Why Short Squeezes Send Stocks Parabolic and Then Collapse

22 mins ago

South Korea is home to some of the world’s most consequential technology companies, yet most international investors have little clarity on how its two stock exchanges actually differ, or which one aligns with their portfolio objectives. Both the KOSPI and the KOSDAQ operate under the unified Korea Exchange (KRX), but they serve fundamentally different market segments. As interest in Asian equity markets continues to grow among internationally diversified investors, understanding the structural difference between these two boards is the first step toward a coherent Korean equity strategy. What follows is a practical breakdown of each exchange’s character, sector composition, and risk profile, the trading mechanics that govern both boards, a framework for building a workable allocation across them, and the foreign-specific risks that can quietly erode returns if left unaddressed.

The most common misconception about South Korean equities is that the KOSPI and KOSDAQ are competing exchanges. They are not. Both boards are administered by the Korea Exchange (KRX) and share identical trading infrastructure, settlement procedures, and regulatory standards. The same daily price limit of ±30% applies to all equities listed on either exchange. Trading hours are the same. Settlement rules are the same.

The distinction between KOSPI and KOSDAQ lies in the types of companies listed and their associated risk characteristics, not in regulatory quality or market integrity. They are complementary tiers within a single unified system.

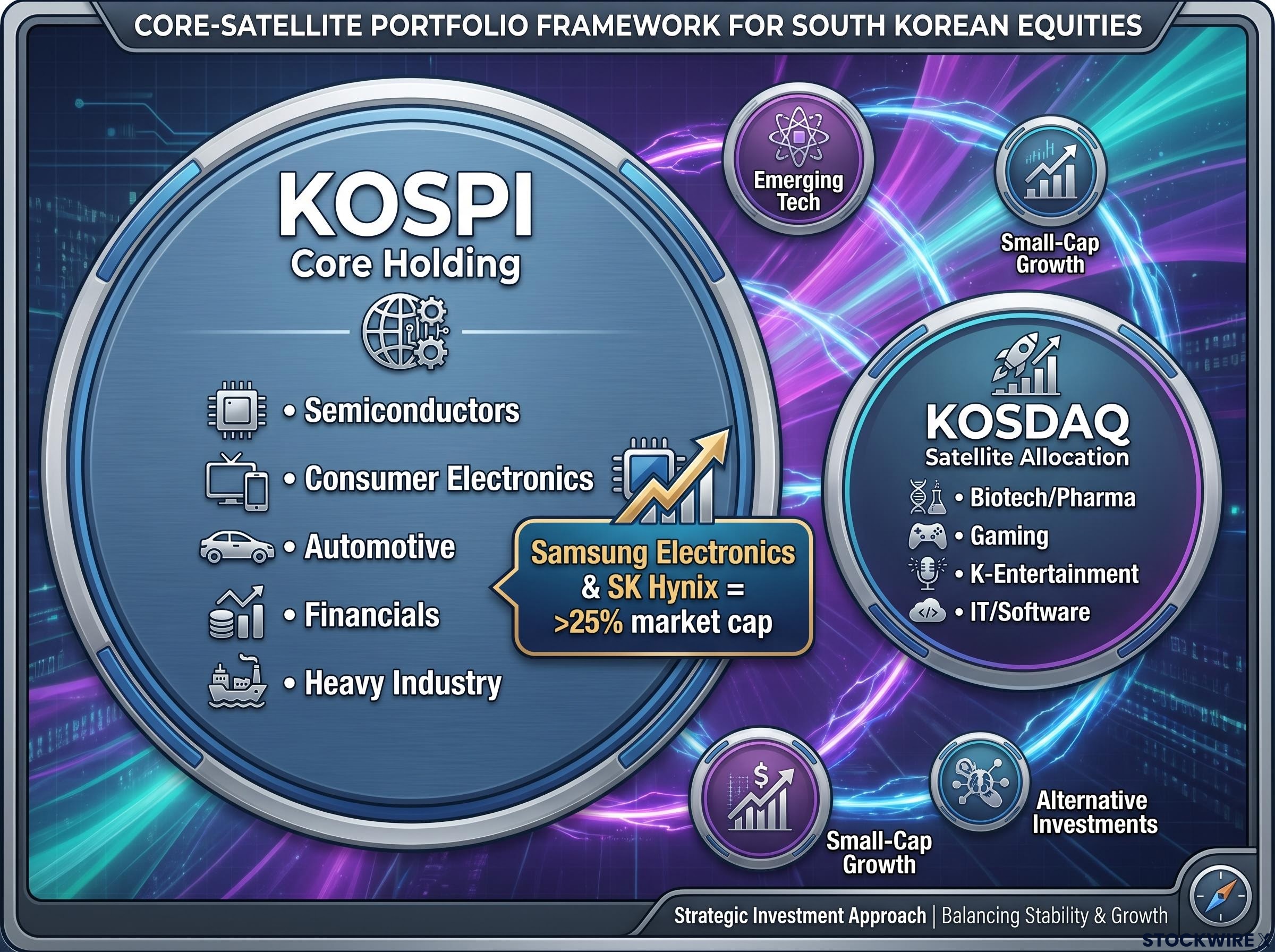

Where the two boards diverge is at the company level. The KOSPI lists South Korea’s largest, most established corporations. The KOSDAQ lists younger, higher-growth firms. Thinking of them as complementary tiers, rather than rival platforms, is the framing that leads to better allocation decisions. One is a core holding. The other is a satellite. Understanding why requires looking at each board’s composition in detail.

The KOSPI hosts South Korea’s most internationally recognised corporations, with heavy representation from chaebol affiliates spanning semiconductors, consumer electronics, automotive, financials, heavy industry, and materials. The composition reads like a roll call of South Korea’s industrial economy.

Samsung Electronics and SK Hynix together account for more than one-quarter of the KOSPI’s aggregate market capitalisation, a weighting that fluctuates with sector performance but consistently ties index-level returns to the global memory and semiconductor cycle.

That concentration has practical implications. Investors who already hold global technology exchange-traded funds (ETFs) with significant semiconductor exposure may find that adding broad KOSPI index positions doubles down on a sector bet rather than diversifying away from it. Evaluating existing portfolio overlap is a necessary step before sizing a KOSPI allocation.

KOSPI index concentration amplifies this dynamic in a specific way: because Samsung Electronics and SK Hynix together have represented well over 40% of the benchmark’s total market capitalisation, a sell-off in either name can transmit as a broad market decline through passive ETF redemption mechanics, even when the rest of the index is unchanged.

