The most consequential events in financial history, the collapse of a reserve currency, the moment one great power overtakes another, the restructuring of a sovereign debt pile so large it reshapes an entire monetary system, happen so rarely that no living investor has a playbook for them. Most have never experienced even one. That gap between lived experience and historical reality is where the largest portfolio risks hide.

Survivorship bias in investment strategy is one reason the gap between lived experience and historical reality Dalio identifies is so persistent: the investors who lost money during prior debt-cycle resolutions and regime changes rarely become the public voices shaping how the next generation thinks about risk.

Ray Dalio spent years building a historical dataset spanning roughly 500 years and multiple great powers specifically because he recognised this problem. The research, published as Principles for Dealing with the Changing World Order, was not an academic exercise. It was a direct response to an epistemological blind spot: the events most likely to destroy portfolios were, by definition, absent from recent market data.

What follows here is a structural map of the five forces Dalio identified as drivers of every major cycle of rise and decline, how they interact, what his quantitative bubble gauge is signalling right now, and what all of it means for the way you think about your own positioning.

Why standard market history leaves investors exposed

Most institutional risk models draw on 20 to 40 years of data. That window captures recessions, corrections, and even the occasional financial crisis. What it does not capture is the kind of event that rewrites the rules entirely: a currency regime collapse, a reserve-currency sovereign default, or a hegemonic power transition. These phenomena occur only once or twice per century. They sit outside the dataset.

Dalio’s response was to extend the dataset. By studying the rise and fall of the Dutch, British, American, and Chinese empires across centuries, he arrived at a conclusion that reframes how you should think about tail risk: the mechanisms are not random. They are mechanical and repeatable.

Across different civilisations and centuries, the same underlying combination of conditions has appeared before every major collapse of monetary, political, and geopolitical order.

That finding is the foundation of everything that follows. The same underlying causes, debt excess, internal conflict, external power shifts, nature shocks, and technology transitions, have appeared before every major systemic breakdown his research identified. Your job as an investor is not to predict when the next one arrives. It is to recognise the configuration when it is present.

