for B2B wholesale travel intermediaries has not.

WEB’s WebBeds division supplies hotel accommodation inventory to travel agents and online travel agencies, a model that relies on healthy distribution margins. Hotel chains have increasingly prioritised direct booking channels, reducing their reliance on wholesale intermediaries and compressing the margins WEB depends on. The approximately 37% year-to-date decline reflects a business caught between rising travel volumes and shrinking intermediary economics.

Five sectors, one shared theme: where the ASX 200 growth trade stands now

The five removals span restaurants, education, hotel technology, online retail, and wholesale travel. They are not, however, five unrelated stories.

All five companies were positioned near the bottom of the ASX 200 by market capitalisation. All five carried elevated growth valuations originating from the 2020-2021 period. All five have faced the sustained reversal of the macro conditions that justified those valuations: cheap capital, pandemic-era consumer behaviour shifts, and expansionary government policy on migration and education.

The ASX 200 has increasingly separated into two tiers. Large-cap financials, resources, and infrastructure names have broadly retained their index positions, while smaller, growth-oriented companies have been systematically squeezed out across multiple quarterly rebalances since 2022.

ASX 200 concentration has intensified as the rebalance cycle removes smaller growth names and the index weight accrues further toward large-cap financials, resources, and infrastructure; with financials and materials alone accounting for more than 50% of the index by market-cap weight, each quarterly removal of a growth-oriented constituent tilts the benchmark incrementally further in that direction.

The technology and SaaS derating has been a multi-year process running from 2022 through 2026, and both SDR and TPW sit within that arc. The international education headwind facing IEL is embedded in legislative changes, not cyclical policy settings. Investors holding other growth-oriented smaller-cap ASX names outside this list may find the pattern worth examining in their own portfolios.

The ASX 200 valuation entering June 2026 at approximately 16.7x forward earnings, well above the long-run average of 14.9x, frames the context in which these five removals land: the index is not cheap at the aggregate level even as individual growth names are being systematically excluded, and the gap between the premium assigned to large-cap names and the deterioration in smaller growth companies reflects the two-tier dynamic playing out in real time.

What the rebalance means for IOZ holders

For long-term holders of IOZ, the practical impact is modest. The ETF will sell all five deleted positions at or around 22 June 2026 and replace them with the incoming additions. The combined weight of the five removed stocks was small given their positions near the bottom of the index by market capitalisation, and the portfolio refreshes automatically.

That automatic adjustment is the self-cleansing property of index investing: passive holders are released from sustained underperformers without needing to make an active decision.

Cap-weighted index construction means the mechanical selling that follows each removal has a self-reinforcing quality: as smaller companies exit and their weights are redistributed to larger constituents, the gap between the top tier and the bottom of the index widens, making it structurally harder for mid-sized growth names to maintain the market capitalisation floor across successive rebalances.

The picture differs for direct shareholders. Three groups of investors are affected differently:

- Long-term IOZ holders with no direct exposure to the deleted stocks face no action required; the ETF adjusts on their behalf

- IOZ holders who also own one or more of the five stocks directly should note that the mechanical selling by index funds at the effective date can add short-term downward price pressure on those direct holdings

- Direct shareholders of the deleted stocks with no IOZ exposure should be aware that index-fund selling is a technical effect, not a new signal about the company’s fundamentals

ETF managers are legally required to replicate index composition and cannot exercise discretion over individual holdings. The selling pressure is typically concentrated in the days immediately before and on the effective date.

The next rebalance is three months away: what to watch

The September 2026 quarterly rebalance is next, and market participants will begin monitoring potential candidates for addition and removal from today onward.

The sector vulnerabilities exposed by the June 2026 removals remain live conditions heading into the next quarter:

- Consumer discretionary spending under sustained cost-of-living pressure

- International student policy settings constraining education sector revenues

- SaaS and technology valuation multiples still adjusting to the higher-rate environment

- B2B travel distribution margins facing continued pressure from direct booking channels

The rebalance calendar (March, June, September, December) is a recurring feature of index investing. The June 2026 removals are part of a continuous process of market-cap-driven index renewal.

A market that keeps its own score

The S&P/ASX 200 does not make qualitative judgments. GYG, IEL, SDR, TPW, and WEB were removed because their market capitalisations fell below the line. For shareholders in those five companies, the declines represent real losses during a period of genuine business difficulty. For passive investors, the index did what it is designed to do: it adjusted, automatically, to reflect the market as it stands today.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.