High daily trading volumes in large-cap KOSPI equities allow investors to enter and exit positions at more predictable price levels. For those transacting in meaningful size, this liquidity profile distinguishes the KOSPI sharply from the KOSDAQ.

| Sector | Representative Company Type | Portfolio Role |

|---|---|---|

| Semiconductors | Memory and chip fabrication conglomerates | Core growth and cyclical exposure |

| Consumer Electronics | Global device and display manufacturers | Diversified consumer demand proxy |

| Automotive | Vehicle and EV component manufacturers | Industrial and mobility cycle exposure |

| Financials | Banks and insurance groups | Domestic economic indicator |

| Heavy Industry / Materials | Shipbuilding, steel, and chemicals producers | Commodity cycle and infrastructure proxy |

Where the KOSPI is stability and scale, the KOSDAQ is opportunity and volatility. The exchange is built around younger, higher-growth companies operating in sectors where South Korea holds a notable global competitive position:

These are firms more dependent on future earnings potential and narrative than on current profitability. The KOSDAQ’s sector mix reflects South Korea’s innovation economy, offering international investors exposure to growth themes that have few equivalents on other Asian exchanges.

That exposure comes with a different risk character. KOSDAQ-listed firms are more likely to experience sharp, binary price moves. Biotech names in particular can swing dramatically on clinical trial outcomes or regulatory decisions, making event-driven volatility a defining feature of the board rather than an occasional disruption.

The KOSDAQ’s role in a Korean equity strategy is best understood as a satellite allocation: selective, thesis-driven, and sized with discipline.

Thinner order books on the KOSDAQ mean that available buy and sell orders at any given price are more limited than on the KOSPI. For investors transacting in larger quantities, this creates a practical risk: entering or exiting a position can itself move the price.

Verifying average daily trading volume before sizing a position is not optional on the KOSDAQ. It is the basic precondition for managing execution risk, particularly in biotech and smaller software names where liquidity can thin further during periods of low market activity.

Three operational details define how Korean equity markets function day to day:

The KRX guide to trading in the Korean stock market sets out the official rules governing price limits, settlement procedures, and circuit breaker thresholds that apply uniformly across both the KOSPI and KOSDAQ boards, providing international investors with the primary regulatory reference for understanding how the unified exchange infrastructure operates in practice.

The ±30% daily price limit has no direct equivalent in US or European equity markets. Setting stop-loss parameters and interpreting intraday price behaviour on Korean equities requires adjusting for this structural feature.

For international investors accustomed to markets where single-session moves are theoretically uncapped, the ±30% limit changes the mechanics of risk management. A stock hitting the limit does not necessarily mean the move is complete; it may gap further at the following session’s open.

