Lululemon Fundamental Analysis: the Price of Brand Dilution

1 hr ago

The global pharmaceutical sector is undergoing a profound structural rotation, and the divergence has never been clearer than in the first quarter of 2026. While traditional immunization portfolios face mounting distribution hurdles, specialised therapeutic treatments are commanding unprecedented profitability. This stark contrast anchors the latest AstraZeneca earnings report, revealing a distinct shift in how British pharmaceutical giants are generating revenue. What follows is a comprehensive breakdown of the financial metrics, sector rotations, and domestic infrastructure impacts defining the quarter.

This analysis examines the financial outperformance driven by oncology and rare diseases, evaluating how these high-margin segments insulate broader portfolios from macroeconomic headwinds. Finance professionals and life sciences investors require precise data to understand the underlying mechanics of this transition. By dissecting the recent quarterly results and their direct translation into massive domestic capital expenditure, this report delivers the necessary context to evaluate the trajectory of the British life sciences sector.

The pharmaceutical industry is actively recalibrating its growth models to absorb prevailing macroeconomic headwinds facing standard immunization portfolios across North America and Europe. General revenue streams are compressing under the weight of shifting geopolitical and social factors. This compression forces global entities to rotate capital toward specialty medicines, rare diseases, and oncology as the new foundational pillars of pharmaceutical growth.

Comparative macroeconomic studies in the Quantastic Journal pharmaceutical review illustrate how preventative medicine profit margins continue to lag significantly behind the pricing power enjoyed by novel targeted treatments.

The challenges facing traditional mass-market portfolios are multi-faceted and persistent. Investors must account for the following primary headwinds currently dampening global immunization distribution:

Increased vaccine hesitancy stemming from highly polarised political climates, particularly within the United States. Complex logistical distribution hurdles that elevate operational costs across European markets. * Heightened regulatory scrutiny over broad-spectrum pricing models that limit margin expansion.

Despite these immediate distribution and hesitancy challenges, the underlying demand for preventative medicine remains intact. Market projections indicate the global vaccine market is still expected to scale from $76.8 billion in 2026 to $117 billion by 2033. However, the current margin pressure explains why capital is rotating rapidly toward targeted therapeutic engines that offer superior pricing power and insulated revenue streams.

The rotation toward specialty therapeutics directly fueled a significant financial beat for AstraZeneca in the first quarter. The company absorbed broader industry pressures and delivered total quarterly revenue of $15.3 billion, representing an 8% increase at constant exchange rates. This performance validates the management strategy to prioritise high-margin therapeutic areas over standard market volumes.

The headline figures demonstrate substantial outperformance against market consensus. The reported revenue of $15.29 billion comfortably exceeded the market expectation of $14.74 billion, delivering a positive variance of $545.93 million. Furthermore, the full-year 2026 guidance projects mid-to-high single-digit revenue growth and low double-digit Core Earnings Per Share (EPS) growth.

Financial disclosures verified by Reuters market coverage show that the total revenue beat was fundamentally driven by the expanding oncology and rare disease units.

| Metric | Q1 2026 Reported | Market Expectation | Variance |

|---|---|---|---|

| Total Revenue | $15.29 billion | $14.74 billion | +$545.93 million |

| Revenue Growth (Constant FX) | 8.0% | N/A | N/A |

| Core EPS Growth Projection | Low double-digit | N/A | N/A |

The underlying divisional metrics reveal exactly where this revenue beat originated. According to company data, the tumor treatment portfolio expanded by 16%, while rare condition therapies increased by 15% during the quarter.

These specific high-growth segments effectively insulated the broader portfolio from other sector weaknesses. The double-digit expansion in oncology and rare diseases confirms that targeted treatments are now the primary engines of corporate profitability.

The financial outperformance of specialty segments requires an understanding of the underlying business mechanics driving modern pharmaceutical economics. Specialty medicines and rare disease therapies differ fundamentally from mass-market immunizations, which rely on immense volume and low individual unit costs. In contrast, targeted therapies address smaller, highly specific patient populations with complex medical needs.

This economic model grants pharmaceutical developers significant pricing power, supported by the extraordinarily high research and development barriers to entry. Competitors cannot easily replicate the advanced biological engineering required to produce these treatments, allowing the original developers to command premium margins. The strategy relies on securing regulatory clearance for novel treatments that address unmet medical needs.

