Why Drug Reformulation Carries Less Risk Than Investors Price in

5 hrs ago

Most investors spend hours researching which stocks to buy. Almost none spend an hour thinking about which account to buy them in. That single structural decision, where an investment sits rather than what it is, can quietly cost or save tens of thousands of dollars over a lifetime of investing.

The U.S. tax code treats the same investment activity very differently depending on the account type it occurs in, the holding period involved, and what happens to the asset at the end of the investor’s life. These rules are not hidden, but they are rarely discussed alongside stock selection decisions in ways that make the stakes concrete. What follows is a practical framework for understanding how tax drag erodes returns, why account structure determines whether stock picking is mathematically defensible, and how to match investment activity to the right account type. The result is a clear decision rule applicable to any portfolio.

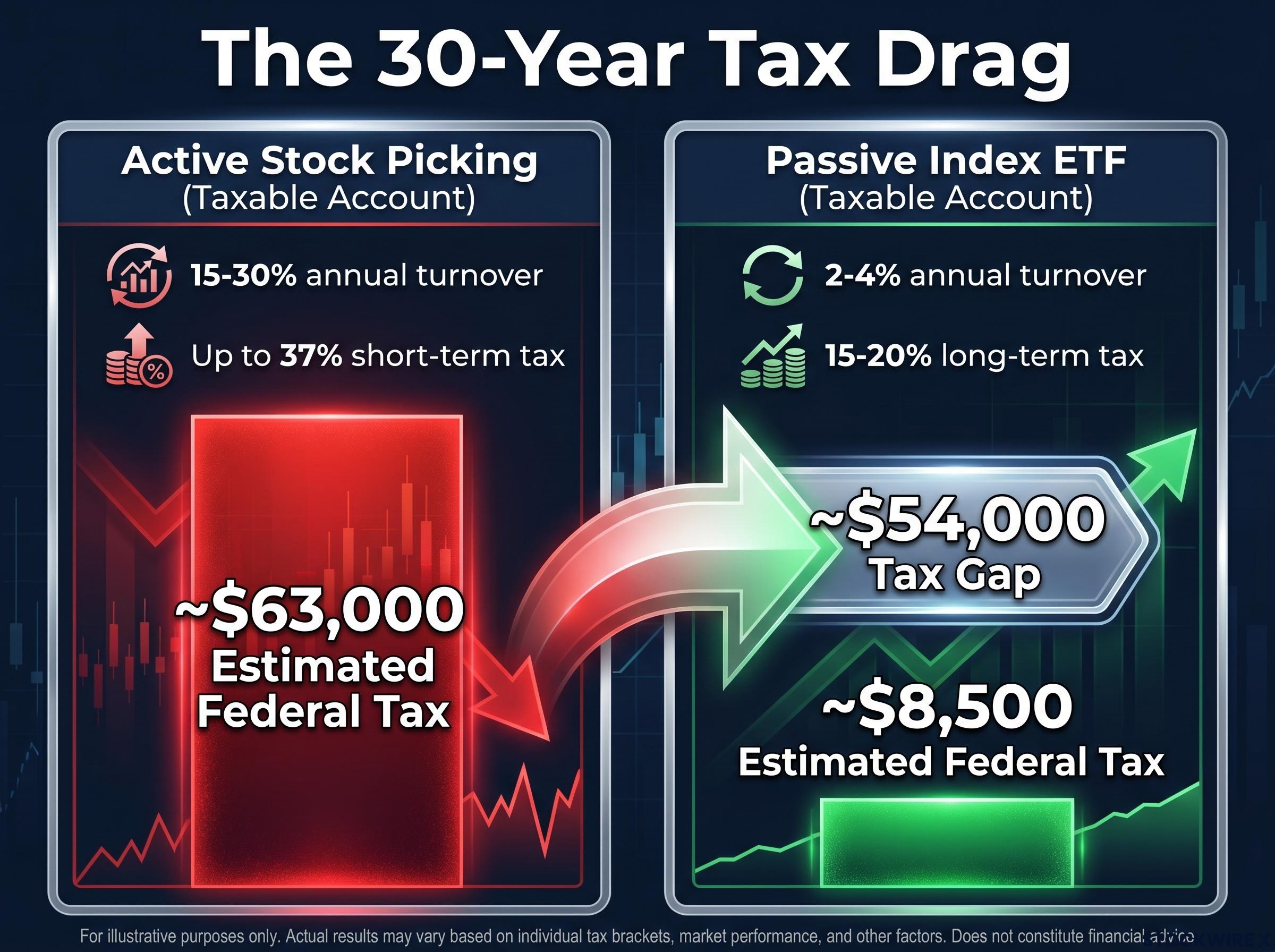

Consider two investors who start with the same capital, earn the same annual return, and invest for 30 years. One actively picks stocks in a taxable brokerage account, turning over 15-30% of holdings each year. The other buys a broad-market index ETF with annual turnover of just 2-4% and never sells.

The active investor pays approximately $63,000 in federal taxes on realised trading gains over that period. The index investor pays roughly $8,500. The gap is around $54,000, and it compounds: every dollar paid in tax is a dollar permanently removed from the base on which future returns are earned.

The data on active vs passive investing is unambiguous at the fund level: over 90% of active large-cap managers underperform the S&P 500 over a 20-year horizon, a failure rate William Sharpe’s 1991 arithmetic principle identifies as structural rather than cyclical, since active managers collectively cannot exceed the market return before fees.

The mechanism is straightforward. Each sale in a taxable account is a taxable event. Short-term capital gains (assets held one year or less) are taxed at ordinary income rates, currently up to 37% federally. Long-term gains receive preferential treatment at 0%, 15%, or 20%, with a potential 3.8% Net Investment Income Tax for high earners. Active traders, by definition, realise gains more frequently and at shorter holding periods, paying higher rates on a larger share of their returns.