Choosing between the KOSPI and KOSDAQ is only part of the decision. Three categories of risk sit outside the exchange comparison itself but can dominate actual return outcomes for foreign investors:

| Risk Type | Description | What to Do About It |

|---|---|---|

| Currency (KRW) | KRW movements relative to USD, EUR, or SGD can dominate total equity returns over shorter horizons | Assess KRW exposure explicitly; consider hedged ETFs or currency overlay strategies where available |

| Withholding Tax | Korean withholding tax on dividends reduces total returns for foreign investors; rate varies by domicile and tax treaty | Review applicable double taxation agreements; factor net-of-tax yield into income projections |

| Regulatory / Policy | Changes to short-selling rules and retail-protection measures can affect liquidity and pricing, particularly on the KOSDAQ | Monitor KRX regulatory announcements; maintain flexibility in position sizing and exit timelines |

These risks are invisible in a side-by-side exchange comparison but can be the most consequential factors in actual portfolio outcomes.

Geopolitical supply shocks represent a fourth category of foreign investor risk that sits outside the exchange-selection framework entirely: South Korea routes over 90% of its crude oil imports through the Strait of Hormuz, meaning a Middle East disruption can transmit directly into semiconductor manufacturing costs and KOSPI index returns even when the triggering event has no Korean dimension whatsoever.

The KOSPI and KOSDAQ are not a binary choice. Investors can, and in many cases should, engage with both boards concurrently within the same portfolio. The question is how to weight them.

The core-satellite framework offers a practical structure: allocate the majority of Korean equity holdings to the KOSPI as a liquid, large-cap core, while reserving a smaller allocation for targeted KOSDAQ positions based on specific sector views in areas such as biotechnology, gaming, or entertainment. This approach captures the stability and liquidity of the blue-chip tier while allowing selective exposure to South Korea’s growth economy.

| Dimension | KOSPI | KOSDAQ |

|---|---|---|

| Company profile | Large, established blue-chips; chaebol affiliates | Smaller, younger, growth-oriented firms |

| Sector tilt | Semiconductors, consumer electronics, automotive, financials, heavy industry | Biotech/pharma, gaming, K-entertainment, IT/software |

| Liquidity | High; deep order books; suitable for larger positions | Lower; thinner order books; position sizing more critical |

| Volatility | Moderate; index heavily influenced by Samsung and SK Hynix | Higher; significant event-driven risk, especially in biotech |

| Portfolio role | Core holding; stable, broad South Korean economic exposure | Satellite allocation; selective, thesis-driven positions |

| Suitable investor profile | Lower risk tolerance; institutional and broad-market investors | Higher risk tolerance; growth-oriented, sector-specific investors |

Three practical access routes are available, listed in order of increasing directness:

Each access method involves different cost structures, tax treatment implications, and tracking characteristics. Evaluating these against individual circumstances and local regulations is a necessary step before committing capital.

Institutional risk management on KOSPI positions after a sustained rally introduces considerations that go beyond the structural allocation framework: record retail margin debt, overbought signals on a relative-strength basis, and the mechanics of forced selling can interact to produce drawdowns that exceed what fundamentals alone would predict, making position-size discipline as important as initial entry logic.

The KOSPI and KOSDAQ are not competing choices. They are complementary tiers within the same unified Korea Exchange, and the most coherent approach for international investors uses both. The KOSPI provides stable, liquid exposure to South Korea’s established industrial economy. The KOSDAQ provides selective access to its innovation and growth sectors. A core-satellite framework, with the majority of Korean equity holdings in the KOSPI and targeted allocations to KOSDAQ names driven by specific sector conviction, captures the strengths of each board.

As Korean equities continue attracting international capital across semiconductors, biotech, and entertainment, understanding both boards is foundational for any investor seeking a structured approach to one of Asia’s most consequential equity markets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The KOSPI lists South Korea's largest, most established corporations across semiconductors, automotive, and financials, while the KOSDAQ focuses on younger, higher-growth firms in biotechnology, gaming, and K-entertainment. Both boards are administered by the same Korea Exchange (KRX) and share identical trading infrastructure, settlement procedures, and regulatory standards.

Yes, both the KOSPI and KOSDAQ operate under the unified Korea Exchange (KRX) and share the same trading infrastructure, settlement rules, and daily price limits. The distinction lies in the types of companies listed, not in regulatory quality or market integrity.

The Korea Exchange enforces a maximum daily price fluctuation of plus or minus 30% for all equities listed on both the KOSPI and KOSDAQ. This hard cap applies equally to both boards and functions as a built-in circuit breaker to prevent extreme single-session price swings.

International investors can access Korean equities through three main routes: country or sector ETFs focused on KRX constituents, ADRs and GDRs for select major KOSPI names, or direct broker access through international brokers with KRX market connectivity. Each method carries different cost structures, tax treatment implications, and tracking characteristics.

Foreign investors face KRW currency volatility that can materially reduce or even negate equity gains when converting returns back to their home currency. Additionally, Korean withholding tax applies to dividends received from Korean-listed equities, with the applicable rate varying by investor domicile and the terms of any double taxation agreement with South Korea.