Securing European orphan drug designations for these specialised medicines grants developers extended market exclusivity periods; this regulatory moat protects the premium pricing required to offset immense research expenditures.

According to industry reports, four fresh medical therapies receiving regulatory clearance since the start of the 2026 calendar year directly support this high-margin strategy. These targeted approvals ensure a continuous pipeline of premium-priced assets to offset legacy product declines.

Pricing Power in Specialised Therapeutics The transition toward rare disease portfolios fundamentally alters corporate valuation, as developers secure insulated revenue streams supported by stringent patent protection and significant barriers to entry.

While AstraZeneca demonstrates the upside of specialty dominance, GSK provides a nuanced picture of an entity successfully navigating a pressured transition. The latest quarterly turnover for GSK highlights operational improvement, despite missing broader United States dollar market expectations. Q1 turnover was reported at £7.6 billion, representing a 5% increase at constant exchange rates.

When translated to USD terms, the revenue landed at approximately $10.10 billion, missing the projected $10.42 billion. However, the internal divisional performance proves that GSK is successfully executing the same specialty pivot as its peers. According to company data, the most striking metric is the massive 28% surge in tumor medication revenue, demonstrating formidable momentum in the oncology space.

This specialty success is vital, as the company must counterbalance broader immunization market weakness in the Americas. According to company data, the shingles immunization portfolio, known as Shingrix, achieved unprecedented commercial returns exceeding £1 billion, serving as a critical stabiliser. Analyst consensus projects core EPS around 180-206 pence for FY 2026, reflecting confidence in this balanced transition.

Investors exploring how these two British pharmaceutical giants are navigating their respective transitions will find our detailed coverage of the AstraZeneca and GSK quarterly divergence, which breaks down segment-by-segment revenue growth and pipeline valuations.

| Therapeutic Area | Q1 Performance | Strategic Impact |

|---|---|---|

| Tumor Medication | 28% revenue surge | Validates the ongoing pivot toward specialty therapeutics. |

| Shingrix Immunization | Exceeded £1 billion returns | Counterbalances broader vaccine market vulnerabilities. |

| Total Quarterly Operations | £7.6 billion turnover | Delivers 5% constant currency growth despite USD miss. |