The IRS Topic 409 capital gains rates confirm the current federal schedule: short-term gains taxed at ordinary income rates up to 37%, long-term gains at 0%, 15%, or 20% depending on taxable income, with the 3.8% Net Investment Income Tax applying to high earners above applicable thresholds.

According to Russell Investments, the average U.S. equity product surrendered approximately 2% of pre-tax return to taxes over a recent three-year period.

The SEC has noted that for stock funds, the annual tax impact has ranged up to 5.6 percentage points per year for the least tax-efficient funds.

| Strategy | Typical Turnover Rate | Applicable Tax Rate | Estimated 30-Year Federal Tax Cost |

|---|---|---|---|

| Active stock picking (taxable account) | 15-30% annually | Up to 37% (short-term); 15-20% (long-term) | ~$63,000 |

| Passive index ETF (taxable account) | 2-4% annually | 15-20% (long-term, if realised) | ~$8,500 |

Assumptions: illustrative figures based on a common starting capital, assumed annual return, turnover rates as shown, and an effective federal capital gains rate. Actual results vary by individual circumstances.

The gap between active and passive is not just about how often an investor trades. The investment vehicle itself carries structural tax consequences that operate independently of any decision the shareholder makes.

Index ETFs such as VOO utilise an in-kind creation and redemption mechanism. When large institutional participants redeem shares, the ETF delivers a basket of underlying securities rather than selling them on the open market. This process generally avoids triggering taxable capital gain distributions to remaining shareholders. The result is that most index ETF investors control when they personally realise gains: taxes are deferred until the investor decides to sell.

BlackRock has noted that ETFs, including active ETFs, have historically been more tax-efficient than mutual funds. The structural differences come down to three points:

Many actively managed mutual funds distribute taxable capital gains to shareholders annually, even when the shareholder takes no action. A fund manager selling appreciated positions to rebalance or meet redemptions generates gains that are passed through as distributions. These are taxable in the year of distribution regardless of whether the investor sold a single share.

This makes actively managed mutual funds materially less suitable for taxable accounts compared to low-turnover index ETFs. The tax drag is silent, and it is structural rather than behavioural.