When big ASX news breaks, our subscribers know first

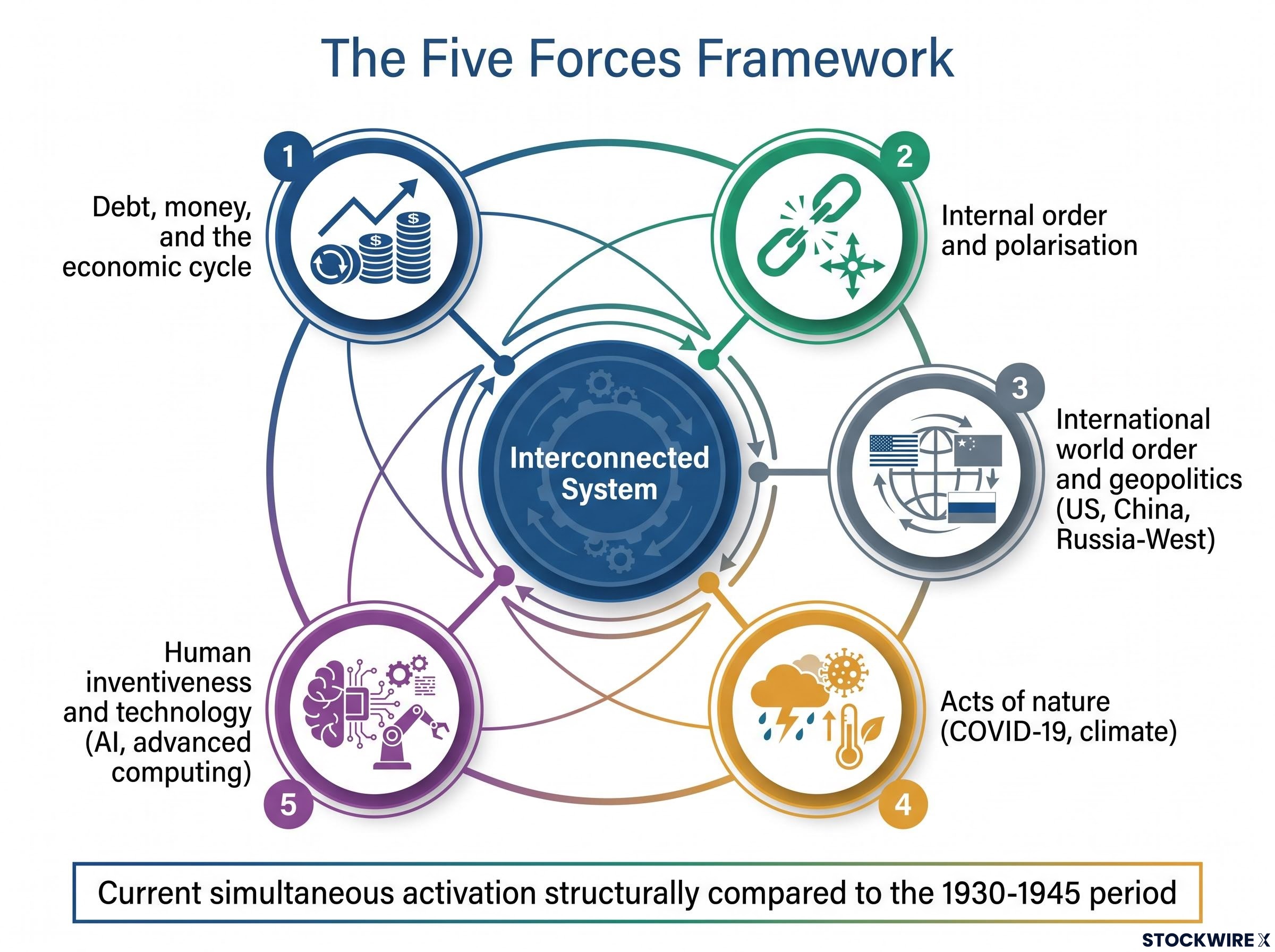

The framework at a glance: five forces, one cycle

Dalio’s framework organises the forces that drive these long cycles into five categories. Before examining each in depth, here is the structural map:

- Debt, money, and the economic cycle: Credit expansion, debt accumulation, and the boom-bust dynamics that eventually force restructuring.

- Internal order and polarisation: Wealth inequality, values conflicts, and the erosion of institutional trust that constrains policy responses.

- International world order and geopolitics: The rules governing relations between great powers, and what happens when those rules break down.

- Acts of nature: Droughts, floods, pandemics, and climate-driven costs that impose fiscal burdens and trigger political upheaval.

- Human inventiveness and technology: The most consistently positive long-run force, currently expressed through artificial intelligence and advanced computing.

These are not five separate risks to monitor independently. They form one interconnected system.

How the forces create one cycle

The power of the framework lies in the interactions. Debt stress (Force 1) makes politically painful adjustments, higher taxes, reduced spending, harder to implement when polarisation (Force 2) is already high. Geopolitical competition (Force 3) encourages defence spending, reshoring, and trade barriers, which reduce economic efficiency and deepen fiscal pressures that feed back into the debt cycle. Acts of nature (Force 4) add further supply-side shocks and fiscal burdens on top of already-strained budgets. And technology (Force 5), while offering productivity relief, simultaneously reshapes labour markets and the distribution of gains in ways that can intensify domestic conflict and fuel a technology race between competing powers.

Dalio’s comparison of the current moment to the 1930-1945 period rests on precisely this simultaneous activation, not any single force in isolation. All five forces are currently in a disruptive phase at the same time, and his assessment is that this configuration makes negative surprises more likely than positive ones. For you, the 1930-1945 comparison is not a prediction of war. It is a structural similarity in the combination of forces present, which determines the probability distribution of outcomes you should be positioning for.

The debt cycle: from expansion to inevitable resolution

Credit does something deceptively simple: it expands buying power today by borrowing from tomorrow. When an economy is growing and incomes are rising, debt-service obligations remain manageable. The trouble is mechanical. As debt accumulates relative to income, the servicing burden compresses spending capacity. At some point, the maths forces a resolution.