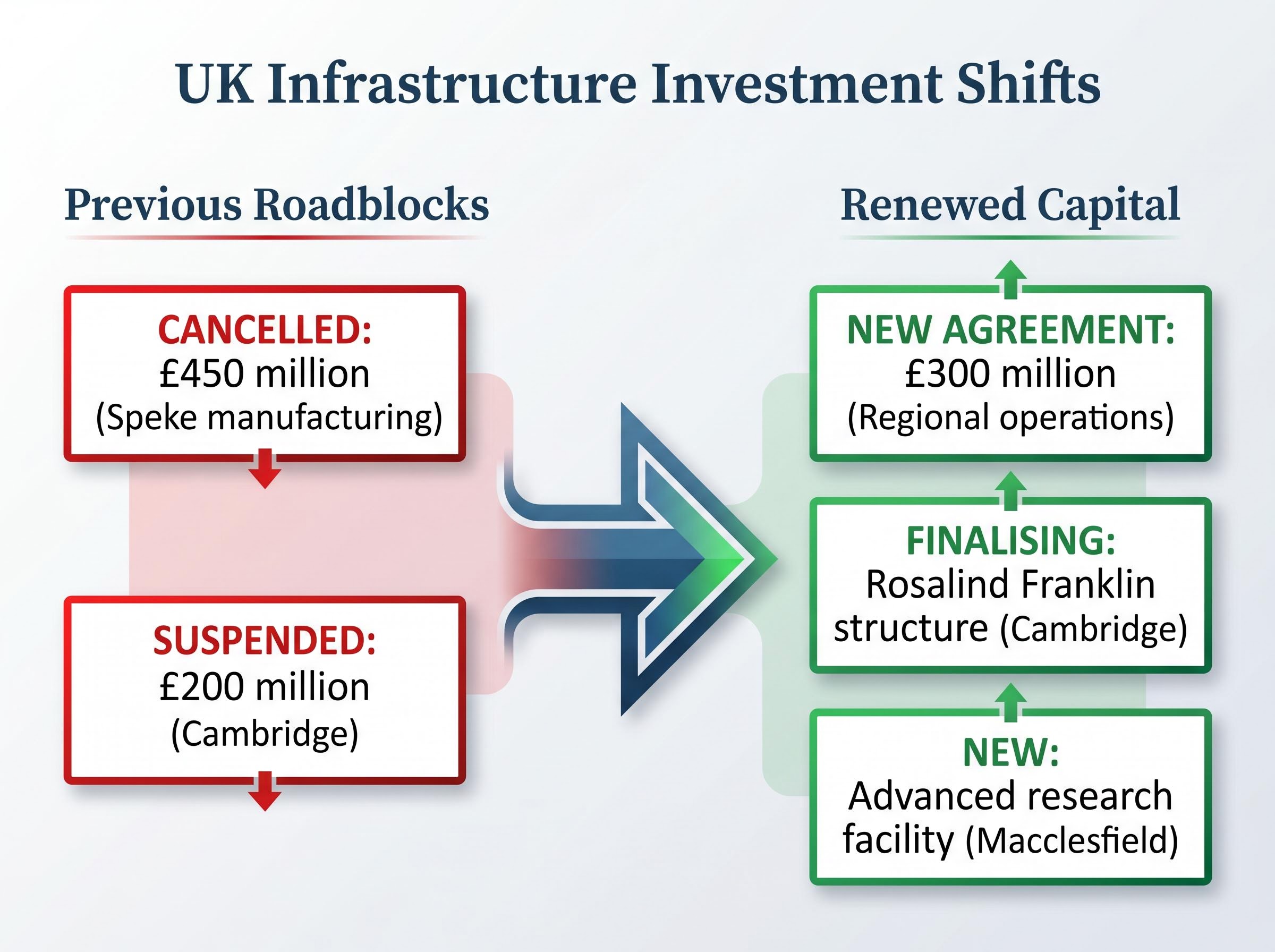

The impressive global sales figures are now translating directly into tangible domestic infrastructure investments within the United Kingdom. Following intense negotiations with American authorities and local leadership, the life sciences ecosystem received a massive vote of confidence through a sudden reversal of suspended expansion plans. This capital allocation carries significant political weight, highlighted by Prime Minister Keir Starmer announcing the renewed commitment.

Historically, the sector faced substantial friction regarding National Health Service accessibility and medication valuation frameworks. These commercial disagreements previously forced companies to freeze capital expenditure, threatening regional employment and technological advancement. The recent negotiations have clearly resolved these structural bottlenecks.

The historical context surrounding these domestic infrastructure allocation decisions reveals significant friction over National Health Service pricing frameworks, which had previously prompted multinational developers to pivot investments toward more accommodating international markets.

The commercial conditions that caused earlier pauses have shifted dramatically, prompting Chief Executive Officer Pascal Soriot to praise recent regulatory authority improvements. This improved relationship unlocked the sudden deployment of capital that had been stalled for months.

The scale of this reversal is best understood by comparing the historical cancellations against the newly committed funds:

The financial outcomes of the first quarter of 2026 deliver a definitive verdict on modern pharmaceutical strategy. Mastery over oncology and rare diseases is now the defining metric for corporate growth, insulating entities from the logistical and political headwinds facing mass-market immunizations. The aggressive revenue expansion in these targeted areas proves the viability of the specialty medicine rotation.

Crucially, these impressive financial beats from global sales are translating into tangible domestic infrastructure investments across the UK. The resolution of historical regulatory friction has unlocked hundreds of millions in capital expenditure, securing advanced manufacturing and research facilities. As the calendar progresses through 2026, the British life sciences sector is positioned to leverage this renewed capital confidence on the global stage.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AstraZeneca's Q1 2026 earnings were primarily driven by significant growth in its oncology and rare disease segments, which expanded by 16% and 15% respectively, exceeding market expectations.

The pharmaceutical sector is recalibrating its growth model by rotating capital toward specialty medicines, rare diseases, and oncology, moving away from broad immunization portfolios due to macroeconomic headwinds and margin pressures.

Specialty therapeutics offer significant pricing power and insulated revenue streams due to high research and development barriers to entry and regulatory clearance for novel treatments addressing unmet medical needs.

Yes, AstraZeneca's impressive global sales have translated into renewed capital confidence in the UK life sciences sector, with a new £300 million commitment for upgrading regional operations and research facilities.

GSK also demonstrated a successful specialty pivot with a 28% surge in tumor medication revenue, which helped counterbalance broader immunization market weakness and validated a similar strategic direction to AstraZeneca.