The U.S. tax code does more than tolerate patient capital. Under current federal law, it actively rewards it through a provision that can eliminate decades of accumulated capital gains in a single step.

When an investor dies holding appreciated securities, the cost basis resets to fair market value on the date of death. Heirs owe zero federal capital gains tax on any appreciation that occurred during the decedent’s lifetime.

This is the step-up in cost basis. Heirs are taxed only on appreciation that occurs after the date of inheritance, if they subsequently sell. For a long-term index investor who holds positions for decades without selling, this means unrealised gains accumulated over an entire investing lifetime can be passed to the next generation with no capital gains tax liability attached.

The contrast with active trading is stark. An investor who rotated positions over those same decades realised and paid taxes on gains throughout their lifetime. There is no equivalent recovery mechanism. The capital consumed by annual tax bills is gone permanently.

This distinction converts a multi-decade buy-and-hold strategy from merely tax-deferred to potentially tax-eliminated, a meaningful difference from a generational wealth perspective. One caveat applies: the step-up provision exists under current law and could be modified or repealed by future legislation. Capital gains rates and retirement account contribution limits are similarly subject to legislative change.

The step-up provision’s long-term value depends entirely on its legislative survival, and unrealized capital gains tax proposals have resurfaced repeatedly at the federal level, most recently as part of Biden-era budget discussions, while constitutional questions left open by the Supreme Court in Moore v. United States (2024) mean the legal framework for taxing paper gains remains unsettled.

A concentrated position held for 30-plus years without any trading activity theoretically mirrors the tax profile of a buy-and-hold index investor. Gains remain unrealised, and the step-up provision can eliminate all accumulated tax liability at death.

The behavioural reality is different. Very few investors hold a concentrated position through multiple severe drawdowns without trimming or rotating. The 30-year no-trade threshold is rare in actual practice. Beyond behaviour, concentration risk makes the tax discussion secondary: the company may fail entirely, rendering any tax efficiency irrelevant. A diversified index automatically removes failing companies and captures top performers without requiring any trading decision from the investor.