The resolution options are limited, and none of them are painless. Inflation erodes the real value of the debt but punishes savers and fixed-income holders. Default wipes out creditors. Restructuring redistributes losses. Each path produces severe consequences for different groups, which is precisely where this force connects to the political one.

There is a systemic dimension that makes the problem harder to contain. Every debt is simultaneously an asset on someone else’s balance sheet. The sustainability of high government debt depends on who is willing and able to hold those bonds: domestic savers, foreign central banks, or the issuing country’s own central bank acting as buyer of last resort. When that willingness erodes, the repricing is sudden.

The debt cycle force connects directly to reserve currency dynamics, because the willingness of foreign central banks and institutional investors to absorb new government issuance depends heavily on confidence in the issuing currency, a confidence that erodes gradually and then, historically, very quickly.

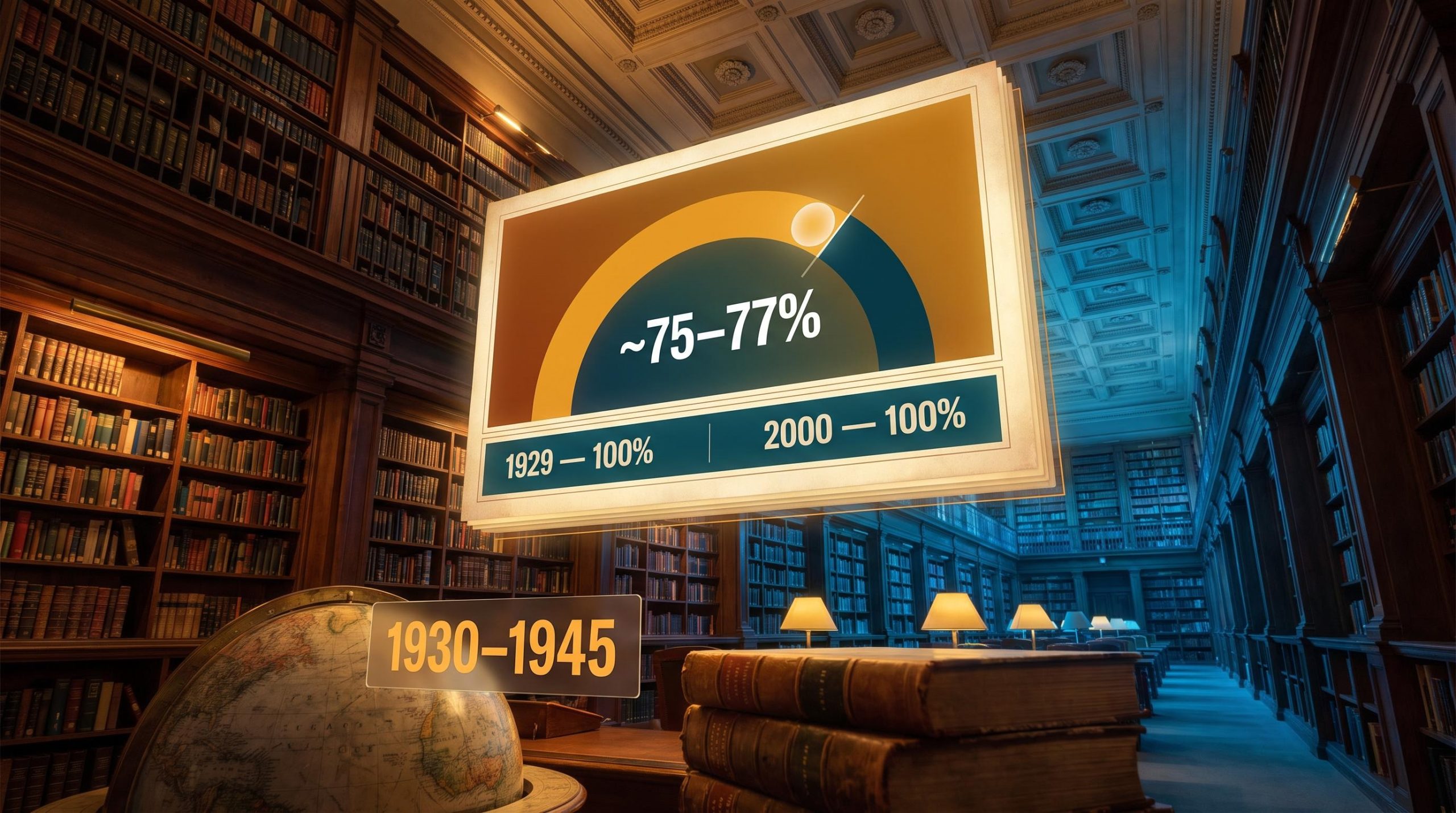

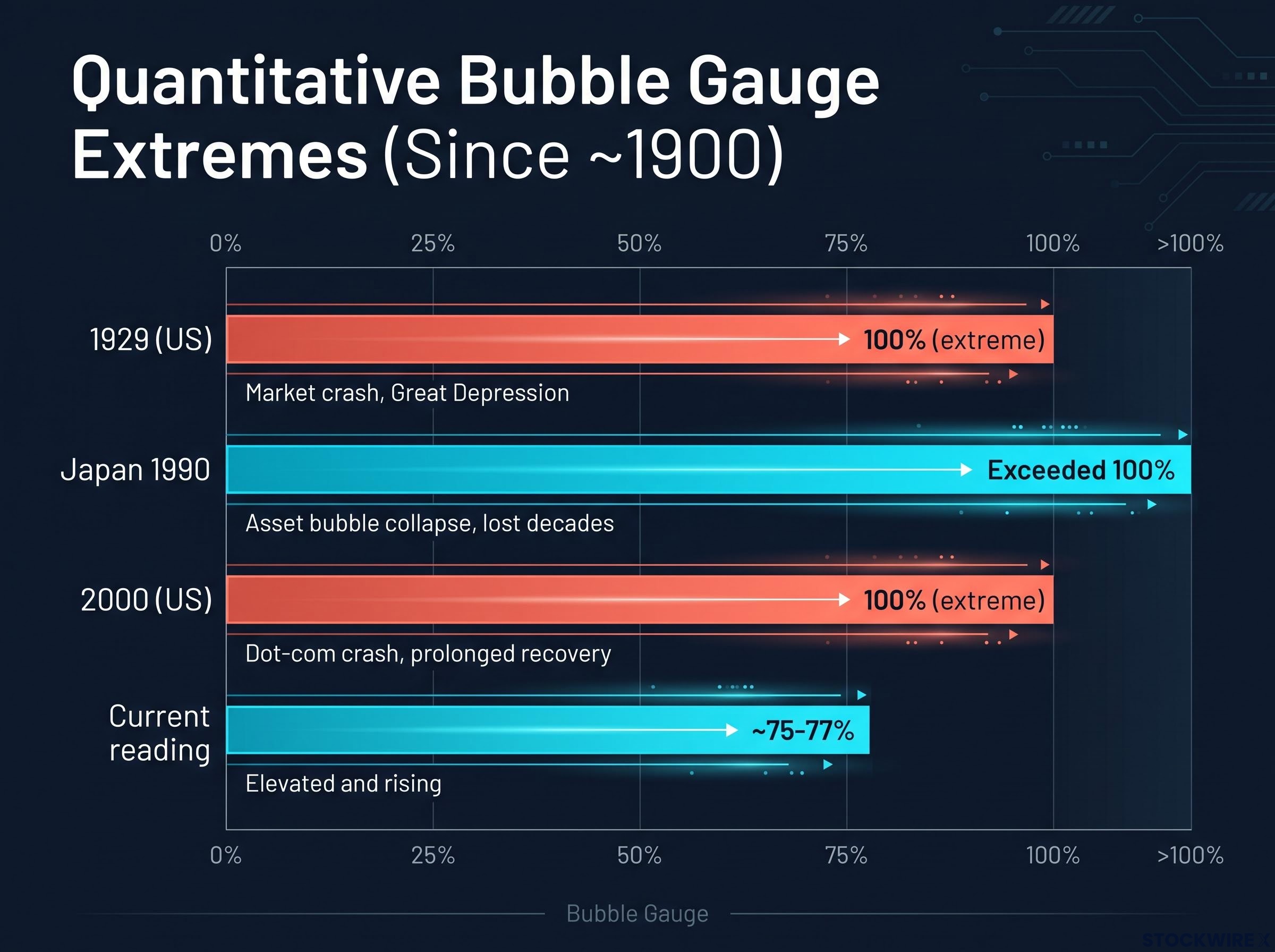

Dalio points to massive debt accumulation and late-cycle monetary conditions as dominant forces today, drawing an explicit comparison to the 1930-1945 and specifically the 1937-1938 period in terms of debt and monetary stress. His quantitative bubble gauge, which tracks valuations, debt-financed speculation, and interest-rate sensitivity across multiple countries dating back to approximately 1900, provides a concrete reading of where you stand right now.

The bubble gauge currently reads at approximately 75-77% of the extreme levels recorded in both 1929 and 2000, elevated and rising, but not yet at historic extremes.

| Era | Gauge Reading (Approximate) | Outcome |

|---|---|---|

| 1929 (US) | 100% (extreme) | Market crash, Great Depression |