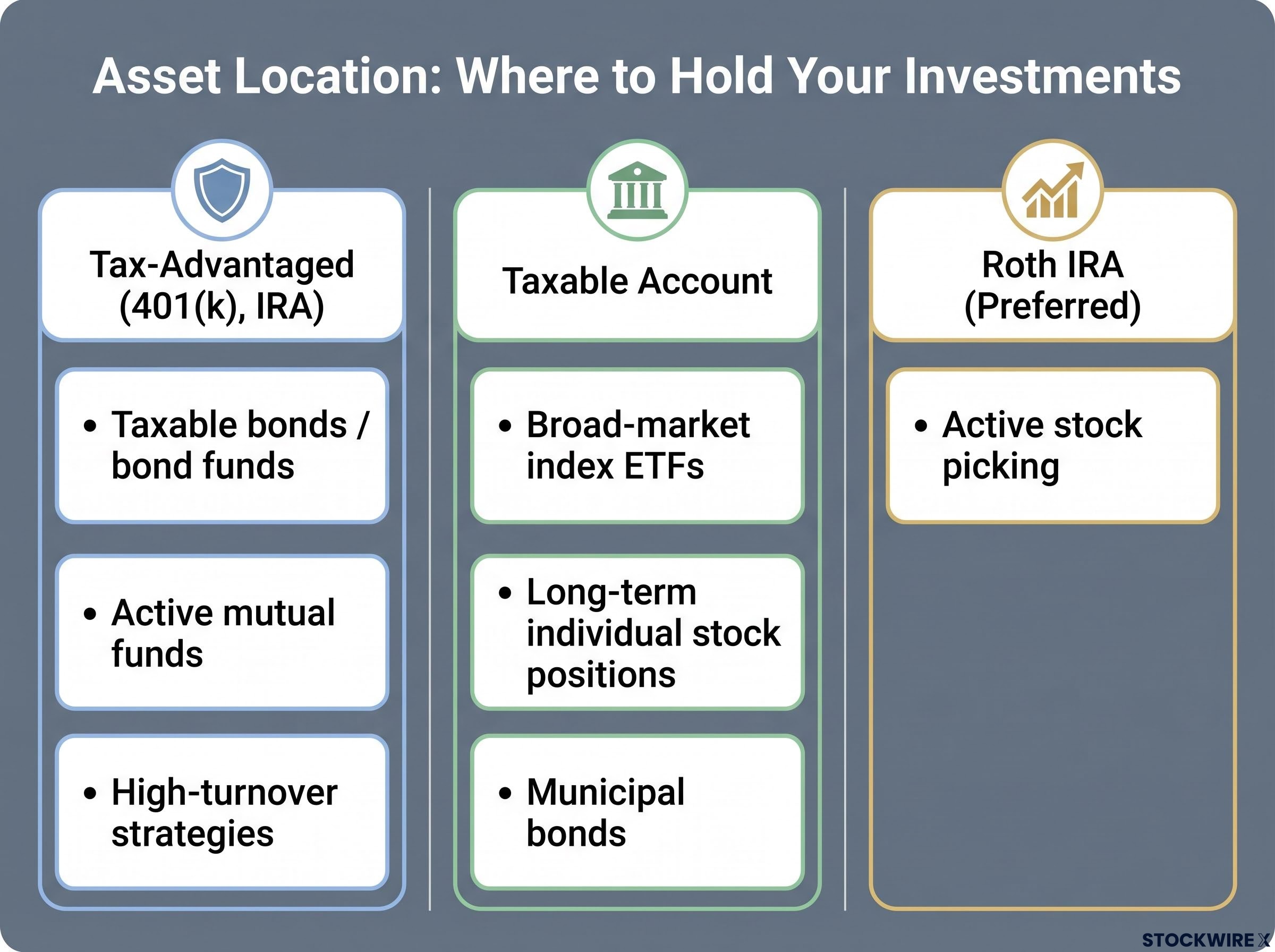

Account type is not administrative paperwork. It is the variable that determines whether the same trading activity is rational or self-defeating. Each account creates a distinct decision environment.

Taxable brokerage accounts are the home for patient capital. Realised gains and dividends are taxable in the year they occur, with short-term gains taxed at ordinary income rates and long-term gains at preferential rates. This makes taxable accounts best suited for low-turnover index ETFs and long-term individual stock positions where the step-up provision may apply. They are the worst possible location for frequent trading.

Traditional 401(k) accounts defer all taxes until withdrawal. Contributions are pre-tax, growth compounds without annual tax bills, and trading inside the account generates no current tax liability. The trade-off: all withdrawals are taxed as ordinary income regardless of whether the underlying gains were long-term or short-term. The long-term capital gains rate does not apply.

The IRS Roth comparison chart sets out the official contribution limits, income thresholds, and qualified distribution requirements that govern both Roth IRAs and traditional 401(k) accounts, confirming that all withdrawals from pre-tax 401(k) balances are taxed at ordinary income rates regardless of how the underlying gains were earned.

Roth IRAs are structurally the most rational location for active stock picking. Contributions are after-tax, but qualified withdrawals in retirement are entirely tax-free, including all accumulated gains. Trading inside the Roth has no tax impact at any point. This removes the core objection to active trading (tax drag on turnover) while preserving the full upside on outperformance. The binding constraint is capacity: annual contribution limits mean the Roth IRA is a bounded resource that must be allocated deliberately.

Conducting individual stock picking inside a taxable brokerage account when Roth IRA contribution room is available is one of the most costly structural errors a retail investor can make.

| Account Type | Tax Treatment of Gains | Tax Treatment of Withdrawals | Best Suited For | Worst Use Case |

|---|---|---|---|---|

| Taxable brokerage | Taxed annually as realised | N/A (no withdrawal restriction) | Low-turnover index ETFs, long-term holds | Frequent trading |

| Traditional 401(k) | Tax-deferred until withdrawal | Ordinary income rates on all withdrawals | Tax-inefficient assets, bonds, active funds | Assets that would benefit from long-term capital gains rates |

| Roth IRA | None (tax-free growth) | Tax-free (qualified withdrawals) | Active stock picking, highest-growth assets | Holding tax-exempt bonds (wastes tax-free space) |

The framework from the previous section translates into a concrete sorting rule. Tax-inefficient assets belong in tax-advantaged accounts, where their annual taxable distributions are sheltered. Tax-efficient assets belong in taxable accounts, where they can benefit from preferential long-term rates and the step-up provision.