| Japan 1990 | Exceeded 100% | Asset bubble collapse, lost decades |

| 2000 (US) | 100% (extreme) | Dot-com crash, prolonged recovery |

| Current reading | ~75-77% | Elevated and rising |

A reading at 75-77% of the 1929 and 2000 extremes does not mean a crash is imminent. What it tells you is that the buffer between current conditions and historically catastrophic levels is meaningfully narrower than it was a decade ago, and the gauge is trending higher, not plateauing.

External pressures: geopolitical shifts, environmental shocks, and technological frontiers

The remaining three forces operate on different timescales, but each imposes structural costs that interact with the debt and political dynamics already described.

Geopolitics: from cooperation to competition

The post-1945 international order, built by the United States and sustained through multilateral institutions, is breaking down. Dalio’s research shows that this is not a temporary disruption. With no shared framework governing how nations resolve their disputes, the breakdown of that order leaves only conflict as a mechanism for settling disagreements.

Rising tensions between the United States and China, the Russia-West conflict, and broader fragmentation of global trade and capital flows are all expressions of this force in its disruptive phase. For you, the implication is structural: supply chains, energy systems, technology standards, and even access to certain markets can be reshaped by power competition and sanctions. Geopolitical risk is no longer episodic. It is a permanent repricing of assumptions about how the global economy is wired.

Acts of nature: the underpriced force

Dalio’s historical research surfaces a finding that should recalibrate how you think about natural disasters as an investment risk: across the full sweep of recorded history, floods, droughts, and pandemics have collectively claimed more lives than armed conflict. These events have repeatedly triggered famines, migrations, fiscal crises, and political upheaval, yet they remain treated as low-probability tail risks in most economic models.

Climate change is the dominant current expression of this force, with costs to agriculture, infrastructure, insurance, and coastal real estate that are likely to be large and persistent. The COVID-19 pandemic demonstrated how unprepared systems were despite centuries of precedent. Both interact directly with debt, fiscal policy, and political stress, amplifying pressures that are already elevated.

Technology: disruption and the long-run tailwind

Across centuries, Dalio finds that human inventiveness is the most consistently positive force in the framework. It raises productivity, incomes, and life expectancy over the long run, even when its short-term effects are disruptive.

Dalio regards the current wave of artificial intelligence and advanced computing as ranking among the most transformative innovations in human history, with the potential to produce substantial productivity gains across the economy.

That optimism comes with a structural caveat. AI simultaneously risks exacerbating inequality by concentrating gains among those who own and deploy the technology, and it fuels a technology competition between nations that maps directly onto the geopolitical force. For your portfolio, technology is not just a sector allocation decision. It is a macro force that will reshape productivity, profit distribution, labour markets, and the balance of geopolitical power.

Technology competition between nations now extends well beyond AI model capability into export controls on semiconductors, state-funded research programs, and data localisation mandates that determine which companies capture sector returns based on jurisdictional positioning rather than technological lead alone.