Broad-market index funds with expense ratios near 0.05% are available commission-free on major platforms and represent the foundational holding in a tax-efficient portfolio structure, capturing diversified market returns without the turnover that creates annual tax bills in taxable accounts.

| Asset or Strategy | Recommended Account | Primary Reason |

|---|---|---|

| Taxable bonds / bond funds | Tax-advantaged (401(k), IRA) | Interest income taxed at ordinary rates |

| Active mutual funds | Tax-advantaged | Annual capital gain distributions regardless of investor action |

| High-turnover strategies | Tax-advantaged | Frequent realisation events create annual tax bills |

| Broad-market index ETFs | Taxable account | Low turnover, in-kind redemptions, minimal distributions |

| Long-term individual stock positions | Taxable account | Unrealised gains, potential step-up benefit at death |

| Municipal bonds | Taxable account | Interest typically federal tax-exempt; tax shelter unnecessary |

| Active stock picking | Roth IRA (preferred) | Zero tax drag on turnover; full gain retained |

Municipal bond interest is typically exempt from federal tax, which means placing them inside a tax-advantaged account wastes sheltered space without providing additional benefit.

For active investors who do trade in taxable accounts, tax-loss harvesting is the primary mitigation tool:

Stock picking is neither always irrational nor always wise. The question is whether the conditions required for it to be rational are actually met. Three conditions, applied together, form a defensible test:

All three conditions carry equal weight. Meeting two of three does not make the activity defensible.

The decisions that compound most powerfully over a 20-plus year accumulation horizon are structural, not tactical. They happen before a single stock is selected, and they operate in silence for decades.

The framework reduces to three steps, in order of priority:

This hierarchy is most consequential for investors in the accumulation phase with a multi-decade horizon, where compounding differences between tax-efficient and tax-inefficient structures have the most time to manifest. Over shorter periods, the gap is smaller. Over 20-plus years, it dominates.

All advantages described in this framework, including capital gains rates, the step-up in basis provision, and retirement account contribution limits, reflect current U.S. federal law and are subject to future legislative changes.

The single most impactful structural decision most retail investors can make right now is straightforward: move any planned individual stock picking activity out of a taxable brokerage account and into the Roth IRA before the next contribution window closes. The stock selection can wait. The structure should not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and all tax provisions discussed are subject to change based on future legislation.

Tax efficient investing means structuring your portfolio so that the least possible return is lost to taxes each year. Because every dollar paid in tax is permanently removed from your compounding base, the structural decisions around account type and asset location can be worth tens of thousands of dollars over a 30-year horizon.

A Roth IRA is the most rational account for active stock picking because qualified withdrawals, including all accumulated gains, are entirely tax-free, eliminating the tax drag on frequent trading that makes stock picking in a taxable brokerage account so costly.

The step-up in cost basis is a U.S. tax provision that resets the cost basis of inherited securities to fair market value on the date of the original owner's death, meaning heirs owe zero federal capital gains tax on any appreciation that occurred during the decedent's lifetime.

Based on illustrative figures in the article, an active stock picker turning over 15-30% of holdings annually in a taxable account pays approximately $63,000 in federal taxes on realised gains over 30 years, compared to roughly $8,500 for a passive index ETF investor, a gap of around $54,000.

Tax-efficient assets such as broad-market index ETFs, long-term individual stock positions, and municipal bonds belong in taxable accounts, while tax-inefficient assets such as bonds, active mutual funds, and high-turnover strategies belong in tax-advantaged accounts like a 401(k) or IRA where their annual taxable distributions are sheltered.