Wealth gaps and social division: eroding the basis for compromise

The political force in Dalio’s framework is not about which side of a values debate is correct. It is about a mechanical constraint. Rising wealth inequality leads to political polarisation. Polarisation erodes institutional trust. Eroded trust reduces the set of feasible policy responses. Constrained policy options increase the probability of forced redistribution or capital controls.

- Rising income and wealth inequality leads to growing political polarisation

- Polarisation erodes trust in institutions and the capacity for compromise

- Eroded trust narrows the range of politically viable policy responses

- Constrained policy options raise the likelihood of capital controls, forced redistribution, or radical political change

Dalio characterises current levels of polarisation in the United States and parts of Europe as historically high, with wealth and values gaps reaching a point where, in his assessment, groups can no longer find common ground on which to compromise. He frames this as observation, not political commentary: when large groups view the system as fundamentally unfair, demands for radical change become structurally more likely regardless of which party holds power.

The Brookings Institution analysis of rising inequality documents the empirical trend behind Dalio’s political force, showing that wealth concentration in major economies has followed a trajectory that historically precedes the kind of institutional trust erosion and policy constraint his framework describes.

For you, this force explains why debt problems that look soluble in theory often are not in practice. A late-cycle debt burden that could theoretically be managed through a combination of higher taxes and lower spending becomes politically impossible when polarisation prevents the compromise needed to implement either. High polarisation is not a risk to monitor from a distance. It is a signal that the politically available options for managing economic stress are more constrained than in lower-polarisation periods.

The next major ASX story will hit our subscribers first

What the framework actually means for how you build a portfolio

Dalio’s five forces are not a trading system. They are a structural risk map. The goal is situational awareness, not prediction. Five practical implications follow:

- Extend your risk horizon. Assess your portfolio not just against next-quarter earnings or the next rate decision, but against scenarios consistent with late-stage debt cycles, regime changes, or geopolitical fracture, the kind of events that play out over years and decades.

- Monitor debt and valuation signals seriously. The bubble gauge, currently reading at approximately 75-77% of the 1929 and 2000 extremes and trending higher, gives you a concrete, quantifiable signal to track rather than an abstract warning about debt levels.

- Treat geopolitical fragmentation as structural. Position for a world of competing blocs, more sanctions, and less predictable access to markets and supply chains, rather than assuming a return to the hyper-globalisation of the 1990s and 2000s.

- Recognise technology as a macro force. Evaluate how AI and related technologies may alter productivity, profit shares, labour markets, and geopolitical balance, not just which individual stocks are “AI plays.”

- Diversify across systems, not only assets. Dalio emphasises diversification across countries, currencies, and types of exposures, because correlations spike when the big cycle turns and multiple forces hit simultaneously. Owning different asset classes within a single country and currency may not protect you when the systemic forces converge.

The question the framework should prompt is not “will this happen?” It is: is your portfolio robust to the range of outcomes this configuration of forces has historically produced?

What the five forces together are telling investors right now

Across all five forces, the current configuration is clear: debt is elevated and the bubble gauge is rising. Polarisation is at historically high levels in multiple major democracies. The geopolitical order is fragmenting with no mechanism to restore cooperation. Climate and pandemic costs are ongoing and interacting with fiscal stress. AI is delivering both productivity promise and structural disruption simultaneously.

What matters most is how all five forces interact as a combined system, not the behaviour of any one force viewed in isolation.

Dalio’s comparison to the 1930-1945 period rests on precisely this simultaneous activation. His conclusion is not a forecast of specific events. It is an assessment that this configuration has historically produced a wider range of negative outcomes than markets typically price, and that the cost of being unprepared is higher than it has been for most of the past three decades.

Applying this framework well means using it as a prompt to stress-test your holdings against scenarios that feel remote but have recurred throughout history. The events that reshape monetary systems, political orders, and geopolitical hierarchies are not hypothetical. They have happened before, repeatedly, under conditions that look uncomfortably familiar.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. The framework and gauge readings discussed reflect Ray Dalio’s stated positions and are subject to interpretation and revision as conditions evolve.